Summary

The purpose of this webpage is to assist vendors/tax practitioners to complete the Value-Added Tax (VAT201) return accurately and honestly. Included this guide are the steps to on how to request, complete and submit the VAT201 return and make payments.

Introduction

The South African Revenue Service (SARS) has been modernising and simplifying tax processes in line with international best practice. Improvements are being made continuously as we aim to better our service standards, increase efficiency and compliance.

One of the aspects of compliance that SARS wishes to address is the VAT201 Return and payment of VAT.

The following changes have been applied in previous years:

- Changes to the VAT201 Return aimed not only at improving its systems, but also at addressing SARS’s efficiency regarding risk assessment and tax compliance.

- A new VAT201 Return in landscape format has been introduced. It contains the same fields as the previous VAT201 Return but with the following additional fields:

- Demographic information,

- The declarant’s signature.

- A Payment Reference Number (PRN) which will be pre-populated by SARS will replace the previous “reference number”.

The current environment used to administer the claims of Diesel refunds makes provision for four concession types, namely On Land, Offshore and Rail, Peak Power Plants and Electricity Generators. The rates contained therein are used by vendors to convert the diesel litre usage to rands, and to calculate the refund due based on the relevant rate. The form auto calculates, the vendor only declares their litres.

Effective 1 April 2018, the VAT rate increased from 14% to 15%.

A functionality has been enabled on eFiling for a VAT vendor to view the VAT filing control table for a 12-month period. This is available to registered VAT vendors with an active eFiling profile.

- Note: The “VAT Filing Control Table” and “VAT Control Table” references in this document are the same and will be used interchangeably.

Enhancements to the VAT system include the following:

- Display the Estimated VAT 201 return on eFiling.

- Vendors will be able to submit relevant material from the VAT217 and VAT201 work page on eFiling.

- Vendors will be able to request an extension for a period to submit relevant material or returns.

- A vendor must not be able to dispute a Section 95(1)(c) estimate or an estimate due to no submission of a return; but must be allowed to request a Suspension of Payment using the existing process.

Requesting the VAT201 Return (Original or Revision where Previously Filed)

- A vendor will be allowed to:

- View the VAT filing control table;

- Request a VAT201 Return for the current tax period and the tax period following the current period; and

- Request a VAT201 Return for a past tax period.

- The following channels may be used by a vendor to request a VAT201 Return:

- eFiling; or

- Contact Centre; or

- Request at a SARS office.

- All vendors should make an appointment on the SARS website before visiting the SARS office.

- eFiling

- If a vendor wishes to use the eFiling channel, the vendor must be registered as an eFiler;

- The Payment Reference Number (PRN) will be pre-populated on the return.

- Vendors are encouraged to register for eFiling, as eFiling will enable timesaving, hassle-free submission of VAT201 returns and payments. Vendors who submit their VAT201 returns manually must do so by the 25th of the month, while vendors who use eFiling have until the last business day of the month to submit VAT201 returns and payments. eFiling therefore affords the vendor additional days for submissions and payments. This represents a significant financial advantage. You can register for eFiling at www.sarsefiling.co.za.

- SARS Office:

- When a vendor request the VAT201 Return in person at a SARS office, the agent will request the requestor to provide the following details:

- The business’ trading name;

- Name and surname of the requester;

- The VAT registration number;

- The tax period for which the return will be made;

- Business postal address;

- Customs code (if applicable).

- When a vendor request the VAT201 Return in person at a SARS office, the agent will request the requestor to provide the following details:

- Vendors can both request and submit their VAT201 Return at a SARS office. When a vendor chooses to follow this option, the vendor must be in possession of and furnish all the amounts to be entered on the relevant fields in the VAT201 Return.

- SARS officials will not be able to assist by analysing the vendor’s financial data and calculating the amounts to be entered in the relevant fields of the VAT201 Return. The vendor/representative will have to be present to sign the completed VAT201 Return to authorise the submission at the SARS office.

- Note: Copies of the VAT201 Returns printed from eFiling and used for manual filing will not be accepted and will not be processed by SARS. Photocopies will also not be accepted.

Registering on eFiling for VAT Purposes

- A vendor has to be registered as an eFiler to be able to submit VAT201 returns and make VAT payments via eFiling. This applies to:

- Individuals;

- Tax practitioners;

- Organisations (e.g. Companies, Close Corporations, Trusts and Exempt Institutions).

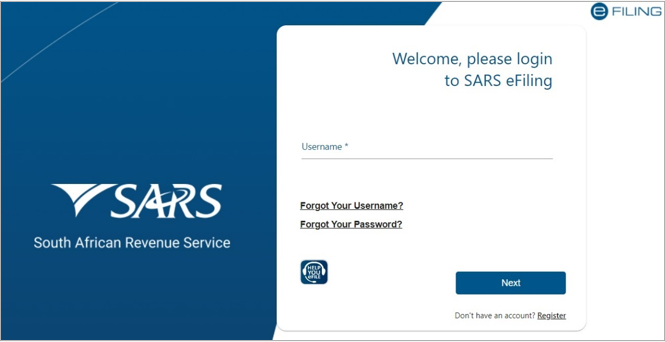

- Navigate to www.sars.gov.za and click “Login”.

- Enter your username and click the “Next” button to enter the password.

- If you have forgotten your Username and/or Password, click on the “Forgot Your Username?” or “Forgot Your Password” hyperlinks.

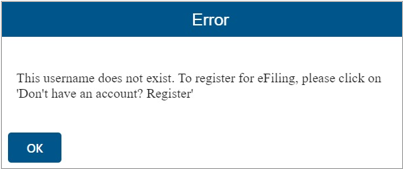

- If the username entered is incorrect, the following error message will be displayed.

- Note: If the login and password details are incorrect, an error message will be displayed on the screen for the user.

- For further assistance with eFiling registration or profile management, refer to the “How to register for eFiling and manage your user profile” available on the SARS website www.sars.gov.za.

Activation of Tax Type

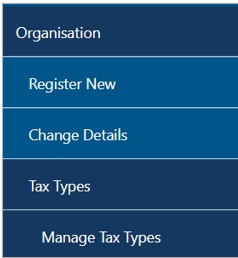

- If you are already registered on eFiling and wish to activate VAT on eFiling to submit VAT201 Returns and make payments follow the steps below.

- Once logged into eFiling, select “Organisation”, “Tax Types” and “Manage Tax Types” from the side menu options under ORGANISATIONS.

- Select the “Activate” tick box to activate the VAT tax type on eFiling and click the Submit button to proceed.

- Once the tax type has been activated, the status will be displayed as “Successfully Activated”.

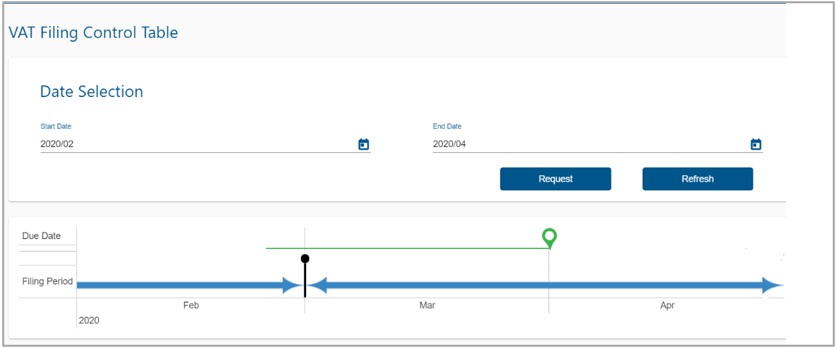

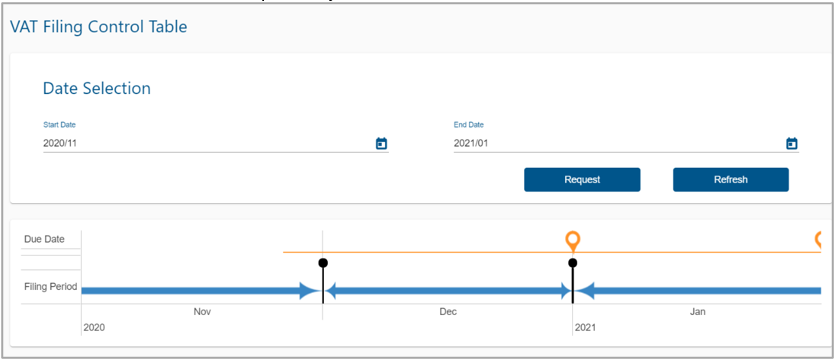

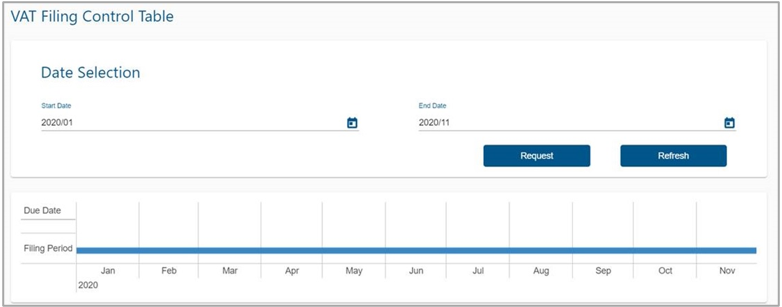

View VAT Filing Control Table

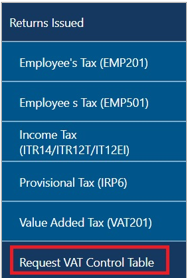

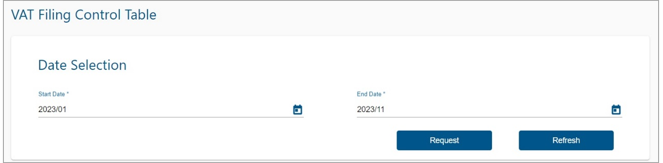

- To view the VAT filing control table:

- Select “Returns”, then “Returns Issued” and “Request VAT Control Table”.

- The VAT control table landing page will be displayed.

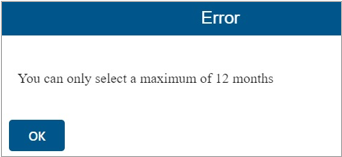

- Enter a “Start” and “End” date range, a maximum of 12 months is allowed, and click “Request”.

- Error message will be displayed if the date range is incorrect. Click “OK” on the message to clear it.

- Enter a “Start” and “End” date range, a maximum of 12 months is allowed, and click “Request”.

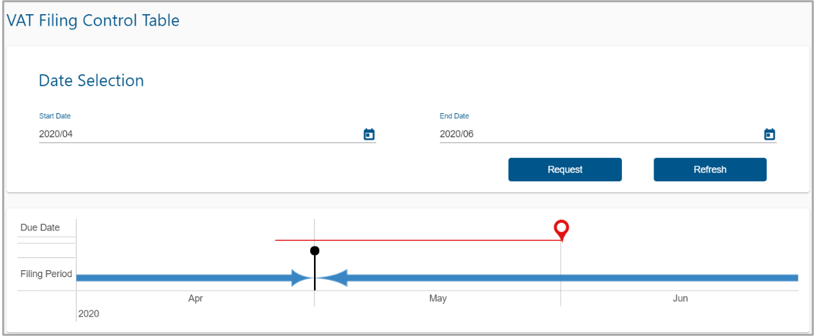

- The data for the selected date range will be displayed:

- If a “No Results” error message displays and the selected date range falls within the liability date, click the “Refresh” button to obtain the most recent information from SARS.

- Select the “Refresh” button if the vendor made a change to the category on registration or requested deregistration.

- The data for the selected date range will be displayed:

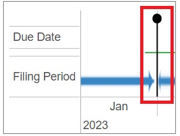

- The period breaker indicated by the black line between the months is placed after each tax period where a return is required.

- Example: If the January return is required, period breaker will be placed after February tax period. The due date ribbon will be placed in February (Return due date for January is in February).

- The below ribbons indicate the returns due date and their statuses:

- The RED indicator: “Return is outstanding and overdue”. For example, the return for the tax period ending April is outstanding and overdue.

- The Green indicator: “Return was received”. For example, the return for tax period ending February was received by the due date in March.

- The Orange ribbon indicator: “Return is required”. For example, the return for tax period ending November is required by the due date in December.

- The Blue ribbon indicator: “Return not required”.

Requesting a VAT201 Return on eFiling

- Note: A vendor will be able to request the VAT201 Return immediately after the VAT tax type has successfully been activated.

- A vendor will be allowed to:

- Request a VAT201 Return for the current tax period and the tax period following current tax period, and

- Request and submit a VAT201 Return for a past tax period.

- Select “Returns”, then “Returns Issued” and “Value Added Tax (VAT201)” to request the VAT201 return.

- The following steps must be completed to request the VAT201 Return. Select the required period and the “Request Return” button.

- If you are not required to submit for a Return specified tax period, the following error message will be displayed. Ensure that the correct tax periods are selected for the VAT201 Return to be generated for completion.

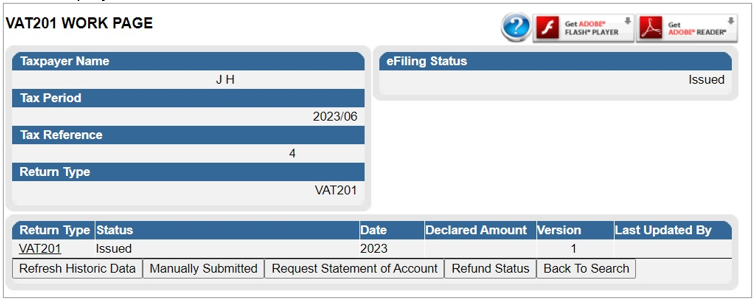

- Once you have selected the required return and it is generated, the VAT201 Work Page will be displayed.

- By clicking on the VAT201 link you will be presented with an editable return for the selected tax period. The VAT201 will be displayed in HTML format. Ensure that you have a compatible browser to view the VAT201 return.

- If you have already submitted the return at a SARS office, select the “Manually Submitted” option to update the eFiling return status.

- Note: If a timeout occurs while in the process of requesting a VAT201 Return, eFiling will display the following message: “Your return could not be issued at this time, please try again later”.

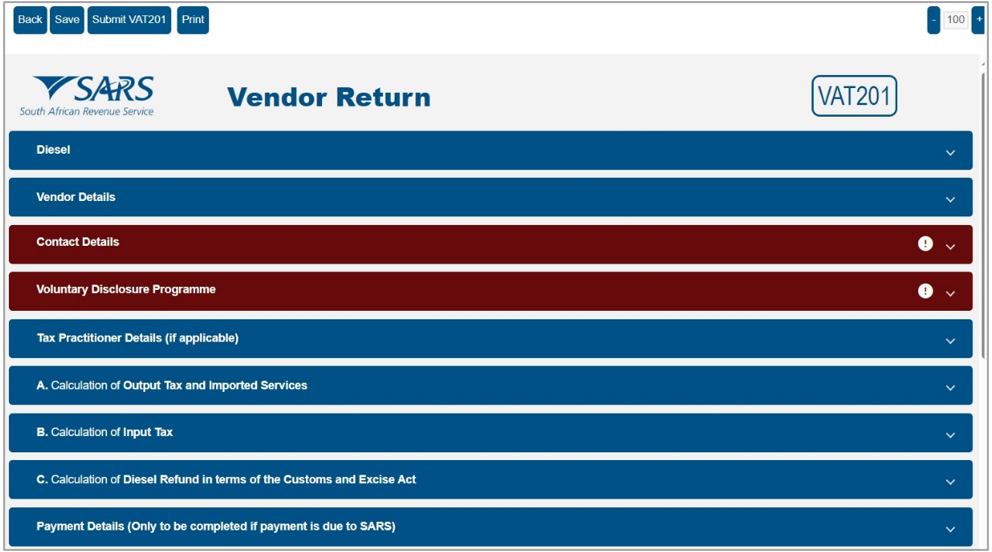

- The Vendor Return (VAT201) will be displayed for completion.

- Container headings displayed in red contain mandatory information to be completed.

- Mandatory fields in the containers are indicated as below:

- Once you have completed a field, it will be displayed in green as per the example below:

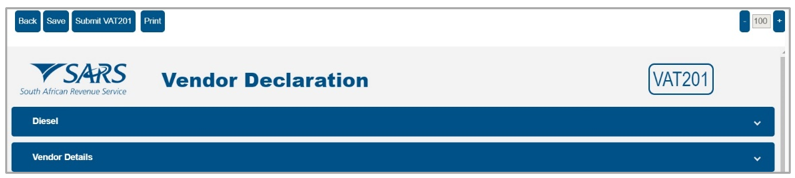

- On the toolbar, the following tabs will be available for selection.

- If you select the “Back” button, the return will be saved and the VAT201 Work Page will be displayed.

- The “Save” button will allow you to save the return and you can submit at a later stage.

- The “Submit VAT201” button will allow you to submit the VAT201 Return to SARS.

- The “Print” button will allow you to print the return.

- On the far-right hand side of the screen the zoom buttons are indicated to reduce or increase the display size of the return.

Completing the VAT201 Return

- Complete all the relevant information that is required for the processing of the VAT201 Return.

- The following fields will be pre-populated with the information at the disposal of SARS:

- Trading or Other Name;

- VAT Registration Number;

- Tax period for which the return is to be submitted;

- Payment Reference Number (PRN);

- Diesel Rates to be applied for the applicable year in which the indicated tax period falls and according to the type of diesel activity for which the vendor is registered.

- Vendors whose tax periods span between the old VAT rate of 14% and the new VAT rate of 15% (effective from 1 April 2018) will be required to declare these transactions on a single VAT201 return.

- The most impacted will be the Category B vendors whose tax periods are periods of two months ending on the last day of April 2018.

- Also impacted are the Category D vendors whose tax periods are periods of six months ending on the last day of August 2018. Category E vendors whose tax periods are periods of twelve months ending on the last day of the year of assessment will also be impacted.

- Vendors who have tax periods that span between the 14% and 15% VAT rate (Category B, D and E vendors) as well as future tax periods where the rate of 14% is applicable will be required to disclose their transactions on the VAT201 as follows:

- Output Tax

- For all standard rated supplies where VAT at 15% has been levied, vendors will use the fields that are normally used to declare the output tax.

- For all standard rated supplies where VAT at 14% has been levied, vendors must declare the output tax in field 12 – “Other and Imported Services” on the VAT201.

- Input tax

- For all acquisitions of goods and services charged with VAT at a rate of 15%, vendors must use fields 14 and 15 on the VAT 201 (as applicable) to deduct the input tax.

- For all acquisitions of goods and services where VAT rate of 14% is applicable, vendors are requested to use field 18 –“Other” of the VAT201, to deduct the input tax; and

- For all imports, irrespective of whether the VAT was charged at 14% or 15%, vendors are requested to use Field 14A and 15A of the VAT201 to deduct the input tax.

- For revising the original/previous submission of a VAT201 Return for any tax period, the following fields will be pre-populated:

- Trading or Other Name;

- VAT Registration Number;

- Tax period for which the Return is to be made;

- The same Payment Reference Number (PRN) as in the original VAT201 Return;

- Diesel Rates to be applied for the applicable year in which the indicated tax period falls and according to the type of diesel activity for which the vendor is registered.

- Financial data from the original/previous VAT201 Return submitted. (For tax periods prior to the implementation of the new VAT201 Return, the financial data will not be pre-populated)

- Contact details of the person who completed the original/previous submission of the VAT201 Return for the tax period concerned.

- The vendor will not be able to edit any of the fields listed above, except for the contact details of the person who completed the original/previous submission of the VAT201 Return.

- For a VAT201 Return that has already submitted but requires a revision and which is posted to vendors, all the pre-populated fields will be printed in black ink, with the exception of the financial data and the contact details from the original/previous VAT201 Return which will be printed in pink ink. This will allow the vendor to write over the pink ink in black or blue ink. Any pre-populated amount that is not overwritten in black or blue ink will be processed unchanged in the relevant field. If the revision is for a tax period prior to the last two years, the diesel portion of the VAT201 Return will be printed in black ink.

Diesel

- Note: The selection of Diesel rebate type can be made if the vendor is registered for a Diesel refund.

- On Land

- The farming, forestry and mining industries will qualify for this refund.

- Offshore

- Commercial fishing, coastal shipping, offshore mining and the National Sea Rescue Institute will qualify for this refund.

- Rail and Harbour Services

- Rail freight hauliers and specific harbour service operators will qualify for this refund.

- Peak Power Plant

- If a vendor is not registered for the “Peak Power Plant” concession, the vendor will not be able to select this option.

- Peak power plant will qualify for this refund.

- Note: These options “boxes” are not selectable, they are prepopulated based on your activity code.

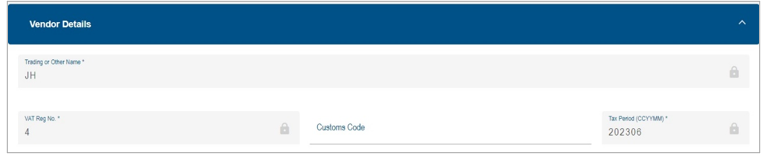

- Note: The vendor’s details must be completed if all the fields have not been pre-populated.

- Trading or Other Name

- The trading name is the name under which your business trades. It is also the name known by your suppliers or your customers and it may be different from your business’ legal name. This field is pre-populated. If the trading name or other name has changed, you are required to inform SARS in writing.

- VAT Registration Number

- The VAT registration number is the 10-digit number allocated by SARS to a registered vendor. This field is pre-populated.

- Customs Code

- The Customs Code is a number allocated to exporters/ importers. The vendor must complete the Customs Code field if fields 2A, 14A or 15A (or any combination thereof) are completed.

- Tax Period (CCYYMM)

- This is the period for which the VAT201 Return must be submitted, and it depends on the return and payment category under which the vendor is registered. This field will be pre-populated.

Contact Details

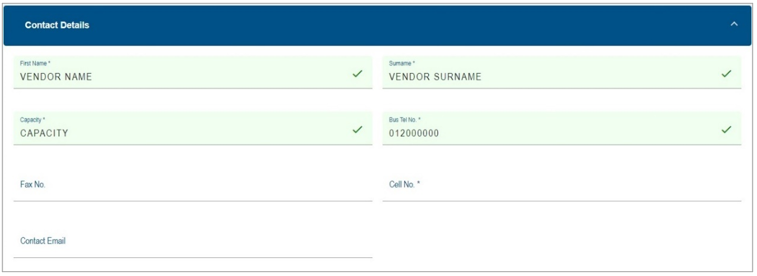

- The vendor must complete the demographic information of the person responsible for completing the VAT201 Return. The following fields will be displayed for completion.

- First Name

- The name of the person responsible for completing the VAT201 Return.

- Surname

- The surname of the person responsible for completing the VAT201 Return.

- Capacity

- The capacity of the person responsible for completing the VAT201 Return.

- Either the business telephone or cell phone number must be provided. The business telephone number must commence with the relevant area code. If the business number is not provided, the cell phone number is mandatory.

- Business Telephone Number

- The business telephone number of the person responsible for completing the VAT201 Return.

- Fax Number

- This is an optional field and may be completed. The fax number of the person responsible for completing the VAT201 Return.

- Cell phone Number

- The cellular telephone number of the person responsible for completing the VAT201 Return.

- Contact Email

- This is an optional field and may be completed. Provide the email address of the person responsible for completing the VAT201 Return.

Voluntary Disclosure Programme (VDP)

- What is the purpose of VDP?

- VDP seeks to:

- Give applicants an opportunity to come clean by disclosing their tax defaults and/or exchange control contraventions and obtain relief if successful.

- Establish a process within which the application criteria is transparent and relief parameters clearly prescribed

- Enhance the culture of compliance in both the tax and exchange control environments.

- VDP seeks to:

- Once the VDP application has been evaluated by the VDP Unit, a written agreement will be concluded between you and SARS to effect the necessary assessments.

- Should you require more information, a Comprehensive Guide concerning VDP is available on the SARS website www.sars.gov.za.

- Where an approved VDP agreement exists between the vendor and SARS, the following information must be completed.

- Is this declaration made in respect of a VDP agreement with SARS?

- Make sure that an “X” is inserted in the “Y” box.

- VDP application number

- The VDP application number as found on the VDP agreement must be completed.

- This is a mandatory field if the “Y” block is selected.

- Note: When completing the remainder of the return, do not forget to include all amounts applicable for the tax year for which VDP was granted, including the previously omitted information.

Tax Practitioner Details (If applicable)

- Note: This section should only be completed if a tax practitioner is completing the VAT201 Return.

- Tax Practitioner Registration No.

- Complete the tax practitioner registration number.

- Tax Practitioner’s Tel No

- Complete the contact number for the tax practitioner.

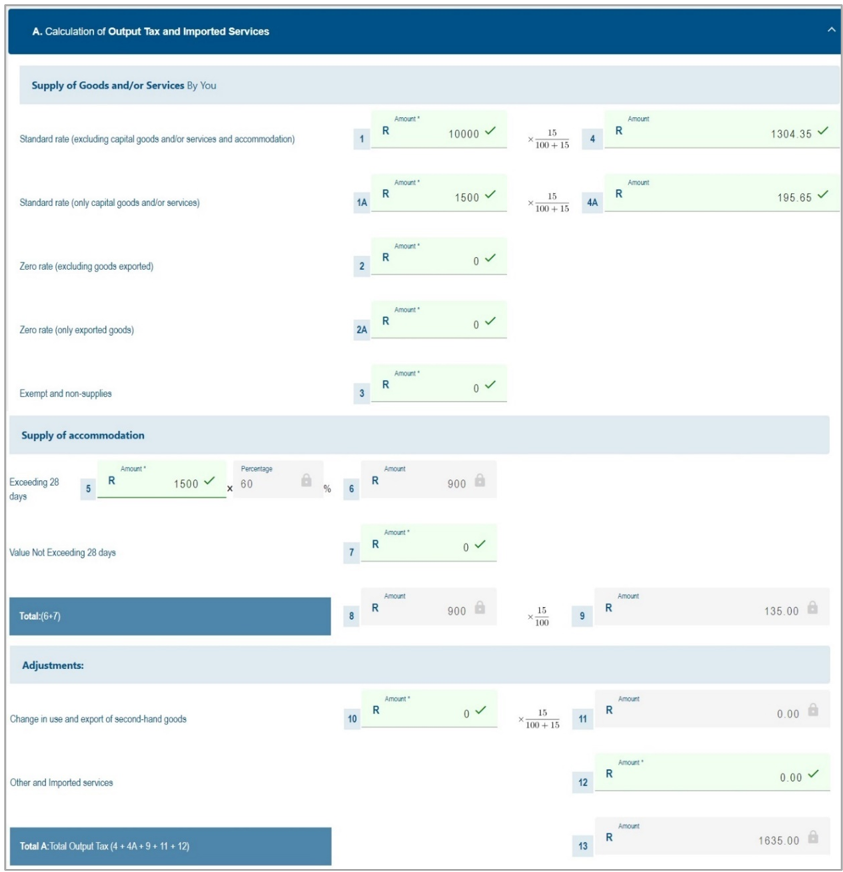

Calculation of Output Tax and Imported Services

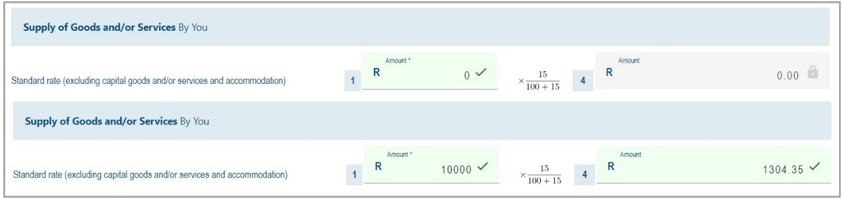

- The green fields are editable, and the greyed-out fields are fields that will be auto calculated as indicated in the below example of field 1.

- Field 1 – Standard rate (excluding capital goods and/or services and accommodation)

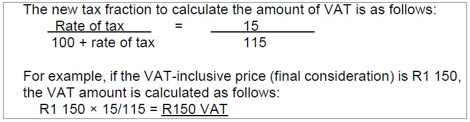

- The new tax fraction applicable from 1 April 2018 is set out below:

- Effect of VAT rate increase on VAT vendors.

- Vendors need to make all necessary changes and adjustments to their business systems, including tax invoices to ensure that VAT at the rate of 15% is levied on all goods and services supplied, where those supplies qualify to be charged with VAT at the new rate of 15%.

- Vendors should determine when supplies of goods and services are deemed to have taken place and also consider the special rules that apply when there is a change in the VAT rate to ensure that the correct rate of VAT is applied in respect of the supply, the acquisition and importation of goods and services.

- Examples of standard rated supplies (sales) are:

- Aircraft fuel;

- Building materials and services;

- Books and newspapers;

- Cigarettes, cold drinks and liquor;

- Clothing;

- Electricity, water and refuse removal;

- Entrance fees to sporting events;

- Furniture;

- Hotel accommodation;

- Lawyer’s services;

- Local air travel;

- Meat and any food served as a meal;

- Medicines;

- Medical services (other than by State hospitals);

- Motor repairs;

- Motor vehicles and spares;

- Paraffin (excluding illuminating kerosene);

- Postage stamps;

- Restaurant services;

- Telephone services;

- Transport of goods(local);

- Washing powder;

- White bread.

- Effect of VAT rate increase on VAT vendors

- Vendors need to make all necessary changes and adjustments to their business systems, including tax invoices to ensure that VAT at the rate of 15% is levied on all goods and services supplied, where those supplies qualify to be charged with VAT at the new rate of 15%.

- Vendors should determine when supplies of goods and services are deemed to have taken place and also consider the special rules that apply when there is a change in the VAT rate to ensure that the correct rate of VAT is applied in respect of the supply, the acquisition and importation of goods and services.

- Field 1A – Standard rate (only capital goods and/or services)

- The VAT inclusive amount of goods and/or services supplied by you at the standard rate, only capital goods and/or services must be completed in Field 1A. This field must reflect the consideration received (VAT included) in respect of:

- Sale of capital goods and/or services (e.g. Sale of land and buildings, plant and machinery, intellectual property).

- VAT on assets upon termination of registration.

- The VAT inclusive amount of goods and/or services supplied by you at the standard rate, only capital goods and/or services must be completed in Field 1A. This field must reflect the consideration received (VAT included) in respect of:

- Field 2 – Zero rate (excluding goods exported)

- The amount of goods and/or services supplied by you at zero rate, excluding exported goods, must be completed in Field 2. Zero rated supplies are taxable supplies, taxed at a rate of 0%. Examples of zero-rated supplies are:

- Brown bread;

- Eggs of domesticated chickens;

- Edible legumes and pulses of leguminous plants;

- Fresh/frozen fruit and vegetables;

- Dried beans;

- Illuminating kerosene;

- Lentils;

- Maize meal;

- Milk, cultured milk, milk powder and dairy powder blend;

- Pilchards/ sardines in tins or cans;

- Vegetable oil excluding olive oil;

- Fuel levy goods (e.g. petrol and diesel);

- The sale of a business or part of a business as a going concern;

- Services supplied in respect of goods temporarily admitted into the RSA from an export country for the purposes of being repaired or serviced.

- International travel.

- The amount of goods and/or services supplied by you at zero rate, excluding exported goods, must be completed in Field 2. Zero rated supplies are taxable supplies, taxed at a rate of 0%. Examples of zero-rated supplies are:

- Field 2A – Zero rate (only exported goods)

- The amount of goods supplied by you at the zero rate which has been exported from the RSA must be completed in Field 2A. The Customs Code field is mandatory, if Field 2A is completed.

- Field 3 – Exempt and non-supplies

- The amount of exempt supplies or non-supplies supplied by you must be completed in Field 3. No output tax is levied in respect of exempt supplies and no input tax relating to the expenditure on these supplies may be deducted. The following are examples of exempt supplies:

- Financial services;

- Donated goods or services by an association not for gain;

- Residential accommodation;

- The letting of leasehold land;

- The sale or letting of land situated outside the Republic;

- Transport of fare-paying passengers by road or railway;

- The supply of educational services;

- Membership contributions to employee organisations, such as trade unions;

- The supply of childcare services.

- The amount of exempt supplies or non-supplies supplied by you must be completed in Field 3. No output tax is levied in respect of exempt supplies and no input tax relating to the expenditure on these supplies may be deducted. The following are examples of exempt supplies:

- Field 4 must be equal to Field 1 x (r/ (100 + r)), where r is the current VAT rate of 15%.

- This amount is automatically calculated on the VAT201 Return but will be editable if the vendor disagrees with the automatic calculations. If the edited amount differs considerably from the auto calculated amount, an error message will prompt the vendor to ensure that the correct value is entered.

- Field 4A must be equal to Field 1A x (r/ (100 + r)).

- This amount is automatically calculated on the VAT201 Return but will be editable if the vendor disagrees with the automatic calculations. If the edited amount differs considerably from the auto calculated amount, an error message will prompt the vendor to ensure that the correct value is entered.

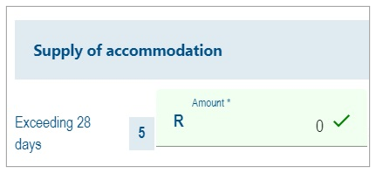

- Field 5 – Supply of accommodation

- The VAT exclusive amount of commercial accommodation supplied exceeding 28 days must be completed in Field 5. The total value (VAT excluded) in respect of:

- Commercial accommodation provided for a full period of more than 28 days must be reported in Field 5;

- The amount charged must be an all-inclusive charge that includes the charge for domestic goods and services. If the amount is not an all-inclusive charge, the amount (inclusive of tax) must be reflected in Field 1 above.

- The VAT exclusive amount of commercial accommodation supplied exceeding 28 days must be completed in Field 5. The total value (VAT excluded) in respect of:

- Field 6 must be equal to Field 5 x 60%. This amount is automatically calculated on the VAT201 Return.

- Field 7

- The VAT exclusive amount of accommodation supplied not exceeding 28 days must be completed in Field 7. The total value (VAT excluded) in respect of accommodation supplied for a period equal to or less than 28 days (full period) must be reported in Field 7

- Field 8 must be equal to the sum of Fields 6 and 7. This amount is automatically calculated on the VAT201 Return.

- Field 9 must be equal to Field 8 x (r/100). This amount is automatically calculated on the VAT201 Return.

- Field 9 is calculated by applying the tax rate (i.e. 15%) instead of the tax fraction (15/115) to Field 8.

Adjustments

- Field 10 – Change in use and export of second-hand goods

- The amount of change in use and the export of second-hand goods must be completed in Field 10. Consideration (VAT included) in respect of goods and/or services purchased for taxable supplies but applied for private use and exempt supply use.

- The purchase price of second-hand goods for which a national input tax was deducted where those goods were subsequently exported must be completed in Field 10.

- Field 11 must be equal to Field 10 x (r/ (100 + r)).

- This amount is automatically calculated on the VAT201 Return but will be editable if the vendor disagrees with the automatic calculations. If the edited amount differs considerably from the auto calculated amount, an error message will prompt the vendor to ensure that the correct value is entered.

- Field 12 – Other and imported services

- Only VAT payable in respect of the following may be entered:

- Debit notes issued;

- Credit notes received;

- Recovery of irrecoverable debts;

- Barter transactions;

- Services imported by you for purposes of making non taxable supplies;

- Adjustments in respect of acquisition of a going concern;

- VAT adjustments in respect of change in accounting basis.

- Only VAT payable in respect of the following may be entered:

- Field 13 – Total Output Tax

- Total Output Tax must be equal to the sum of Fields (4+4A+9+11+12). This amount is automatically calculated on the VAT201 Return.

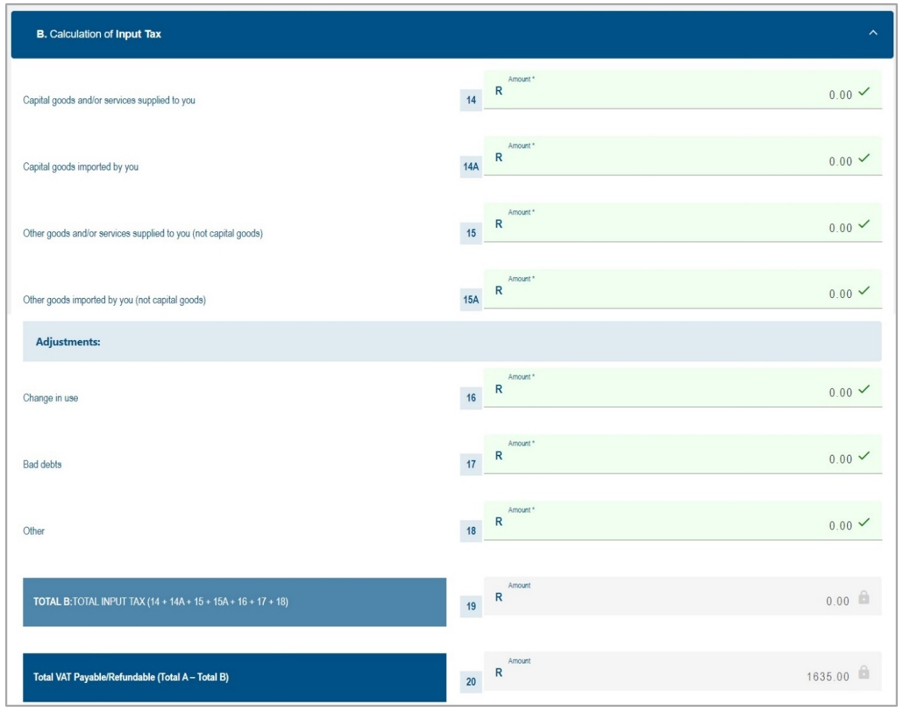

Calculation of Input Tax

- Field 14 – Capital goods and/or services supplied to you

- The permissible VAT amount of capital goods and/or services supplied to you must be completed in Field 14. The prescribed document, for example a valid tax invoice must be held by you before you complete any amount in this field. Examples of such acquisitions are:

- Office equipment;

- Furniture;

- Trucks;

- Land and buildings.

- The permissible VAT amount of capital goods and/or services supplied to you must be completed in Field 14. The prescribed document, for example a valid tax invoice must be held by you before you complete any amount in this field. Examples of such acquisitions are:

- Field 14A – Capital goods imported by you

- The permissible VAT amount of capital goods imported by you must be completed in Field 14A. The Customs Code field is mandatory. This field applies to capital goods imported in respect of which a bill of entry valid release document and receipt for the payment of the VAT issued by Customs, is held.

- Field 15 – Other goods and/or services supplied to you (not capital goods)

- The permissible VAT amount of other goods and/or services supplied to you (not capital goods) must be completed in Field 15.The prescribed document, for example a valid tax invoice, must be held by you before you complete any amount in this field. Examples of such acquisitions are:

- Accounting fees;

- Advertisements;

- Commission paid;

- Cleaning materials;

- Short term insurance premiums;

- Membership fees;

- Rent;

- Repairs

- Second-hand goods (notional input tax);

- Stationery;

- Stock purchases;

- Telephone;

- Water and lights.

- The permissible VAT amount of other goods and/or services supplied to you (not capital goods) must be completed in Field 15.The prescribed document, for example a valid tax invoice, must be held by you before you complete any amount in this field. Examples of such acquisitions are:

- Field 15A – Other goods imported by you (not capital goods)

- The permissible VAT amount of other goods imported by you (not capital goods) must be completed in Field 15A. The Customs Code field is mandatory. This applies to non-capital goods imported in respect of which a bill of entry ,valid release document and receipt for the payment of the VAT issued by Customs, is held. An example of such acquisition is the importation of trading stock.

Adjustments

- Field 16 – Change in use

- The VAT amount in respect of the change in use must be completed in Field 16. Only the VAT amount in respect of:

- Goods and services previously applied for non-taxable purposes and now wholly or partially applied for taxable purposes.

- An increase in the extent of application of use of goods and / or services for taxable purposes.

- The VAT amount in respect of the change in use must be completed in Field 16. Only the VAT amount in respect of:

- Field 17 – Bad debts

- The VAT amount in respect of bad debts must be completed in Field 17. Fill in only the VAT amount in respect of irrecoverable debts on which VAT was levied during the sale. Only applies if registered under the invoice basis of VAT accounting.

- Field 18 – Other

- Only the VAT amount in respect of:

- Credit notes issued

- Debit notes received

- VAT adjustments in respect of change in accounting basis

- Only the VAT amount in respect of:

- Field 19 – Total Input Tax must be equal to the sum of Fields (14+14A+15+15A+16+17+18). This amount is automatically calculated on the VAT201 Return.

- Field 20 – VAT Payable /Refundable (Total A – Total B) must be equal to the difference between Fields 13 and 19.

- This amount is automatically calculated on the VAT201 Return. If the difference between Field 13 and 19 is less than zero, then the minus (-) sign must be added in the first block before the amount entered in the field. The minus sign (-) will indicate that a refund is due. If Field 20 has no minus sign (-) before the amount, then the amount indicates that payment is due.

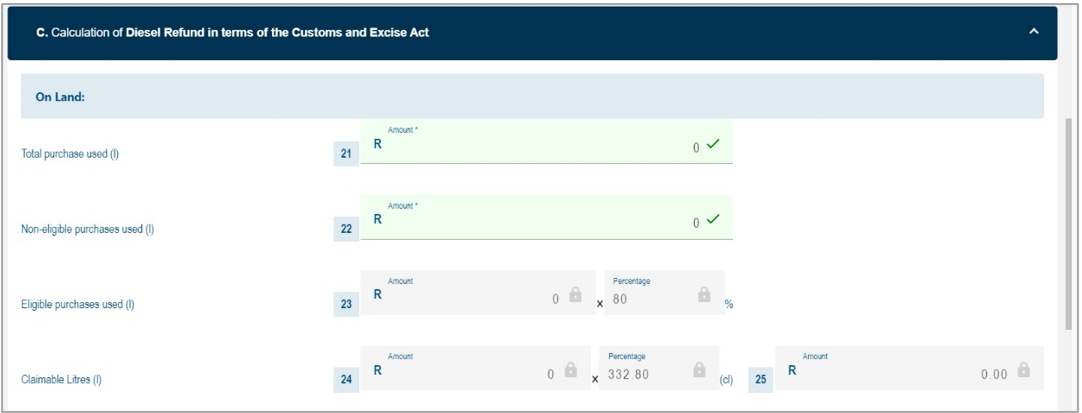

Calculation of Diesel Refund in terms of Customs and Excise Act

Note: Below is an example of how the return will be displayed for the Land section. The “Offshore”, “Rail &Harbour services” and “Peak Power Plant” sections will have the same look.

On Land

- Field 21 – Total Purchases (l)

- The total amount of diesel purchases in litres in respect of eligible and non-eligible purchases.

- Field 22 – Non-eligible purchases (l)

- The total amount of non-eligible litres.

- Field 23 – Eligible purchases (l)

- The amount of diesel in respect of eligible purchases (total purchases less non-eligible purchases). This field is mandatory if field 21 was completed and must be in full litres.

- Field 24 – Claimable litres (l)

- Eligible litres x 80% (concession percentage). This amount is automatically calculated on the VAT201 Return.

- Field 25 – Total

- The value of field 24 x (current diesel rate for on land) cents per litre/ 100. This amount is automatically calculated on the VAT201 Return.

Offshore

- Field 26 – Total Purchases (l)

- The total amount of diesel purchases in litres in respect of eligible and non-eligible purchases.

- Field 27 – Non-eligible purchases (l)

- The total amount of non-eligible litres.

- Field 28 – Eligible purchases (l)

- The amount of diesel in respect of eligible purchases (total purchases less non-eligible purchases). This field is mandatory if Field 26 was completed and must be in full litres.

- Field 29 – Total

- The total value of field 28 x (current diesel rate for offshore) cents per litre/100. This amount is automatically calculated on the VAT201 Return.

Rail & Harbour Services

- Field 30

- The total amount of diesel purchases in litres in respect of eligible and non-eligible purchases.

- Field 31

- The total amount of non-eligible litres.

- Field 32

- The amount of diesel in respect of eligible purchases (total purchases less non-eligible purchases). This field is mandatory if field 30 was completed and must be in full litres.

- Field 33

- The value of field 32 x (current diesel rate for rail) cents per litre/ 100. This amount is automatically calculated on the VAT201 Return.

Peak Power Plant

- Field 34

- The total amount of diesel purchases in litres in respect of eligible and non-eligible purchases.

- Field 35

- The total amount of non-eligible litres.

- Field 36

- The amount of diesel in respect of eligible purchases (total purchases less non-eligible purchases). This field is mandatory if field 30 was completed and must be in full litres.

- Field 37

- The total value of field 36 x (current diesel rate for peak power plant) cents per litre/ 100. This amount is automatically calculated on the VAT201 Return.

- Field 38

- The amount of diesel in respect of eligible purchases (total purchases less non-eligible purchases). This field is mandatory if field 36 was completed and must be in full litres.

- Field 38 = Fields 20 – (25 + 29 + 33+37) or 20+(25+29+33+37)

- If Field 38 is less than zero, then the minus sign (-) must be added in the first block before the amount is entered in the field. This means a refund is due

- If Field 38 is more than zero, it means a payment is due.

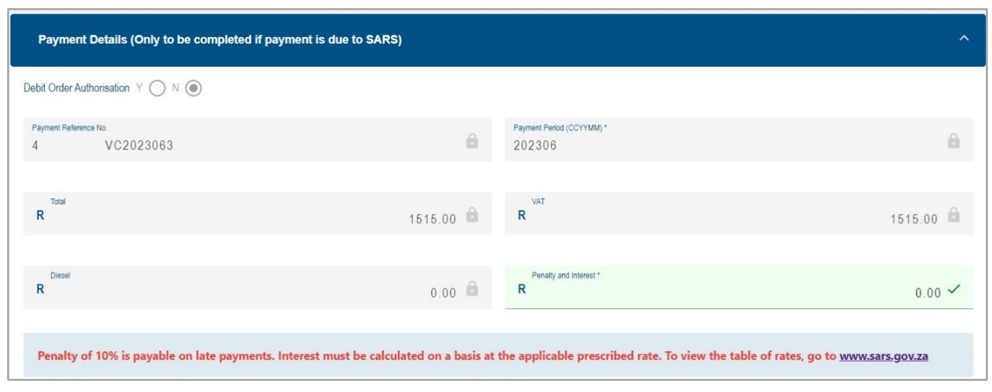

Payment Details

- Note: The details of payment made must be completed in this section.

- Debit Order Authorisation

- The VAT debit order facility as arranged with SARS, will no longer apply and an “N” will show for all eFilers.

- Payment Reference Number (PRN)

- This number will be generated by SARS when the VAT201 Return is issued to the vendor.

- Payment Period (CCYYMM)

- This field will be automatically pre-populated. The payment period will be exactly the same as the tax period under the Vendor Details section.

- Total

- The total amount of the VAT payment due to SARS is automatically calculated on the VAT201 Return. If you are registered for diesel and entered any amounts in the diesel section, then the Total field is calculated as Fields 20 – (25 + 29 + 33) + Penalties and Interest (where applicable). If you are not registered for diesel, then the Total field is equal to Field 20 + Penalties and Interest (where applicable).

- VAT

- The portion of the total amount of the payment for VAT will be equal to Field 20 and will be automatically populated on the VAT201 Return.

- Diesel

- The diesel amount is the sum of Fields 25+29+33. This field will be automatically calculated on the VAT201 Return.

- Penalty and Interest

- The portion of the payment that must be allocated to a penalty and/or interest for the specific tax period must be completed in this field. If the vendor wants to pay interest/penalties/outstanding taxes in respect of another tax period, the PRN for that tax period must be used.

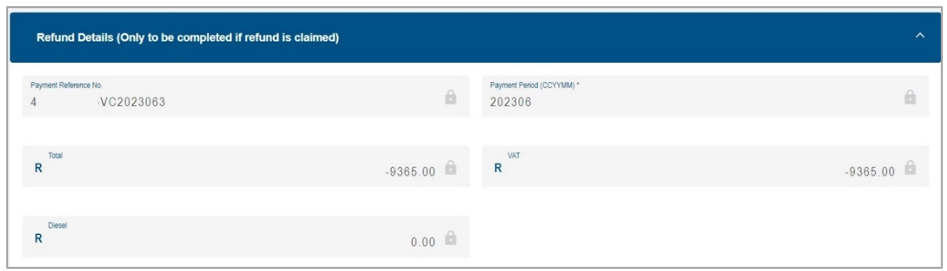

Refund Details

- Note: This section will be applicable if a refund is claimed by the vendor.

- Payment Reference Number (PRN)

- This number will be generated by SARS when the VAT201 Return is issued on eFiling.

- Payment Period (CCYYMM)

- This field will be pre-populated. The payment period will be exactly the same as the tax period under the Vendor Details section.

- Total

- The total amount of the refund claimed is automatically calculated on the VAT201 Return. If you are registered for diesel and entered any amounts in the diesel section, then the Total field is calculated as Fields 20 – (25 + 29 + 33). If you are not registered for diesel then the Total field must be equal to Field 20.

- VAT

- The total amount of the VAT refundable (Field 20) will automatically be populated on the VAT201 Return.

- Diesel

- The diesel amount is the sum of Fields 25+29+33. This field will be automatically calculated on the VAT201 Return.

Declaration

The electronic signature (i.e. the vendor’s log in) associated with an eFiler is deemed to be the signature of the declarant.

Submitting the VAT201 Return

- The following channels can be used by a vendor to submit a VAT201 Return:

- eFiling; or

- At a SARS Office

- All vendors should make an appointment on the SARS website before visiting a SARS office.

- Submit at a SARS Office

- The completed VAT201 Return can be submitted personally at any SARS Office, by making an appointment on the SARS website. When submitting the VAT201 Return at the SARS office, the Return will be captured/processed by the SARS agent. For physical addresses of SARS offices go to www.sars.gov.za and click on Contact Us.

- eFiling submissions

- The VAT201 Return can be completed electronically by entering the relevant information into the applicable fields. After the VAT201 Return has been completed, it must be submitted using the eFiling channel. The VAT201 Return will automatically be processed by SARS.

- Note: Faxed, emailed or photocopied VAT201 Returns printed from eFiling will not be accepted by SARS.

Submission of VAT201 via eFiling

- Once all the required fields have been captured, click on the “Save” or “Submit VAT201” button to save or submit your VAT201 Return.

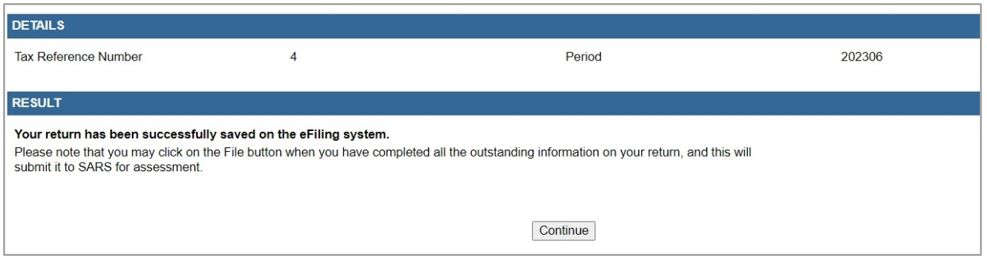

- If the VAT201 Return is saved it will be stored on the eFiling system and it will still be available for editing before submitting the VAT201 Return to SARS. If the VAT201 Return is filed, it will be automatically submitted and processed by SARS.

- If your VAT201 Return has been successfully saved on eFiling, the following screen will display:

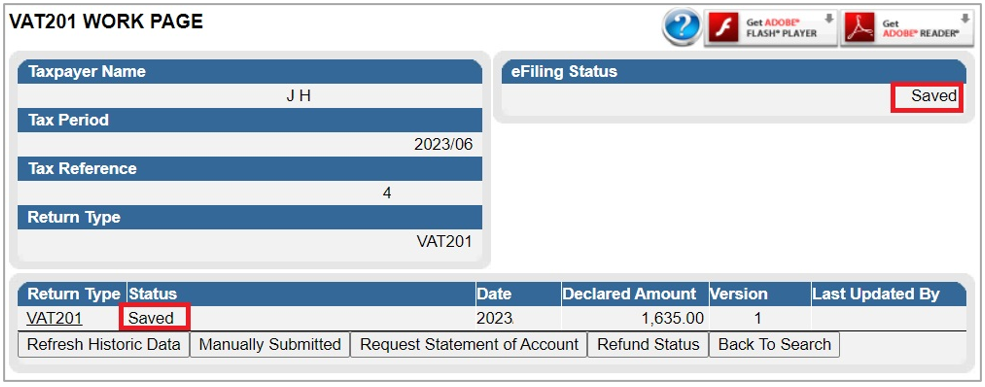

- The VAT201 Work Page will be updated to indicate that the return has been “Saved”.

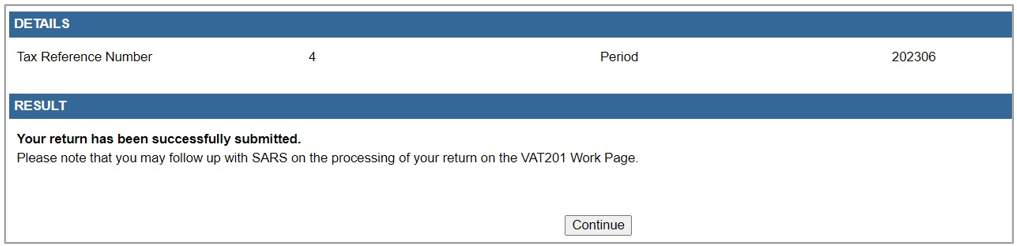

- If your VAT201 Return has been successfully filed on eFiling, the following screen will be displayed:

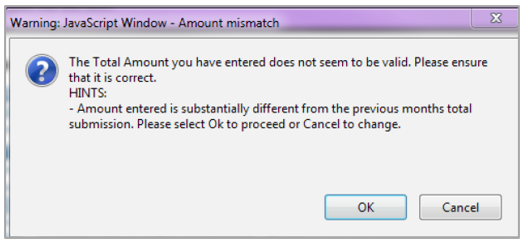

- Note: Before the VAT201 Return is filed and if the amount declared for this tax period is substantially different from the amount declared in the previous tax period, the following message will be displayed:

- Notes:

- If a vendor was in the process of completing their VAT201 Return in respect of any tax period using the old format, these VAT201 returns will be removed so that the updated VAT201 with the correct rate of tax can be requested.

- A vendor will only be allowed to submit a VAT201 Return on the 1st day of the month following the tax period for which the return must be made.

- If a VAT return is submitted at a SARS office, the submitted return, including estimations processed by SARS and the corresponding assessment notice (VAT217) will be sent to eFiling, if the vendor is a registered eFiler.

- The VAT return status will be indicated on the VAT Work Page as “Filed through another channel”.

- The vendor will be able to request for correction using the current process.

- If any Verification or Audit cases on these returns are still active, the corresponding letters will be sent to eFiling to activate the supporting documents link to allow the submission of supporting documents via eFiling.

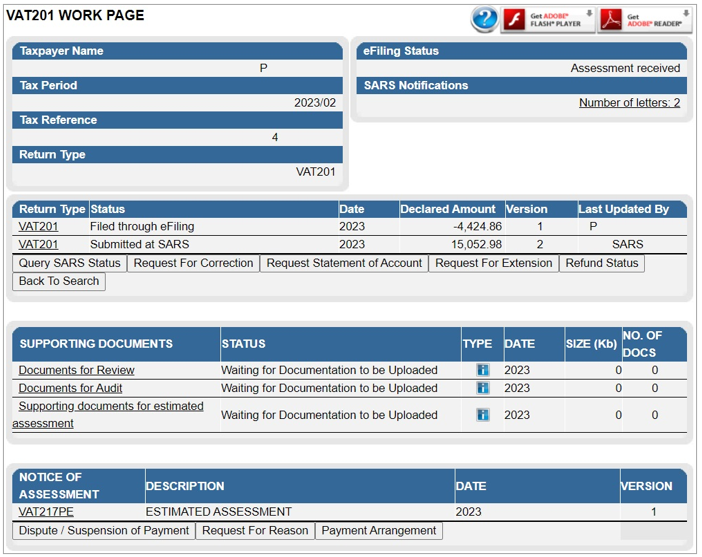

- The VAT201 Work Page will display the “Dispute / Suspension of Payment” button.

- For assistance with the Dispute, including Suspension on Payment process, refer to the “Guide to submit a Dispute via eFiling – External Guide” available on the SARS website www.sars.gov.za.

Additional/Revised Estimated VAT Assessments

- The VAT verification process has been enhanced and certain functionality will be available on eFiling to vendors where SARS raise a section 95(1)(c) estimate assessment for those vendors that fail to submit supporting documents. Vendors will now:

- Submit relevant material after a section 95 estimate assessment was issued;

- Request for extension to submit supporting documents;

- Request Suspension of payment if a relevant Material case has been created

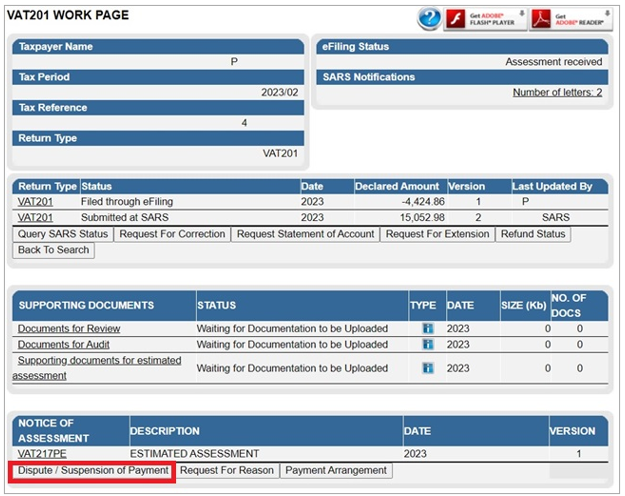

- The Assessment Notice (VAT217) will be displayed on the VAT Work Page to reflect the Section 95(1)(c) estimates and reason(s) for assessment.

- The VAT Work Page will indicate the status “Submitted at SARS” as indicated below:

- The VAT217 will be displayed on the work page as well.

Request for Extension

- Section 95 of the Tax Administration Act has been amended to allow for the Vendor to have the ability to request extension for the period, allowed to submit relevant material or a return after an estimate assessment has been issued.

- The Vendor will have the ability to request extension to submit relevant material related to S95(1)(c) estimated assessment after the Notice of Assessment (VAT217) has been issued to the Vendor.

- The “Request for extension” button to provide relevant material will be available up to 5 years and 40 business days after the original assessment for which the verification case was created.

- If no request is received from the vendor after 5 Years and 40 business days after the original assessment for which the verification case was created, both the “Request for extension” and the option to submit relevant material will be unavailable for selection.

- A message will be displayed to the Vendor: ‘Request for Extension” can no longer be submitted as the allowable days to file the request has lapsed. Therefore, the Estimate Assessment issued to you for the tax period is now considered final’.

- Once a Request for Extension has been submitted to SARS for a tax period, the Vendor will not be allowed to request extension for that same period again from the respective channels while the case is in progress or the date for which it has been approved has not lapsed.

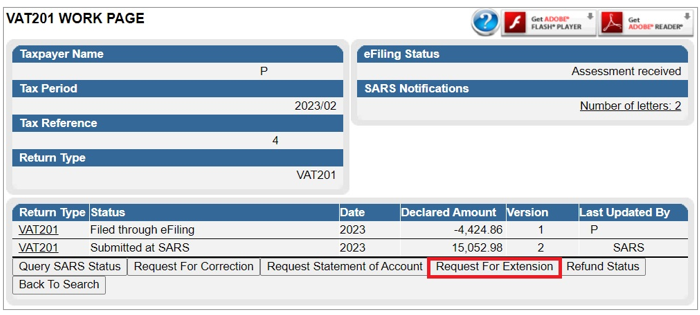

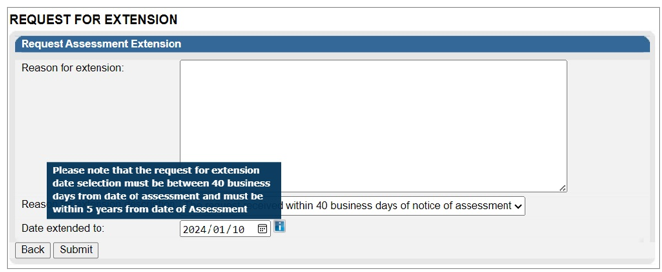

- Click the “Request for Extension” button on the VAT Work Page as indicated in the below screen.

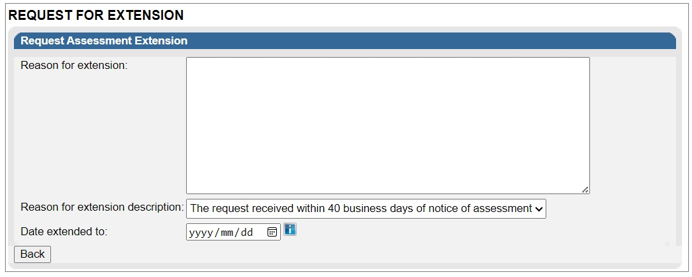

- The Request for Extension screen will be displayed for completion.

- The following fields must be completed:

- Reason for Extension;

- Reason for extension description; and

- Date extended to.

- If you hover over the date information “i”, the following message will be displayed, namely “Please note that the request for extension date selection must be between 40 business days from the date of assessment and must be within 5 years from date of assessment.”

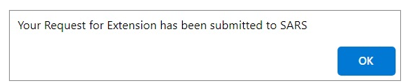

- Select “Back” to revert to the VAT Work Page or “Submit” to submit the Request for Extension to SARS. Select the “OK” button on the confirmation message after submitting the Request for Extension to SARS.

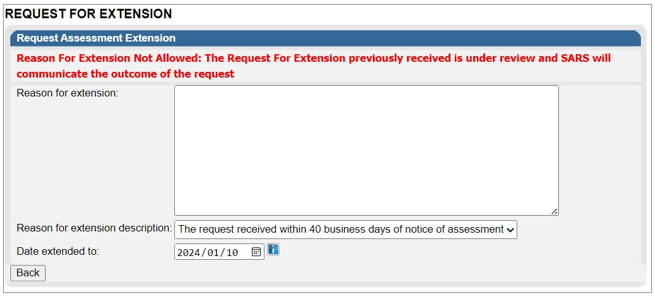

- Error messages will be displayed after the submission of the Request for Extension and the vendor tries to request the extension again:

- If a Vendor has submitted the Request for Extension, and the Request for Extension was received by SARS, but the Vendor has not received the Confirmation Notice and attempts to select the Request for Extension button again:

- The Request for Extension previously received is under review and SARS will communicate the outcome of the request’.

- If a Vendor has submitted the Request for Extension and the request is granted by SARS, however, the Vendor attempts to select the Request for Extension button again on a date before the period for which the extension was approved:

- ‘The request for an extension has been finalized and a new date to submit the relevant material was granted’.

- If the vendor attempts to submit a return after this period of extension has lapsed the following message will display:

- ‘The request for VAT201 cannot be processed as allowable period to submit VAT201 return after estimate has lapsed.’

- In the event a vendor attempts to submit relevant material more than 5 years plus 40 business days after a section 95(1)(c) estimate assessment was issued, the following message will be displayed to the vendor:

- ‘The deadline for submitting the relevant material has lapsed. Your request cannot be processed. Therefore, the Estimated Assessment issued to you for the tax period is now considered final’.

- In the event a vendor attempts to submit relevant material more than 40 business days after a section 95(1)(c) estimate was issued and has not applied for extension or the request for extension has lapsed, the following message will be displayed to the vendor:

- ‘The deadline for submitting the relevant material has elapsed. You can however request for an extension. Should your request for an extension be approved, you will be allowed to submit the relevant material’.

- If a Vendor has submitted the Request for Extension, and the Request for Extension was received by SARS, but the Vendor has not received the Confirmation Notice and attempts to select the Request for Extension button again:

- Below is an example of a screen that indicate the message on the Request for Extension screen.

- Upon the completion of the request for extension by SARS, outcome letters will be issued and available on the Correspondence and the return Work Page on eFiling.

- The request for Extension button will be displayed on the VAT217 screen as well, as indicated below.

Making a Payment

- The VAT201 Return contains a new Payment Reference Number (PRN). This number will be pre-populated by SARS. The vendor must use this PRN when making VAT and Diesel to SARS in order to link the actual payment to the payment declared on the VAT201 Return.

- Note: The unique PRN on the VAT 201 Return provided by SARS must be used when making payments. Each VAT201 Return that you request from SARS will have its own unique PRN which will be used to track individual payments and queries.

- The PRN should only be used once for that specific tax period’s submission of return and payment. The 19-digit PRN is structured as follows:

- Digit 1-10 is your VAT registration number

- Digit 11-19 will be systematically allocated by SARS

- For example: 4123456789VC2011091

- Vendors can make use of the following payment methods:

- eFiling;

- Approved banking institution;

- EFT.

- EFT

- Payments can be made directly to SARS using the internet banking services offered by:

- ABSA

- Al Baraka Bank

- Capitec

- FNB

- Grobank Ltd (previously Bank of Athens)

- HSBC

- Investec

- JP Morgan

- Mercantile Bank

- Nedbank

- Standard Bank

- Payments can be made directly to SARS using the internet banking services offered by:

- In all instances it is imperative that the correct PRN is provided to ensure that tax payments are easily identified and correctly allocated by SARS.

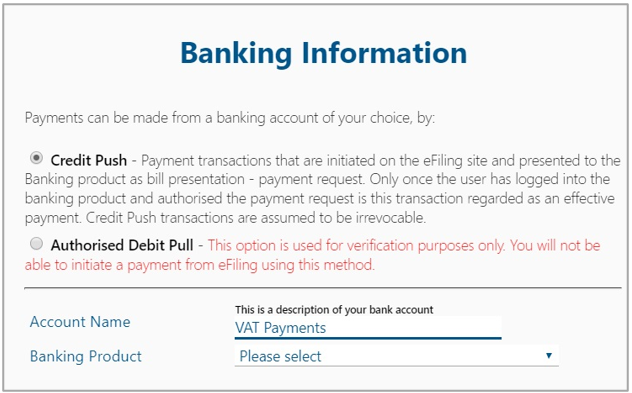

- Note: “Additional Payments” on eFiling for Income Tax, Provisional Tax, Value-Added Tax (VAT) and Pay-As-You-Earn (PAYE) is not available via the Debit Pull facility. In such cases the Credit Push facility must be used.

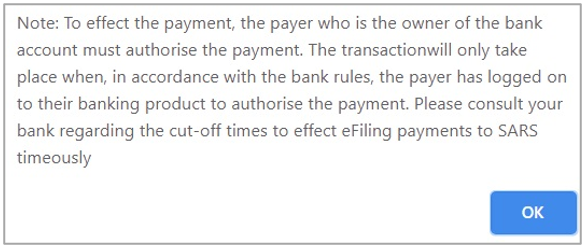

- Credit push

- Refers to payment transactions that are initiated on the eFiling site and presented to the banking product as bill presentation, i.e. a payment request. Only once the user has logged into the banking product and authorised the payment request is this transaction regarded as an effective payment. Credit push transactions are irrevocable once approved.

- Banking institutions

- Payment can be made at any ABSA, Capitec, FNB, Nedbank or Standard Bank branch. These payments must comply with the same PRN requirements as EFT payments.

- eFiling

- Note: For more information on payment rules and acceptable payment methods, please refer to the SARS Payment Rules External Guide which is available on www.sars.gov.za

- You can make the payment immediately after the submission of the VAT201 Return or opt to make the payment at a later stage by selecting the Payments menu on eFiling.

- Notes:

- Vendors can complete their VAT201 Return on eFiling and make the corresponding payment on eFiling.

- Vendors can complete their VAT201 Return on eFiling and submit to SARS. Thereafter the vendor can make the corresponding payment at a later time on eFiling via the VAT201 Work Page or another channel (i.e. Internet Banking, Bank).

- A vendor will not be able to make a payment via eFiling prior to submitting the corresponding VAT201 Return via eFiling.

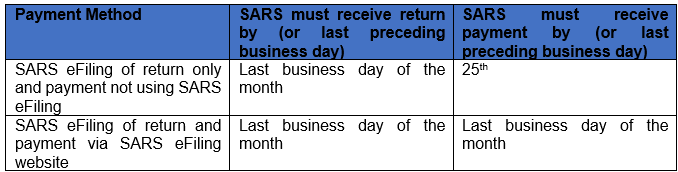

- The date on which the VAT201 Return and payment must be received by SARS will be explained in the table below:

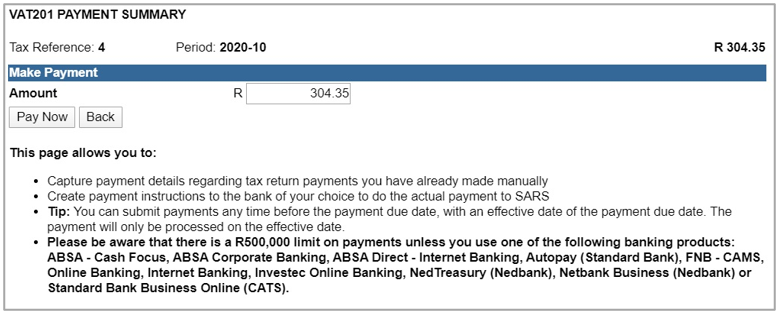

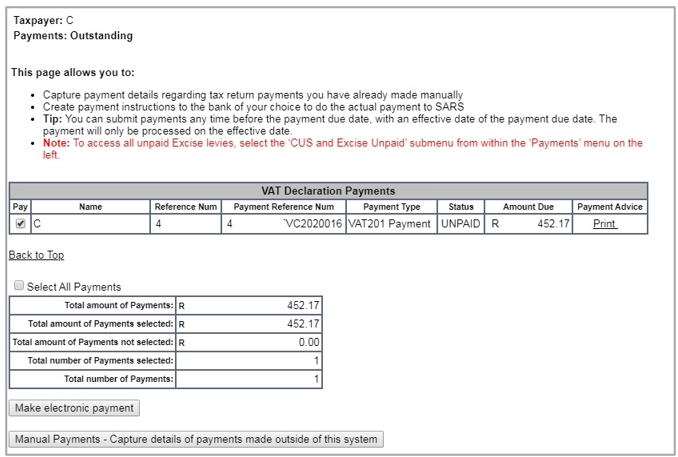

- On the VAT201 Work Page, the “Make Payment” button will be available to make the payment to SARS:

- If you click on the “Make Payment” button VAT201 Payment Summary screen will be displayed:

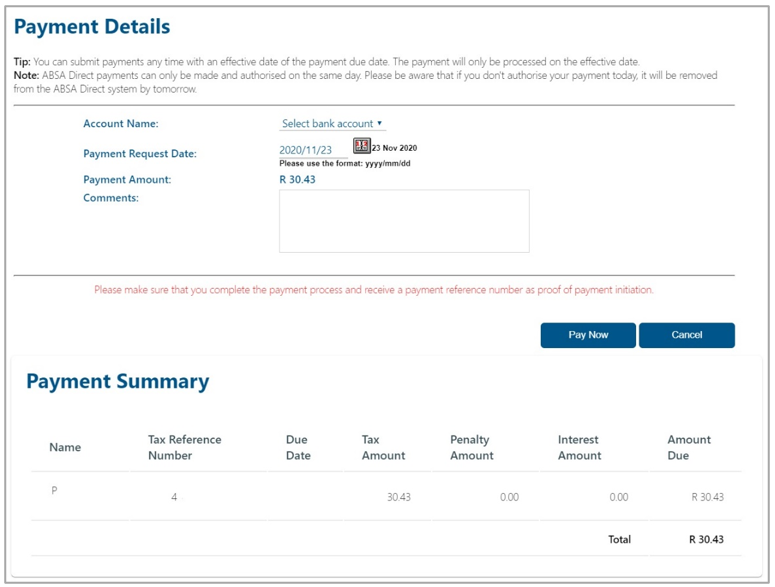

- If you click on the “Pay Now” button, the following screen will be displayed, and you will be requested to provide your bank details to initiate the payment process:

- Amount – This field is editable to allow you to enter the amount you would like to pay

- Pay Now – This button will redirect you to the Payment Details page.

- Back – This button will take you back to theVAT201 Work Page.

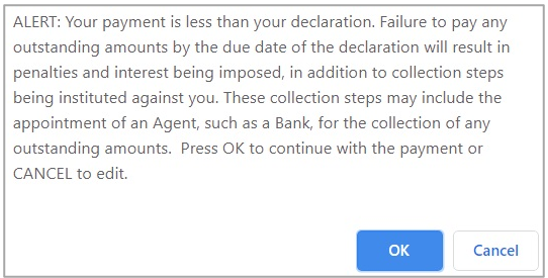

- Should you reduce the populated amount to be paid, the following message will be displayed:

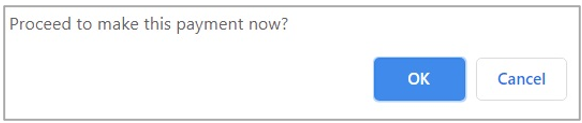

- Click “OK” to proceed with the reduced payment or “Cancel” to be routed back to the Payment Summary screen. If you click “OK”, you will receive a confirmation message as indicated below.

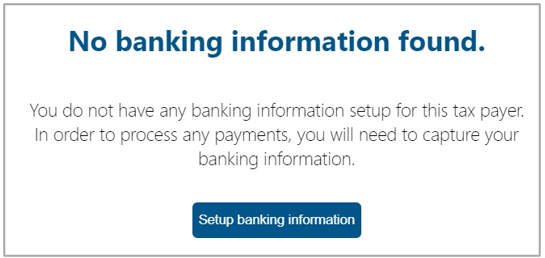

- If there are no bank details set up on eFiling, the following screen will be displayed.

- Click “Setup banking information” to save bank details on eFiling to initiate payments.

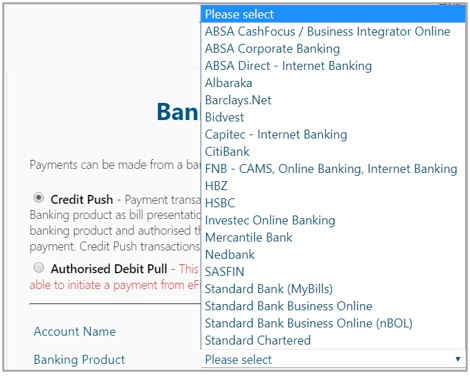

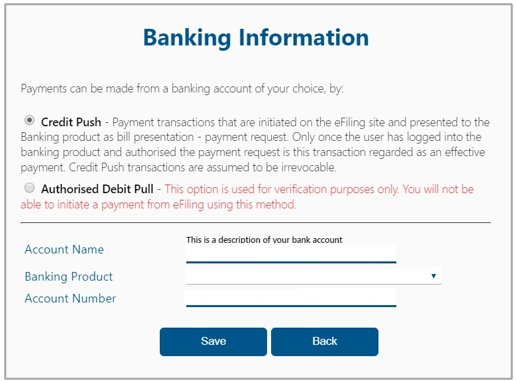

- If you select the “Banking Product” field, a list of banks will be displayed. Select the relevant bank.

- After selecting the bank, the Account Number field will be displayed for completion. Complete this field and select “Save” to proceed or “Back” to make changes to the bank information captured.

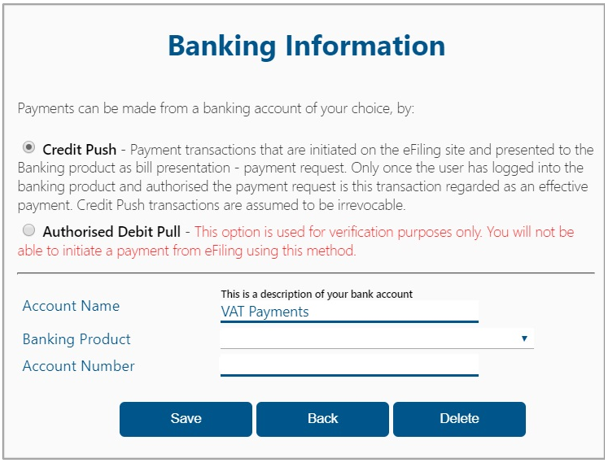

- After you have saved the bank details, the details will be saved on eFiling as indicated below.

- If you click the “Open” hyperlink, the banking Information page will be displayed.

- To remove the bank details, click the “Delete” button. Click “OK” to confirm the deletion of the bank details or “Cancel” to close the message.

- After you have confirmed the deletion of the bank details, no bank details will be displayed on the banking details page on eFiling.

- If the amount entered is the required amount as populated on the VAT 201 Return, the following screen will be displayed:

- Ensure that the payment is selected and click “Make electronic payment” to continue.

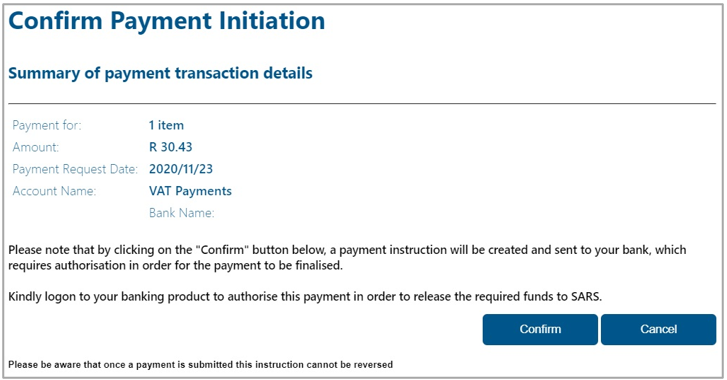

- If you click on the “Cancel” button, you will be redirected to the Return Search page. If you click on “Pay Now” the following screen will be displayed:

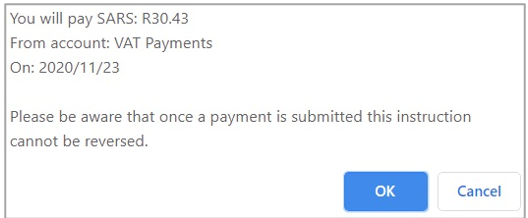

- Click “OK” to proceed and the “Confirm Payment Initiation” screen as indicated below.

- If you click on the “Confirm” button a payment summary pop-up message will be displayed:

- If you click on the “Cancel” button, you will be redirected to the Return Search page. If you click on the “OK” button the confirmation page will be displayed:

- If you click on the “Cancel” button, you will be redirected to the Return Search page.

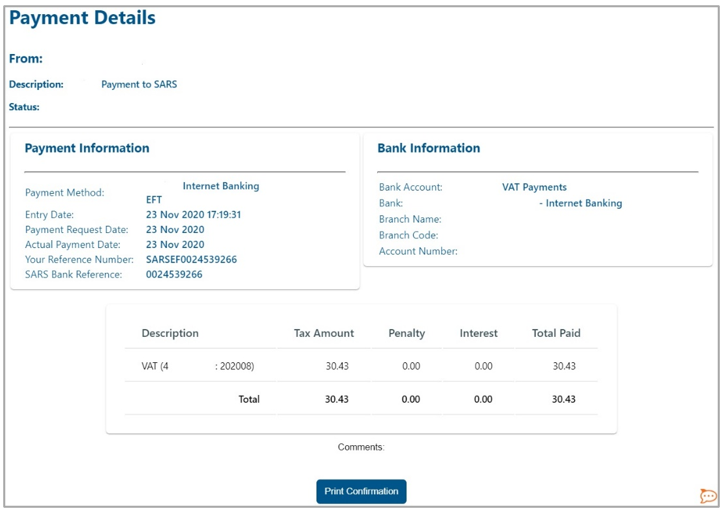

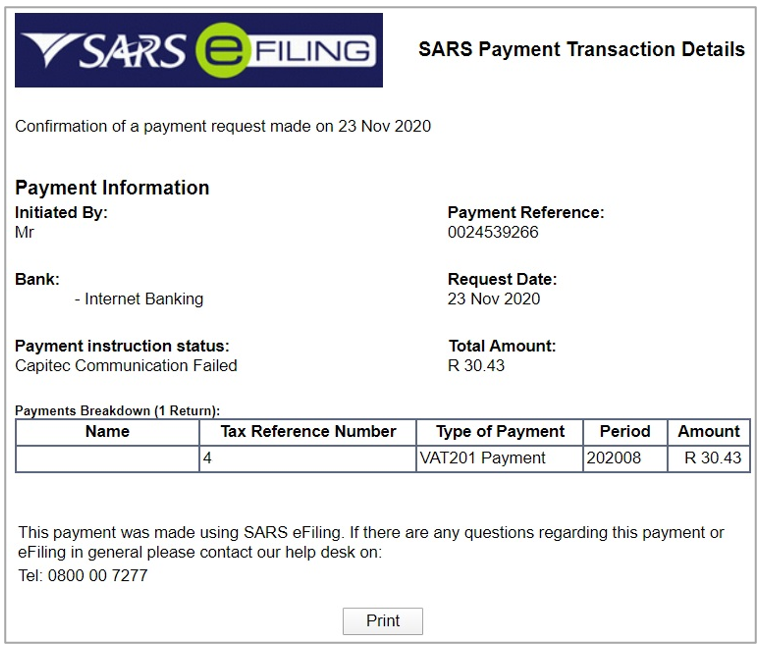

- To view your payment confirmation, click on the “Print Confirmation” button. The following screen will be displayed:

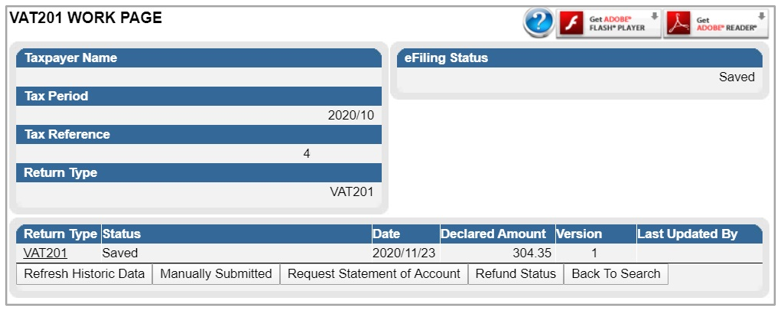

- If you opted to pay later you will find your saved VAT201 Return in the VAT201 Work Page. The following screen will be displayed when you return to the VAT201 Work Page:

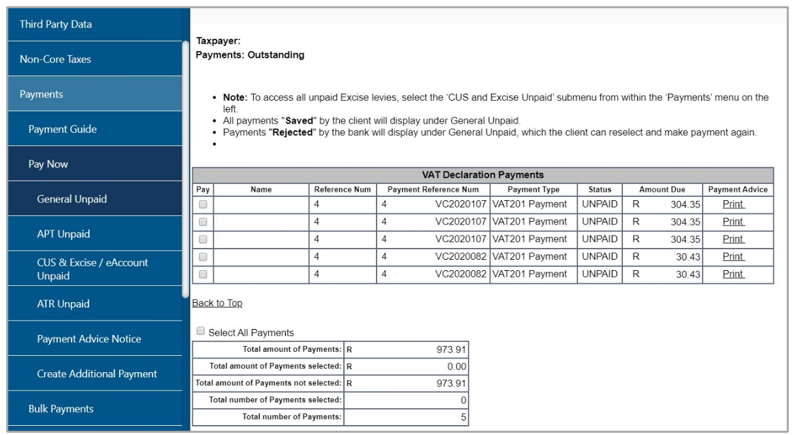

- If a payment was abandoned during the payment process, the payment entry will be created and listed as “General Unpaid” in the Payments You will be able to confirm the payment by ticking the “Pay” box. Please note that you will not be able to edit the amount reflected in this section.

Request for Correction

Vendors can revise a previously submitted VAT201 Return, whether it is for the current tax period or a prior tax period, amounts under Part A can be increased or decreased, however amounts under Part B can only be decreased on the VAT201 Return to reflect the correct VAT liability.

Notes:

- The vendor will be allowed to do a revision on the VAT portion of the VAT201 Return for any tax period within the last 5 years.

- The vendor will be allowed to do a revision on the diesel portion of the VAT201 Return for any tax period within the last 2 years.

- Revisions on the VAT201 Returns will only be accepted if submitted in the new format.

- There will be no limit on the number of revisions permitted to the vendors per tax period.

- When a vendor revises a VAT201 Return for the second time onwards (version 3), the vendor is required to submit supporting documents with the submission of the revised VAT201 Return to support the change made to the Return.

- The vendor will be able to request for a correction on the VAT201 Return from any channel and not only the channel on which the vendor submitted the original assessment for the tax period concerned.

- If an audit case has been finalised or a correction was done by a SARS user, the vendor will not be allowed to submit a revision of the VAT201 Return.

Manual Corrections

When a vendor intends to adjust any VAT201 Return to reflect the correct amounts, noting that the amounts under Part A can be increased or decreased, however amounts under Part B can only be decreased the following must be done:

- Request a new VAT201 Return for the relevant tax period from SARS. The PRN will be pre-populated when the revised VAT201 Return is posted to the vendor. This PRN number will be the same as the PRN in the original VAT201 Return.

- Complete the new VAT201 Return for the specific tax period where the correction needs to be made.

- Complete the full amounts on the new VAT201 Return (NOT the difference between the amounts completed on the current and previous Return).

- Any additional payment must be made using the same PRN.

Note: The vendor will not be allowed to increase his input tax deduction when doing a revision on a past tax period. If the vendor wishes to deduct input tax attributable to a past tax period, a deduction can be made in the next tax period or any future tax period, only if the deduction is made within five years from the date of first entitlement to such input tax deduction.

eFiling Corrections

When a vendor wants to increase/decrease the payment amount and needs to adjust the VAT201 Return for the specific tax period to reflect the correct figures, the following must be done:

- Access the previously submitted VAT201 Return via eFiling and use the “Request for Correction (RFC)” option.

- The application will automatically create an additional VAT201 Return with the same PRN and tax period, and will be reflected as a new version

- Complete the full amounts on the revised VAT201 Return (NOT the difference between the amounts completed on the current and previous return).

- Any additional payment must be made using the same PRN.

The following two scenarios will be where a vendor can request a correction on the filed VAT201 Return:

- Overstated Return: The vendor wants to decrease the return for a specific tax period.

- Understated Return: The vendor wants to increase the return for a specific tax period.

Select the desired return where a correction needs to be made on “Returns History” from the side menu options under Returns.

Select the “Request for Correction” option and the second version of the VAT201 Return will be available for editing.

When a vendor requests for a revision, the selected filed return is presented in a SAVED status and is allocated a new version.

Note: For corrections to previously submitted returns, vendors will only be allowed to adjust the last version of each return, therefore ensuring that the correct version is always adjusted

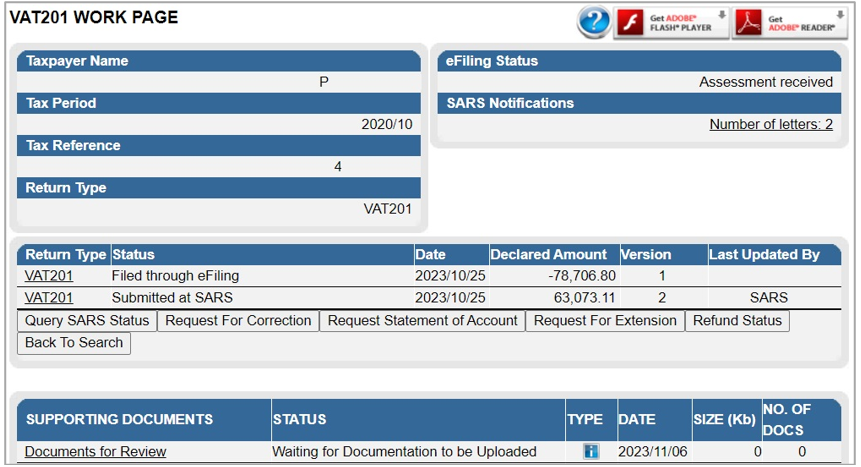

The vendor will be able to view the work page of any submitted VAT201 Returns. It will contain the following:

- Return type: VAT201 Return

- Tax period and Version: indicates the version number of the last submitted VAT201 Return

- Status: indicates the current status of the VAT201 Return

- Submission date: indicates the date on which that particular version of the VAT201 Return was submitted

- Submission Channel: indicates the channel by which that version was submitted

- Last updated by: indicates the name of the person who last updated the VAT201 Return.

A new VAT201 Return will be created with the minimal pre-populated fields.

- Notes:

- The vendor must submit a totally revised VAT201 Return and not just the difference on the fields the vendor wishes to revise.

- The vendor will be able to view the previously submitted return when performing the correction.

- The vendor will not be allowed to increase his input tax deduction when doing a revision on a past tax period. If the vendor wishes to deduct input tax attributable to a past tax period, a deduction can be made in the next tax period or any future tax period, only if the deduction is made within five years from the date of first entitlement to such input tax deduction.

Submitting Supporting Documents to SARS via eFiling

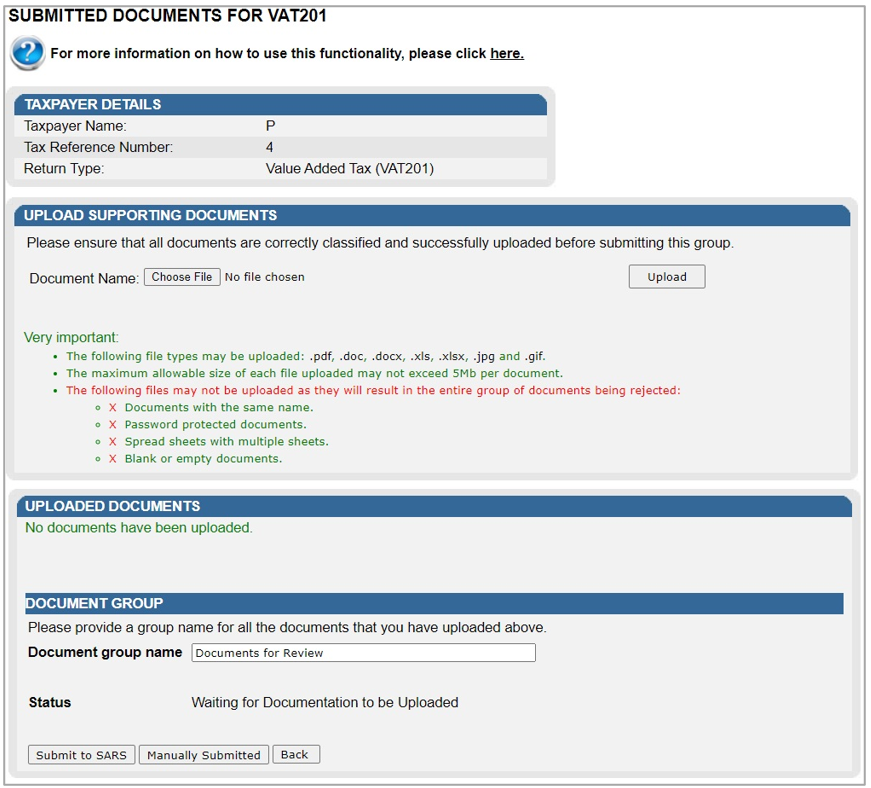

- SARS might request the vendor to upload relevant material, if it deems to be necessary. Relevant material must only be uploaded if a letter is received from SARS requesting the vendor to submit relevant material. This letter will be issued via eFiling and can be accessed under “SARS Correspondence”. Once the letter is opened, another container will open on the VAT201 work page under SUPPORTING DOCUMENTS from where the relevant material can now be uploaded.

- Select the relevant hyperlink displayed to upload the relevant material.

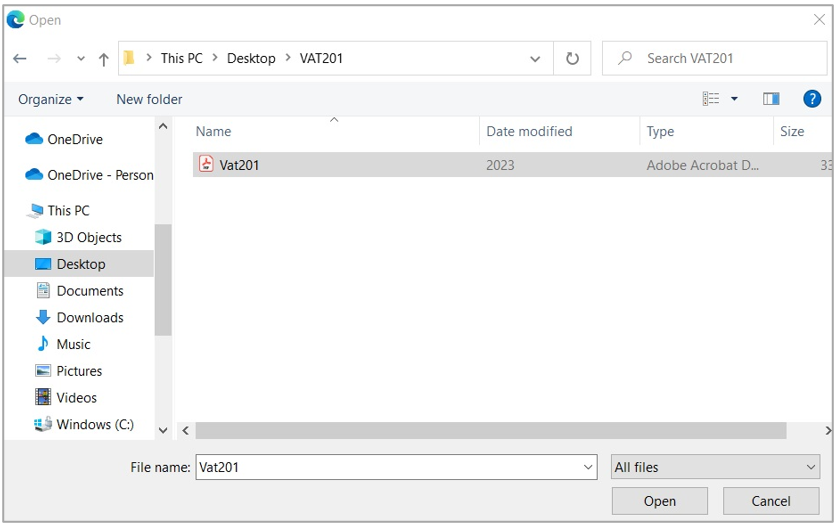

- Click on the “Choose File” button displayed on the screen and the following screen will be displayed to allow you to select the document(s) to be uploaded:

- This option will allow you to browse for documents saved on the computer, external storage devices and networks.

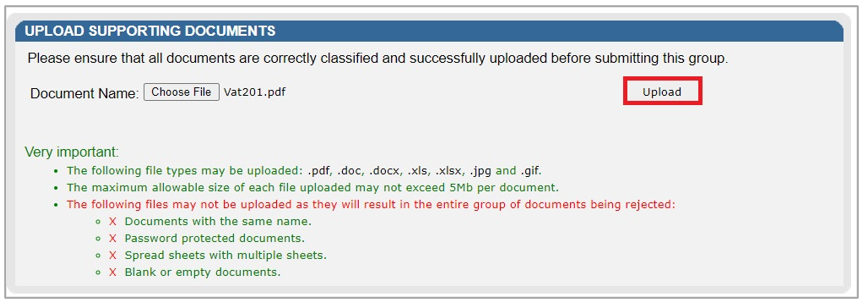

- Once you have selected the document(s) you can upload the supporting document(s) by clicking on the “Upload” button.

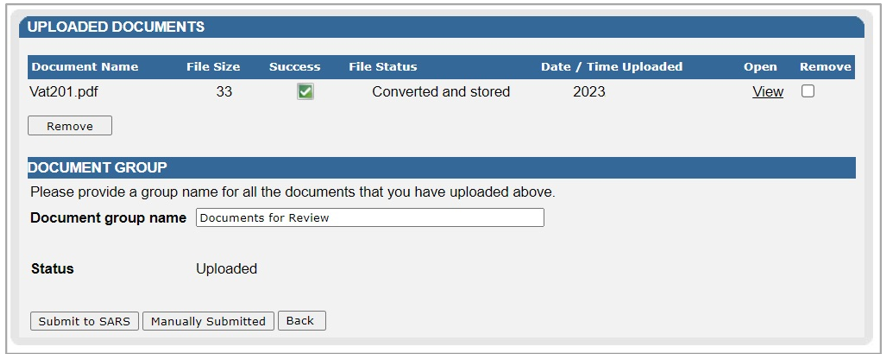

- The documents will be listed under the “Uploaded Documents” section on the below screen:

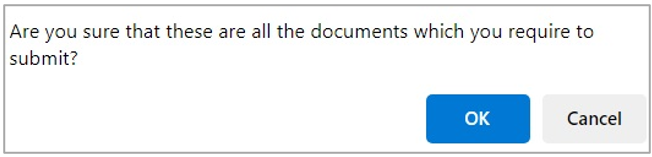

- Click the “Submit to SARS” button to proceed. Click the “OK” button on the confirmation message to submit all documents to SARS.

- Once the documents has been submitted to SARS, the supporting documents work page will be updated with a “Submitted” status.

- On the VAT217 notice, a “Submission of Relevant Material” button will be displayed to make it easier to submit supporting documents. When this button is selected, the vendor will be directed to the current upload documents screen to upload their relevant material

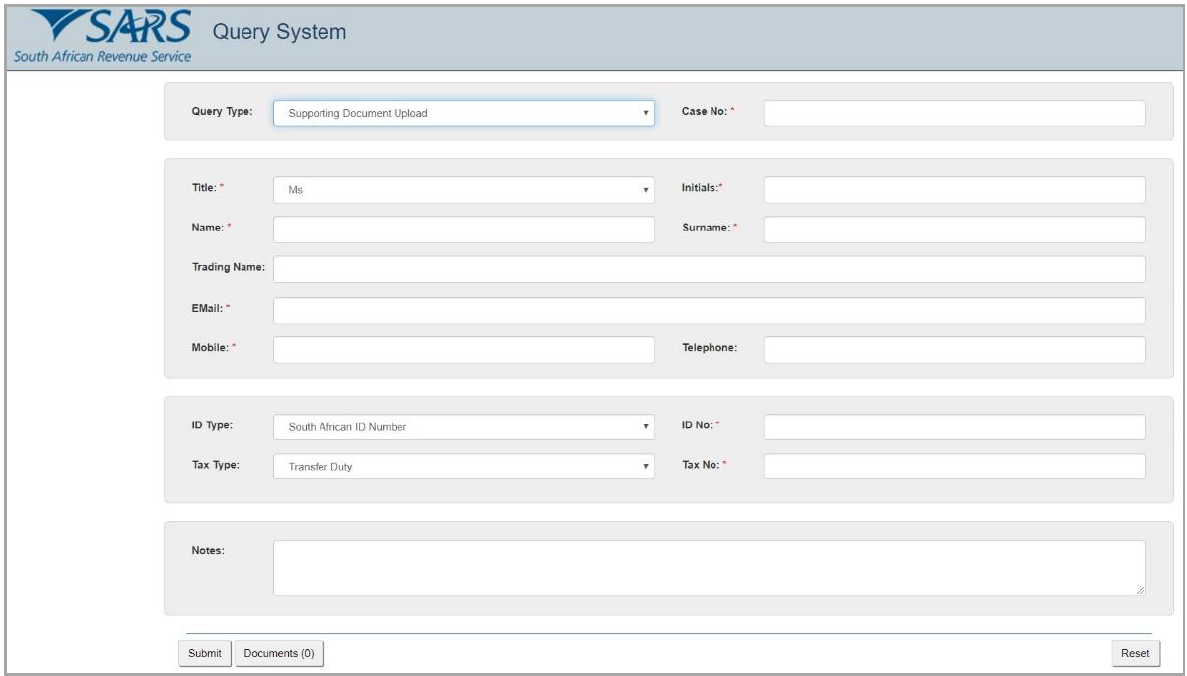

Upload of Required Supporting Documents via SARS Online Query System

- Access the SARS Online Query System on the SARS website www.sars.gov.za

- Complete all the relevant fields, upload the documents and submit to SARS.

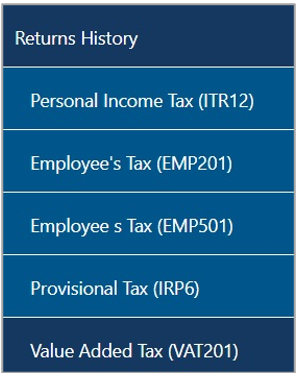

Viewing Historic Returns on eFiling

- On eFiling, users will have the ability to search for and view their filed VAT201 Returns. The VAT201 Returns that are listed in the “Returns History” list will be accessible from the Returns Search menu option.

- VAT201 Returns that have the status as set out below will be displayed on this menu:

- Submitted to SARS

- Processed by SARS

- Manually Submitted

- Selected for Audit.

- Click on the “Open” button on the grid to be redirected to the VAT201 Work Page.

- For a comprehensive understanding of VAT, the VAT404 Guide for Vendors is available on the SARS website at www.sars.gov.za

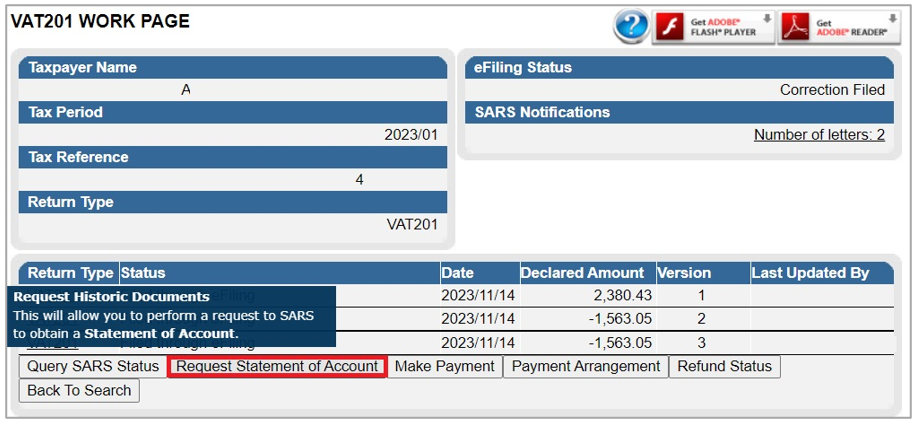

Requesting a Statement of Account (VATSOA) on eFiling

- This function will allow you to manage your VAT account by giving your insight into transactions per tax period.

- Notes:

- The vendor will only be able to request VATSOAs within the last 5 years, from date of request for statement. The vendor will only be able to request the VATSOA after March 2007 on eFiling, prior to this date the VATSOA must be obtained from a SARS branch.

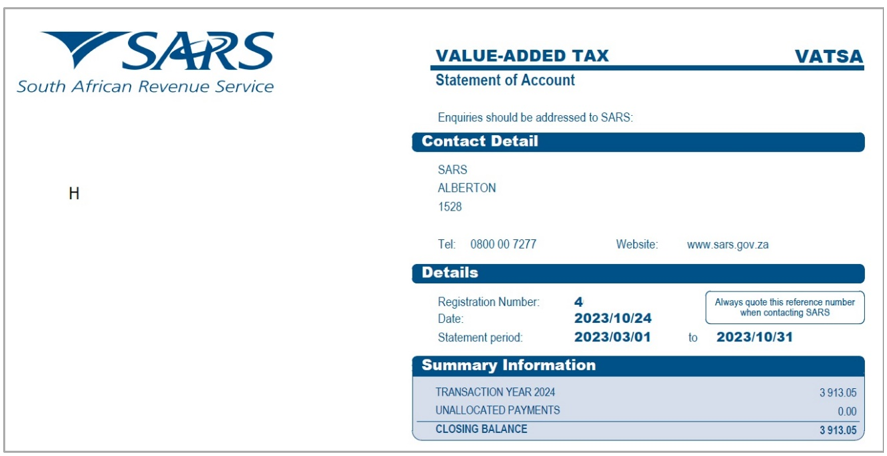

- The vendor will be able to open the VATSOA on eFiling in .pdf format and either save it on a local disk or print it to a local printer.

- Only a copy of the last requested VATSOA will be kept on eFiling. The next requested VATSOA will replace the current VATSOA on eFiling. Please print or save a copy of each VATSOA requested if you want to keep record of all the previous requests.

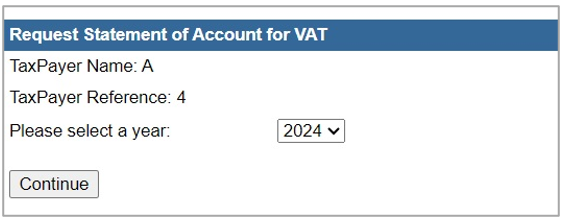

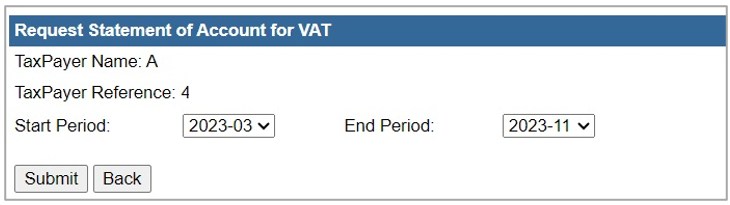

- On the VAT Work Page, select the option “Request Statement of Account”

- The following screen will be displayed:

- The vendor must be able to specify the transactional year (March to Feb) by selecting the appropriate year from a drop-down list.

- Once the vendor has selected the transactional year, the vendor must be able to specify the tax periods within that year by selecting the “Start Period” and the “End Period” from drop-down lists.

- Note: A tax period must be specified in the following format: (YYYYMM)

- Where a vendor requires a VATSOA for a single tax period, the vendor must be able to select the same tax period as the “From” and the “To” tax period. This statement will therefore display all the transactions related to this selected period.

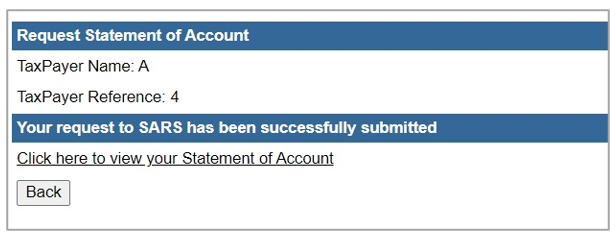

- The following screen will be displayed:

- The VATSOA will always be accompanied by notes to assist the reader on the interpretation of the account.

- The notes will provide explanations for tax periods indicated as those for which the vendor was not registered for VAT and those for which the vendor was registered but on which no transactions were processed.

- If the vendor was not registered at all for the specified statement period, the following message will be displayed on the screen: “You were not registered for VAT for the statement period specified by you. Press OK to specify a different statement period or press Cancel to cancel the request.”

- If the statement of account cannot be displayed, the following message will appear on the screen: “Due to a system problem we are unfortunately unable to issue your statement now. Processing your request can take up to 48 hours. The Statement of Account will be issued to you on eFiling within this period. Press OK”.

- Vendors must visit the Value Added Tax page on the SARS website www.sars.gov.za where they will find guides and FAQ’s to assist them in understanding the implications of the VAT rate increase on various types of transactions or contact the SARS Contact Centre on 0800 00 7277.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.