Purpose

The purpose of this webpage is to assist to complete an income tax return for individuals where there is income received or accrued to a deceased or insolvent estate.

This webpage is applicable to:

- executors representing individuals who have passed away on or after 1 March 2016, and

- appointed trustees/administrators where an individual becomes insolvent, and income accrued, or business conducted from the date of sequestration.

General Information

Deceased Estates

- Upon the death of an individual taxpayer, there are two types of assessments that must be considered: a pre-date of death assessment and a post-date of death assessment.

Pre-Date of Death Assessment

- This assessment is for income and deductions applicable to the taxpayer up to the date of his/her death.

- For assistance to complete an ITR12 return for income and deductions up to date of death please refer to the “Comprehensive Guide to the ITR12 Income Tax Return for Individuals” which is available on the SARS website (www.sars.gov.za).

Post-Date of Death Assessment – Deceased Estate

- This assessment is for income earned and deductions applicable to the deceased estate after date of death. For example this can include rental and/or interest income earned by the deceased estate.

- For individuals who have passed away on or after 1 March 2016, a second income tax registration is required for the deceased estate if taxable income accrued to the deceased estate. This registration will be triggered by either the executor of the deceased estate or by SARS.

- For more information please refer to the guide “How to Complete the Registration, Amendments and Verification Form (RAV01)” which is available on the SARS website.

- This webpage provides guidelines to help you declare post-death income, deductions, and CGT transactions on the income tax return.

Insolvency

When a natural person becomes insolvent, a possibility of dealing with three taxpayers might arise:

- the insolvent person for the period before sequestration (taxpayer 1)

- the insolvent estate (taxpayer 2).

- the insolvent person for the period after sequestration (taxpayer 3).

The effect of insolvency from an income tax point of view is to terminate the tax status of the insolvent person before sequestration and to substitute it with a new taxpayer from the date of sequestration, that is, the insolvent person after sequestration. In addition, the natural person (insolvent person after sequestration) receives a new taxpayer identity from the date of sequestration. Where there are assets in the insolvent person the assets will be disposed of under the insolvent estate.

A separate tax return must be submitted for each of the periods identified above.

The Insolvent Person Before Sequestration

- A final tax return must be completed for the insolvent person for the period from the first day of the year of assessment to the day before the date of sequestration.

- For assistance to complete an income tax return for income and deductions up to the period prior to the date of sequestration please refer to the “Comprehensive Guide to the ITR12 Income Tax Return for Individuals” which is available on the SARS website (www.sars.gov.za).

The Insolvent Estate

- The insolvent estate is registered as a separate tax entity and a new income tax reference number is allocated to it. The insolvent estate will come into being only if there are capital gains and losses that must be accounted for in case where assets are disposed to third parties.

- Its first period of assessment will commence on the date of sequestration and end on the last day of February that follows thereafter. The second and subsequent years of assessment will commence on 1 March of that year and end on the last day of February that follows thereafter. The period of assessment during which the estate is wound up will commence on 1 March of that year and end on the date when the estate is finally wound up.

The Insolvent Person After Sequestration

- An insolvent person who enters into employment or carries on a profession or business after his sequestration, is liable for tax on that income in its own right.

- The first tax period will run from the date of sequestration to the last day of that year of assessment.

- For assistance to complete an income tax return for income and deductions after the date of sequestration please refer to the “Comprehensive Guide to the ITR12 Income Tax Return for Individuals” which is available on the SARS website (www.sars.gov.za).

Return For Deceased or Insolvent Estate

- At present, the return that must be completed for deceased or insolvent estates is the same as the income tax return used for individuals. This means that there are certain sections on the return that are NOT applicable to a deceased or insolvent estates. This webpage specifies which sections these are and which options to select.

How to submit a Return for the Deceased or Insolvent Estate

An ITR12 return can be completed and submitted for a deceased or insolvent estate through any of the following channels:

- eFiling: If the deceased or insolvent estate is not registered for eFiling, please log on to www.sars.gov.za and proceed to the eFiling website to register. For any assistance with the registration process, please contact the SARS on 0800 00 7277.

- SARS Mobi App

- SARS Office: Make an appointment on the SARS website to visit your nearest SARS office and a SARS official will assist you.

Important Notes:

- In terms of section 240 of the Tax Administration Act No.28 of 2011, all Tax Practitioners who complete and submit tax returns on behalf of clients must be registered with a Recognised Controlling Body (RCB) and with SARS. Such tax practitioners have the full authority to prepare and submit tax returns on behalf of their clients. Practitioners that are not registered with the RCBs will not have this privilege.

- If services of a tax practitioner to submit the ITR12 return via eFiling/MobiApp and that tax practitioner is NOT registered with a Recognised Controlling Body, that tax practitioner will only be allowed to complete and save the electronic return but will not be able to submit the electronic return to SARS. The following options are available on eFiling for non-registered tax practitioners:

- ‘Save’ – This option allows the return to be saved without performing form validations and saves the incomplete return on eFiling for completion at a later stage.

- ‘Save for Filing’ – this option allows form validations to be performed when the income tax return is saved on eFiling. The prepared return will be available for retrieval at a SARS Office or to the executor/trustee or appointed agent via shared access for return submission on eFiling.

- To ensure that the tax return is submitted to SARS before the due date the executor/trustee or appointed agent must:

- Make an appointment on the SARS website to visit the nearest SARS Office where a SARS official will retrieve the completed return and submit it for processing; or

- Register for eFiling and request shared access from the tax practitioner.

Documentation required to complete the Return

Supporting documents are required to complete an income tax return. Below are examples of documentation/information that may be required:

- Certificates received for local interest income, foreign interest income, foreign dividend income, tax free investments.

- All information relating to local and foreign capital gains transactions.

- All information relating to the letting of assets.

- Financial statements for trading and farming activities (if applicable)

- Any other documents relating to income that must be declared or deductions that may be claimed.

All supporting documents must be retained for a period of five (5) years from the date of submission of the return, as SARS may request these documents to verify the information that was declared on the income tax return.

Creating an Income Tax Return for a Deceased or Insolvent Estate

- The Income Tax Return consists of several standard and comprehensive questions. The income tax return will be customised according to the answers to these questions.

- It is important to note that only certain income and deductions are applicable to a deceased or insolvent estate. Therefore, only the applicable sections of the return must be completed.

- From 2025 year of assessment onwards, on the header of the return, under the tax number and year of assessment, the following note will be displayed on the return: “Mark with an X”, if marked it means you confirm information or indicate in agreement.”

- The questions are discussed very briefly below. For further details, please refer to the applicable sections in this webpage.

Person making the Declaration

- From 2025 year of assessment onwards, the question will be displayed as “Mark with an ‘X’ if you are completing the return as a Tax Practitioner.”

- For the 2024 year of assessment, the question will be displayed as “Mark with an “X” if this declaration is made by a Tax Practitioner?”

- For the 2023 year of assessment and prior, the question will be displayed as “Is this declaration made by a Tax Practitioner?”

Investment Income

- ‘Did you receive any interest (local and foreign), distributions from a Real Estate Investment Trust (REIT)/Taxable local dividends, taxable foreign dividends and/or dividends deemed to be income in terms of section s8E & s8EA (excluding amounts received as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)?’ (Select ‘Y’ or ‘N’)

- If yes, indicate ‘Did you receive exempt local and/or foreign dividend income?’

- All gross receipts and accruals must be declared.

- If exempt local dividend income was received, the following sections must be completed on the return:

- ‘Amounts considered non-taxable’

- ‘Exempt Local Dividends’ field must be completed.

- If yes, indicate ‘Did you receive exempt local and/or foreign dividend income?’

- Mark with an “X” if you received or became entitled to any income as a beneficiary of a Trust, or income deemed to be yours under s7.

- If marked, indicate the number of Trust(s) applicable.

- The ‘Trust Income’ section will be added to the return and repeated according to the value entered in the field (maximum of 20 allowed).

- If more than 20 trusts, consolidate the additional amounts and add it to the amount in the 20th trust income section of the return.

- For 2024 year of assessment and prior, the question will be displayed as “Was any income distributed to you / vested in you as a beneficiary of a trust, or deemed to have accrued in terms of s7?”

- If yes, indicate the number of Trust(s) applicable?

- ‘Were there any transactions (contributions, transfers, withdrawals, income received/accrued) on any Tax Free Investments held by you during this year of assessment?’ (Select ‘Y’ or ‘N’)

- Indicate the number of Tax Free Investment(s)

- Note: This will be in respect of tax free investments that were in the name of the deceased or insolvent person that may be transferred directly to the deceased or insolvent estate.

- Maximum of 10 tax free investments can be declared on the return.

- If more than 10 tax free investments to declare, consolidate the additional amounts and add it to the amount in the 10th institution on the return.

Rental Income

- ‘Did you derive income from the letting of fixed property(ies) (excluding amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)?’

- If yes, indicate: ‘From how many separate rental properties did you derive income?’

- The section for ‘Local Rental Income from the letting of Fixed Property’ will be added to the return and will be repeated according to the number of rental activities inserted in this field.

- Note: A maximum of 20 rental properties can be declared on the return.

- If more than 20 rental properties to declare, consolidate the additional amounts and add it to the amount in the 20th rental property on the return.

Director or Member of Close Corporation

- ‘Mark with an ‘X’ if you are a director of a company or a member of a close corporation?’

- This question is not applicable to a deceased estate.

- Note: This question is applicable for an insolvent estate. Refer to section below for more information on the “same person rule” applicable to the Insolvent Person and Insolvent Estate.

Assets in excess of R50 million

- Mark with an “X” if you have assets which at market value are in excess of R50 million.

- If marked, complete the Statement of Assets and Liabilities section of the return.

Voluntary Disclosure Programme

- ‘Mark with an ‘X’ if any declaration in this return relates to an application made under the SARS Voluntary Disclosure Programme.’

- If marked, the Voluntary Disclosure Programme container will be added to the return.

Donations

- ‘Do you want to claim donations made to an approved organisation(s) in terms of s18A?’ (Select ‘Y’ or ‘N’)

- If yes, indicate ‘How many organisations did you donate to?’

- The maximum amount allowed is 99.

Other Income and Allowable Expenses

- ‘Mark with an ‘X’ if you received any other income (e.g. local business, trade, and professional income, but excluding amounts received/accrued as a beneficiary of a Trust(s) or deemed to have accrued in terms of s7) and/or incur any other allowable expenses (e.g. home office expenses) not addressed above.’

- If marked, a more comprehensive list of questions will display for completion.

Foreign Income (Excluding amounts received / accrued as a beneficiary of trust(s), or deemed to have accrued in terms of s7)

- ‘Did you receive any foreign income (including remuneration) apart from foreign interest and foreign dividend income and excluding foreign capital gain transactions?’ (Select ‘Y’ or ‘N’)

- From 2024 year of assessment onwards, the question will be displayed as “Did you receive any foreign income apart from foreign interest and foreign dividend income and excluding foreign capital gain transactions?”

Capital Gain / Loss (Excluding amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

- ‘Did you dispose of any local capital attracting capital gain or loss (including crypto asset(s))?’ (Select ‘Y’ or ‘N’).

- If yes, indicate ‘How many disposals (shares to be combined as one disposal) took place?’

- ‘Did you dispose of any foreign capital attracting capital gain or loss (including crypto asset(s))?’ (Select ‘Y’ or ‘N’)

- If yes, indicate ‘How many disposals (shares to be combined as one disposal) took place?’

- Each disposal must be declared separately. The return makes provision for a maximum 10 local and 10 foreign disposals.

- If the deceased estate disposed shares (and such shares are administered by one single administrator) and one advice was received for the disposal of these shares, the disposals can (for the completion of the return purposes) be regarded as one transaction. For further detail refer to the ‘Capital Gain/Loss’ section in this webpage.

Local Business Trade and Professional Income (Including crypto asset(s)) (Excluding amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

- ‘Did you derive income from local business trade or profession other than rental income from the letting of fixed property(ies)?’ (Select ‘Y’ or ‘N’)

- If yes indicate ‘How many separate trading activities did you carry on?’

- The return makes provision for a maximum of 8 trading activities to be declared.

- Note: Rental income must be declared separately under the section for ‘Local Rental Income from the letting of Fixed Property’.

- Ensure that the Partnership question is selected as ‘Yes’ to complete partnership information in this container.

Local Farming

- ‘Did you participate in any local farming operations?’

- Select ‘Y’ or ‘N’.

- ‘Did you participate in any farming partnership operations?’

- Select ‘N’ as this is not applicable to a deceased estate.

- This question would be applicable in the case of an insolvent estate. The estate of a partnership is separate to the estate of the individual partners. The sequestration of a personal estate of a partner result in a dissolution of the partnership by virtue of withdrawal of such partner’s share in the partnership.

- Ensure that the Partnership question is selected as ‘Yes’ to complete farming partnership information in this container.

Other Taxable Receipts and Accruals (Including remuneration from foreign employer(s) for services rendered in South Africa) (Excluding amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

- ‘Did you have any receipts and accruals not addressed by the previous questions but excluding amounts that you consider non-taxable?’ (Select ‘Y’ or ‘N’)

- If yes, the section for ‘Other Receipts and Accruals’ will be added to the return.

Foreign Tax Credits – s6quin <OR> Foreign Tax Refunded / Discharged

- ‘Were any foreign tax credits refunded/discharged during the year of assessment for which a rebate/deduction was allowed during a previous year of assessment?’ (Select ‘Y’ or ‘N’).

- If yes, the ‘Foreign Tax Credits Refunded/Discharged’ container will be displayed if year of assessment is 2017 onward, otherwise for 2016 year of assessment and prior the container ‘Foreign Tax Credits Refunded / Discharged by the government of a foreign country in respect of a rebate allowed by SARS in a previous year – s6quin’ for completion.

- Applicable for 2014 year of assessment onwards.

- For 2016 year of assessment and prior, the question will be displayed as ‘Will you be claiming any foreign tax credits in terms of s6quin (Foreign taxes on income from source within the Republic)?’

- If yes, the ‘Foreign Tax Credits’ container will be displayed for completion.

- If yes, the ‘Foreign Tax Credits Refunded/Discharged’ container will be displayed if year of assessment is 2017 onward, otherwise for 2016 year of assessment and prior the container ‘Foreign Tax Credits Refunded / Discharged by the government of a foreign country in respect of a rebate allowed by SARS in a previous year – s6quin’ for completion.

Amounts Considered Non-Taxable (Excluding amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

- ‘Did you receive any amount that you consider non-taxable?’ (Select ‘Y’ or ‘N’)

- If yes, the ‘Amounts considered non-taxable’ section must be completed on the return.

- This section makes provision for the declaration of the amount(s) that is exempt.

Recoupment of Venture Capital Company Shares Sold

- ‘Did you invest in SARS approved Venture Capital Companies in exchange for shares on or before 30 June 2021?’ (Select ‘Y’ or ‘N’)

- If yes, ‘Specify the number of investments made in SARS approved Venture Capital Companies’

- Note: The return caters for a maximum of 10. If the deceased or insolvent estate has invested in more than 10 venture capital companies, declare the total amount of all investments for the year of assessment and only complete the details of the top 10 investments on the return.

- This is not applicable from 2023 YOA and onwards.

- ‘Were any SARS approved Venture Capital Company shares sold during the year of assessment, for which a tax deduction was allowed?’ (Select ‘Y’ or ‘N’).

Other Deductions

- ‘Did you incur any expenditure that you wish to claim as a deduction that was not addressed by the previous questions (e.g. home office expenses)?’ (Select ‘Y’ or ‘N’).

- If yes, the section for “Other Deductions” will be added to the return.

Completing the Return

- The income tax return will be populated with demographic information, including passport information that is available to SARS. Please ensure that the information is correct.

- From 2025 year of assessment onwards, on the header of the return, under the tax number and year of assessment, the following note will be displayed on the header of the return: “Mark with an X”, if marked it means you confirm information or indicate in agreement.”

Taxpayer Information

- The following information will be pre-populated and cannot be amended on the return.

- “Income tax reference number”

- “Year of assessment”: This is the period commencing on 1 March of a particular year to the end of February of the following year.

- Personal details: You can only update some of the personal information via this section of the return. Complete the deceased taxpayer’s details if it is not pre-populated on the return or if the pre-populated information can be amended:

- “Surname”: This is a mandatory field that must be completed

- “First name”: This is a mandatory field that must be completed

- “Other name”: This is an optional field

- “Initials”: This is a mandatory field that must be completed.

- The following fields cannot be updated via the return. If the information is incorrect, please visit the nearest SARS Office to change it:

- Date of birth

- Identity number

- Passport number

- Passport Issue Date

- Passport Country

- “Marital status”: This field is mandatory on the return.

- This field will not be displayed if the form is completed for a deceased estate.

- Select the ‘Not married (Single, Divorced, Widow / Widower)’ option for the deceased estate.

- Note: Only the deceased’s portion of post date of death income must be declared on the return.

- Note: Indicate the correct marital status as the insolvent person and insolvent estate is regarded as the same person. Refer to section below for more information regarding the “Same person rule”.

- “Spouse details”: not applicable to the deceased estate.

- Indicate the Spouse details for the insolvent person, if applicable.

- Contact Details: the executor’s or appointed trustee/administrator details must be completed in this section.

- “Email”

- You are encouraged to provide an email address to assist SARS with its Go-Green initiative which intends to decrease the use of paper.

- If a valid email address is provided, the notice of assessment will be emailed.

- If you do not have an email address, indicate this by selecting the field ‘Mark here with an ‘X’ if you declare that you do not have an email address’.

- “Cell Number”

- You are encouraged to provide your cell number so that SARS can send communications to your cell number. For example: once your return is successfully processed, SARS will automatically send you an SMS with your assessment result.

- If you do not have a cell phone number, indicate this by selecting the field ‘Mark here with an ‘X’ if you declare that you do not have a cell phone number’.

- “Home Telephone Number”

- “Business Telephone Number”

- “Do you confirm that the email and telephone number(s) supplied are correct?”: Select Y or N

- “Email”

- Address Details: The appointed trustee/administrator/executor’s details must be completed in this section. If the residential address is the same as the postal address, it is not necessary to repeat the address details in the postal address section. You can mark the box indicating that the addresses are the same.

- Tax Practitioner Details (if applicable): If the return is completed by a tax practitioner the following details must be provided under the ‘Tax Practitioner Details’ section of the return:

- “Tax Practitioner Registration No.”: The first characters must be PR followed by 7 alphanumeric characters.

- “Tax Practitioner Telephone No.”

- “Tax Practitioner Email Address”.

- If you do not have an email address, indicate this by selecting the field ‘Mark here with an ‘X’ if you declare that you do not have an email address.

- “Note: If this declaration is not made by a Tax Practitioner, unselect the “X” on the first tab of this return (Standard Form Wizard).”

- For 2024 year of assessment and prior, the “Note” will be displayed as ‘If this declaration is not made by a Tax Practitioner, unselect the “X” on the first page of this return.’

Bank Details

- SARS has adopted a policy of issuing all refunds electronically. It is therefore imperative that the bank account details are correct.

- The banking details of the estate must be inserted in this section. If the banking details are available to SARS, it will be pre-populated on the return.

- Click the ‘Select from bank accounts’ button to add from existing estate bank account details that SARS have on record.

- Upon selecting this button, the following message will be displayed “Editing this data can cause an error on your submission. Do you want to proceed?” Select ‘Yes’ or ‘No’.

- If ‘Yes’ is selected, a list of masked bank details will be displayed to select.

- If ‘No’ is selected, the message will close.

- If there is no bank details on record, the following message will be displayed “No bank accounts found. Please continue to add a bank account.”

- Upon selecting this button, the following message will be displayed “Editing this data can cause an error on your submission. Do you want to proceed?” Select ‘Yes’ or ‘No’.

- Click the ‘Add account details’ button on the Bank Details container header to capture new bank details.

- Upon selecting this button, the following message will be displayed “Editing this data can cause an error on your submission. Do you want to proceed?” Select ‘Yes’ or ‘No’.

- If ‘Yes’ is selected and there is already previous bank details, that current bank details will be displayed, and the Bank Account Details fields will be available to capture the new estate bank details as provided by the appointed trustee/administrator/executor.

- If there is no bank details, the Bank Account Details fields will be available to capture new estate bank details.

- Once the bank details have been captured correctly and submitted, the bank details will be verified and the following message will be displayed “Your bank account details will be sent for verification. If the verification fails, SARS will ask you to submit supporting documents.”

- Upon selecting this button, the following message will be displayed “Editing this data can cause an error on your submission. Do you want to proceed?” Select ‘Yes’ or ‘No’.

- For 2024 year of assessment and prior, the “Edit” button will be displayed to update bank account details.

Bank Account Holder Declaration

- ‘Bank Account Holder Declaration’ – select one of the following:

- “I use South African bank accounts”.

- “I use a South African bank account of a 3rd party”

- “I declare that I have no South African bank account”

- ‘Reason for No Local / 3rd Party Bank Account’ – select one of the following:

- “Non-resident without a local bank account”

- “Insolvency/Curatorship”

- “Deceased Estate”

- “Shared Account”

- “Income below tax threshold / Impractical”

- “Statutory restrictions”

- “Minor child”

Bank Account Details

- ‘Bank Account Status’ – this field is for SARS use and will be prepopulated by the SARS system.

- ‘Account number’ – enter the bank account number.

- If bank account details was selected from the existing list of bank details, the masked bank details will be displayed, and you must recapture the corresponding bank account number.

- If the account number does not match the masked bank account number, the following error message will be displayed “Please note that the account number you have captured does not match account number selected. Either recapture the correct number or use the Add bank account details button to supply new bank details.”

- If bank account details was selected from the existing list of bank details, the masked bank details will be displayed, and you must recapture the corresponding bank account number.

- ‘Branch number’, ‘Bank Name’ and ‘Branch Name’

- For eFiling submissions, a drop-down list containing bank names has been included on the income tax return.

- Select the applicable bank name. Once selected, the ‘branch name’ and the ‘branch number’ fields will be automatically inserted on the return.

- If you cannot find the bank name on the list, select ‘Other’ and complete all the necessary fields.

- ‘Account type’ – Indicate if the account is a cheque, savings or transmission account.

- ‘Account holder name’ – please insert the account holder name as registered at the bank.

- Once all the changes have been captured, click ‘Update’ to proceed or ‘Cancel’ to close the editing of the bank details.

- The following note is displayed on the return “All changes will be verified before updating your banking profile. SARS will let you know if you need to come into a SARS branch with supporting documents. Bank details are required for refunds.”

- ‘Agreement Statement’

- Mark the corresponding statement on the return with an ‘X’.

- This is to declare that the information provided is true and correct in every respect.

Documentation required for Bank Detail Changes

If you are amending banking details on the Income Tax Return, you may be required to submit supporting documentation to verify the banking detail changes. SARS will notify you if verification is required. For more information on how to change bank details for estates, refer to the Estates webpage on the SARS website www.sars.gov.za.

Banking detail changes cannot be made via:

- Fax;

- Post; or

- Telephonically.

Should you require any further information concerning banking detail changes for estates, you can:

- Refer to the ‘Change of Banking Details Guide’ on the SARS website www.sars.gov.za

- Call the SARS on 0800 00 7277

- Make an appointment on the SARS website to visit your nearest SARS Office.

Taxpayer Information: Income

General

Income flows to a deceased estate in two ways –

- a deceased estate will be taxed on any income that is received by or accrued to or in favour of any person in the capacity of the Executor, and

- any other amount which would have been income in the hands of the deceased person had that amount been received by or accrued to or in favour of that deceased person during his or her lifetime.

The sections below provide a brief overview of some of the types of income that flow to a deceased or insolvent estate.

Person before Sequestration and Insolvent Estate – The “One and the Same Person” Rule

Section 25C deems the estate of the person before sequestration and that person’s insolvent estate to be one and the same person for purposes of –

- the amount of any allowance, deduction or set-off to which the insolvent estate may be entitled;

- any amount which is recovered or recouped by or otherwise required to be included in the income of the insolvent estate; and

- any taxable capital gain or assessed capital loss of the insolvent estate.

This, amongst other things, means that:

- An assessed loss incurred by the insolvent person can be set off against the insolvent estate’s income.

- Expenditure and allowances claimed by the insolvent person before the date of sequestration can be recouped in the insolvent estate, for example, depreciation allowances and bad debts previously written off as bad.

- Debts incurred in the income of the insolvent person before the date of sequestration can be claimed as bad debts by the insolvent estate.

- The write-off of assets and allowances can continue to be claimed in the insolvent estate.

- Closing stock taken into account in the insolvent person’s taxable income calculation may be taken into account as opening stock in the insolvent estate’s first taxable income calculation.

- Any amount that would otherwise be required to be included in the income of the insolvent person may be included in the income of the insolvent estate, for example, the amount allowed as an allowance for doubtful debts or the allowance for future expenditure under section 24C.

- The reduction or cancellation of debt provisions in section 19 must be kept in mind if the insolvent estate reduces a debt by more than the amount of consideration given for that reduction, for example in terms of a compromise with a creditor.

- A disposal does not take place when the insolvent person’s assets pass from the insolvent person to the insolvent estate on sequestration.

- Capital gains and capital losses arising because of disposals by the insolvent estate to third parties will be included in the hands of the insolvent estate but will take into account events that occurred in the insolvent’s hands, for example previous depreciation allowances.

- As assessed capital loss incurred by the insolvent person before the date of sequestration may be set-off against capital gains arising in the insolvent estate.

For more information, refer to “Interpretation Note: 8 Insolvent Estates of Natural Persons” on the SARS website.

Investment Income (Excl. Exempt Dividends and any amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

- Note: Only income that received by or accrued to or in favour of the deceased or insolvent estate must be declared on the return.

- For 2022 YOA and prior, the communal indicator will be applied to the Investment container.

Exemption for Investment Income

- Section 10(1)(i) provides only for an exemption of interest received from a source in the Republic.

- The exemption applicable for a deceased estate from the 2015 year of assessment onwards is R23 800.

- The following amounts must be declared in the “Amounts considered non-taxable” section of the return:

- Exempted local dividends income in terms of section 10(1)(k)(i)

- Exempted foreign dividends in terms of section 10B(2).

- Interest earned by a non-resident in terms of s10(1)(h) – only applicable in the abovementioned container for 2020 year of assessment and prior.

- Section 10(1)(h) provides for an exemption in respect of SA source interest received or accrued by or to a person that is a not a resident. The exemption does not apply in certain cases.

- Note: Distributions from a Real Estate Investment Trust (REIT) do not qualify for exemption.

Local Interest (Excluding SARS Interest)

- All local interest (excluding SARS Interest) accrued/received by the deceased or insolvent estate must be inserted next to source code 4201.

- This field will not be pre-populated for deceased and insolvent estates.

- Mark with an “X” if you have incurred allowable interest in the production of interest received or accrued.

- If marked, the ‘Allowable interest expenses incurred in the production of interest received or accrued’ field will be pre-populated with the aggregate amount(s) entered in the corresponding field(s) on transactional level.

- The aggregate of the interest expenses incurred from the production of all the interest received, accrued or earned from different accounts will be populated in this Bank charges must be excluded.

- Applicable from 2026 year of assessment onwards.

- Expenses claimed against interest received cannot create a loss.

- Applicable from 2021 Year of Assessment.

- Refer to Practice Note 31 for more information.

- If marked, the ‘Allowable interest expenses incurred in the production of interest received or accrued’ field will be pre-populated with the aggregate amount(s) entered in the corresponding field(s) on transactional level.

- Interest Earned From and Interest Earned To (CCYY/MM/DD)

- Fields are displayed from the 2024 year of assessment onwards on all original forms.

- If the question “Did you receive any interest (local and foreign), distributions from a Real Estate Investment Trust (REIT)/Taxable dividend, and / or dividends deemed to be income in terms of s8E & s8EA (excluding amounts received as a beneficiary of a trust(s), or deemed to have accrued in terms of s7) from an RSA source?” is marked “Yes” and the return is coded deceased estate, the field will be open for completion on a YOA after the Taxpayer passed on.

- The deceased estate “Interest earned from” and “Interest earned to” field must only display for the year of assessment after the year of assessment the taxpayer passed on.

- Example: If the taxpayer date of death is 12/05/2025 = 2026 YOA and received interest income in the 2027 YOA, the new fields will be displayed in the 2027 YOA.

- Note: Where there is multiple interest earned, complete the earliest interest earned date and latest interest earned date.

- Fields are displayed from the 2024 year of assessment onwards on all original forms.

- Local Interest (excluding SARS Interest) (Own)

- Complete the Institution, Account No, Allowable interest expenses incurred in the production of interest received or accrued and Amount fields if you have local interest to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (e. married in community of property)”

- If marked, ensure that you have a Will and/or Antenuptial Contract in place to support this declaration.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the interest exceeding 30.

- Where there is pre-populated information, taxpayers who are coded (i.e., Deceased Estate, Deceased Person, Insolvent person and Insolvent estate) will be able edit the information.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (e. married in community of property)”

- Complete the Institution, Account No, Allowable interest expenses incurred in the production of interest received or accrued and Amount fields if you have local interest to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Local Interest (excluding SARS Interest) (Spouse)

- Complete the Account Holder ID number, Institution, Account No, Amount, and Allowable interest expenses incurred in the production of interest received or accrued fields.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the interest exceeding 30.

- Where there is pre-populated information, taxpayers who are coded (i.e., Deceased Estate, Deceased Person, Insolvent person and Insolvent estate) will be able edit the information.

- Complete the Account Holder ID number, Institution, Account No, Amount, and Allowable interest expenses incurred in the production of interest received or accrued fields.

- SARS Interest received during this year of assessment by the deceased or insolvent estate must be inserted next to source code 4237.

- This field will not be pre-populated for deceased and insolvent estates.

- SARS Interest received during this year of assessment (Own)

- Complete the Tax Type, Tax Reference No and Amount fields for SARS interest received during the year.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the SARS interest exceeding 30.

- Complete the Tax Type, Tax Reference No and Amount fields for SARS interest received during the year.

- SARS Interest received during this year of assessment (Spouse)

- Complete the Account Holder ID number, Tax Type, Taxpayer Ref No and Amount fields.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the interest exceeding 30.

- Complete the Account Holder ID number, Tax Type, Taxpayer Ref No and Amount fields.

Foreign Interest and Foreign Tax Credits on Foreign Interest

- For 2022 YOA and prior, the container heading will be displayed as “Foreign Interest – Rands only – unless cents specified”.

- Mark with an “X” if you have incurred allowable interest in the production of interest received or accrued.

- If marked, the ‘Allowable interest expenses incurred in the production of interest received or accrued’ field will be pre-populated with the aggregate amount(s) entered in the corresponding field(s) on transactional level.

- Applicable from 2026 year of assessment onwards.

- All ‘foreign interest’ received by or accrued to or in favour of the deceased or insolvent estate must be inserted next to source code 4218.

- This field will not be pre-populated for deceased and insolvent estates.

- “Foreign tax credits on foreign interest”: If any withholding tax was paid on the foreign interest received, this amount will appear on the certificate received from the institution administering the investment. The gross amount of withholding tax must be declared next to the source code 4113.

- This field will not be pre-populated for deceased estates.

- Allowable interest expenses incurred in the production of interest received

- This field is effective from 2021 year of assessment onwards and will not be pre-populated.

- Expenses incurred in the production of foreign interest will be limited to the interest earned.

- Foreign Interest and Foreign Tax Credits on Foreign Interest (own)

- Complete the Institution, Account No and Foreign Interest Amount (“Amount” only will be displayed for 2022 YOA and prior), and Foreign Tax Credit on Foreign Interest Amount and Allowable interest expenses incurred in the production of interest received or accrued fields if you have foreign interest to declare that, by clicking the ‘Add’ button. The ‘Delete’ button will display manually captured information.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (e. married in community of property)”

- If marked, ensure that you have a Will and/or Antenuptial Contract in place to support this declaration.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the foreign interest exceeding 30.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (e. married in community of property)”

- Complete the Institution, Account No and Foreign Interest Amount (“Amount” only will be displayed for 2022 YOA and prior), and Foreign Tax Credit on Foreign Interest Amount and Allowable interest expenses incurred in the production of interest received or accrued fields if you have foreign interest to declare that, by clicking the ‘Add’ button. The ‘Delete’ button will display manually captured information.

- Foreign Interest and Foreign Tax Credits on Foreign Interest (Spouse)

- Complete the Account Holder ID number, Account No, Foreign Interest Amount and Foreign Tax Credit on Foreign Interest Amount and Allowable interest expenses incurred in the production of interest received or accrued fields if you have foreign tax credits on foreign interest to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display manually captured information.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the foreign tax credits on foreign interest exceeding 30.

- Complete the Account Holder ID number, Account No, Foreign Interest Amount and Foreign Tax Credit on Foreign Interest Amount and Allowable interest expenses incurred in the production of interest received or accrued fields if you have foreign tax credits on foreign interest to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display manually captured information.

Gross Foreign Dividends Subject to SA Normal Tax and Foreign Tax Credits on Foreign Dividends

- For 2022 YOA and prior, the container heading will be displayed as “Gross Foreign Dividends subject to SA normal tax”.

- The amount in respect of “Gross foreign dividends subject to SA normal tax” must be inserted next to source code 4216. The exemption in terms of section 10B(3) on foreign dividends subject to SA normal tax will be applied programmatically by SARS. The exemption is calculated in terms of the formula: A = B x C (ratio of 25/45).

- This field will not be pre-populated for deceased and insolvent estates.

- “Foreign tax credits on foreign dividends”: If any withholding tax was paid on the foreign dividend received, this amount will appear on the certificate received from the institution administering the investment. The gross amount of withholding tax must be declared next to source code 4112.

- This field will not be pre-populated for deceased and insolvent estates.

- Gross Foreign Dividends subject to SA normal tax and Foreign Tax Credits on Foreign Dividends (Own)

- Complete the Institution, Account No and Gross Foreign Dividends subject to SA normal tax Amount and Foreign Tax Credits on Foreign Dividends Amount fields if you have foreign dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (if married in community of property)”

- If marked, ensure that you have a Will and/or Antenuptial Contract in place to support this declaration.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the foreign dividends exceeding 30.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (if married in community of property)”

- Complete the Institution, Account No and Gross Foreign Dividends subject to SA normal tax Amount and Foreign Tax Credits on Foreign Dividends Amount fields if you have foreign dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Gross Foreign Dividends subject to SA normal tax and Foreign Tax Credits on Foreign Dividends (Spouse)

- Complete the Account Holder ID Number, Institution, Account No, Gross Foreign Dividends subject to SA normal tax and Foreign Tax Credits on Foreign Dividends Amount fields if you have Foreign tax credits on such foreign dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the foreign tax credits on such foreign dividends exceeding 30.

- Complete the Account Holder ID Number, Institution, Account No, Gross Foreign Dividends subject to SA normal tax and Foreign Tax Credits on Foreign Dividends Amount fields if you have Foreign tax credits on such foreign dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

Distribution from Real Estate Investment Trust(s) (REIT) / Taxable Local Dividends

- Real Estate Investment Trusts (REITs) are companies listed on the JSE that manage a portfolio of immovable property assets. The taxation of a REIT is regulated in section 25BB on the Income Tax Act. Any person can invest in a REIT. Dividends distributed by a REIT is subject to normal tax in the hands of the shareholder (s10(1)(k)(i)(aa) of the Income Tax Act) but is exempt from Dividends Tax (refer to section 64F(l) of the Income Tax Act).

- Insert the deceased or insolvent estate’s portion of income from a Real Estate Investment Trust (REIT) / Taxable Local Dividends next to source code 4238.

- This field will not be pre-populated for deceased and insolvent estates.

- Distribution from REIT / Taxable Local Dividends (Own)

- Complete the Institution, Account No and Amount fields if you have REIT/Taxable Local Dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (if married in community of property)”

- If marked, ensure that you have a Will and/or Antenuptial Contract in place to support this declaration.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the REIT exceeding 30.

- “Mark with an ‘X’ if any of the amounts declared by you should be excluded from the communal estate (if married in community of property)”

- Complete the Institution, Account No and Amount fields if you have REIT/Taxable Local Dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Distribution from REIT / Taxable Local Dividends (Spouse)

- Complete the Account Holder ID Number, Institution, Account No, Amount fields if you have REIT/Taxable Local Dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the REIT exceeding 30.

- Complete the Account Holder ID Number, Institution, Account No, Amount fields if you have REIT/Taxable Local Dividends to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

Dividends Deemed to be Income in terms of S8E and S8EA

- Capture the amount for “Dividends deemed to be income in terms of s8E and s8EA” next to source code 4292.

- This field will not be pre-populated for deceased and insolvent estates.

- Dividends Deemed to be Income in terms of S8E and S8EA (Own)

- Complete the Institution, Account No and Amount fields if the taxpayer have dividends deemed to be income in terms of s8E and s8EA to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the dividends deemed to be income in terms of s8E and s8EA exceeding 30.

- Complete the Institution, Account No and Amount fields if the taxpayer have dividends deemed to be income in terms of s8E and s8EA to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Dividends Deemed to be Income in terms of S8E and S8EA (Spouse)

- Complete the Account Holder ID Number, Institution, Account No and Amount fields if the taxpayer have dividends deemed to be income in terms of s8E and s8EA to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

- Maximum of 30 sub-fields will be allowed and the 30th sub-field should be a consolidated aggregate of the dividends deemed to be income in terms of s8E and s8EA exceeding 30.

- Complete the Account Holder ID Number, Institution, Account No and Amount fields if the taxpayer have dividends deemed to be income in terms of s8E and s8EA to declare, by clicking the ‘Add’ button. The ‘Delete’ button will display for manually captured information.

Foreign Income (Excl. Investment Income, CGT and amounts received / accrued as a beneficiary of a trust(s), or deemed to have accrued in terms of s7)

Complete the amounts next to the applicable source codes in this section. Use the amounts in the foreign financial statements/certificates received.

The following codes appear in this section:

- 4288: Foreign Rental (from the letting of fixed property(ies)) – Profit

- 4289: Foreign Rental (from the letting of fixed property(ies)) – Loss

- 4121: Foreign Tax Credits on Foreign Rental Income

- 4222: Business/trading – profit (excluding rental income derived from the letting of fixed property(ies))

- 4223: Business/trading – loss (excluding rental income derived from the letting of fixed property(ies))

- 0192: Farming – profit

- 0193: Farming – loss

- 4278: Royalties – profit

- 4279: Royalties – loss

- 4228: Other – Profit (Excluding Rental from the letting of fixed property(ies))

- 4229: Other – Loss (Excluding Rental from the letting of fixed property(ies))

- 4230: Controlled Foreign Company (CFC) – share of profit.

- Only the deceased estate’s share of the profit from a CFC must be completed here.

- 4235: ‘Income received from foreign employment services reflected on a South African IRP5/IT3(a) certificate that was subjected to tax outside the RSA and the s10(1)(o)(ii) exemption does not apply’.

- For year of assessment 2020 and prior, the field will be displayed as ‘Income reflected on a South African IRP5/IT3(a) certificate, that was subject to tax outside the RSA.

- This amount is not applicable to an insolvent estate.

- 4111: Other Foreign Tax Credits (excluding rental from letting of property(ies)

- This field will display for year of assessment 2020 and prior and 2024 year of assessment onwards.

- From 2021 to 2023 year of assessment the field will be displayed as ‘Other foreign tax credits (excluding rental from letting of property(ies) and Income received from foreign employment services and not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(ii) exemption applies)’

- 4298: Income received from foreign employment services not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(ii) exemption does not apply.

- This field will be displayed from 2023 year of assessment onwards.

- 4299: Income received from foreign employment services not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(i) exemption applies.

- This field will be displayed from 2023 year of assessment onwards.

- From 2024 year of assessment, this field will be moved to the “Qualifying criteria for s10(1)(o)(i)” container.

- 4304: Income received from foreign employment services not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(i) exemption does not apply.

- This field will be displayed from 2023 year of assessment onwards.

- 4259: Income received from foreign employment services not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(ii) exemption applies.

- This field will display from 2021 year of assessment onwards.

- If the amount entered is greater than zero, the following field will be displayed and mandatory to complete.

- Foreign tax credit on income received from foreign employment services not reflected on a South African IRP5/IT3(a) certificate, subject to tax outside RSA and the s10(1)(o)(ii) exemption applies

- This field will only display from 2021 year of assessment onwards.

- From 2024 year of assessment, these two fields will be moved to the “Qualifying Criteria for s10(1)(o)(ii) exemption ( excluding s8A/8C gains and dividends)” container .

Note that all foreign income must be declared in South African currency.

Although financial statements that are drawn up in another currency will be acceptable as supporting documents, if so requested by SARS, it must be translated to South African currency.

Foreign Currency Translation

- A natural person (that is a resident) who derives income measured in a foreign currency may, in translating the taxable income to Rands, make an election between either:

- The spot rate

- The average exchange rate for the relevant year of assessment.

- Where the information supplied is in a foreign currency, the average exchange rates can be used for conversion purposes to South African currency.

- The average exchange rates can be obtained on the SARS website (www.sars.gov.za). Note that only the main currencies are addressed in this webpage. If the exchange rates of another country are applicable, it can be obtained from any of the local merchant banks.

Proof of Payment for Foreign Taxes

The following will be accepted as proof of payment of foreign taxes if requested by SARS:

- Where foreign tax has been withheld at source – the original documentation issued by the applicable institution.

- Where foreign tax has not been withheld at source – an assessment or receipt issued by the relevant tax authority.

Limitation of foreign credits (section 6quat)

- Foreign tax credits will be limited to the South African tax payable in relation to the foreign income received by applying the following formula:

![]()

For further details refer to “Interpretation Note No 18: Rebates and Deduction for Foreign Taxes on Income” on the SARS website www.sars.gov.za.

Foreign Tax Credits

The foreign tax that is paid on income that is taxable in South Africa may be deducted from the South African tax on that income. This is done in terms of the following provisions:

- Section 6quat:

- This refers to a foreign tax rebate in respect of foreign tax on income from a non-South African source.

- Section 6quat(1) provides relief for foreign taxes proved to be payable on income derived from a foreign source that is included in a resident’s taxable income.

- Foreign taxes falling within this category do not qualify for the section 6quat(1C) deduction.

- Section 6quat1(C)

- Under section 6quat(1C), a resident may claim foreign taxes, that do not qualify for the section 6quat(1) rebate, as a deduction in determining taxable income. That is, essentially, foreign taxes payable on South African-sourced amounts.

For further details refer to “Interpretation Note No 18: Rebates and Deduction for Foreign Taxes” on Income on the SARS website.

Foreign Tax Credits – Refunded / Discharged

A section 6quat rebate/deduction reduces the taxable income of a South African resident. This in turn reduces the normal tax liability of the taxpayer. Where a South African resident claimed a rebate/deduction for foreign tax paid/payable in terms of section 6quat and in a subsequent year of assessment the foreign tax was refunded or the taxpayer was discharged from the applicable tax liability, then the amount that was discharged (limited to the amount that was originally claimed) will be deemed to be an amount of normal tax payable by that taxpayer in the subsequent year of assessment.

Complete the following fields:

- “Specify the portion of the amount so refunded/discharged as was previously allowed by SARS as a rebate”

- “Specify the portion of the amount so refunded / discharged as was previously allowed by SARS as a deduction in terms of s6quat(1C)”.

- Insert the amount next to source code 4249.

Trust Income

The section ‘Trust Income – Income distributed to you/ vested in you as a beneficiary of a trust or deemed to have accrued in terms of s7’ will display for 2017 YOA onwards.

If a taxpayer received income from a trust or income accrued to him/her as a beneficiary of a trust, or a taxpayer has a vested interest in an asset held by a trust or a capital gain is made by a trust vested in the taxpayer; the income received, accrued or deemed to have been received/accrued from the trust must be declared on the return.

- From the 2017 year of assessment onward, this income must be declared separately in this section of the return.

- For years prior to 2017, this income must be declared in the specific part of the return relating to the type (source) of income prior to the distribution by the trust (e.g. interest income received must be declared next to source code 4201 in the ‘Investment Income’ section of the return).

Capture the following information:

- ‘Trust Name’

- ‘Trust Registration Number’

- ‘Trust Tax Reference Number’

- ‘Interest Earned From’ and ‘Interest Earned To’ (CCYY/MM/DD)

- The deceased estate “interest earned from” and “Interest earned to” field must only display for the year of assessment after the year of assessment the taxpayer passed on.

- Interest Earned From date field cannot be later than the date specified in the Period Interest Earned To field.

- From 2024 year of assessment, the following note will be displayed “Where there is multiple interest earned, complete the earliest interest earned date and latest interest earned date.”

- The deceased estate “interest earned from” and “Interest earned to” field must only display for the year of assessment after the year of assessment the taxpayer passed on.

- ‘Mark here with an “X” if this amount should be excluded from the communal estate (i.e. married in community of property)’

- ‘Details of Local Income’

- ‘Local Remuneration’

- If an income amount is entered, insert the income source code.

- The source code must fall within the following range: 3601-3606, 3616, 3617 and 3667.

- ‘Local Annuities’

- If an income amount is entered, insert the income source code (3610 or 3611).

- ‘Local Interest’ – 4201

- SARS Interest – 4237

- ‘Distribution from Real Estate Investment Trust(s) (REIT) / Taxable Local Dividends’ – 4238

- ‘Local Capital Gain/Loss’

- If an amount is entered, insert the source code (4250 or 4251)

- ‘Local Rental Income from the letting of fixed property(ies)’ – 4210

- ‘Dividends deemed to be income in terms of s8E and s8EA’ – 4292

- ‘Local Business and trading Income (excluding Rental Income from letting of fixed property(ies) and income from Farming Operations)’

- If an amount is entered, insert the source code.

- ‘Income from Local Farming Operations (IT48)’

- If an amount is entered, insert the source code.

- This amount will auto-populate in the new ‘Income from Local Farming Operations (IT48) distributed by a trust(s)’ on the IT48.

- ‘Deemed Annuity’ – 3611

- ‘Other Local Income’

- If an amount is entered, insert the source code.

- Details of Foreign Income

- ‘Foreign Interest’ – 4218

- ‘Foreign Tax credits on foreign Interest’- 4113

- ‘Foreign Dividends’ – 4216

- ‘Foreign Tax credits on foreign dividends’ – 4112

- ‘Foreign Capital Gain/Loss’

- If an amount is entered, insert the source code (4252 or 4253)

- ‘Foreign Tax credits i.r.o capital gain/loss’ – 4114

- ‘Foreign Farming’ – 0192

- ‘Foreign tax credits on foreign farming income’ – 4119

- ‘Other Foreign Income’ – 4220

- ‘Imputed Net Income from Controlled Foreign Companies (CFC)’ – 4276

- ‘Foreign Tax Credit on Imputed Net Income from Controlled Foreign Companies (CFC)’ – 4122

- ‘Foreign tax credits on foreign other income’ – 4110

- ‘Amount Considered Non-Taxable’

- ‘Local Remuneration’

Capital Gains Tax (CGT)

- CGT provisions became effective from 1 October 2001. In order to give effect to the proposals relating to Capital Gain Tax (CGT), an Eighth Schedule was added to the Income Tax Act. This schedule determines a taxable capital gain or assessed capital loss and section 26A of the Act provides that a taxable capital gain is included in taxable income.

- For detailed information on CGT, please refer to the “Comprehensive Guide to Capital Gains Tax” which is available on the SARS website.

- Determining a capital gain or a capital loss: A CGT event is triggered by the disposal of an asset. Unless such disposal (or deemed disposal) occurs, no gain or loss arises. CGT applies to all assets disposed of on or after 1 October 2001 (valuation date). Only the gain or loss attributable from 1 October 2001 to date of disposal will be subject to the CGT.

- An asset is defined as widely as possible and includes any property of any nature and any interest therein

- A disposal covers any event, act, forbearance, or operation of law, which results in a creation, variation, transfer, or extinction of an asset. It also includes certain events treated as disposals, such as the change in the use of the asset. (Paragraphs 65 and 66 of the Eighth Schedule to the Income Tax Act make provision for the election of tax relief in respect of reinvestment and involuntary disposals in respect of assets disposed of on or after 22 December 2003. Once an asset is disposed of, the amount that is received by (or which accrues to) the seller of the asset constitutes the proceeds/income from the disposal.

- The base cost of the asset is generally the expenses that were actually incurred in obtaining the asset, together with the following:

- Expenses directly related to the asset’s improvement

- Expenses and direct costs in respect of its acquisition and disposal of the asset

- Certain holding costs.

- The base cost does not include any amounts otherwise allowed as a deduction for income tax purposes.

Deceased Estate

- In terms of section 9HA(1) of the Income Tax Act, a person who dies on or after 1 March 2016 is deemed to have disposed of his/her assets at the date of death. The deceased person is regarded as having disposed of his/her assets for an amount equal to the market value on the date of death. This rule does not apply in the following circumstances:

- assets that are awarded to the surviving spouse (s9HA(2)). See discussion below;

- a long term insurance policy of the deceased, of which the capital gain or loss would have been disregarded in terms of paragraph 55 of the Eight Schedule;

- An interest of the deceased in a pension, pension preservation, provident, provident preservation, retirement annuity fund, or any fund, arrangement or instrument situated outside South Africa which provides similar benefits, if any capital gain or loss that would have resulted would have been disregarded in terms of paragraph 54 of the Eight Schedule.

- For the surviving spouse to qualify for the exclusion stated in section 9HA(1), the surviving spouse:

- must be a resident;

- must acquire the asset:

- by intestate or testamentary succession;

- as a result of a redistribution agreement between heirs and legatees; or

- in settling an accrual claim (section 3 of Matrimonial Property Act No 88 of 1984).

- The value to be placed on the disposal of the asset will be an amount received or accrued equal to:

- the expenditure incurred by the deceased person (s9HA(2)(b)) and any expenditure incurred by the deceased estate on that asset (s25(4)(b)) or

- the base cost of asset as laid out in paragraph 20 of the Eight Schedule.

- In addition, the surviving spouse:

- acquires the asset on the same date as the deceased person or the deceased estate;

- incurs further expenditure on the date and same currency in which it was incurred by the deceased person or deceased estate; and

- uses that asset in the same manner as the manner in which that asset had been used by the deceased person and the deceased estate.

- The value to be placed on the disposal of the asset will be an amount received or accrued equal to:

- Where an asset is transferred directly to an heir or legatee by a deceased person, the heir or legatee must be treated as having acquired that asset at the market value (paragraph 31 of Eight Schedule) on at date of death of the deceased person (s9HA(3)).

- Where the deceased estate disposes of an asset to an heir or legatee, that disposal is for an amount received or accrued equal to the amount of expenditure incurred by the deceased estate; and the heir or legatee acquires that asset at the same value (s25(3)).

- A new time of disposal rule was inserted in terms of section 25(3)(c) on 19 January 2022, but only comes into operation on 1 March 2022 and applies in respect of liquidation and distribution accounts finalised on or after that date. Section 25(3)(c) provides that a deceased estate must be treated as having disposed of that asset on the earlier of the date on which that asset is disposed of or on which the liquidation and distribution account becomes final.

- A deceased estate is regarded as a natural person (s25(5)(a)) except from rebates (s6) and medical credits (ss6A and 6B). This means that the deceased estate is entitled to the same exclusions and relief provisions below as a natural person:

- annual exclusion of R40 000 (prior to 1 March 2016, this was R30 000);

- inclusion rate of 40% (prior to 1 March 2016, this was 33.3%);

- primary residence exclusion;

- personal-use asset exclusion;

- small business asset relief (paragraph 57 of the Eight Schedule) – this is the R1.8 million lifetime exclusion (the remainder of the exclusion amount not utilised by the deceased person);

- Section 25(5)(b) provides that if the deceased person was a resident at the time of his or her death, the deceased estate will also be regarded as a resident.

- The annual exclusion for individuals has been increased from R300 000 to R440 000 in the year of death.

- Where a taxable capital gain results from the disposal of assets from the deceased person to the deceased estate (s9HA(1)), and the tax calculated exceeds 50% of the net value of the deceased estate (i.e. the value of estates as determined in terms of s4 of the Estate Duty Act, before taking into account the amount of tax calculated on the taxable gain and before deducting the R3.5 million abatement); and the executor is required to dispose (sell) of the asset of the estate to pay this tax:

- The heir or legatee who would be entitled to that asset had there been no tax liability, can elect that, that asset be distributed to that heir or legatee if that heir or legatee accepts liability for this tax debt (s25(6)).

- The heir or legatee must pay this tax debt within a period of 3 years (the 3 years starts from the date after the estate was distributed in terms of section 35(12) of the Administration of Estates Act) (s25(6)).

- This tax debt becomes a debt due to SARS by that heir or legatee (s25(7)).

Insolvent Estate

- On sequestration a person’s assets pass to that person’s insolvent estate. The change of ownership usually triggers a disposal, however the ‘one and the same person’ principle brings the two entities together and since a person cannot dispose of something to himself, there is no disposal of the individual’s assets on the date of sequestration.

- Capital gains and losses are therefore determined in the hands of the insolvent estate when the assets are disposed of to third parties.

- Under Paragraph 83(1) of the Eight Schedule, the disposal of an asset by an insolvent estate is treated in the same manner as if the natural person whose estate has been sequestrated had disposed of that asset. This means that the insolvent estate is treated as a natural person and will be entitled to the same exemptions and exclusions the insolvent person would have been entitled to, had the person disposed of the assets.

- The purpose of this provision is to ensure that the insolvent estates will not be taxed on the disposal of the personal assets of the insolvent person such as that person’s primary residence (to the maximum amount of the primary residence exclusion), furniture or private motor vehicles. It also confers the same 40% inclusion rate and annual exclusion on the insolvent estate.

- The insolvent person before sequestration, the insolvent estate and the insolvent person on and after sequestration share the annual exclusion, in that order, in the year of sequestration. Therefore, to the extent that the insolvent person before sequestration has not used the annual exclusion during the applicable period of assessment, the excess will be available for set-off against capital gains and capital losses arising firstly in the insolvent estate and secondly, if any excess remains, in the insolvent person on and after sequestration.

- In the subsequent years, the insolvent estate and the insolvent person on or after sequestration will each be entitled to the full annual exclusion.

- Under section 25C the “one and the same person” rule in relation to determining any taxable capital gain or assessed loss of the insolvent estate, an assessed loss in the hands of the insolvent person before sequestration may be carried forward to the insolvent estate. Any assessed capital loss remaining in the insolvent estate at the time it is finally terminated will be forfeited.

- In an instance whereby CGT annual exclusion R 40 000 is not fully used on Tax reference number 1, then the remaining balance must be used on Tax reference number 2 or vice versa during the same year of assessment.

- Example for Insolvent Estate

- Where the annual exclusion of R25 000 was used on tax number 1, the remaining annual exclusion of not more than R15 000 will be used on tax number 2.

- Example for Insolvent Estate

Completion of the Capital Gains Tax Section

- The income tax return makes provision for ten local and ten foreign capital gain or loss transactions to be declared. Each transaction must be declared separately. Where multiple disposals of shares (that is administered by a single administrator) take place and the disposal of such shares are reported on a single certificate, the disposals reflected on the certificate can be treated as one disposal.

- ‘Mark here with an ‘X’ if this amount should be excluded from the communal estate (i.e. married in community of property).’

- The communal indicator will be repeated based on the number of transactions indicated.

- ‘Mark with an “X” if this transaction is deemed disposal’

- This field is applicable from 2025 year for the deceased person for the deemed disposal that takes place at the date of death. This field does not apply to deceased estates.

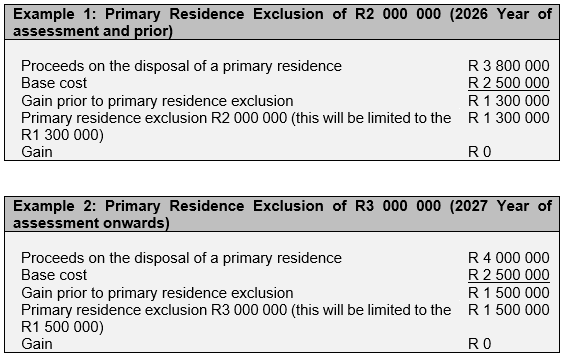

- Regarding the disposal of a primary residence, the return caters for the insertion of the primary residence exclusion. From 2027 year of assessment, the primary residence exclusion is R3 000 000.00.

- If a primary residence was disposed and the difference between the proceeds and the base cost is less than the primary residence exclusion, the gain must be indicated as a ‘0’. See the example below:

- Select the applicable Main Asset Type Source Code relating to the local/foreign capital gain/loss transaction:

- 6502: GAIN: Immovable assets

- 6503: LOSS: Immovable assets

- 6504: GAIN: Primary residence – If selected, complete the Primary Residence section.

- 6505: LOSS: Primary residence – If selected, complete the Primary Residence section.

- 6506: GAIN: Financial instruments – Listed, including assets of which prices are regularly published in newspaper

- 6507: LOSS: Financial instruments – Listed, including assets of which prices are regularly published in newspaper

- 6508: GAIN: Financial instruments – Unlisted

- 6509: LOSS: Financial instruments – Unlisted

- 6510: GAIN: Intangible assets

- 6511: LOSS: Intangible assets

- 6514: GAIN: Plant and machinery

- 6515: LOSS: Plant and machinery

- 6516: GAIN: Other movable property used mainly for trade purposes

- 6517: LOSS: Other movable property used mainly for trade purposes

- 6518: GAIN: Other movable property used mainly for trade purposes other than personal-use assets

- 6519: LOSS: Other movable property used mainly for trade purposes other than persona-use assets

- 6520: GAIN: Financial instruments – crypto assets

- 6521: LOSS: Financial instruments – crypto assets

- Note: Depending on the specific Main Asset Type Source code selected, the applicable fields will be displayed for completion.

Primary Residence

- “Do you confirm that this transaction relates to a primary residence?” – Select ‘Y’ or ‘N’

- This is a mandatory field.

- “If Yes, indicate whether the primary residence is held jointly?”

- “Is the primary residence held in a partnership?” – Select ‘Y’ or ‘N’.

- ‘If Yes, state the percentage held’.

- “Mark the applicable field with an ‘X’ to confirm that the full amounts relating to proceeds and base cost of the primary residence are declared”

- “Does any exemption/rollover other than primary residence exemption apply to this transaction” – Select ‘Y’ or ‘N’

- These questions must be answered in respect of each capital gain/loss transaction.

- Complete the following fields if a ‘Local Gain/Loss’ is applicable:

- “Proceeds”

- If ‘yes’ is selected for the question ‘Does the transaction relate to a primary residence?’ and the amount captured in this field is less than or equal to R3 000 000, a pop-up message will display to indicate that proceeds on the disposal of the primary residence does not exceed R3 000 000, therefore capital gain/ loss is disregarded.

- “Base cost”

- “Primary residence / Other Exclusions (excl. annual exclusions)”

- If ‘yes’ is selected for the question “Does the transaction relate to a primary residence?” this field will be auto-populated with R3 000 000.

- Exclusion/Roll-over (excluding annual exclusion)

- “Gain” (4250)

- This field is auto-calculated by the system

- The capital gain will be disregarded if the proceeds on the disposal of the primary residence does not exceed R3 000 000.

- If an amount greater than 0 is captured, complete the field ‘Less: Prior year clogged loss brought forward and deductible from the capital gains listed above derived from a disposal to the same connected person (par. 39 of the Eighth Schedule)’

- “Loss” (4251)

- This field is auto-calculated by the system

- The capital loss will be disregarded if the proceeds on the disposal of the primary residence does not exceed R3 000 000.