Summary

The purpose of this webpage is to assist employers in understanding the validation rules for completion of Employees’ Income Tax certificates for 2024.

This webpage prescribes validation rules applicable to:

- Data (employee tax certificate information) included in CSV files; and

- Fields on employees’ tax certificates which are manually completed.

For more information visit the SARS website www.sars.gov.za > Types of Tax > PAYE.

Reconciliation Process

- EMP501 Reconciliation process (Employees’ Income Tax certificates submitted to SARS from 1 March 2023).

- Changes to the specifications for employees’ tax certificates and reconciliation processes have been introduced (e.g., additional fields on various reconciliation documents, etc).

- The employer demographic information no longer forms part of the certificate as the “Certificate Number” now contains the PAYE reference number of the employer, which links the employer demographic information to the employee;

- All validation rules in respect of submissions after February 2012, have been re-instated;

- With the introduction of this process, the CSV file layout and validation rules were standardised to ensure that all CSV files (irrespective of the transaction year of the file) comply with the same validation rules.

- Changes to the specifications for employees’ tax certificates and reconciliation processes have been introduced (e.g., additional fields on various reconciliation documents, etc).

- When the EMP501 Reconciliation is submitted, the employer’s compliance status will be verified. If the employer is deemed non-compliant, a letter notifying the employer to rectify the non-compliance will be issued.

- If the EMP501 Reconciliation is requested and the reconciliation period is in a transaction year prior to the earliest liability start date of the Employment Taxes as per SARS records, the request will be rejected. For an example: PAYE liability start date is 2020/03/01 and the EMP501 return for 2019/08 is requested.

- SARS will issue a letter advising the employer to rectify the start liability dates using the RAV01 process.

- If no EMP201 returns were submitted, the employer will receive a letter to first submit EMP201 returns and make the necessary payment before EMP501 Reconciliation can be submitted.

- Employers will be prevented from submitting EMP201 returns once the employer’s status is suspended (s-coded). However, if all the employment taxes are suspended in July 2023, the employer will be able to submit outstanding EMP201 returns for periods prior to July 2023.

- Balancing check will be performed on all EMP501 Reconciliation, regardless of the submitting channel.

- If IRP5/IT3(a) certificates linked to the EMP501 Reconciliation have failed balancing check, no information will be pre-populated on the employee’s income tax return. A letter will be issued to inform the employer of the next step.

Interim Reconciliation Process

- An interim reconciliation process has been introduced in respect of reconciliation submissions after the February 2010 submission.

- The interim reconciliation process became effective in August 2010 for reconciliation declarations of 2011 and later transaction years.

- Employers will not be allowed to submit an interim reconciliation via eFiling if the final reconciliation was submitted via a different channel and processed to the employer’s account.

- Employees’ tax certificates relating to interim reconciliation declarations:

- The employees’ tax certificate may only be issued to an employee where the employer:

- Has ceased to be an employer in relation to the employee concerned (e.g., death, retirement, resignation or immigration of the employee); and

- Has ceased to be an employer (e.g., the employer stopped trading).

- The employer must reflect Employees’ tax deducted from the employee’s remuneration under code 4102 (PAYE).

- The employees’ tax certificate may only be issued to an employee where the employer:

Note 1: It will be accepted in cases where the employer’s payroll program does the split programmatically.

Note 2: The legal requirements would apply if the employer ceased to be an employer or the employee dies, retires, resigns or immigrates before the closing of the interim period (e.g., 31 August). A final tax calculation at the end of the Employees’ tax period must be done and the certificate must be issued as a final tax certificate with a calendar month indication of “02” in the certificate number.

- Reconciliation declarations in respect of the interim submissions:

- The actual liability per month for the first 6 months of the tax year (i.e., from March to August) must be completed on the declaration.

- Submission of reconciliation documents:

- The employer reconciles his monthly submission bi-annually at the end of August and February. The six-monthly submissions of EMP201 declarations are consolidated into a reconciliation using the EMP501.

- The reconciliation documents must be submitted via one of the following available channels:

Note 3: No CSV files will be accepted by SARS. CSV files must be imported into e@syFileTM. Employers who use the e@syFileTM software must also capture all their manual certificates by using the application.

Note 4: SARS will only accept an EMP701 for adjustments between the years 1999 -2008. From 2009 going forward, adjustments for reconciliation submissions must be made by resubmitting a modified EMP501.

- Employment Tax Incentive (ETI)

- The employer must:

- Identify all qualifying employees in respect of that specific month, refer to PAYE-GEN-01-G05 – Guide for Employers in respect of Employment Tax Incentive – External Guide.

- Determine the applicable employment period for each qualifying employee;

- Determine each employee’s “monthly remuneration”;

- Calculate the employment tax incentive amount per qualifying employee; and

- Reduce the amount of PAYE payable by the amount of ETI utilised on the EMP201 declaration.

- The employer must:

Note 5: If the monthly calculated ETI amount claimed exceeds the gross employees’ tax (before ETI) for a specific month, the excess ETI will be carried forward to the next month. The ETI amount claimed will only be allowed to the extent that the “Nett PAYE” is equal to zero.

Note 6: The excess ETI carry forward amount shall be refunded to the employer at the end of each reconciliation period (August and February). Employers can only claim ETI from 2014 year of assessment.

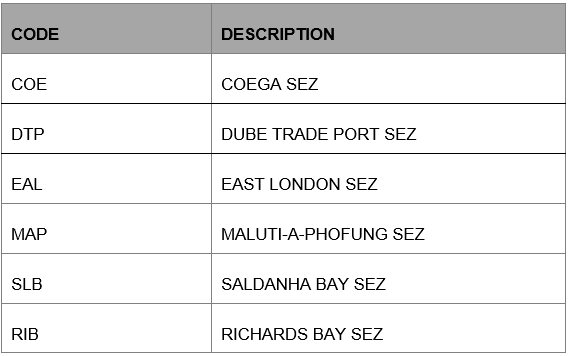

- Any employee who renders services inside a special economic zone (SEZ) to an employer that is operating inside SEZ as listed below, will qualify for ETI.

- The Minister of Finance has identified the following six as SEZs:

General Rules

- Tax certificates issued by employers to employees for their personal use may contain additional information, provided that the information required according to the validation rules is included and that the information for the relevant field is valid.

- Tax certificates submitted to SARS must be in the CSV files:

- The record structure of CSV files is as follows:

- Employer header record;

- Employer and financial information records for all tax certificates (including Employment Tax Incentive (ETI) information); and

- Employer totals trailer record.

- Each CSV file may only contain tax certificate information for a single employer (no multiple employer records will be accepted if it is contained in a CSV file).

- The CSV file format should start with the code, followed by the data for the relevant code, followed by the next code, etc. for example: Code, data,code,data,code,data,code,data,9999

- The first code of the record may not be preceded by any character (e.g., space, comma, etc);

- The last code of the record must be 9999 and may not be followed by any character (e.g., space, comma, etc.).

- The record structure of CSV files is as follows:

- Tax certificates submitted via eFiling:

- Tax certificates submitted via walk-in.

- The manual capturing of the certificate can be done at the branch (walk-in) as long as the total number of certificates does not exceed 50.

- The reconciliation and submission of the EMP501 return and tax certificates to SARS must be done within the dates announced by the Minister in the government gazette. Failure to comply within the prescribed dates may lead to penalties and interest imposed.

- Employees’ Income Tax certificates:

- The certificate must consist of the following:

- The employee’s personal information and the employer information.

- Tax Directive information, financial information and Employment Tax Incentive (ETI) information pertaining to the employee, if any.

- The tax certificate number must be unique per employer and employee.

- The same certificate number may not be used more than once by an employer; and

- May not be duplicated in either the current, past or future years of assessments by the employer.

- The last 14 digits for the same individual need not be the same for the final certificate as it was for the interim certificate. These digits can be the same if the 2 digits indicating the period of reconciliation are different.

- Where the final certificate was issued in the bi-annual submission, the full year certificate must have the same certificate number.

- Income source codes are restricted to a maximum of 20 and the deduction codes are restricted to a maximum of 12.

- Local and foreign income source codes may be completed on the same certificate for a specific employee.

- At least one income source code with a value greater than zero must be completed. However, if it is a director of a private company or a member of a close corporation where the remuneration cannot be determined at the end of the tax period, the source code 3601/3651 may be reported with a zero value with effect from 2019 year of assessment.

- No negative values are accepted.

- Cents of all amounts must be dropped off/omitted (rounded down), except for the fields containing the tax, SDL and UIF amounts where the cents must be specified even if it is zero.

- The following codes may only appear once on a certificate:

- All the employer information codes,

- All the employee information codes, excluding code 3230, and

- All Tax Certificate Information codes representing financial information excluding the following codes:

- Income received codes: 3601 to 3924 and 3651 to 3957

- Deduction/Contribution codes: 4001 to 4055, and

- Employment Tax Incentive Information codes: 7002 to 7005, 7007, 7008 and 7009.

- Code 3230 (directive number) may appear up to five times on a certificate.

- All income and deduction fields that have a zero value must not be reported except if specified otherwise in the validation rules.

- All cents for Rands must be dropped off with the exception of the following –

- 4101, 4102,

- 4115, 4116, 4118

- 4120

- 4141, 4142, 4149,

- 6030, 7002, 7003, 7004 and 7008.

- where the Rand value including the cents must be specified (even if it is zero).

- If year of assessment (code 3025) is greater or equal to 2021 and Voluntary Over-deduction Indicator (code 3195) is “Y” then PAYE (code 4102) must be less or equal to the sum of Non-taxable income (code 3696) and Gross Employment Income (taxable) [code 3699];

- If year of assessment (code 3025) is greater or equal to 2021 and Voluntary Over-deduction Indicator (code 3195) is “N” then PAYE (code 4102) must be less or equal to Gross Employment Income (taxable) [code 3699].

- The certificate must consist of the following:

Employment Tax Incentive (ETI)

- The monthly ETI data must be added to the end of the tax certificate information for every employee which qualifies for ETI. Information in respect of ETI for every month must be reported in the reconciliation statement for that specific period.

- ETI information for bi-annual reconciliation (6 months, March to August) and for final reconciliation (12 months , March to February) must be reported in the following manner:

- If the employee does not qualify for ETI, the Employment Tax Incentive indicator will be “N” and ETI fields must NOT be completed.

- If the employee qualifies for ETI for one or more months, the Employment Tax Incentive indicator will be “Y” and ETI codes and values must be completed for all the months as per validation rules for each code.

Note: No ETI related fields must be printed on the IRP5 certificate that is issued to the employee.

- The government granted an additional assistance to those employers who were adversely affected by COVID-19, as well as assisting in the process of reconstructing businesses. The expansion of the ETI was extended for another limited four-month period, from 1 August 2021 to 30 November 2021.

- Initially, the expansion of the ETI programme was made available for a limited period of four months, beginning 1 April 2020 and ending on 31 July 2020. Please refer to GEN-REG-01-G05 – Guide for Employers in respect of Employment Tax Incentive – External Guide for more details.

Error Reports

- An error report will be provided by eFiling and e@syFileTM when uploading a CSV file on the software. This error report will indicate all the errors that were found when the data of the file was validated.

- Error messages: The file will be rejected if any error message is displayed. An error message indicates to an employer that the data for the relevant field does not comply with the validation rule and must be corrected before the submission can be accepted by SARS.

2024 Validation Rules

- The validations rules to fields only applicable on CSV files will be specifically indicated. Fields not specifically indicated apply to both the field on the CSV file as well as the field on the Employees’ Income Tax certificate.

- 2024 Validation Rules are applied to the following –

- Employer Information;

- Employee Information;

- Employee Bank Account Details;

- Employee Directive Information;

- Employee Financial Information;

- Employment Tax Incentive Information.

- The above information is available on the SARS website www.sars.gov.za> Types of Tax > PAYE > BRS – PAYE Employer Reconciliation for 2023 / 2024.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.