Purpose

The purpose of this webpage is to assist employers in understanding their obligations relating to allowances paid or payable to their employees.

Scope

This basic guide explains the methods to be applied by the employers in respect of allowances paid or payable to employees and includes the legislation requirements as well as examples.

Allowances

Subsistence Allowance

| Reference to the Act | Section 8(1)(a) read together with section 8(1)(c) of the Income Tax Act No. 58 of 1962 (the Income Tax Act). |

| Meaning | A subsistence allowance is any allowance given to an employee or a holder of any office for expenses incurred or to be incurred in respect of personal subsistence and incidental costs (for example, drinks, lunch, parking). |

| Amounts deemed to be expended |

Section 8(1)(c) of the Income Tax Act prescribes that the employee shall be deemed to have actually expended a certain amount (daily expenses in respect of meals and/or incidentals costs) where the employee is absent from his/her usual place of residence. Where the accommodation to which the allowance or advance relates is in the Republic, an amount equal to the following is deemed to be expended for each day or part of a day in the period during which the employee is absent from his/her usual place of residence —

Section 8(1)(a)(ii) of the Income Tax Act states that where the recipient is by reason of the duties of his or her office or employment obliged to spend a part of a day away from his or her usual place of work or employment and provides proof of such expenditure to the employer, a reimbursement or advance for such expenditure actually incurred by the recipient is excluded from taxable income if the recipient is allowed by his or her principal to incur expenditure on meals and other incidental costs for that part of a day and the amount of the expenditure does not exceed an amount of R184. |

| Example | If an employer allows an employee to incur expenditure on meals when obliged to spend a part of a day away from his/her usual place of work/employment by reason of the employee’s employment, and reimburses the employee upon the submission of proof of expenditure, such reimbursement up to an amount announced by notice in the Gazette (R184 per day for the 2027 YoA), is not taxable and must therefore not be declared on the IRP5/IT3(a). However, where the reimbursement exceeds the lower of the amount announced or the amount for which proof of expenditure was submitted by the employee, the excess is fully taxable and therefore liable to PAYE and must be declared under income code 3713 on the IRP5/IT3(a). |

| Employer borne expenses | Where the accommodation to which the allowance or advance relates is outside the Republic, an amount equal to prescribed amount applicable to the relevant country is deemed to be expended for each day or part of a day in the period during which the employee is absent from his/her usual place of residence in accordance with the table for the country in which that accommodation is located, please refer to Subsistence Allowance – Foreign travel – external annexure. |

| Please note |

The rates are for guidance purposes only. The rates for each tax year will be published by notice in the Government Gazette

|

| Employees’ tax | Employees’ tax must not be deducted from the subsistence allowance, regardless of whether the deemed amounts and/or prescribed periods are exceeded. |

Travel Allowance

| Reference to the Act |

Section 8(1)(b) |

| Meaning |

A travel allowance is any allowance paid, or advance given to an employee in respect of Any allowance or advance in respect of travelling expenses not to have been expended on The following two situations are envisaged, namely —

The definition of variable remuneration was extended to include any amount paid or granted |

| Travel allowance |

The employees’ tax deducted in respect of the travel allowance must be reflected as Pay- 80% of the travel allowance paid to an employee is subject to the deduction of employees’ Where a travel allowance is paid in addition to a reimbursive allowance (see discussion |

| Vehicle let to the employer |

Where an employee, his/her spouse or child owns or leases a motor vehicle (whether Note: The rental received by the employee must not be declared as rental income but as a |

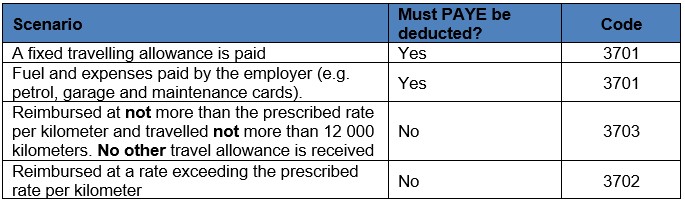

| Reimbursive travel allowance |

A reimbursive travel allowance is where an allowance or advance is based on the actual distance travelled for business purposes (that is excluding private use). |

| Prescribed rate per kilometre |

The rate per kilometre is fixed by the Minister of Finance and currently is —

Pre-1 March 2018 (2018 and prior tax years) – An allowance or advance which is based on the actual distance travelled for business

The table hereunder displays the relevant source codes under which the amounts must be

From 1 March 2018 –

Example:

Example: |

Allowance to a Holder of a Public Office

| Reference to the Act | Section 8(1)(d) and 8(1)(f) |

| Meaning |

Any allowance granted to the holder of a public office to enable him/her to defray expenditure incurred by him/her in connection with his/her office, to have been expended by him/her to the extent that he/she has actually incurred expenses for the purposes of his/her office in respect of —

Where it is expected from the following office holders:

|

| Portion of salary deemed to be a public office allowance |

To defray any expenditure out of his/her salary, an amount equal to a portion of such salary is deemed to be an allowance to the holder of a public office. This is prescribed by the provisions in section 8(1) (f) and the amount is determined by the National Assembly or the President. Where the employee has held a public office for less than 12 months, the portion of his/her salary which is deemed to be an allowance to a holder of a public office in terms of section 8(1)(f), must be apportioned to determine the amount relevant for the actual period for which the office was held. A part of a month shall be reckoned as a full month. |

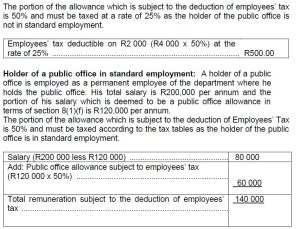

| Employees’ tax | Only a 50% portion of the allowance is subject to the deduction of employees’ tax. |

| IRP5/IT3(a) details |

The full allowance (100%) must be reflected under code 3708; and All the other income components must be reflected under the relevant codes (e.g. salary, overtime, bonus, etc.). |

| Example |

Holder of a public office not in standard employment: A holder of a public office receives an allowance of R4 000 per month to enable him to defray expenditure in respect of his office. The portion of the allowance which is subject to the deduction of employees’ tax is 50% and must be taxed at a rate of 25% as the holder of the public office is not in standard employment.

|

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed via the following link: Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.