Quick Reference Card

In his Budget Speech on 12 March 2025, the Minister of Finance announced new tax rates, tax rebates, tax thresholds and other tax amendments for individuals. Details of these proposals are listed below and employers must update their payroll systems accordingly. The deduction tables and instructions in this guide came into effect on 1 March 2025.

Tax Tables for Individuals and Special Trusts

2025/2026 Tax Year (1 March 2025 to 28 February 2026)

TAXABLE INCOME (R) | RATES OF TAX (R) |

0 – R 237 100 | 18% of taxable income |

R 237 101 – R 370 500 | R 42 678 + 26% of taxable income above R 237 100 |

R 370 501 – R 512 800 | R 77 362 + 31% of taxable income above R 370 500 |

R 512 801 – R 673 000 | R121 475 + 36% of taxable income above R 512 800 |

R 673 001 – R 857 900 | R179 147 + 39% of taxable income above R 673 000 |

R 857 901 – R 1 817 000 | R251 258 + 41% of taxable income above R 857 900 |

R 1 817 001 and above | R644 489 + 45% of taxable income above R 1 817 000 |

Tax rebates applicable to individuals | 2026 |

Primary rebate | R17 235 |

Secondary rebate (for persons 65 years and older) | R 9 444 |

Tertiary rebate (for persons 75 years and older) | R 3 145 |

Tax thresholds applicable to individuals | 2026 |

Persons under 65 years | R 95 750 |

Persons 65 years and older | R148 217 |

Persons 75 years and older | R165 689 |

Medical scheme fees tax credit | 2026 |

For the taxpayer | R 364 |

For the first dependant | R 364 |

For each additional dependant | R 246 |

Subsistence allowance (RSA only) | 2026 |

Meals and incidental – day trip | R 176 |

Only incidental costs per day | R 176 |

Meals and incidental costs per day | R 570 |

Official interest rate

In the case of a debt which is denominated in the currency of the Republic, a rate of interest equal to the South African repurchase rate plus 100 basis points, if the country’s repurchase rate is 6%, the official interest rate will be 7% (6% plus 100 basis points).

In the case of a debt, which is denominated in any other currency than the currency of the Republic, a rate of interest will be the equivalents of the country’s repurchase rate plus 100 basis points. Where a new purchase rate or equivalent rate is determined, the new rate of interest applies from the first day of the month following the date on which that new purchase rate or equivalent rate came into operation.

Residential accommodation

Travelling allowance |

80% of the travel allowance is subject to the deduction of employees’ tax, meaning 80% of the travel allowance must be included in the employee’s remuneration when calculating employees’ tax. Provided that where the employer is satisfied that at least 80% of the use of the motor vehicle for a year of assessment will be for business purposes, then only 20% of the allowance will be subject to employees’ tax. |

Travel allowance cost scale table for 2026 tax year (from 01 March 2025) | |

Vehicle cost ceiling | R800 000 |

The simplified rate per kilometer | R4.76 |

Exempt Bursary | 2026 |

Remuneration proxy | R600 000 |

Grade R to 12 and NQF level 1 to 4 (relative of employee without disability) | R20 000 |

Grade R to 12 and NQF level 1 to 4 (family member of employee with disability) | R30 000 |

NQF level 5 to 10 (relative of the employee without disability) | R60 000 |

NQF level 5 to 10 (family member of employee with disability) | R90 000 |

Fringe benefit: employer – owned provided motor vehicles

With effect from 1 March 2011, the percentage rate for all employers – owned provided vehicles is 3.5 % per month of the vehicle’s determined value. However, vehicles with maintenance plans included within the purchase price at the time of purchase will trigger only a 3.25% monthly fringe benefit.

With effect from 1 March 2014, where the vehicle is acquired by the employer under an operating lease concluded at arm’s length and that are not connected persons in relation to each other, the value of a fringe benefit is the actual cost to the employer incurred under this lease plus the cost of fuel in respect of that vehicle.

Retirement Fund Contributions

The tax harmonization reforms for Pension fund, Provident fund and Retirement Annuity fund (retirement funds) has been implemented from 1 March 2016. All individuals who contribute towards a retirement fund after 1 March 2016 will qualify for a tax deduction of the lesser of:

- R350 000; OR

- 27.5% of the higher of –

- Remuneration as defined in Fourth Schedule (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit); or

- Taxable income before allowing any deduction under ss11F, 6quat(1C) and 18A) (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit)

OR

- Taxable income (before allowing any deduction under ss11F, 6quat(1C) and 18A) and before inclusion of any taxable capital gain (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit).

Period for keeping records

Records need not be retained by the person after a period of five years from the date of the submission of the return and after a period of five years from the end of the relevant tax period.

If the records are relevant to an audit or investigation or a person lodges an objection or appeal against the assessment or decision made, the person must retain the records relevant to the audit, objection or appeal until the audit is concluded or the assessment or the decision becomes final.

FURTHER INFORMATION

For more information

- Visit the SARS website www.sars.gov.za,

- Call the SARS Contact Centre on 0800 00SARS (7277), or

- Visit your nearest SARS branch.

Purpose

- The purpose of this webpage is to assist employers in understanding their obligations relating to Employees’ Tax, Skills Development Levy (SDL) and Unemployment Insurance Fund (UIF) contributions.

Scope

- This basic guide is issued in terms of Paragraph 9(2) of the Fourth Schedule to the Income Tax Act No. 58 of 1962.

- This guide prescribes the:

- Employees’ tax deduction tables as contemplated in Paragraph 9(1) of the Fourth Schedule to the Income Tax Act;

- Manner in which the tables must be applied by the employer.

Background

What is employees’ tax | - Where an employer pays or becomes liable to pay remuneration to an employee, the employer has an obligation to deduct or withhold employees’ tax from the remuneration and pay the tax deducted or withheld to the South African Revenue Service (SARS) on a monthly basis. In most instances, the employer is obliged to issue each employee with an employees’ tax certificate [IRP5/IT3 (a)] at the end of each tax period which reflects, amongst other details, the employees’ tax deducted.

- These subjects are fully dealt with later in this guide. In addition thereto, the employer is obliged to submit an Employer Reconciliation Declaration (EMP501) to SARS.

- In terms of Paragraph 3 of the Fourth Schedule, employees’ tax receives preference over any other deduction from the employee’s remuneration which the employer has a right or is obliged to deduct otherwise than in terms of any law.

- Any reference to the start date and end date of a tax period is 1 March and 28/29 February. This guide will include the start and end dates of 2nd alternate period. An alternate period is normally determined at the option of the employer which may be exercised in relation to all employees or any class of employee. Where an employer adopts the so-called alternate period, any remuneration paid to an employee during such alternate period is regarded as having been paid to him/her during the corresponding tax year.

|

What is SDL | - This is a compulsory levy scheme for the purposes of funding education and training as envisaged in the Skills Development Act, 1998. This levy came into operation on 1 April 2000 and is payable by employers on a monthly basis.

|

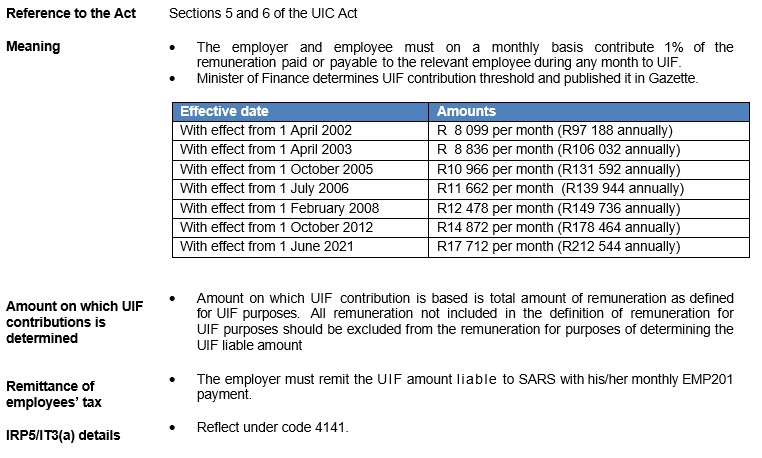

What are UIF

contributions | - This is a compulsory contribution to fund unemployment benefits. Since 1 April 2002, the contributions deducted and payable by employers on a monthly basis have been collected by SARS and are paid over to the UIF which is managed by the UI Commissioner.

|

Liability of representative employer

| - The representative employer is not relieved from any liability, responsibility or duty of the employer and is therefore subject to the same duties, responsibilities and liabilities as the employer.

|

References to the Act

| - Paragraphs of the Fourth and Seventh Schedules and Sections referred to in this publication are governed by the Income Tax Act. References to the Skills Development Levies Act (the SDL Act), Unemployment Insurance Contributions Act (the UIC Act) and Tax Administrative Act (the TA Act) are specifically indicated.

|

Registration

Registration as an Employer

References to the Act | Chapter 3 of the TA Act Paragraph 15(1) of the Fourth Schedule, Sections 4 and 5 of the SDL Act Sections 4 and 10 of the UIC Act |

Meaning | - Employer must apply for registration for employees’ tax purposes with SARS within 21 business days after he/she becomes an employer unless none of the employees are liable for normal tax.

- Where an employer is liable to pay the SDL levy, the employer must register as an employer with SARS and must indicate the jurisdiction of the SETA within which the employer must be classified.

- Where an employer is liable to pay the UIF contribution, the employer must register with SARS or the UIF office (whichever is applicable to such employer) for the payment of the contributions.

|

Application to register | - Application to register as an employer must be made via eFiling or at the SARS Branch.

|

Employers exempt from paying the SDL levy | - The following employers are exempt from paying the SDL, any:

- Public service employer in the national or provincial sphere of Government.

- Public service employer in the national or provincial sphere of Government.

- National or provincial public entity if 80% or more of its expenditure is paid directly or indirectly from funds voted by Parliament.

Note: These employers must budget for an amount equal to the levies payable for training and education of their employees - Public benefit organisation, exempt from the payment of Income Tax in terms of section 10(1)(cN), which solely carries on certain welfare and humanitarian (paragraph 1 of Part 1 of the Ninth Schedule), health care (limited to paragraph 2(a), (b), (c) and (d) of Part1 of the Ninth Schedule), religion, belief or philosophy public benefit activities (paragraph 5 of Part 1 of the Ninth Schedule) or solely provides funds to such a public benefit organisation (paragraph 10 of Part 1 of the Ninth Schedule) and to whom a letter of exemption has been issued by the SARS Tax Exemption Unit;

- Municipality in respect of which a certificate of exemption is issued by the Minister of Labour.

- Although the above-mentioned employers are exempt from payment of levy, they are not absolved from registration. An employer is not required to register as an employer for SDL purposes if there are during any month reasonable grounds for believing that total leviable amount paid or payable by that employer to all its employees during the following 12 month period will not exceed R500 000 even though such employer is liable to register with SARS for Employees’ Tax purposes.

|

Registration with the UI Commissioner for UIF purposes | - The following employers must register with the UI Commissioner:

- If employer is not required to register for employees’ tax purposes at SARS;

- Employer who has not registered voluntarily as an employer for employees’ tax purposes at SARS;

- Employer who is not liable for the payment of SDL.

- Employer/employee is not required to contribute in following circumstances:

- An employee and his/her employer, where such employee is employed by the employer for less than 24 hours a month;

- Employees and employers in the national and provincial spheres of Government who are officers or employees as defined in Section 1(1) of the Public Service Act 1994 (Proclamation No. 103 of 1994);

- The President, Deputy President, a Minister, Deputy Minister, a member of the National Assembly, a permanent delegate to the National Council of Provinces, a Premier, a member of an Executive Council or a member of a provincial legislature; and

- Any member of a municipal council, a traditional leader, a member of a provincial House of Traditional Leaders and a member of the Council of Traditional Leaders.

|

Branches Registered Separately

Reference to the Act | Chapter 3 of the TA Act Paragraph 15(1) of the Fourth Schedule |

Meaning | - Where employer has applied for separate registration of branches of his/her undertaking, each branch shall be deemed to be a separate employer.

|

Application form | - Application must be made on an EMP102 form.

|

Transferring between branches | - Where an employee is transferred between branches, the branch where the employee has worked until date of transfer must issue an IRP5/IT3(a) for the period 1 March (or date of commencement of employment if such date was after 1 March) up to the day preceding the transfer. The branch to which the employee was transferred must issue a further IRP5/IT3(a) to cover the period from date of transfer up to the end of February (or other date, e.g. where the employee’s service was terminated).

|

Changes of Registered Particulars

Reference to the Act | Chapter 3 of the TA Act |

Meaning | - An employer must inform SARS in writing within 21 business days of any change in registered particulars:

- Postal address;

- Physical address;

- Representative taxpayer;

- Banking particulars used for transactions with SARS;

- Electronic address used for communication with SARS; or

- Such other details as the Commissioner may require by public notice.

|

Deregistration of an Employer

Reference to the Act | Paragraph 15(3) of the Fourth Schedule |

Meaning | - Every person who is registered as an employer shall within 14 days after ceasing to be an employer, notify the Commissioner in writing of the fact of the employer have ceased to be an employer.

|

Record Keeping

Employer Records

Reference to the Act | Chapter 4 of the TA Act Paragraph 14(1)) of the Fourth Schedule |

Meaning | - The employer must keep a register and must contain personal particulars as well as financial details of each employee and maintained in such a form, including any electronic form, as may be prescribed by the Commissioner.

- The following records of all employees’ needs are to be maintained by the employer, as may be prescribed by the Commissioner.

- Amount of remuneration paid;

- Employees’ tax deducted/withheld on all remuneration;

- UIF contributions;

- Income Tax reference number of that employee; and

- Such further information as the Commissioner may prescribe.

|

| Prescribed period for keeping records | - The records must be kept for a period of five (5) years from the date of the submission of the return and from the end of the relevant tax period if the person is not required to submit a tax return but has earned some form of taxable income. The employer must retain such records and make them available for scrutiny by the Commissioner.

- Employers who supply the tax certificate information on an electronic medium or electronically, must also keep such records for the prescribed period.

|

Records and Information to be provided by the Employee

Reference to the Act | Paragraph 14(1) of the Fourth Schedule |

Meaning | - The employee must supply the following particulars to his/her employer to ensure that the employer’s records are correct:

- Surname and full names;

- Address;

- South African Identity number or passport number and date of birth;

- Income Tax reference number (if any);

- Written declaration where required.

|

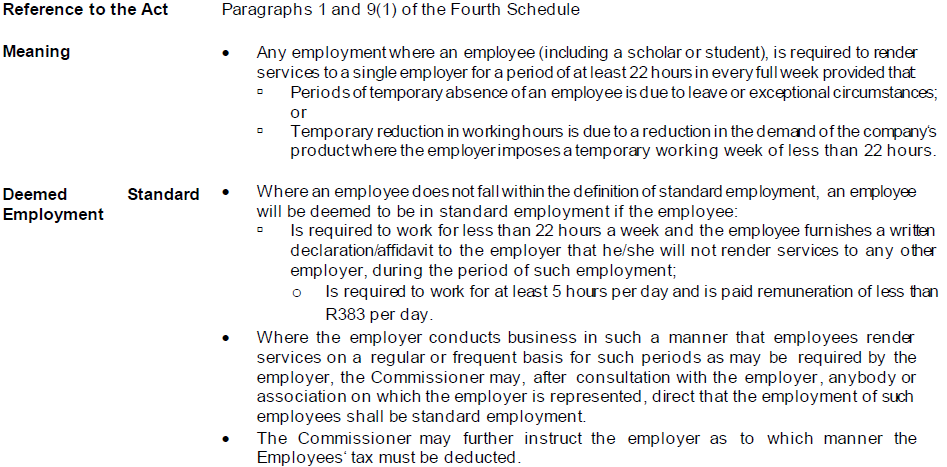

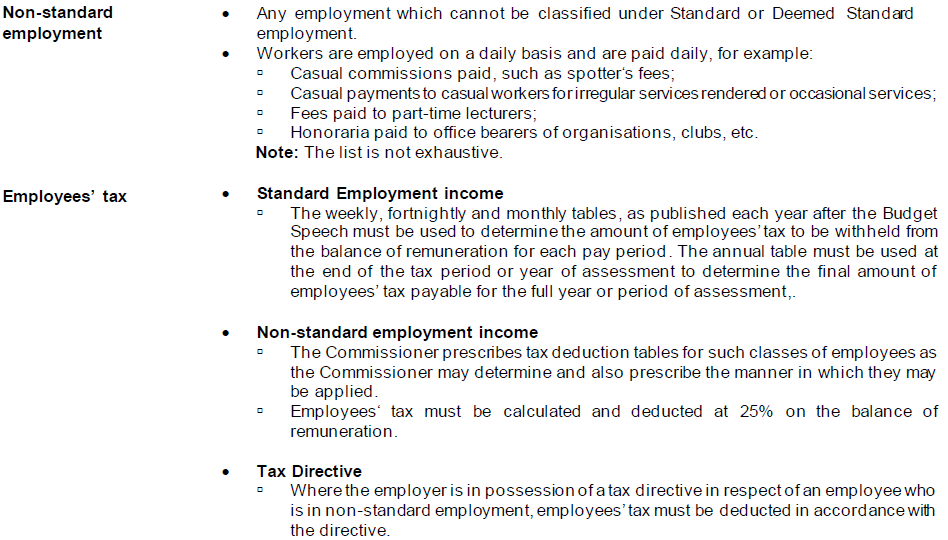

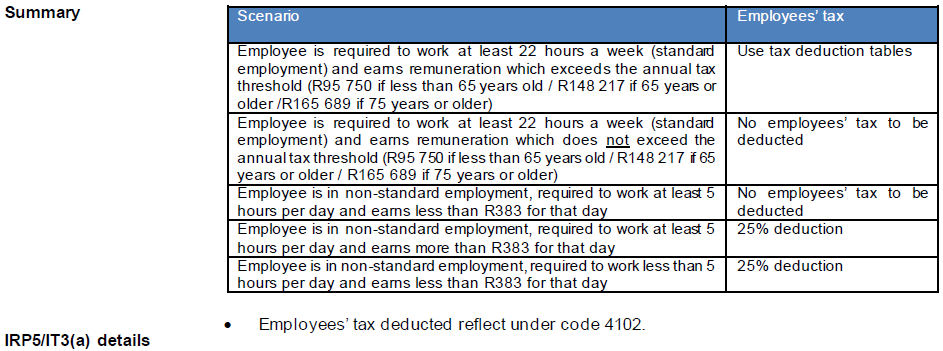

Written declaration by employee | - An employee is deemed to be in standard employment –

- Where such employee renders services to the employer for 22 hours or less in every completed week;

- The employee furnishes the employer with a written declaration stating that he/she does not or will not render services to another employer during the period he/she hold such employment at the relevant employer.

|

Determining the Employees’ Tax, SDL and UIF Liability

Elements Required before Employees’ Tax may be Deducted

Reference to the Act | Definitions of employer, employee and remuneration in Paragraph 1 of the Fourth Schedule |

Meaning | - The Fourth Schedule requires the presence of the three elements before employees’ tax may be deducted, namely, an employer paying remuneration to an employee.

- The employer must determine the employment relationship to be able to classify the worker correctly in order to determine the rate which must be applied to deduct employees’ tax from the remuneration of the specific employee.

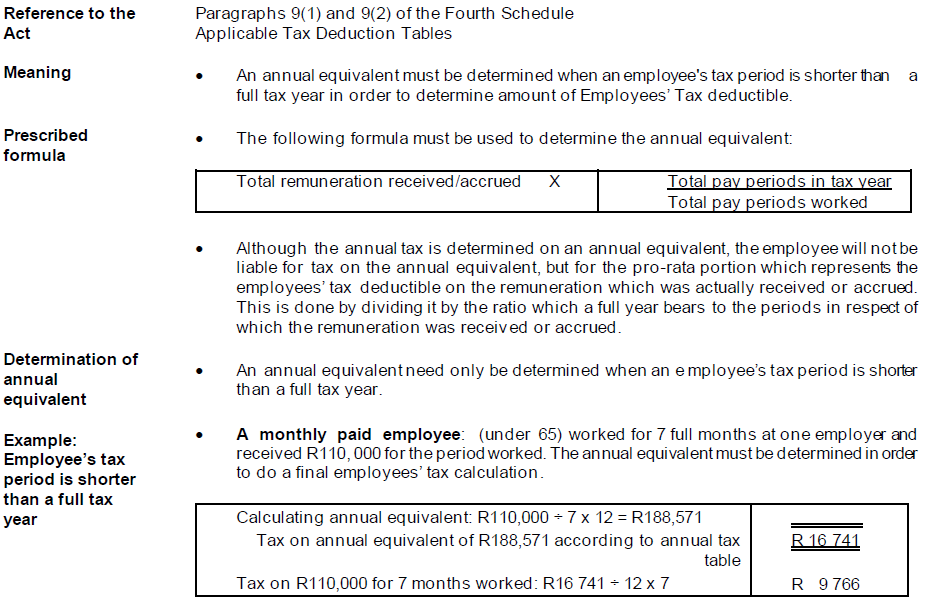

|

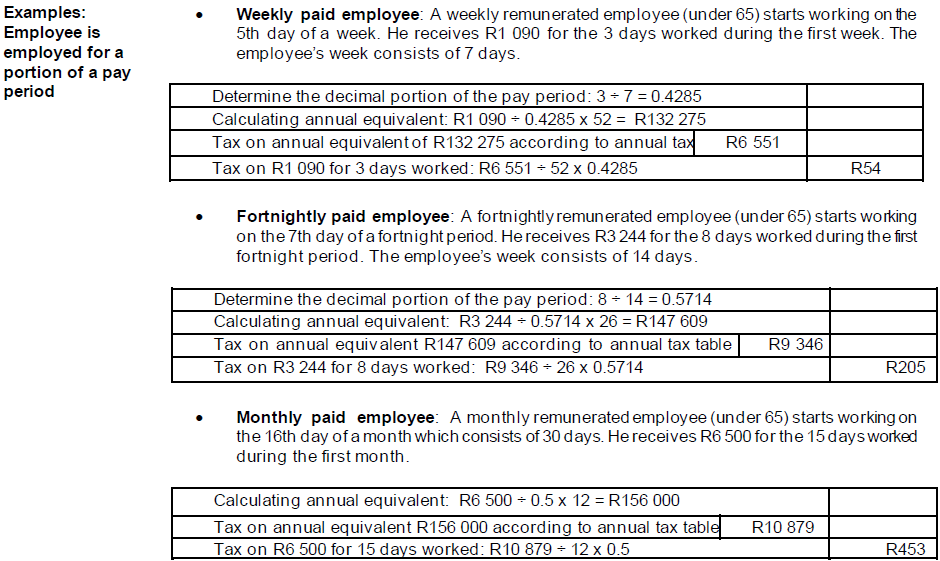

Annual Equivalent Calculation

Deduction to Determine the Balance of Remuneration

Retirement Fund Contributions

| Reference to the Act | Paragraph 2(4)(a), (b) an d (‘’bA) of the Fourth Schedule Section 11F |

| Meaning | - The employer must deduct contributions made by the employee to any pension fund, provident fund or/and retirement annuity fund (RAF) which the employer is entitled or required to deduct from the employee’s remuneration.

- From 1 March 2016, contributions made or amount paid by the employer of the person on behalf of or for the benefit of that person will be a taxable fringe benefit and a deemed contribution in the hands of the employee. Therefore, current contributions = contributions actually made by the employee plus employer contributions / payments (deemed employee contributions).

|

| Limitation | - Allowable deduction must be limited to the deduction to which employee is entitled under section 11F having regard to the remuneration and period (e.g. current or arrear contributions) i.r.o. of which it is payable. Provided that at any time during year of assessment, the amount of contribution to be deducted i.t.o paragraphs (a), (b) and (bA) must not exceed an amount that bears to amount stipulated in section 11F(2)(a) same ratio as period during which remuneration was paid by employer to employee bears to a whole year.

- Current contributions — The deduction must be limited to the lesser of :

- R350 000; OR

- 27.5% of the higher of –

- Remuneration as defined in Fourth Schedule (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit); or

- Taxable income before allowing any deduction under ss11F, 6quat(1C) and 18A) (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit)

OR - Taxable income (before allowing any deduction under ss11F, 6quat(1C) and 18A) and before inclusion of any taxable capital gain (excluding retirement fund lump sum benefit, retirement lump sum withdrawal benefit and severance benefit).

|

| IRP5/IT3(a) details | - Total current pension fund contributions reflect under code 4001 (current plus arrear contributions).

- Total current provident fund contributions reflect under code 4003.

- Only provident fund contributions made on or after 1 March 2016 are allowable as a deduction. Contributions made pre – 1 March 2016 are not allowed as a deduction.

- Total current retirement annuity fund contributions reflect under code 4006 (current plus arrear contributions).

- A partner in a partnership must be deemed to be an employee of a partnership and a partnership must be deemed to be the employer to the partners in that partnership with effect from 1 March 2016.

|

Donations

Reference to the Act | Paragraph 2(4)(f) of the Fourth Schedule Section 18A(2)(a) |

| Meaning | - The employer must deduct so much of any donation deductible from the remuneration of the employee in terms of section 18A(2)(a) and pay such amount to relevant approved organisation on behalf of the employee.

|

| Limitation | - Deduction may not exceed 5% of remuneration after deducting pension, provident and retirement annuity fund contributions. The deduction is only allowed if employee has provided employer with receipt which reflects details as prescribed in section 18A(2)(a).

|

IRP5/IT3(a) details | - Reflect under code 4030 and not only the allowable portion deducted from remuneration.

|

COVID 19 – Tax Relief : Donations to Solidarity Fund | - In order to alleviate cash flow problems for employees who make donations through the employer, the maximum deduction of 5% is increased. An additional limit of up to a maximum of 33,3% for three months or 16,66% for six months depending on the employee’s circumstances, is available.

- This amendment is effective from 1 April 2020 up until 30 September 2020.

|

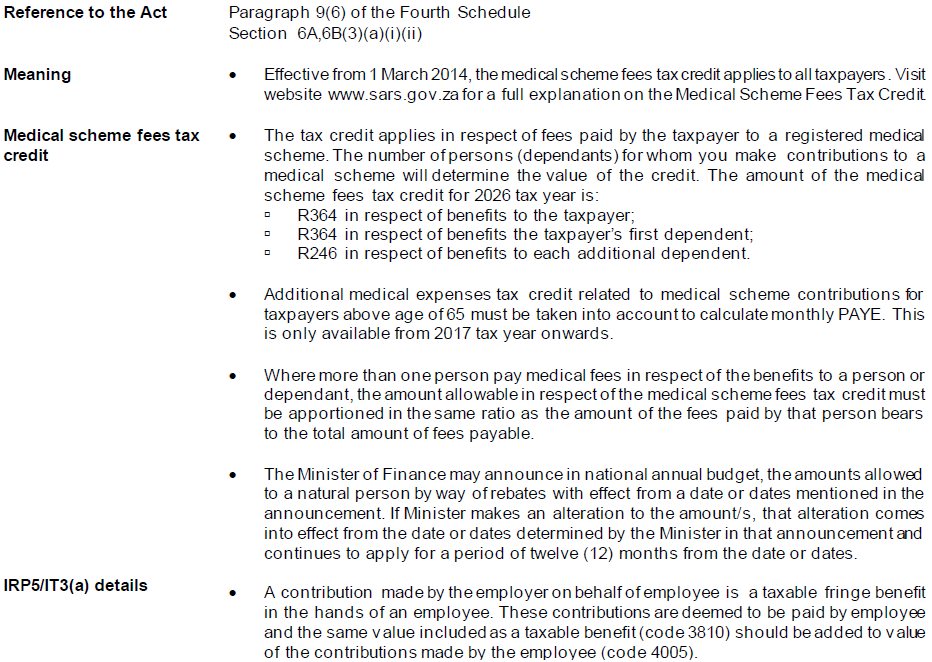

Medical Scheme Fees Tax Credit

Employees’ Tax Deduction

Reference to the Act | Paragraphs 2(1), 2(2), 2(4), 2(5)(c), 3 and 7 of the Fourth Schedule Section 7B |

| Meaning | - Must be deducted from any amount that is paid by way of remuneration.

|

Amount on which employees’ tax is deductible | - Deduction is calculated on the balance of remuneration after the deduction of all allowable deductions (e.g. Retirement annuity fund contribution, provident fund contribution, pension fund contribution and donations).

|

Voluntary additional employees’ tax deduction | - For various reasons, employees may find that they have to pay in fairly large amounts upon receipt of their assessments. To reduce the amount payable on assessment or avoid having to pay in an additional amount, such employees may request (in writing) their employers to deduct from their remuneration a greater amount of employees’ tax than is required.

|

Agreement between employer and employee | - Employer and employee may under no circumstances conclude an agreement whereby employer undertakes not to deduct or withhold employees’ tax or UIF contributions. Such agreement is void in terms of Paragraph 7 of Fourth Schedule.

|

Remittance of employees’ tax | - The employer must remit the amount deducted or withheld to SARS with his/her Monthly Employer Declaration (EMP201).

|

| IRP5/IT3(a) details | - Reflect under code the following codes —

- Code 4102 – The PAYE component of the employees’ tax deducted / withheld including any voluntary additional employees’ tax deducted;

- Code 4103 – The total of code 4101.

|

SDL Liable Amount

| Reference to the Act | Sections 3(1) and (4) of the SDL Act Paragraph 2(5) of the Fourth Schedule |

Meaning | - Employer must pay SDL at the following rates:

- From 1 April 2000, at a rate of 0,5 per cent of the leviable amount, and

- From 1 April 2001, at a rate of one per cent of the leviable amount.

- If the Minister makes changes to the rate, the new rate will apply with effect from the date announced by the Minister by notice in the Government gazette.

|

Amount on which SDL is determined | - The leviable amount is the total amount of remuneration, paid or payable, or deemed to be paid or payable, by an employer to its employees during any month, as determined in accordance with the Fourth Schedule provisions for purposes of determining the employer’s liability for Employees’ Tax.

- SDL is therefore determined on the balance of remuneration after the deduction of all allowable deductions (i.e. pension or provident fund contributions, RAF contributions and donations).

Note: All remuneration not included in the definition of remuneration for SDL purposes should be excluded from the balance of remuneration result. |

Remuneration excluded for the purposes of SDL | - Remuneration for the purposes of calculating SDL excludes amounts:

- Paid or payable as contemplated in paragraphs ‘(c) and (d) of the definition of “employee” in paragraph 1 of the Fourth Schedule, to whom a certificate of exemption has been issued in terms of paragraph 2(5)(a) of that schedule,

- Paid or payable to any person by way of any pension, superannuation allowance or retiring allowance,

- In terms of paragraph (a), (d), (‘e) or (‘eA) of definition of “gross income” in section 1,

- Payable to a learner in terms of a contract of employment as contemplated in section 18 (3) of the SDL Act.

|

| IRP5/IT3(a) details | |

UIF Liable Amount

Estimated Assessment

Reference to the Act | Chapter 8 of the TA Act Section 9A of the UIC Act |

Meaning | - Employees’ tax must be deducted from any amount that is paid by way of remuneration

- The Commissioner may estimate the amount (based on information readily available) of Employees’ tax, SDL or UIF due by employer where employer has:

- Failed to furnish an EMP201 as required; or

- Submitted a return or information that is incorrect or inadequate.

- If taxpayer is unable to submit an accurate return, a senior SARS official may agree in writing with taxpayer as to an amount of tax chargeable and issue an assessment accordingly Assessment is final and cannot be subjected to an objection and appeal.

- Employer shall be liable to the Commissioner for payment of amount of employees’ tax, SDL or UIF contributions estimated as if such an amount was deducted / withheld as required by the provisions of the relevant Tax Acts.

- The estimate amount payable by employer is subject to objection and appeal unless both employer and Commissioner in terms of section 95(3) of Tax Administration Act agree in writing to said estimate assessment(s).

|

Payments

Payment of Employees’ Tax, SDL and UIF

Reference to the Act | Chapter 10 of the TA Act Paragraphs 2(1), 5(1) and 14(2) of the Fourth Schedule Section 6 of the SDL Act Section 7(4) and 8 of the UIC Act |

Meaning | - The employees’ tax and UIF contributions as well as SDL must be paid over to SARS within seven days after the end of the month during which the amount was deducted or due or such longer period as the Commissioner determines.

- Where the seventh day falls on a Saturday, Sunday or public holiday, the payment must be made not later than the last business day prior to such day. These cut-off dates apply to SDL and UIF contributions as well.

|

Monthly declaration | - The employer must submit such declaration as the Commissioner may prescribe when making any payment. The prescribed EMP201 must be requested by the employer for payment purposes each month.

- Payments in respect of employees’ tax, SDL and UIF contributions must be reflected correctly and separately on the EMP201 in order to avoid the incorrect allocation of these payments and the unnecessary issue of final demands.

|

Requesting an EMP201 | - Employer must request EMP201 declaration from SARS:

|

Employer personally liable | - An employer who fails to deduct or withhold the full amount of Employees’ tax and / or UIF contributions is personally liable for the shortfall.

|

Payments | |

Allocation of payments | - Where any payment is made by an employer in respect of Employees’ Tax, SDL and UIF, such payment will be allocated in the following order:

- Penalty;

- Interest, to the extent to which the payment exceeds the amount of penalty;

- Employees’ tax or additional penalty, to the extent to which the payment exceeds the amount of penalty and interest.

- Where there is a shortfall after the allocation of penalties and interest and the outstanding tax has not been covered in full, interest will continue to accrue on the outstanding tax. These rules are also applicable to SDL and UIF contribution payments.

- SARS may allocate any payment against the oldest tax and/or the oldest interest where no designation on an account has been received excluding amount not yet due.

|

Interest and Penalty

| Reference to the Act | Chapter 15 of the TA Act Paragraph 6(1) of the Fourth Schedule Section 89bis(2) Sections 11, 12(1) and 12(3) of the SDL Act Section 13(1) of the UIC Act |

| Meaning | - Interest and penalty may be imposed on late payments or outstanding amounts.

- A penalty equal to 10% in addition to the interest will be imposed on late payments or outstanding amounts.

- Interest is payable at the prescribed rate if any amount of Employees’ tax, SDL or UIF contributions is not paid in full within the prescribed period for payment of such amount.

- If the employer fails to pay an amount with intent to evade his/her obligation, he/she may be liable to pay penalty not exceeding an amount equal to twice amount of employees’ tax, SDL or UIF contributions which employer so failed to pay.

|

Offences

Reference to the Act | Chapters 15, 16 and 17 of the TA Act Paragraph 30(1) of the Fourth Schedule |

Meaning | - Any person will be guilty of an offence and liable on conviction to a fine or imprisonment where he/she:

- Fails to:

- Deduct employees’ tax from remuneration or to pay tax to the Commissioner within the prescribed period;

- Deliver IRP5/IT3(a) to employees or former employees within the prescribed periods

- Apply for registration as an employer;

- Comply with a written request for information;

- Notify the Commissioner of a change of address; or that he/she has ceased to be an employer;

- Comply with the conditions for using a mechanised system for printing IRP5/IT3(a) to be issued to employees or former employees;

- Maintain a record of remuneration paid and tax deducted

- Comply with any condition prescribed by the Commissioner in regard to the manner in which IRP5/IT3(a) may be used, the surrender of unused stocks of certificates, accounting for used, unused and spoiled IRP5/IT3(a) when required by the Commissioner to do so or to surrender unused IRP5/IT3(a) when ceasing to be an employer;

- Comply with an Income Tax directive issued by Commissioner

- Uses/applies employees’ tax deducted or withheld, for purposes other than the payment of such amount to the Commissioner;

- Permits a false IRP5/IT3(a) to be issued or knowingly is in possession of or uses a false IRP5/IT3(a);

- Alters an IRP5/IT3(a) issued by any other person, purports to be employee named on any IRP5/IT3(a) or obtains a credit for his/her own advantage or benefit in respect of employees’ tax deducted or withheld from another person’s remuneration;

- Not being an employer and without authority from an employer issues or causes to be issued, any document purporting to be an IRP5/IT3(a);

- Furnishes false information or misleads his/her employer regarding the amount of employees’ tax to be deducted in his/her case;

- Defaults in rendering a return.

|

Penalty clause | - An employer shall be guilty of an offence may be fined or sentenced to imprisonment for a period not exceeding 12 months.

|

Tax Directives

Purpose of a Tax Directive

Reference to the Act | Paragraph 9(3) of the Fourth Schedule |

Meaning | - A directive is an authorisation issued by SARS to the employer/ fund administrator on how to deduct employees’ tax from certain payments.

- Tax calculations according to the tax directive shall be calculated and be determined by the Commissioner.

|

Rules related to tax directives | - The following rules relate to a tax directive:

- A tax directive is only valid for the tax year or period stated thereon;

- Employers may not act upon photocopies of directives;

- Employers may under no circumstances deviate from the instructions of the directive;

- Tax directives issued to electronic clients via the SARS Interface are valid directives;

- Employers must apply the percentage of employees’ tax as indicated on the directive prior to taking into account allowable deductions for employees’ tax purposes (e.g. pension, retirement annuity fund contributions, etc.).

|

Application forms | - Application forms have been developed for purposes of applying for a specific tax directive and are available on SARS website www.sars.gov. Form A & D, Form B, Form C and Form E are samples of forms to be used by funds and fund administrators must add their own logo and address when submitting applications forms.

- When applying for a tax directive, the employer/fund administrator must ensure that the correct application form is used according to reason for the exit from fund/employer’s service and nature of amount payable to employee/member of fund.

- The forms available are:

- IRP3(a) – Severance benefit paid by employer (e.g. death/retirement/retrenchment). The form must also be used for share options without obligation, Two Pot Savings withdrawal benefit or other lump sums;

- IRP3(b) – Employees’ tax to be deducted at a fixed percentage (e.g. commission agents/personal service provider);

- IRP3(c) – Employees’ Tax to be deducted at a fixed amount (e.g. Paragraph 11 of the Fourth Schedule (hardship) / assessed loss carried forward);

- IRP3(s) – Employees’ tax to be deducted on any amount to be included under section 8A or 8C of the Income Tax Act.

- Form A & D – Lump sum benefits paid by pension and/or provident fund. (e.g. death before retirement/retirement due to ill health/retirement);

- Form B – Lump sum benefits paid by pension or provident fund on resignation/withdrawal/winding up/transfer or payment as defined in Paragraph (eA) of the definition of gross income/future surplus apportionment/unclaimed benefit/divorce payments);

- Form C – Lump sum benefits paid by a RAF to a member (e.g. death before retirement / retirement due to ill health/transfer from one RAF to another before retirement);

- Form E – Lump sum benefits payable after retirement (e.g. Death Member/Former Member after Retirement, Par. (c) Living Annuity Commutation, Death – Next Generation Annuitant, Next Generation Annuitant Commutation, Gn16: Existing Annuity).

- To avoid a delay in the issuing of a directive, certain minimum information is required on the relevant application form. For more information refer to Guide for Tax Directives – External on the SARS website: www.sars.gov.za.

- Normal termination of service: The lump sum paid by an employer to an employee is treated as an annual payment (for example, service bonus) and the applicable formula is used for the calculation of employees’ tax. A gratuitous payment (leave pay that the employee is not entitled to but which is paid out voluntarily by the employer) upon termination of employment that is calculated with reference to leave days, does not constitute leave pay and could be included in the severance benefit amount.

- Leave pay is a payment in respect of services rendered and the amount does not form part of a severance benefit.

|

Employees’ tax | - Retrenchment, retirement or death: A tax directive must be obtained from SARS preferably where employee is registered for Income Tax purposes. The applicable exemption shall be determined by SARS with the processing of tax directive application.

- Normal termination of service: PAYE calculation must be done at the end of the tax period to determine the PAYE.

|

IRP5/IT3(a) details | - Retrenchment, retirement or death: Lump sum amount paid due to retrenchment, retirement, etc. reflect on IRP5/IT3(a) certificate under code 3901.

|

Hardship Due to Illness or other Circumstances

Reference to the Act | Paragraph 11 of the Fourth Schedule |

Meaning | - The Commissioner may, having regard to the circumstances of the case, issue a directive authorising the employer to:

- Refrain from deducting any employees’ tax from the remuneration of an employee;

- Deduct a specified amount of employees’ tax from the remuneration of an employee;

- Deduct an amount of employees’ tax determined in accordance with a specified rate or scale.

|

Reason for directive | This type of directive is issued: - In order to alleviate hardship to that employee due to circumstances outside the control of the employee;

- To correct any error in regard to the calculation of employees’ tax;

- In case of remuneration constituting commission (IRP3(b) application form);

- Where remuneration is paid to a personal service provider (IRP3(b) application form);

|

Application form | - Either an IRP3(b) or IRP3(c) application form must be submitted in respect of the above.

|

Taxation of Multiple Sources of Income

Reference to the Act | Paragraph 2 (2B) of the Fourth Schedule |

Meaning | - Where the person or a taxpayer receives remuneration from more than one employer particularly retirement income in a tax year, are often left with a tax debt due to under payment of PAYE.

|

Reason for directive | This type of directive is issued: - In order to alleviate the burden, the person that is a pension fund, pension preservation fund, provident fund, provident preservation fund, retirement annuity fund when deducting or withholding employees’ tax in respect of any year of assessment, apply the fixed tax rate that the commissioner directs must be used in determining the amount of employees’ tax to be withheld where the person to whom that annuity is paid receives an amount of remuneration from more than one employer.

|

Dividends I.R.O Employee-Based Share Schemes

Reference to the Act | Paragraph (g) definition of “remuneration” of the Fourth Schedule Section 10(1)(k)(i): proviso (dd), (ii), (jj) and (kk), section 31(3)(b)(i) |

| Meaning | - Effective from 1 March 2017 (2018 year of assessment), where any dividend is received or accrued to a person by way of dividend contemplated in the following provisos, these amounts must be included in remuneration and employees’ tax MUST be deducted.

- Pre 1 March 2017 these amounts were only taxable on assessment. From 1 March 2018 in terms of paragraph 11A(4) of the Fourth Schedule, the employer must ascertain from the Commissioner the amount of employees’ tax to be deducted or withheld. The updated tax directive application

|

IRP5/IT3(a) details | Paragraph (dd) of the proviso to section 10(1)(k)(i) - Dividends received or accrued i.r.o of services rendered or be rendered or i.r.o or by virtue of employment or the holding of any office are taxable as ordinary revenue, unless the:

- Dividend received i.ro. of restricted equity instrument as defined in s8C;

- Share is held by the employee, or

- Restricted equity instrument constitutes an interest in a trust.

- Reflect under code 3719. Code 3769 MUST only be used for local dividends linked to foreign services.

Paragraph (ii) of the proviso to section 10(1)(k)(i) - Exemption in s10(1)(k)(i) will not apply to any dividend received by or accrued to a person i.r.o. services rendered or to be rendered i.r.o. of or by virtue of employment or the holding of any office, other than a dividend received or accrued i.r.o a restricted equity instrument as defined in s8C held by that person or in respect of a share held by that person.

- Reflect under code 3720. Code 3770 MUST only be used for local dividends linked to foreign services.

Paragraph (jj) of the proviso to section 10(1)(k)(i) - Dividends i.r.o. of restricted equity instruments will not be exempt if the value of the underlying shares is liquidated in full or in part by means of a distribution before the restrictions on the shares are lifted.

- The exemption will NOT apply where the dividend is derived directly or indirectly from, or constitutes:

- Amount transferred/applied by a company as consideration for the acquisition or redemption of any share in that company;

- Amount received/accrued in anticipation of, or in course of winding up, liquidation, deregistration or final termination of a company; or

- Equity instrument that is not a restricted equity instrument as defined in s8C, that will, on vesting, be subject to that section.

- Reflect under code 3721. Code 3771 MUST only be used for local dividends linked to foreign services.

Paragraph (kk) of the proviso to section 10(1)(k)(i) - The exemption shall not apply to any amount received as dividend as defined in section 8C that was acquired in circumstances contemplated in section 8C(1) if that dividend is derived directly or indirectly from –

- An amount transferred or applied by a company as a consideration for the acquisition or redemption of any share in that company;

- An amount received or accrued in anticipation or in the course of the winding up, liquidation, deregistration or final termination of a company.

Note: paragraph (kk) came into operation on 1 March 2017. - Reflect under code 3723. Code 3773 MUST only be used for local dividends linked to foreign services.

|

Gains made I.R.O. Rights to Acquire Marketable Securities

Reference to the Act | Paragraph 11A of the Fourth Schedule Section 8A |

| Meaning | - The employer must apply for an IRP3 tax directive in order to ascertain the amount of employees’ tax to be deducted or withheld from any gain made by the exercise, cession or release of any right to acquire any marketable security as contemplated in section 8A which applies if the right was obtained before 26 October 2004.

|

Taxable portion | - A tax liability will arise on the day on which the right is exercised or otherwise dealt with and will be calculated as the difference between the amount paid for the marketable security and the market value at that date.

|

Application form | - IRP3(a) application form must be submitted in respect of the above.

|

| IRP5/IT3(a) details | - Reflect under code 3707 on the certificate.

|

Broad-Based Employee Share Plan

Reference to the Act | Paragraph 11A of the Fourth Schedule Section 8B |

| Meaning | - Employees’ tax must be deducted from any amount received by or accrued to the employee during the year from any gain made from the disposal of any qualifying equity share or any right or interest in a qualifying equity share as contemplated in section 8B, which —

- Was acquired in terms of a broad-based employee share plan;

- Is disposed of by the employee within 5 years from the date of grant of that qualifying equity share, otherwise than:

- In exchange for another qualifying equity share;

- On the death of the employee;

- On the insolvency of the employee.

|

Exchange for other qualifying equity share | - If an employee disposes of a qualifying equity share in exchange solely for any other equity share, that other equity instrument in exchange is deemed to be:

- A qualifying equity share which was acquired by the employee on the date of grant of the qualifying equity share disposed of in exchange;

- Acquired for a consideration equal to any consideration given for the qualifying equity share disposed of in exchange.

|

Acquisition of equity shares | - If an employee acquires any equity share by virtue of any qualifying equity share held by the employee, that other equity share so acquired is deemed to be a qualifying equity share which was acquired on the date of grant of the qualifying equity share so held by the employee.

|

Employees’ tax | - Employers must calculate the employees’ tax deductible from any amount received by or accrued to the employee during the year from any gain made from the disposal of any qualifying equity share or any right or interest in a qualifying equity share, in the same manner as tax on an annual payment (bonus).

|

IRP5/IT3(a) details | - Reflect under code 3717 on the certificate.

|

Vesting of Equity Instruments

Reference to the Act | Paragraph 11A of the Fourth Schedule Paragraph 13(1)(a)(iiB) of the Eighth Schedule Paragraphs 64C and 64E of the Eighth Schedule Paragraph 80(1) and 80(2A) of the Eighth Schedule Section 8C |

Reference to Interpretation Note | Note: These provisions are only applicable to any equity instrument acquired on or after 26 October 2004. See Interpretation Note 55. |

Meaning | - A gain or loss must be included in or deducted from income for a year of assessment in respect of vesting of any equity instrument during that year, which was acquired by that taxpayer –

- Through his/her employment or holding of office by a director of any company or any associated institution in relation to that company or from any person by arrangement with the taxpayer’s employer or by any person employed or is a director of that company or associated institution;

- By virtue of any restricted equity instrument held by that taxpayer in respect of which section 8C will apply upon vesting.

- An amount (including any taxable benefits) received by or accrued to an employee under a share incentive scheme operated for benefit of employees which was derived:

- Capital distributions that include further restricted equity instruments are treated as non-events, and the new restricted equity instrument is subject to section 8C. (became effective in respect of any capital distribution or dividends received or accrued on or after 1 January 2011);

- An employer’s involvement in swaps of equity instruments is no longer a pre-requisite for rollover treatment. As long as the new instrument is treated as a restricted equity instrument by the employer or associated institution, the new instrument will be subject to the provisions of section 8C and the swap is a non-event. (applies to acquisitions occurring on or after 1 January 2011);

- An anti-avoidance provision was included to guard against situations where co-employees and directors collude to avoid the deferment of taxation that section 8C achieves. With effect from 1 January 2011, rollover treatment will apply to equity instruments acquired from employees or directors of same employer.

- Any amount received by or accrued to a taxpayer during year of assessment relating to a restricted equity instrument must be included in taxpayer’s income, if that amount does not constitute:

- A return of capital or foreign return of capital by way of distribution of a restricted equity instrument; or

- A dividend or foreign dividend in respect of that equity instrument; or

- Any amount that must be taken into account for purposes of calculating a gain or loss for purposes of section 8C.

|

Exclusions | - Any equity instrument which was previously taxed and subsequently acquired by the exercise or conversion of, or in exchange for the disposal of any other equity instrument is excluded.

- Any capital gain arising from the disposal of an asset by a trust and a trust beneficiary (employee) has a vested right to an amount derived from that capital gain, the trust must exclude any amount which is already been included in the income of the trust beneficiary in terms of section 8C. This exclusion is deemed to have come into operation with effect from 1 March 2017.

- This section in effect, exempts from tax the benefit that is commonly called the stop loss benefit that can accrue in terms of share incentive schemes.

|

| Disposal | - An equity instrument acquired is deemed to vest in the case of:

- An unrestricted equity instrument, when the employee acquires it.

- A restricted equity instrument, at the earliest of:

- When all relevant restrictions cease;

- Immediately

- Before employee disposes of it (except for disposals discussed hereunder);

- After it terminates (if it is an option);

- Before employee dies if all restrictions relating to that equity instrument are or may be lifted on or after death;

- At the time of disposal where the equity instrument is disposed of for an amount less than the market value or where disposal by way of release, abandonment or lapse of an option or financial instrument occurs.

|

Gain | - The gain to be included in the income of the taxpayer, in the case of:

- A disposal, the amount received or accrued in respect of that disposal which exceeds the sum of any consideration in respect of that equity instrument;

- Any other, the sum of:

- Amount by which the market value of the equity instrument determined at the time that it vests in that employee exceeds the sum of any consideration in respect of that equity instrument;

- Excess amount (if any) which exceeds the consideration in respect of the restricted equity instrument where the consideration includes an amount other than restricted equity instruments.

|

Loss | - In the case of a disposal – the amount by which the sum of any consideration in respect of that equity instrument exceeds that amount received or accrued in respect of that disposal;

- In any other case – the amount by which the consideration in respect of the equity instrument exceeds the market value of that equity instrument determined at that time that it vests in that taxpayer.

|

Employees’ tax | - Where the taxpayer (employee or director) disposes an acquired restricted equity instrument to any person by either a non-arm’s length disposal or the disposal to a connected person this will not be regarded as vesting of the equity instrument and will not attract a taxable gain or loss. The vesting event (i.e. a gain or loss) will continue to remain in the hands of the employee/director.

- The time of disposal of an equity instrument is the time that the equity instrument vests in the beneficiary as contemplated in section 8C.

|

Capital gains implications | - Any capital gain or loss must be disregarded in respect of any restricted equity instrument where:

- Restricted equity instrument is replaced with another restricted equity instrument; or

- Taxpayer disposes the restricted equity instrument to any person by a non-arm’s length disposal or a disposal to a connected person.

|

No value | - Where a capital gain/loss is determined in respect of the vesting by a trust of an asset for a resident trust beneficiary, the gain/loss must be disregarded in the trust and must be taken into account in the hands of the beneficiary.

- When the equity instrument vests in the taxpayer, the gain will be subject to the deduction of employees’ tax. The full gain must be shown on the IRP5 certificate. The employer must apply for an IRP3 tax directive in order to ascertain the amount of employees’ tax to be deducted or withheld from any gain in respect of the vesting of any equity instrument as defined in section 8C.

|

Application form | - An IRP3(a) application form must be submitted in respect of the above.

|

| IRP5/IT3(a) details | - Reflect under code 3718 on the certificate.

|

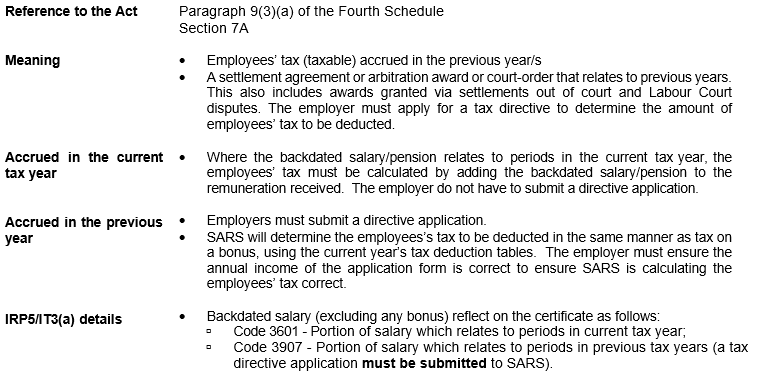

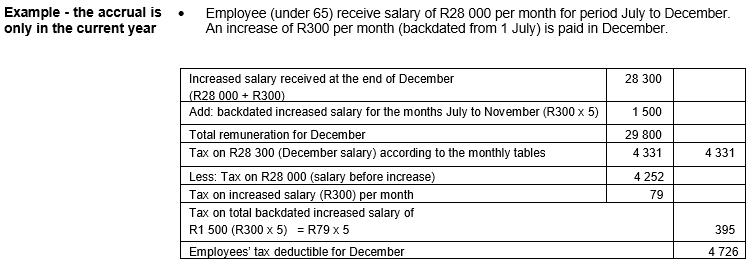

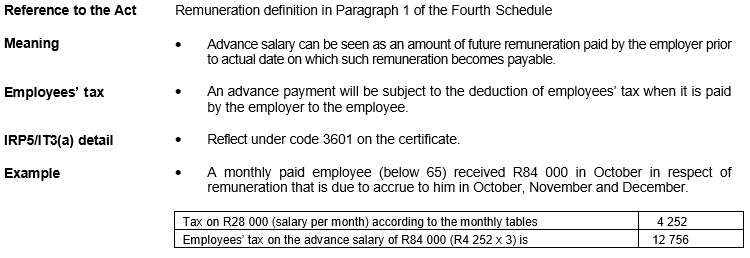

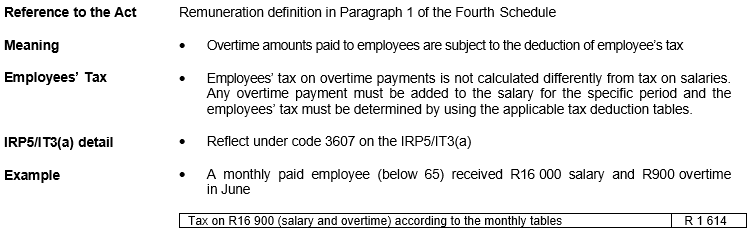

Arbitration Awards

Reference to the Act | Paragraphs (c), (d) and (f) of the definition of gross income in section 1 Paragraph 9(3) of the Fourth Schedule |

| Meaning | - Awards (e.g. CCMA and labour court awards) are remuneration as defined if it can be established that the award is actually in respect of services rendered.

|

| Classification | - Unfair dismissals

- Amounts awarded in respect of unfair dismissals are remuneration as defined in the Fourth Schedule and are therefore subject to deduction of Employees’ Tax.

- Such amounts are received or accrued in respect of the relinquishment, termination, loss, repudiation, cancellation or variation of any office or employment or of any appointment to any office or employment.

- Termination of employment contract prior to its expiry date

- Amounts awarded in respect of termination of an employment contract prior to its expiry date are remuneration as defined in the Fourth Schedule and are therefore subject to the deduction of Employees’ Tax.

- Such amounts are received or accrued in commutation of amounts due under a contract of employment or service or in respect of cancellation or variation of any office or employment

- Unfair labour practices

- Amounts paid or accrued as a result of unfair labour practice, may be included in remuneration as defined.

- SARS will examine the facts of the case and the nature of amounts awarded when the application for a tax directive is received from the employer.

|

Application form | - An employer must apply for a tax directive to determine the amount of employees’ tax to be deducted in respect of the amount payable to an employee or former employee as a result of any arbitration award.

- The reason “other” must be used on the directive application and the amount must be entered in the “Arbitration / CCMA Award” amount field.

Note: The source code reflected on the tax directive must be used on the IRP5 certificate to avoid the rejection of the employees’ return. |

IRP5/IT3(a) details | - The relevant taxable and non-taxable portions of an arbitration award reflect on certificate under:

- Code 3608 (taxable amount); and

- Code 3602 (non-taxable amount).

|

Lump Sum Benefit Payments

Reference to the Act | Second Schedule to the Income Tax Act |

| Meaning | - The provisions of Paragraphs 2(1) and 9(3) of the Fourth Schedule prescribe that trustees or fund administrators must apply for a tax directive at SARS before a lump sum benefit from a pension, pension preservation, provident, provident preservation or retirement annuity fund may be paid.

|

Application form | - The relevant application forms A and D, B, C or E are furnished by the administrators of the relevant funds in accordance with the instructions contained in the Government Gazette No. 22577 (notice no. 1893) dated 24 August 2001.

|

Lump sum payments in respect of withdrawal | - In respect of withdrawal (e.g. resignation, transfer, future surpluses, divorce, housing loan payments, emigration withdrawal, Visa expiry or discontinued contributions):

- Lump sum payments with a date of accrual prior to 1 March 2009:

- From a Pension, Pension preservation or RAF must reflect under code 3902 on the certificate;

- From a Provident or Provident preservation fund must be reflected under code 3904 on the certificate;

- Due to surplus apportionments after 1 January 2006 and NOT paid in terms of section 15B of the Pension Funds Act of 1956 must be reflected under code 3902 or 3904 (according to the fund type) on certificate;

- Due to a court order in respect of a divorce or housing loan must be reflected under code 3902 or 3904 (according to the fund type) on certificate.

|

IRP5/IT3(a) details | - Lump sum payments with a date of accrual after 1 March 2009:

- Withdrawals from a Pension, Pension preservation, Provident, Provident preservation or RAF must be reflected under code 3920 on certificate except for paragraph (eA) of the definition of gross income in section 1;

- Future surplus paid in terms of section 15C of the Pension Funds Act of 1956 reflect under code 3921 on the certificate;

- Due to a court order in respect of a divorce orders, reflect under code 3920 on certificate;

- Due to a withdrawal after retirement from a living annuity in terms of paragraph (c) of the definition of living annuity, where the value of the assets become less than the amount prescribed by the Minister in the Gazette, reflect under code 3921 on certificate.

- With effect from 1 March 2011, the retirement lump sum rate of tax is applicable to the commutation of a living annuity and source code 3915 with the tax code 4115 must be used on the certificate.

- Lump sum payments prior to 1 October 2007 from a:

- Pension or RAF reflect under code 3903

- Provident Fund reflect under code 3905

- Lump sum payments after 1 October 2007 from a Pension, Pension preservation, Provident, Provident preservation or RAF reflect under code 3915

- Lump sum payments by unapproved funds reflect under code 3907

- Unclaimed benefits with date of accrual prior to 1 March 2009 and in terms of the provisions of Interpretation Note 99 reflect under code 3909. This code is applicable from 2007 to 2009 years of assessment.

- Retirement lump sum benefits paid according to paragraph (eA) of the definition of gross income in section 1 reflect under code 3614. These types of benefits include:

- A member of a public sector fund who transfer from a Pension Fund to a Provident Fund while the member remains effectively in the employment of the same employer;

- Any amount which has become payable to the member of a public sector fund or is being utilised to redeem a debt while the member remains effectively in the employment of the same employer.

- Lump sum payments accruing after 28 February 2009 from a Pension or Provident Fund in respect of termination of services per subpa 2(1)(a)((ii)(AA) or (BB) of Second Schedule to Income Tax Act (e.g. retrenchment) reflect under code 3915.

- Lump Sum payments due to retrenchment accruing before 1 March 2009 must be dealt with as withdrawal benefit and average rate in terms of section 5(10) of the Income Tax Act is applicable.

- Either source code 3902 or 3904 must be used.

- The tax portion according to the relevant tax directive must be reflected under:

- Code 4102 if the lump sum payment reflects under code 3902, 3903, 3904, 3905, 3907, 3908, 3909 or 3614;

- Code 4115 if the lump sum payment reflects under code 3915, 3920, 3921, 3922, 3923 (to 2024 year of assessment) and 3924.

|

Lump Sums by Employers – Severance Benefits

Reference to the Act | Definition of “Severance benefit” in section 1 Definition of “Gross income” in section 1 Paragraph 9(3) of the Fourth Schedule |

Meaning | - Severance benefit means any amount (other than a lump sum benefit or an amount contemplated in paragraph (d) (ii) or (iii) of definition of gross income) received by or accrued to a person by way of lump sum from or by arrangement with person’s employer or an associated institution in relation to that employer in respect of relinquishment, termination, loss, repudiation, cancellation or variation of person’s office or employment or of person’s appointment (or right or claim to be appointed) to any office or employment, if such:

- Person has attained the age of 55 years;

- Relinquishment, termination, loss, repudiation, cancellation or variation is due to the person becoming permanently incapable of holding the person’s office or employment due to sickness, accident, injury or incapacity through infirmity of mind or body;

- Termination or loss is due to:

- Person’s employer having ceased to carry on or intending to cease carrying on the trade in respect of which the person was employed or appointed;

- Person having become redundant in consequence of a general reduction in personnel or a reduction in personnel of a particular class by the person’s employer, unless, where the person’s employer is a company, the person at any time held;

- More than five per cent of the issued share capital; or

- Members’ interest in the company.

- Provided that any such amount which becomes payable in consequence of or following upon the death of a person must be deemed to be an amount which accrued to such person immediately prior to his or her death.

|

| Exclusion | - Any amount paid/payable due to services rendered should not be included in the severance benefit amount on the tax directive application form,

- For an example amounts in terms of paragraph (c) or (f) of gross income or bonuses or pro-rata bonus.

- ‘Notice pay’ should also be excluded from the ‘severance benefit’ amount on the tax directive application form.

- The amount must be included as normal income on the IRP5 certificate.

|

Leave payment | - Please note that leave pay is a payment in respect of services rendered and does not form part of a severance benefit. The normal bonus calculation should be used to calculate the tax. The leave payment amount should not be included on the directive since it must be included in the normal income.

|

Application form | - An IRP3(a) application form must be submitted in respect of the above.

- Paragraph 9(3) of the Fourth Schedule prescribes that the employer must submit a directive application before paying out a lump sum to the employee.

- The severance benefit reasons (e.g. severance benefits – retrenchment, severance benefits – death, etc.) must be used.

|

IRP5/IT3(a) details | - The severance benefit rates will be applicable where the employer uses the severance benefit reasons on the IRP3(a) directive application form and source code 3901 must be used on the IRP5/IT3(a) certificate.

- The full amount reflect under code 3901 and the tax under code 4115 on the IRP5 certificate. If IT3(a) certificate is issued, reason code 04 must be used.

|

Lump Sum Compensation for Occupational Death

Reference to the Act | Section 10(1)(gB)(iii) |

| Meaning | - Lump sum payments accruing after 1 March 2011 from a compensation fund in respect of lump sum compensation paid by the employer as a direct result of an occupational death of an employee.

- These payments must be in terms of the Compensation for Occupational Injuries and Diseases Act, 1993 and within the requirements of Section 10(1)(gB)(iii) of the Income Tax Act, as amended.

- Provided that any such amount which becomes payable in consequence of or following upon the death of a person must be deemed to be an amount which accrued to such person immediately prior to his/her death.

|

Application form | - An IRP3(a) application form must be submitted in respect of the above.

|

IRP5/IT3(a) details | - The tax portion according to the relevant tax directive reflect as follows:

- Under code 4115 if the lump sum payment reflects under code 3922 on the IRP5/IT3(a) with effect from 2012 year of assessment.

|

| Exemption | - The death lump sum benefit will be exempt if:

- The death benefit is paid in terms of the Compensation for Occupational Injuries and Diseases Act;

- The employer must pay this amount;

- A maximum amount of R300 000 will be exempt.

|

Employer-Owned Insurance Policies

Reference to the Act | Paragraphs 2(e), 2(k) and 12C of the Seventh Schedule Paragraph 2(4) of the Fourth Schedule Sections 10(1)(gH) and 10(1)(gI) |

| Meaning | - Employers enter into insurance policies arrangements for the benefit of employees or directors, or for their dependants and nominees.

- These policies make payment upon the death, disability or severe illness of an employee of such employer.

- Employer incurs premiums in respect of a policy of insurance that relates to the death, disability or severe illness of employees for direct or indirect benefit of those employees.

- Employers are entitled to a premium deduction in respect of such policy.

- However the payment of these insurance premiums shall give rise to a simultaneous fringe benefit inclusion for employees.

- Where the employer is the named beneficiary and has an arrangement with employee to pay over the proceeds to the employees, the tax treatment should be the same as for payments made directly by the insurer to the employee.

- The fringe benefit will arise on a monthly basis in respect of employer- owned insurance policies for the direct and indirect benefit of employees.

- Lump sum payments accruing on or after 1 March 2012 in respect of policy of insurance are exempt from income tax in terms of section 10(1)(gH) –

- If the policy relates to death, disablement or severe illness of an employee or director, or former employee or director of the person that is a policy holder; and

- No amount of premiums payable for that policy was tax deductible with effect from 1 March 2012 from the income of the policy holder (employer).

- Section 10(1)(gI) exempts any lump sum payment received or accrued in respect of policy of insurance relating to death, disablement, illness or unemployment of the person who is a policy holder or an employee of a policy holder in respect of that policy of insurance to an extent that the benefits from that policy are paid as a result of death, disablement, illness or unemployment, with effect from 1 March 2015.

|

IRP5/IT3(a) details | - Taxable fringe benefit reflect under income source code 3801 on IRP5/IT3(a) certificate.

- The lump sum proceeds in respect of the employer-owned insurance policies must be reflected under the income source code 3908 on the IRP5/IT3(a) certificate where the premiums were included as a fringe benefit and the lump sum is not taxable.

- The lump sum proceeds in respect of the employer-owned insurance policies that should be taxable must be reflected under the income source code 3907 on the IRP5/IT3(a) certificate.

|

| Application form | - An employer is required to apply for a tax directive where any lump sum amount in respect of the employer-owned policy proceeds is payable to an employee.

|

Classification of Employees

Labour Broker

Reference to the Act | Labour broker and employee definition in Paragraph 1 of the Fourth Schedule Paragraph 2(5) of the Fourth Schedule Paragraph (cA) of the definition of gross income in Section 1 |

| Meaning | - The provision or procurement of workers as opposed to the provision of service is of importance.

|

| Client | - Typically, a labour broker arrangement will involve three parties, namely the client, the labour broker and the worker(s).

- The person who specifies the workers required.

- A written or oral service contract would arise between the client and the labour broker where the service conditions of the workers may or may not be stipulated.

- Payments for the workers’ services are made to the labour broker

|

Labour broker | - Is a natural person who, for reward, provides and remunerates workers for a client and is either in or not in possession of an exemption certificate (IRP30).

- The labour broker either makes available his/her own employees to perform work for a client or procures workers for a client.

- The labour broker pays the workers.

|

Workers | - These workers can be any person, including

- Members and/or employees of a close corporation;

- Directors and/or employees of a company;

- Trustees and/or employees of a trading trust;

- Proprietors and/or employees of a business;

- Partners and/or employees of a partnership.

|

Exemption certificate (IRP30) | - Fourth Schedule makes provision for an exemption certificate to be issued by SARS to a labour broker, which will absolve employers from having to deduct Employees’ tax from any payments made to such labour brokers.

- SARS shall not issue an exemption certificate if more than 80% of the gross income of labour broker during the tax year consists of amounts received from any one client, unless labour broker employs three or more full-time employees throughout tax year:

- Who are not connected persons in relation to that labour broker, or

- Who are on a full-time basis engaged in the business of that labour broker of providing persons to or procuring persons for clients of that labour broker

- The labour broker provides to any of its clients the services of any other labor broker; or

- The labour broker is contractually obliged to provide a specified employee of the labour broker to render any service to such client

- An exemption certificate is only valid from the date of issue until the end of the tax year.

- Labour broker must apply annually on an IRP30(a) form for a new exemption certificate

at a SARS branch at least two months before expiring of current exemption certificate. - If the issue of an exemption certificate is delayed for longer than a calendar month, the date of validity will be altered from the date of issue to the date the application was received.

- In such cases any employees’ tax deducted is refundable by the relevant employer.

- An exemption certificate will only be valid if it:

- Is not outdated;

- Bears a labour broker reference number beginning with a 7;

- Has been computer printed;

- The labour broker is in possession of the original; and

- Has not been altered in any way.

- If a labour broker is in possession of a valid exemption certificate and undergoes a change of name, the original certificate must be returned to the relevant SARS branch together with an application for a new certificate, which indicates the changed particulars.

- If an exemption certificate has been lost or misplaced, application for a replacement certificate must be made to SARS Head Office and the replacement certificate will only be issued during the period of validity of the original certificate.

- If a labour broker is not in possession of a valid exemption certificate (IRP30), all payments made to the labour broker will be subject to employees’ tax.

|

Employees’ tax | - An employer who does not deduct employees’ tax from a payment to a labour broker must be in possession of a certified copy of an exemption certificate (IRP30) that must be retained for inspection purposes.

- The deduction is classified in the following categories:

- Labour broker with exemption certificate – no employees’ tax must be deducted;

- Labour broker without an exemption certificate – employees’ tax must be deducted according to the applicable deduction tables;

- Labour broker with a tax directive – employees’ tax must be deducted according to the instructions on the tax directive

- The employees’ tax deducted for a labour broker whether calculated according to the deduction tables or a tax directive must be reflected as PAYE.

|

IRP5/IT3(a) details | - The remuneration reflect under code 3619 on the IRP5/IT3(a) certificate in the case of a labour broker with exemption certificate.

- The remuneration reflect under code 3617 on the IRP5/IT3(a) certificate in the case of a labour broker without exemption certificate.

- The reason code for non-deduction of employees’ tax (where applicable) reflect as 07 on the IRP5/IT3(a) certificate.

|

Independent Contractor

Reference to the Act | Income earned by an independent contractor is specifically excluded from the definition of remuneration in Paragraph 1 of the Fourth Schedule |

| Meaning | - In distinguishing between an employee and an independent contractor / trader one must commence with an analysis of the employment contract.

- The object of the contract (or the parties’ rights and obligations under the contract) must be established.

- The object of the contract is not a mere indicator, but determines the legal nature of the contract.

- The object to be established is the pre-eminent object, for example, if the object is the surrender of productive capacity (whether capacity to provide a service or to produce things), then the contract is for employment of an employee.

- The essence of an employee’s contract (contract of service) is the placing of one person’s services (labour) at the disposal of another, enabling the acquisition of that service itself and not simply the fruits of that productive capacity.

- If the object is the acquisition of the result of deployed productive capacity (of a produced thing or of a provided service), then the contract is for the employment of an independent contractor. The essence of an independent contractor’s contract (contract for services or work) is that the independent contractor only commits himself/herself to deliver the product or end result of that capacity.

|

Deemed independent contractor | - The person will be deemed to be an independent contractor if he/she throughout the year of assessment employs three or more employees (other than any employee who is a connected person in relation to such person) who are on a full-time basis engage in the business of persons rendering any such service and providing that neither of the above two proviso’s under exceptions are applicable

|

| Exceptions | - The Fourth Schedule prescribes that the independent contractor’s income will be deemed to be remuneration and will therefore be subject to Employees’ Tax, if —

- The services are required to be performed mainly at the premises of the person by whom the remuneration is paid/payable or of the person to whom such services were or are to be rendered;

- The person who renders or will render the service is subject to the control and supervision of any other person as to the manner in which his/her duties are performed or to be performed or as to his/her hours of work

|

| Important | - The employer, being a party to the employment contract, is in the best position to determine whether or not the employee is an independent contractor. SARS has therefore provided certain guidelines in order to assist the employer with this responsibility.

- These guidelines are available in Interpretation Note 17 and can be obtained on the SARS website www.sars.gov.za.

|

Employees’ tax | - The employees’ tax deducted for an independent contractor whether calculated according to the deduction tables or a tax directive must be reflected as PAYE.

|

IRP5/IT3(a) details | - Reflect under code 3616 on the IRP5/IT3(a) certificate.

|

Directors of Private Companies/Members of Close Corporations

Reference to the Act | Employee definition in Paragraph 1 of the Fourth Schedule Paragraph 2(1) of the Fourth Schedule, Section 7B Definition of a company in Section 1 |

| Meaning | - The definition of employee includes a director of a private company.

- Any remuneration paid or payable to a director of a private company or a member of a close corporation is therefore subject to the deduction of Employees’ Tax from 1 March 2002.

- The definition of a company includes a close corporation and therefore, the same rules for the deduction of employees’ tax from the remuneration of directors of private companies apply to members of close corporations.

- This definition includes a person who, in respect of a close corporation, holds any office or performs any functions similar to the functions of a director of a company other than a close corporation.

- Effective from 01 March 2017, any variable remuneration received by a director will accrue on the date on which it is paid to the director.

|

Right of recovery | - The employer has the right to recover the PAYE on the deemed remuneration paid by the company from the director. This recovery may, in addition to any other right of recovery, be recovered from any amount which is or may become payable by the company to the director. The director is not entitled to receive an IRP5/IT3(a) in respect of the amount of employees’ tax paid by the company on the deemed remuneration if the company has not recovered the employees’ tax from the director.

|

Director status changes to employee | - Where the person ceases to be a director but remains an employee of the company, section 7B will no longer be used and PAYE must be deducted from remuneration that is actually paid or is payable to the employee. Only one IRP5/IT3(a) needs to be issued for the year.

|

Director appointed during tax year | - Where a person is appointed as a director of a private company during the tax year and the director was not previously an employee of that company, PAYE will be payable on the actual remuneration which is paid or is payable to the director during that tax year.

- The remuneration shown must be the amount of actual remuneration which is paid / payable to the director for the tax year.

- The amount of PAYE will be the sum of the PAYE that was deducted from the actual remuneration of the director and the PAYE paid by the company in respect of the deemed remuneration of that director.

|

IRP5/IT3(a) details | - Salaries paid to directors reflect under code 3615 (only applicable from 2003 to 2018 years of assessment) and all other components of the remuneration (bonus, allowance, benefits, etc.) must be reflected against the existing codes. Code 3601 must be used from 2019 year of assessment.

|

Non – Executive Director (NED) | - The director’s fees received by a resident NED are not regarded as remuneration and the employer is not obligated to deduct/withhold employees’ tax. The director can request a voluntary deduction of employees’ tax.

- If the voluntary deduction is requested, then this income must reflect under code 3620 on the IRP5/IT3(a) certificate.

- Should the resident NED choose not to voluntary pay employees’ tax (PAYE), the employer should not deduct tax and not issue an IRP5/ IT3 (a) certificate.

- Where the NED is a non-resident, the directors’ fee received is regarded as remuneration and the employer must deduct employees’ tax on the amount of directors’ fees payable

- The remuneration must reflect under code 3621 on the IRP5/IT3(a) certificate.

|

Standard Employment

Seasonal Workers

Reference to the Act | Employee definition in Paragraph 1 of the Fourth Schedule |

| Meaning | - A seasonal worker is a person who is only employed during a peak period for a specific period, for example:

- Persons employed on a fruit farm during the picking season to pick and pack fruit;

- Persons employed on a sheep farm to assist with either the lambing or shearing;

- Factories that require additional help during the canning season.

- A tax period commences at the date employee was employed and ends on date his/her employment was terminated.