Purpose

- The purpose of this webpage is to assist employers in determining the amount of employees’ tax to be deducted from remuneration paid/payable according to the prescribed tax deduction tables.

Scope

- This webpage is issued by the South African Revenue Service (SARS) to employers to assist them in calculating the amount of employees’ tax deductible from the remuneration including variable remuneration paid/payable to employees. It further explains the different methods that employers are allowed to apply in this calculation process.

Prescribed Tax Rates

Reference to the Act | Paragraphs 9(1), (2), 10 and 11 of the Fourth Schedule Sections 5 and 6 of the IT Act Section 27(1) of the Public Finance Management Act. |

Meaning | The new tax rates chargeable shall be announced by the Minister of Finance in his / her National Annual Budget as contemplated in the Public Finance Act with effect from a date or dates mentioned in the announcement. Any changes with regard to the rates shall come into effect on the date or dates determined by the Minister of Finance in that announcement and continues to apply for a period of 12 months from that date. |

When to use the tables | In the absence of a tax directive to the contrary as prescribed in Paragraphs 10 and 11 of the Fourth Schedule, employers must make use of the deduction tables prescribed by the Commissioner or use the statutory rates as an alternative. |

Implementation of new rates of tax | The new tax rates must be implemented by employers as soon as possible as contained in the Government Gazette by no later than 1 April of a tax year and employees’ tax must be calculated according to these new rates. Any over deduction of employees’ tax arising as a result of the implementation of new rates not in the employer’s possession on 1 March of each new tax year, may be refunded to the employee as soon as new rates (tables) are implemented. Any under deduction of employees’ tax arising as a result of the implementation of new rates not in the employer’s possession on 1 March of the new tax year, may be adjusted over the remainder of the new tax year (from the date of implementation until 28 February). |

Employee leaves employment before introduction of new tables | If an employee leaves your employment after 1 March of the new tax year but before the implementation of the new rates, the employees’ tax deductions made in accordance with the previous rates are regarded as final. Rebates for individuals which are prescribed in section 6 of the Income Tax Act are deducted from the normal tax determined according to the statutory rates of tax. |

Statutory Rates of Tax

Tax Tables for Individuals and Trusts

2026/2027 Tax Year (1 March 2026 to 28 February 2027)

TAXABLE INCOME (R) | RATES OF TAX (R) |

0 – R 245 100 | 18% of taxable income |

R 245 101 – R 383 100 | R 44 118 + 26% of taxable income above R 245 100 |

R 383 101 – R 530 200 | R 79 998 + 31% of taxable income above R 383 100 |

R 530 201 – R 695 800 | R 125 599 + 36% of taxable income above R 530 200 |

R 695 801 – R 887 000 | R 185 215 + 39% of taxable income above R 695 800 |

R 887 001 – R 1 878 600 | R 259 783 + 41% of taxable income above R 887 000 |

R 1 878 601 and above | R 666 339 + 45% of taxable income above R 1 878 600 |

Tax rebates applicable to individuals | 2027 |

Primary rebate | R 17 820 |

Secondary rebate (for persons 65 years and older) | R 9 765 |

Tertiary rebate (for persons 75 years and older) | R 3 249 |

Tax thresholds applicable to individuals | 2027 |

Persons under 65 years | R 99 000 |

Persons 65 years and older | R 153 250 |

Persons 75 years and older | R 171 300 |

The rebates for individuals must be deducted from normal tax determined according to statutory rates of tax.

- The primary rebate is deductible for all individuals.

- The secondary rebate may only be applied for individuals who will be 65 years or older on the last day of the relevant year of assessment.

- The tertiary rebate is deductible only for individuals who will be 75 years or older on the last day of the relevant year of assessment.

- With effect from 1 March 2014, the Medical Scheme Fees Tax Credit for individuals is a rebate which applies in respect of contributions paid by the taxpayer during the year of assessment to a registered medical scheme. The amount of the rebate (tax credit) is based on the following values per month in the year of assessment in respect of which the contributions were paid in respect of the taxpayer himself/herself, his/her spouse and any dependant of the taxpayer.

Medical scheme fees tax credit | 2027 |

For the taxpayer | R376 |

For the first dependent | R376 |

For each additional dependent | R254 |

Different Versions of Tax Deduction Programs

Differences between tables and tax programs | Small differences may occur between the manual tables, and other computer programs based on the statutory rates of tax. These methods are acceptable in terms of the Income Tax Act provided that the results are within the provisions of this Act. |

Other computer programs | Employers may use computer programs that render the same results, as the results that the employers receive when using the statutory rates of tax. Where an employer use a computerised payroll or his/her/its own created payroll program, the instructions and guidelines as prescribed by SARS must still be followed. |

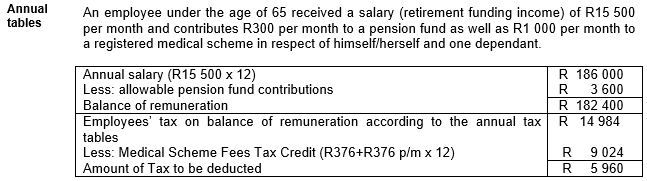

Explanation on how to use the Tax Deduction Tables

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.