Summary

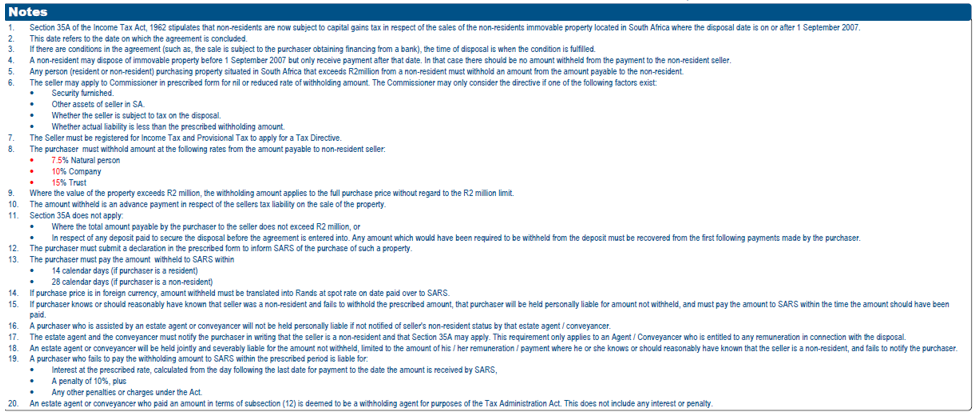

The withholding tax on amounts paid by the Purchaser to Non-Resident sellers of Immovable Property situated within South Africa, as prescribed in Section 35A of the Income Tax Act came into effect from 1 September 2007.

Any person (Purchaser) who is required to pay any amount to a Non-Resident (Seller), or to any other person on behalf of the Seller, in respect of the disposal of Immovable Property in the Republic, must withhold from the amount payable an amount equal to:

- 7,5% of the amount payable, if the seller is a natural person;

- 10% of the amount payable, if the seller is a company; and

- 15% of the amount payable, if the seller is a trust.

Note: Where the value of the property exceeds R2 million, the withholding amount applies to the full purchase price, without regard to the R2 million threshold.

The Seller may apply to the Commissioner, in a format and at the location determined by the Commissioner, for a directive that no amount be reduced or withheld by the purchaser, based solely on:

- Any security furnished for the payment of any tax due on the disposal of the Immovable Property by the seller.

- Whether the seller is subject to tax in respect of the disposal of the immovable property; and

- Whether the actual liability of the seller in respect of tax at the time of the disposal of the immovable property is less than the amount arrived at by applying the percentages of 7, 5%, 10% or 15% as the case may be, stipulated above.

The amount withheld from any payment to the Seller is an advance payment in respect of the seller’s liability for normal tax for the year of assessment during which the property is disposed of by the seller.

If the Seller does not submit a return in respect of that year of assessment within 12 months after the end of that year of assessment, the payment of the amount under subsection (4) is a sufficient basis for an assessment in terms of section 95 of the Tax Administration Act.

Section 35A of the Income Tax Act does not apply to the following:

- If the amounts payable by the Purchaser to the seller and any other person for or on behalf of the Seller, in respect of the acquisition by that purchaser of the Immovable Property, in aggregate do not exceed R2 million, or

- In respect of any deposit paid by the Purchaser for the purpose of securing the disposal of the property by the Seller to that purchaser until the agreement for that disposal becomes unconditional, in which case any amount which would have been required to be withheld from the amount of the deposit must be withheld from the first following payments made by the purchaser in respect of that disposal.

Application of Tax Directive for Withholding and Return Submission

- The Seller, Purchaser, Conveyancer, or Estate agent can download the application and return by logging onto the SARS website at www.sars.gov.za.

- On SARS Home Page >Select Types of Tax

- Select Capital Gains Tax;

- Under the Forms tab, select NR03 (Tax Directive Application by Non-Resident Seller of Immovable Property in SA); or

- Select NR02 (Declaration by Purchaser for Sale of Immovable Property in SA by Non – Resident).

- The Seller/Purchaser/Conveyancer/Estate agent must –

- Click on the form;

- Print the form; and

- Manually complete the relevant information required.

- The Seller/Purchaser/Conveyancer/Estate agent or Representative must complete the mandatory information and submit the application for a Tax Directive (NR03) or the Return (NR02) and the Deed of sale via email.

- Email: [email protected].

- The details of the Taxpayer Engagement Unit to which the applications must be forwarded, are as follows:

| Postal address | Physical Address | Other channel Address |

| Randburg Private Bag X15, Alberton, 1450 | Randburg Branch Office 25 Hill Street Ferndale | Email address: [email protected] |

Note 1: The Seller or Representative is required to request, complete and submit the Tax Directive application by Non-Resident of Immovable Property in SA (NR03) and the Purchaser/Conveyancer/Estate agent must complete and submit the declaration By Purchaser of sale of Immovable Property in SA by Non-Resident (NR02).

Note 2: When applying for the Transfer Duty receipt, the conveyancer must select YES at the question ‘Are the provisions of Section 35A of the Income Tax Act 1962 applicable?’ This is found in the Details of Property container. The NR02 or NR03 must be uploaded along with the Deed of Sale.

- The processing time for the Tax Directive application (NR02)/Return (NR03) is 21 business days.

- When an amount is withheld from a Non-Resident Seller of Immovable Property, it is expected that the Non-Resident should submit a return. If a year passes without submitting a return SARS may regard the amount received/payment as a sufficient basis to raise an assessment.

Completion of Application NR03

- Below information relate to the completion of application Tax Directive form (NR03).

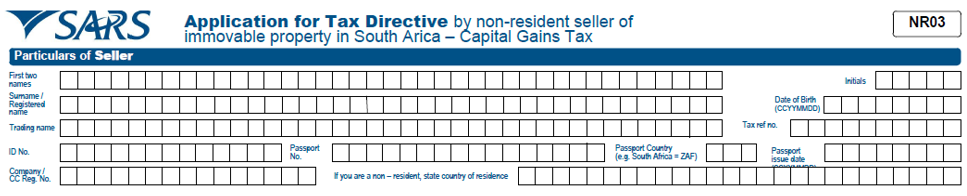

Particulars of Seller

- Complete the following fields for Particulars of Seller

- First two names;

- Initials;

- Surname/Registered Name;

- Trading Name;

- Income Tax Ref. No;

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Passport issue date (CCYYMMDD);

- Company/CC Reg.No,

- If you are non-resident, state country of residence.

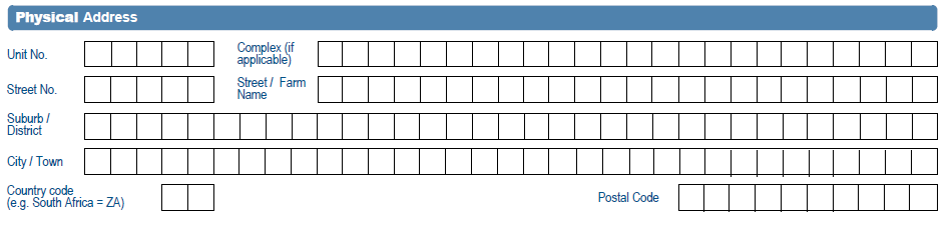

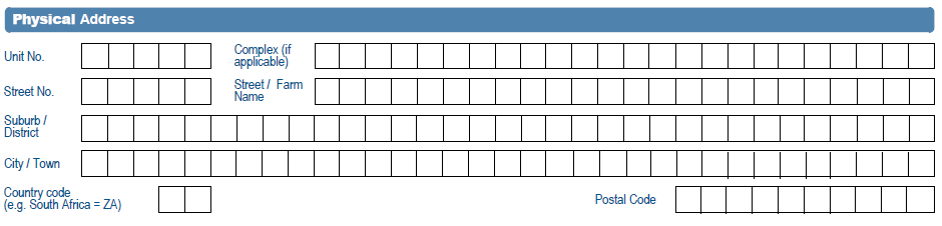

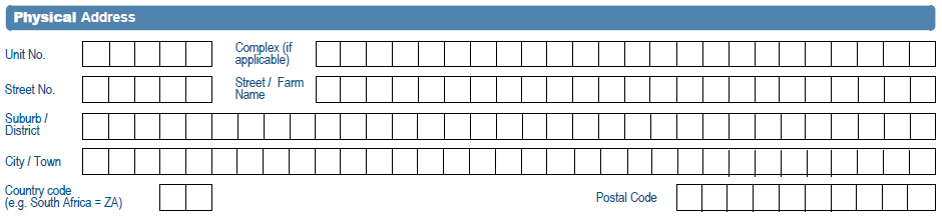

Physical Address

- This is the physical address of the business, i.e. the premises the business is trading from.

- If the business is trading from a flat or townhouse, the actual flat or townhouse unit number must be inserted in “unit no”;

- The name of the block or the block of flats or townhouse complex must be inserted in “complex”, and

- Where the business does not trade from a flat, townhouse or complex these fields are left blank;

- Street No;

- Street/Name of farm;

- Suburb/District;

- City/Town; and

- Postal code.

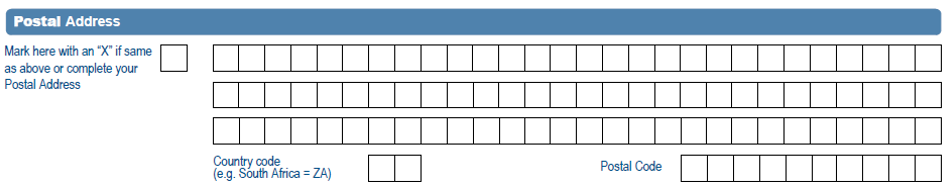

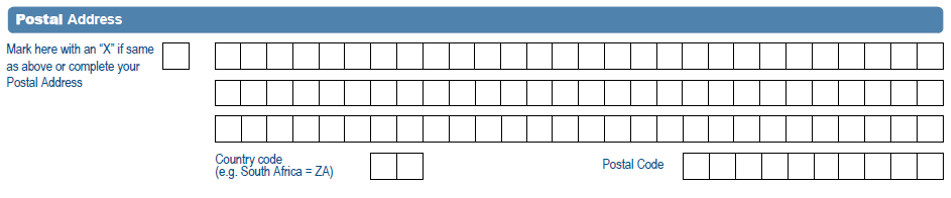

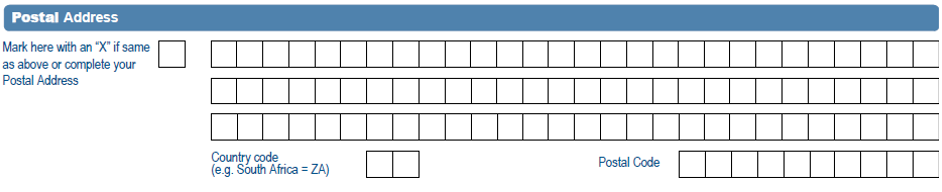

Postal Address

- This is the address that the business would like its post to be sent to. It may be the same as the business address above or it may be a post box number or other address. If it is the same as the business address simply, mark the relevant box with an “X”.

- If the answer is “No”, the following fields will be displayed as open and editable:

- Postal Agency or Other Sub-unit (if applicable) (e.g. POSTNET Suite ID);

- PO Box: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’.

- Private Bag: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Other PO Special Service (specify);

- Number;

- Post Office;

- Postal Code;

- Registered Postal Address indicator.

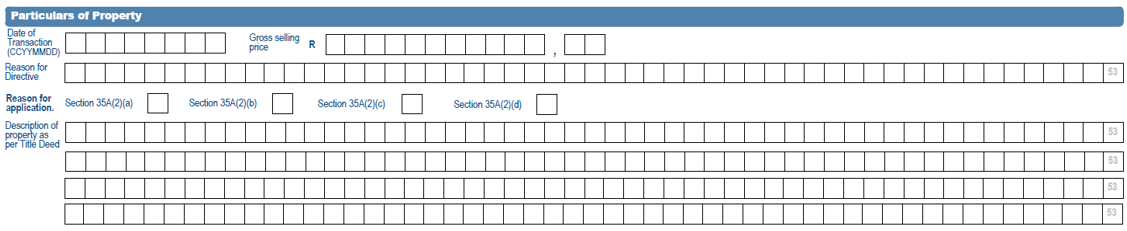

Particulars of Property

- Complete the following fields

- Date of transaction (CCYYMMDD);

- Reason for directive;

- Reason for application: Section 35A(2)(a), Section35A(2)(b), Section 35A(2)(d);

- Description of property as per Title Deed.

Particulars of Purchaser

- Complete the following fields for Particulars of Purchaser

- First two names;

- Initials;

- Surname/Registered Name;

- Trading Name;

- Income Tax Ref. No;

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Passport issue date (CCYYMMDD);

- Company/CC Reg.NO,

- If you are non- resident, state country of residence.

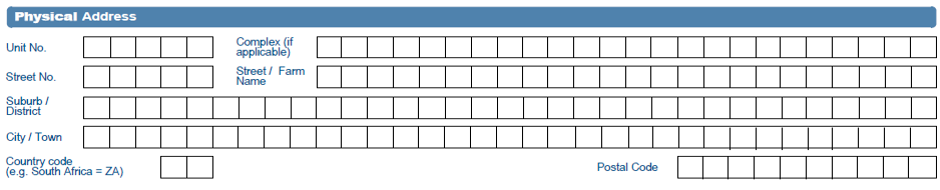

Physical Address

- This is the physical address of the business, i.e. the premises the business is trading from.

- If the business is trading from a flat or townhouse, the actual flat or townhouse unit number must be inserted in “unit no”;

- The name of the block or the block of flats or townhouse complex must be inserted in “complex”, and

- Where the business does not trade from a flat, townhouse or complex these fields are left blank;

- Street no;

- Street/Name of farm;

- Suburb/District;

- City/Town; and

- Postal code.

Postal Address

- This is the address that the business would like its post to be sent to. It may be the same as the business address above or it may be a post box number or other address. If it is the same as the business address simply, mark the relevant box with an “X”.

- If the answer is “No”, the following fields will be displayed as open and editable:

- Postal Agency or Other Sub-unit (if applicable) (e.g. POSTNET Suite ID);

- PO Box: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Private Bag: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Other PO Special Service (specify);

- Number;

- Post Office;

- Postal Code;

- Registered Postal Address indicator.

Calculation of Amount to be Withheld

- Complete the following fields

- Gross selling price (only if gross selling price exceeds R2 million);

- Percentage on gross selling price (Individuals – 7, 5%; Companies – 10%; Trusts – 15%).

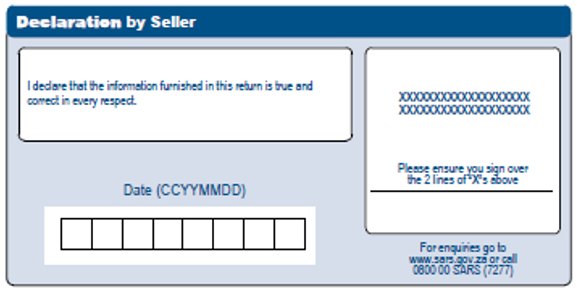

Declaration

- After all the information fields have been completed, the applicant is required to complete, print, and sign the declaration on the first page of the application form. Failure to do so will result in the application being rejected.

Tax Directive Approval or Rejection

- If the seller is not registered for income tax, SARS will register the seller, for the purposes of the withholding tax.

- Once the seller has been registered for income tax, SARS will approve/decline the application according to the requirements as stipulated in Section 35A.

- A letter, Tax Directive (NR03) and third Provisional Payment advice (IRP6) will be issued to the Purchaser/Conveyancer/Estate agent informing him/her of the status of the directive application and the amount payable.

Completion and Submission of the Return (NR02)

- Below information relate to the completion of the Return (NR02)

Particulars of Seller

- Complete the following fields

- First two names;

- Initials;

- Surname/Registered Name;

- Trading Name;

- Income Tax Ref. No;

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Passport issue date (CCYYMMDD);

- Company/CC Reg.NO,

- If you are non- resident, state country of residence.

Physical Address

- This is the physical address of the business, i.e. the premises the business is trading from.

- If the business is trading from a flat or townhouse, the actual flat or townhouse unit number must be inserted in “unit no”;

- The name of the block or the block of flats or townhouse complex must be inserted in “complex”, and

- Where the business does not trade from a flat, townhouse or complex these fields are left blank;

- Street no;

- Street/Name of farm;

- Suburb/District;

- City/Town; and

- Postal code.

Postal Address

- This is the preferred postal address of the business. It may be the same as the business address above or it may be a post box number or other address. If it is the same as the business address simply, mark the relevant box with an “X”.

- If the answer is “No”, the following fields will be displayed as open and editable:

- Postal Agency or Other Sub-unit (if applicable) (e.g. POSTNET Suite ID);

- PO Box: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Private Bag: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Other PO Special Service (specify);

- Number;

- Post Office;

- Postal Code;

- Registered Postal Address indicator.

Description of Property (as per title deed)

- Complete the following fields

- Description of property as per Title Deed.

Name of Public Officer/Trustee

- Complete the following fields

- Surname;

- Initials;

- Date of Birth(CCYYMMDD);

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Income Tax Ref. No;

- Passport issue date (CCYYMMDD);

Particulars of Purchaser/Conveyancer/Estate Agent

- Complete the following fields:

- First two names;

- Initials;

- Surname/Registered Name;

- Trading Name;

- Income Tax Ref. No;

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Passport issue date (CCYYMMDD);

- Company/CC Reg.NO;

- If you are non- resident, state country of residence.

Physical Address

- This is the physical address of the business, i.e. the premises the business is trading from.

- If the business is trading from a flat or townhouse, the actual flat or townhouse unit number must be inserted in “unit no”;

- The name of the block or the block of flats or townhouse complex must be inserted in “complex”, and

- Where the business does not trade from a flat, townhouse or complex these fields are left blank;

- Street no;

- Street/Name of farm;

- Suburb/District;

- City/Town; and

- Postal code.

Postal Address

- This is the address that the business would like its post to be sent to. It may be the same as the business address above or it may be a post box number or other address. If it is the same as the business address simply, mark the relevant box with an “X”.

- If the answer is “No”, the following fields will be displayed as open and editable:

- Postal Agency or Other Sub-unit (if applicable) (e.g. POSTNET Suite ID);

- PO Box: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Private Bag: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’;

- Other PO Special Service (specify);

- Number;

- Post Office;

- Postal Code;

- Registered Postal Address indicator.

Name of Public Officer/Trustee

- Complete the following fields:

- Surname;

- Initials;

- Date of Birth(CCYYMMDD);

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Income Tax Ref. No;

- Passport issue date (CCYYMMDD);

Name of Conveyancer/Estate Agent

- Complete the following fields:

- Surname;

- Initials;

- Date of Birth(CCYYMMDD);

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Income Tax Ref. No;

- Passport issue date (CCYYMMDD);

Name of Conveyancer Firm/Estate Agency

- Complete the following fields:

- Surname;

- Initials;

- Date of Birth(CCYYMMDD);

- ID No;

- Passport No;

- Passport Country (e.g. South Africa = ZAF);

- Income Tax Ref. No;

- Passport issue date (CCYYMMDD);

Calculation of Amount to be Withheld

- Complete the following fields:

- Year of Assessment;

- Date(CCYYMMDD);

- Receipt number;

- Gross selling price(only if gross selling price exceeds R2 million);

- Percentage on gross selling price (Individuals – 7, 5%; Companies – 10%; Trusts – 15%).

- Interest (from :14 days after payment to seller – To : Date of payment of amount withheld to SARS);

- Penalty (10%);

- Total payable;

Notes

- These are the notes in terms of Section 35A.

Payment Process

- If an amount has been withheld from any amount payable in a foreign currency, that amount withheld must be translated to the currency of the Republic (Rand) at the spot rate on the date the amount is paid over to SARS.

- The amount withheld by a purchaser must together with a return be submitted to the Commissioner:

- Where that Purchaser is a resident, within 14 days after the date on which that amount was withheld; or

- Where that Purchaser is not a Resident, within 28 days after the date on which that amount was withheld.

- If a Tax Directive (NR03) was issued by SARS, the Seller/Purchaser/Conveyancer/Estate Agent will be notified of the amount payable, the Declaration by Purchaser for Sale of Immovable Property in SA by Non-Resident (NR02) must accompany the payment to SARS. For all methods of payments, refer to GEN-PAYM-01-G01 – SARS Payment Rules – External Guide.

- If the Seller did not request an NR03 and is registered for Income Tax, the seller will be regarded as a provisional taxpayer. The Purchaser/Conveyancer/Estate agent must submit the third period payment advice (IRP6) in the name of the seller, with the payment to SARS. (Refer to GEN-PAYM-01-G01 – SARS Payment Rules – External Guide).

- If a third provisional payment advice (IRP6) was not received with the original letter and Tax Directive (NR03),

- The (IRP6) can be downloaded from the SARS website: www.sars.gov.za:

- On SARS Home Page >Select Types of Tax;

- Select Provisional Tax;

- Scroll to the bottom of the screen; and

- Below the Top of the Forms tab, select IRP 6 (3) Payment Advice for additional provisional tax.

- The (IRP6) can be downloaded from the SARS website: www.sars.gov.za:

- A payment receipt will be issued to the purchaser/conveyancer/estate agent once the payment is made to SARS.

Completion of Provisional Tax Return (IRP6)

- Completion of Provisional Tax Return (IRP6).

Particulars of Taxpayer (Individual)

- Complete the following details:

- Year of assessment;

- Period:

- First/Second

- Taxpayer Reference Number;

- Date of birth(CCYYMMDD);

- Surname;

- Initials;

- Date on which you ceased to be a resident (CCYYMMDD)

Particulars of Taxpayer (Company/Trust)

- Complete the following details:

- Year of assessment;

- Period:

- First/Second

- Taxpayer Reference Number;

- Registered no.;

- Registered name.

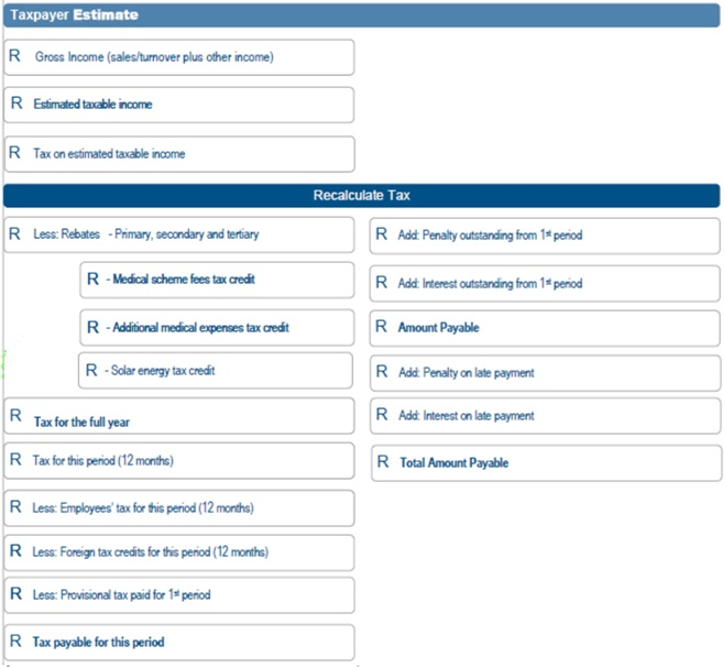

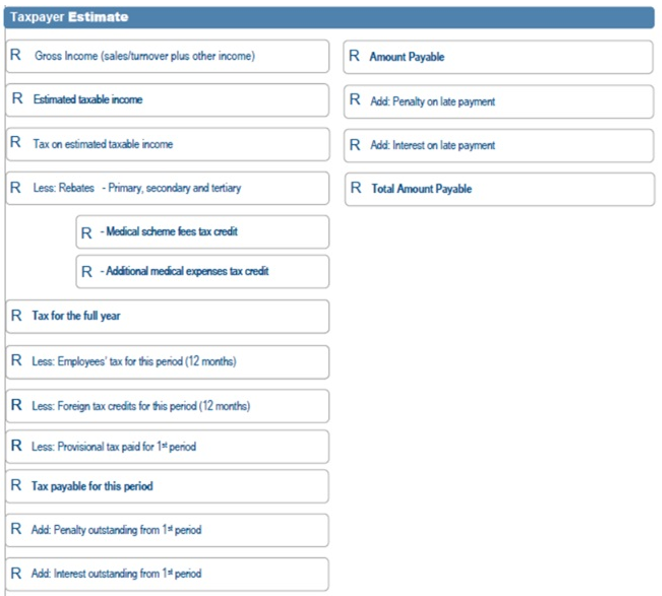

Taxpayer Estimate (Individual)

- Complete the following details:

- Gross Income (sales/turnover plus other income)

- Estimated taxable income

- Tax on estimated Taxable income

- Less:

- Rebates – Primary, secondary and tertiary(for individuals)

- Medical scheme fees tax credit

- Additional medical expense tax credit.

- Tax for the full year;

- Less: Employees’ tax for this period (12 months);

- Less: Foreign tax credits for this period(12 months);

- Less: Provisional Tax paid for 1st period;

- Tax payable for this period;

- Add: Penalty outstanding from 1st period;

- Add: Interest outstanding from 1st period;

- Amount Payable

- Add: Penalty on late payment;

- Add: interest on late payment;

- Total Amount payable for this period

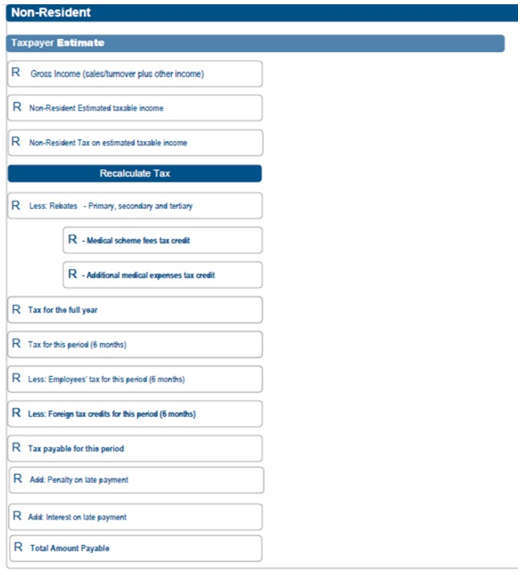

Taxpayer Estimate (Non-Resident)

- Complete the following details:

- Gross Income (sales/turnover plus other income)

- Non-Resident Estimated taxable income

- Non-Resident Tax on estimated Taxable income

- Less:

- Rebates – Primary, secondary and tertiary(for individuals)

- Medical scheme fees tax credit

- Additional medical expense tax credit.

- Tax for the full year;

- Less: Employees’ tax for this period (12 months);

- Less: Foreign tax credits for this period(12 months);

- Less: Provisional Tax paid for 1st period;

- Tax payable for this period;

- Add: Penalty outstanding from 1st period;

- Add: Interest outstanding from 1st period;

- Amount Payable

- Add: Penalty on late payment;

- Add: interest on late payment;

- Total Amount payable for this period

Unusual/Infrequent Amounts included in the Estimated Taxable Income (e.g. CGT, Lump Sums)

- Complete the following field:

- Amount included in estimated taxable income that relates to unusual/infrequent events.

Calculation of the Tax Payable for the Period (Companies/Trust)

- Complete the following details:

- Gross Income (sales/turnover plus other income)

- Estimated taxable income

- Tax on estimated Taxable income

- Less:

- Rebates – Primary, secondary and tertiary

- Medical scheme fees tax credit

- Additional medical expense tax credit.

- Tax for the full year;

- Less: Employees’ tax for this period (12 months);

- Less: Foreign tax credits for this period(12 months);

- Less: Provisional Tax paid for 1st period;

- Tax payable for this period;

- Add: Penalty outstanding from 1st period;

- Add: Interest outstanding from 1st period;

- Amount Payable

- Add: Penalty on late payment;

- Add: Interest on late payment;

- Total Amount payable

Unusual/Infrequent Amounts Included in the Estimated Taxable Income (e.g. CGT, Lump Sums)

- Complete the following field:

- Amount included in estimated taxable income that relates to unusual/infrequent events.

Historical Information

- Complete the following details:

- Year last assessed;

- Taxable income for that year;

- Basic amount.

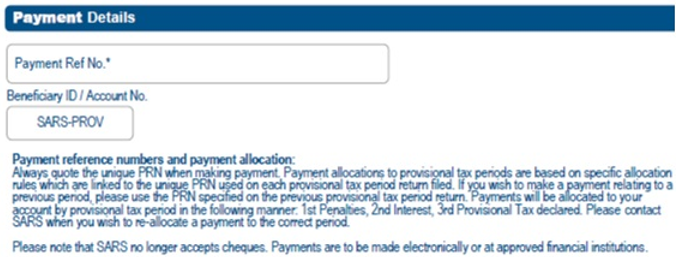

Payment Detail

- Complete the following details:

- Payment reference no(PRN);

- Beneficiary ID/Account number.

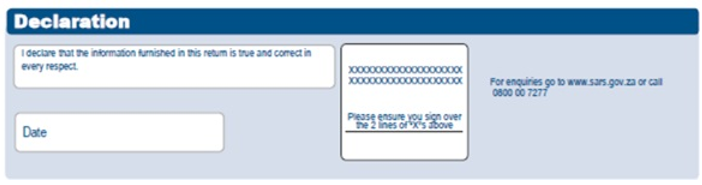

Declaration

- After all the information fields have been completed, the applicant is required to complete, print, and sign the declaration on the first page of the application form. Failure to do so will result in the application being rejected.

- For detailed information regarding Provisional Tax, refer to GEN-PT-01-G01 – Guide for Provisional Tax – External Guide on the SARS website www.sars.gov.za

Failure to Pay the Withholding Tax on Amounts Paid by the Purchaser to Non-Resident Sellers of Immovable Property

- A Purchaser is personally liable if he/she knows or should reasonably have known that the seller is a Non-Resident. The Purchaser must pay the amount to SARS not later than the date on which payment should have been made if the amount was in fact withheld.

- If the Estate agent or Conveyancer has assisted in the disposal of property, a Purchaser will not be held personally liable if not notified of the seller’s Non-Resident status by that Estate agent or Conveyancer;

- Any Estate agent and Conveyancer entitled to any remuneration or other income in respect of services rendered in connection with the disposal of the Immovable Property by the seller or the registration of transfer must, before any payment is made to the seller, notify the purchaser in writing of the fact that the seller is a Non-Resident and that Section 35A may apply. This requirement applies only to an Estate agent / Conveyancer entitled to any remuneration in connection with the disposal;

- If an Estate agent or Conveyancer should reasonably have known that the seller is a Non-Resident and fails to notify the Purchaser, the failing Estate agent or Conveyancer is jointly and severally liable for the payment of the amount which the Purchaser is required to withhold and pay to the Commissioner, but limited to the amount of remuneration or other payment in respect of the services rendered in connection with the disposal of Immovable Property by the seller or the registration of transfer, as the case may be.

- A Purchaser who fails to pay the amount withheld to SARS within the period allowed for payment:

- Is liable for interest at the prescribed rate on any amount outstanding calculated from the day following the last date for payment to the date that the amount is received by SARS; and

- Must pay a penalty equal to 10% of that amount, in addition to any other penalty or charges for which he or she may be liable under the Act.

- Note: No provision is made to waive interest.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.