Summary

- Licensees of Manufacturing Warehouses (VMs), specifically Category 1 manufacturers in the biodiesel industry, are required to complete and submit the DA 162 monthly biodiesel account along with supporting schedules.

- With supporting schedules, this assists SARS to:

- Montor:

- Inputs and Outputs.

- Quantities of biodiesel manufactured.

- Losses or disposals.

- Quantities removed from the Warehouse.

- Collect Excise duties and taxes due.

- Montor:

Completion of the DA 162 Monthly Biodiesel Account and Annexures

- The form required bringing Excise duties; fuel levy and Road Accident Fund (RAF) levy to account is the DA 162 (category 1 commercial manufacturer). The relevant form is the summary of all relevant biodiesel transactions, giving an overall picture of all such transactions during an accounting period, which must be submitted via eFiling.

- The DA 162 and supporting schedules must be completed by the licensee and kept for record purposes.

- If the levy rates that apply to any transactions brought to account are different to the current rates (for example in April each year when rate changes occur, or where earlier year acquittals are brought to account) a separate DA 162 and supporting schedule must be prepared for each rate of levy. In general, supporting schedules are designed to cater for these different rates of levy. Current rate levies appear on schedules with the suffix “A”; previous year’s rates (Current – 1) with the suffix “B”; the year before that (Current – 2) generally with the suffix “C”.

- The boxes described immediately below are to be completed on the DA 162.

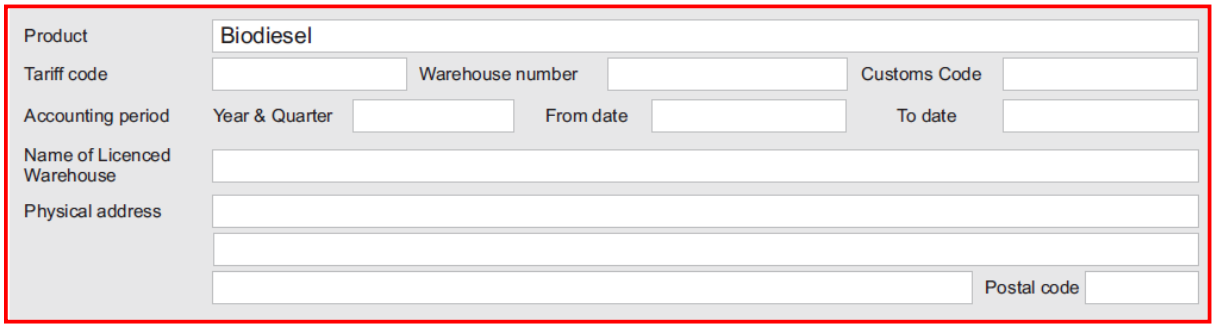

Licensee Detail

- Product – the product name must be inserted in this box: Bio Diesel (Category 1).

- Tariff code – The tariff code for the aforementioned product must be inserted in this box.

- Warehouse number – This box is for the manufacturing warehouse (VM) number.

- Customs code – This box is for the licensees’ Customs code number.

- Accounting period: Year & Month – The year and calendar month in respect of which the account is rendered are to be inserted in this box. The date must use the format CCYYMMDD with no spaces or connecting links such as oblique’s, full stops, colons or dashes.

- From date / To date – These period boxes are provided in order that the first and last day of the accounting month may be indicated. If, for example, the closing date for excise account purposes is the 25th of each month and the excise account in respect of January is rendered, the period would be 26 December to 25 January. The date must again use the format CCYYMMDD with no spaces or connecting links such as oblique’s, full stops, colons or dash.

- Name of Licensed Warehouse – The name under which the VM warehouse is licensed must be inserted in this box.

- Physical Address – The street name, number, suburb, city and postal code must be inserted in this box.

- Postal Code – the postal code must be inserted here.

Duty Calculations

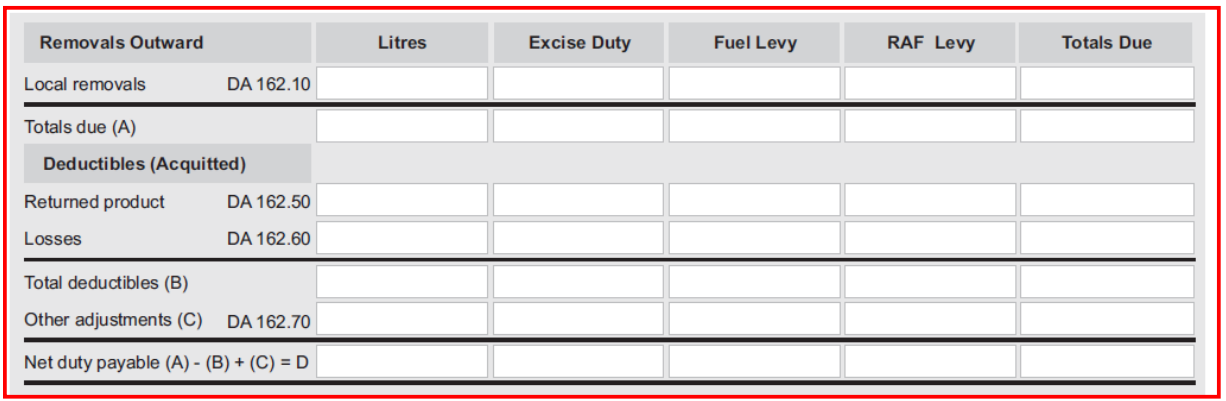

Removals Outwards

- DA 162.10: Local Removals – DA 162.10.A2-Current Rates (April only)

- Details, analysed by the transport mode, in litres of all product destined for local consumption removed from the VM and attracting duty / levies at the rates immediately preceding the currently ruling rates must be inserted;

- The rates of Excise duty, fuel levy and RAF and the final rand values must be captured on the lead schedule (DA 162.10).

- This form would normally only be completed in the month of April.

- Totals due (A) – the totals due on all completed DA 162.10 must be added and entered here.

- Deductables, Acquitted (B)

- Returned Product DA 162.50 {(sub-standard or contaminated) must be captured here}.

- DA 162.50A1: Returned Product: Sub-Standard or Contaminated – Current Rates:

- Full narrative details, with date and document number, and volume in litres, of all products which has been returned to the VM as a result of being found to be sub-standard or contaminated and attracting duty/levies relief at currently ruling rates must be captured

- There is an automatically calculated adjustment for Rule 19A.10 allowances previously granted

- The rates of Excise duty, fuel levy and RAF and the final rand values must be captured on the lead schedule (DA 162.50).

- DA 162.50A2: Returned Product: Sub-Standard or Contaminated – Current Rates-1

- Full narrative details, with date and document number, and volume in litres, of all products which has been returned to the VM as a result of being found to be sub-standard or contaminated and attracting duty / levies relief at the rates immediately preceding the currently ruling rates must be captured.

- There is an automatically calculated adjustment for Rule 19A.10 allowances previously granted.

- The rates of Excise duty, fuel levy and RAF and the final rand values must be captured on the lead schedule (DA 162.50)

- DA 162.50A3: Returned Product: Sub-Standard or Contaminated – Current Rates-2

- Full narrative details, with date and document number, and volume in litres, of all product which has been returned to the VM as a result of being found to be sub-standard or contaminated and attracting duty / levies relief at the rates for the second year preceding the currently ruling rates must be captured.

- There is an automatically calculated adjustment for Rule 19A.10 allowances previously granted.

- The rates of Excise duty, fuel levy and RAF and the final rand values must be captured on the lead schedule (DA 162.50).

- DA 162.50A1: Returned Product: Sub-Standard or Contaminated – Current Rates:

- DA 162.60: Losses which is the sum of A) to E) below:

- DA 162.60A1: Losses – VIS MAJOR – Current Rates

- Full narrative details and volume in litres, of any product which has been lost as a result of vis major and attracting duty / levies relief at currently ruling rates must be captured.

- Before submitting a claim for a VIS MAJOR, loss written authority must be obtained from the Commissioner, granting the claim and must be captured.

- The rates of Excise duty, fuel levy and RAF and the final rand values must be captured on the lead schedule (DA 162.60).

- DA 162.60A2: Losses – VIS MAJOR – Current Rates-1

- This form captures full narrative details, and volume in litres, of any product, which has been lost because of vis major and attracting duty / levies relief at the rates

immediately preceding the currently ruling rates. Before submitting, a claim for a vis major loss written authority must be obtained from the Commissioner, granting the claim (manually insert input). - The rates of Excise duty, fuel levy and RAF immediately preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.60).

- This form captures full narrative details, and volume in litres, of any product, which has been lost because of vis major and attracting duty / levies relief at the rates

- DA 162.60A3: Losses – VIS MAJOR – Current Rates-2

- This form captures full narrative details, and volume in litres, of any product, which has been lost because of vis major and attracting duty / levies relief at the rates for the second year preceding the currently ruling rates. Before submitting, a claim for a vis major loss written authority must be obtained from the Commissioner, granting the claim (manually insert input).

- The rates of Excise duty, fuel levy and RAF for the second year preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.60).

- DA 162.60B1: Losses – Section 75(18)(d) or Section 75(18)(e) – Current Rates.

- The totals must be captured on the DA 162.

- The rates of Excise duty, fuel levy and RAF for the second year preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.60).

- DA 162.60B2: Losses – Section 75(18)(d) or Section 75(18)(e) – Current Rates – 1

- The totals must be captured on the DA 162.

- The rates of Excise duty, fuel levy and RAF immediately preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.60).

- This form would normally only be completed in the month of April.

- DA 162.60A1: Losses – VIS MAJOR – Current Rates

- Total Deductibles (B) which is the sum of DA 162.60A3: Losses – VIS MAJOR – Current Rates-2) and Paragraph here) above must be entered here.

- Returned Product DA 162.50 {(sub-standard or contaminated) must be captured here}.

- DA 162.70: Other Adjustments (Movements & Adjustments after Leaving Refinery Duty Paid). The totals must be captured on the DA 162.

- DA 162.70A1: Other Adjustments (Movements & Adjustments after Leaving Refinery Duty Paid) – Current Rates:

- Full narrative details, and volume in litres, of any unusual or exceptional circumstance,requiring an adjustment not catered for on other forms in this package, and requiring duty/ levies relief or additional duty / levies liability at currently ruling rates must be captured.

The use of this form is likely to occur only in the rarest of circumstances. - Where duty / levies relief is claimed, the volume in litres must be entered as a negative figure (-) and where additional duty / levies liability is being brought to account, the volume in litres must be entered as a positive figure (+).

- The rates of Excise duty, fuel levy and RAF immediately preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.70).

- Full narrative details, and volume in litres, of any unusual or exceptional circumstance,requiring an adjustment not catered for on other forms in this package, and requiring duty/ levies relief or additional duty / levies liability at currently ruling rates must be captured.

- DA 162.70A2: Other Adjustments (Movements & Adjustments after Leaving Refinery Duty Paid) – Current Rates-1

- Full narrative details and volume in litres, of any unusual or exceptional circumstance, requiring an adjustment not catered for on other forms in this package, and requiring duty/ levies relief or additional duty / levies liability at the rates immediately preceding the currently ruling rates must be captured. The use of this form is likely to occur only in the rarest of circumstances.

- Where duty / levies relief is claimed, the volume in litres must be entered as a negative figure (-) and where additional duty / levies liability is being brought to account, the volume in litres must be entered as a positive figure (+).

- The rates of Excise duty, fuel levy and RAF immediately preceding the currently ruling rates and the final rand values must be captured on the lead schedule (DA 162.70).

- DA 162.70A3: Other Adjustments (Movements & Adjustments after Leaving Refinery Duty Paid)- Current Rates-2

- Full narrative details and volume in litres, of any unusual or exceptional circumstance, requiring an adjustment not catered for on other forms in this package, and requiring duty/ levies relief or additional duty / levies liability at the rates for the second year preceding the currently ruling rates. The use of this form is likely to occur only in the rarest of circumstances (manually insert input).

- Where duty relief is claimed, the volume in litres must be entered as a negative figure (-)and where additional duty liability is being brought to account, the volume in litres must be entered as a positive figure.

- The rates of Excise duty, fuel levy and RAF for the second year preceding the currently

ruling rates and the final rand values must be captured on the lead schedule (DA 162.70).

- DA 162.70A1: Other Adjustments (Movements & Adjustments after Leaving Refinery Duty Paid) – Current Rates:

- Net Duty Payable (D) which is Totals Due (A) – Deductibles (B) + other adjustments (C), must be entered here, taking into account that adjustments could either be positive or negative.

Payment Schedule and Amount Payable

- The set date when payment is due should be capture here.

- The payable amount of Excise Duties due must be entered here.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.