Summary

This webpage describes the completion of the DA 70 – ‘Application for Provisional Payment’ (PP).

The PP is lodged in order to protect revenue which is due or may become due to Excise pending compliance of a specified condition by the client or for a possible penalty.

Form Requirements

- Applications to make PP’s must be made on the DA 70 as prescribed in the Customs and Excise Act, No. 91 of 1964 (the Act) and the Rules thereto and may not be altered in any way.

- The DA 70 is commonly referred to as a PP. It must be:

- Printed upright on an A4 size paper;

- Printed in black ink on white paper with a mass of not less than 80 g/m2 (Rule 202.00); and

- Printed back to back and not on two (2) separate pages.

- Information entered on the PP must be typed or printed in block letters and must be legible.

- In all instances where a date is required, such must be completed in the order: century, year, month and day sequence, e.g. 2013/02/15.

- No tippex (correction fluid) is allowed on the PP – changes that must be made are to be neatly crossed out, changed and initialled by the same person who signed or approved the PP.

- The original PP must be clearly endorsed with a stamp impression indicating “ORIGINAL” on the top of the form. In cases where a PP is received at the Office without this “ORIGINAL” indication, the Excise Officer (EO) must endorse the original PP accordingly.

- An original and at least four (4) copies of a PP must be submitted.

- In instances where an EO or team requires a client to lodge a PP, the PP must be completed by the EO or team concerned, if applicable and handed together with the report of the instruction to the client to lodge the PP.

- The client must complete the PP as requested via the inspection outcome and attach a copy of the report thereto.

- Where a deposit covers a contravention, a note advising the client of the procedure prescribed in Section 91 must also be attached.

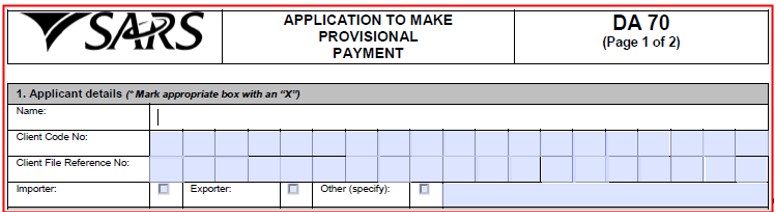

Applicant details

- Name

- The applicant’s name must be entered in this box, e.g. ABC Winery (Pty.) LTD.

- The client’s name can be inserted in brackets if required.

- Client Code No

- The client number allocated to the applicant must be entered in this box.

- The applicant can also be the manufacturer / licensee / registrant / owner.

- The Client file reference No. must be entered in this field if available.

- Importer / Exporter / Other (specify):

- One (1) of the blocks must be completed.

- If the applicant’s name is the same as the information required in this box, it must still be completed.

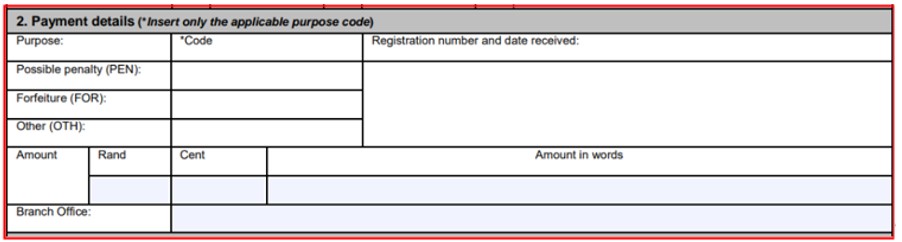

Payment details

- In terms of the Purpose Code, there are only three (3) possible purposes:

- Penalty (PEN);

- Forfeiture (FOR); and

- Other (OTH).

- Enter “Not Applicable”on the registration number and date received field.

- Amount

- The amount of the PP is inserted here in figures and words.

- To verify the correctness of the PP amount, the client must produce a worksheet and where appropriate, a draft declaration reflecting the duties / levies, Tax and / or VAT payable, which must be attached to the original PP.

- The Excise Officer (EO) must verify the worksheet and if correct, print his / her name and sign and date stamp the worksheet.

- In cases where duty / levy Tax and / or VAT is covered pending compliance, the exact amount including cents must be reflected

- Where the PP is completed to cover deposits for contraventions except for VAT penalties, the amount must be reflected in rands only.

- Amounts of the PP are left to the discretion of Controllers / Branch Managers, depending on circumstances and the risk involved. As a general principle Controllers / Branch Managers aspire as far as possible to cover any possible duties / levies, Tax and / or VAT which may become payable. These amounts will naturally be assessed according to the risk, rates of duty and values involved.

- Branch Office

- This is the Branch Office’s name where the PP will be lodged e.g. Stellenbosch.

- No abbreviations must be used in this box.

Circumstances of or reason for the application

- Circumstances of or reason for the application (including, in the case of a deposit as contemplated in Section 91 of the Customs and Excise Act, 1964, the section(s) contravened or not complied with) and a description of the transaction involved:

- In the case where a PP is requested by an EO, the PP must be completed by the EO concerned to ensure the wording etc. are correctly inserted. The completed PP must be handed together with an instruction letter to the client for signature and lodgement of the PP.

- The exact and precise reason for lodging the PP must be inserted in this box. The contravention must be specified in words and referred to the Section / Rule in the Act, which has been contravened on the DA 70 e.g. incorrect tariff heading, under declaration of goods.

- Any wording such as “as per letter” or “as agreed” is not acceptable in this box.

- The reason for making the payment must always reflect

- The reasons and conditions for making the payment,

- The exact requirements to be fulfilled before a refund will be entertained, and

- What the payment covers i.e. duties / levies, Tax and / or VAT.

- Where the PP is made to cover duties / levies, Tax and / or VAT pending the production of documents or to comply with some condition, the amounts of duty / levy, Tax and / or VAT must also be reflected separately.

- This information is crucial when such a PP is liquidated and the amounts must be allocated to the applicable revenue codes e.g. “Provisional Payment lodged to cover R 1567.21 duty and R 2345.50 VAT pending production of ………………. within …………… days”.

- A worksheet must be attached to the original PP where it is clearly indicated how the amounts were calculated in order to substantiate the individual amounts mentioned on the PP.

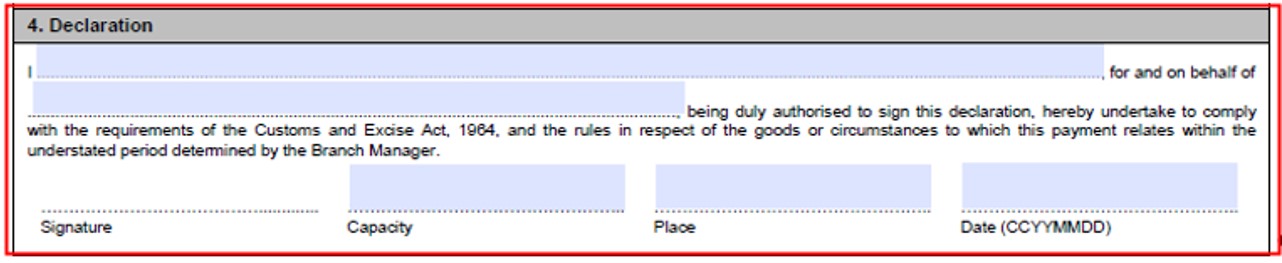

Declaration

- This portion is completed by the manufacturer / licensee / owner where a specific condition must be complied with e.g. production of documents.

- The declaration must, at all times be completed by inserting the name of the manufacturer / licensee / owner.

- The full names (John Walker) and not only initials (J. Walker) of the person who signs the declaration must be legibly inserted in this box.

- The signature of the person whose name appears in the declaration must be inserted in this box.

- The capacity of the person signing must also be indicated.

- Only the applicant may sign the indemnity.

- Where a provisional deposit is financed by a third party, for example, by a friend or by employers, care should be taken to ensure that the PP is signed by the client personally and not by the third party.

- A representative who legally represents the manufacturers / licensees / owners may however sign on behalf of their clients.

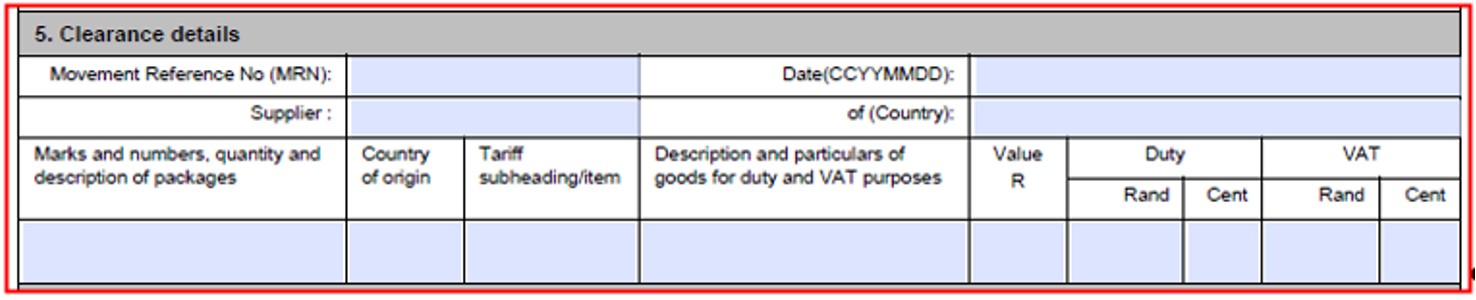

Clearance details

Enter “ Not Applicable” in the following fields

- Movement Reference No. (MRN).

- Date (CCYYMMDD).

- Supplier.

- Country.

- Marks and numbers, quantity and description of packages.

- Country of origin.

- Tariff subheading / item.

- Description and particulars of goods for duty / levy , Tax and / or VAT purposes.

- Value in rands.

- Duty / Levy and or Tax (Rand and Cent).

- VAT (Rand and Cent).

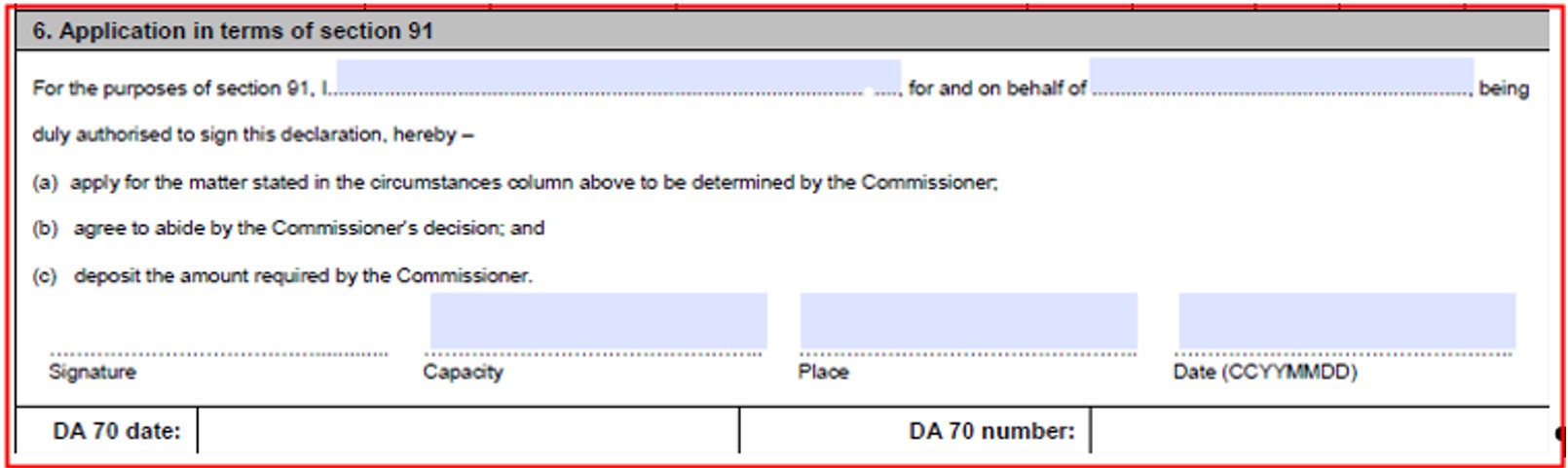

Application in terms of Section 91

- Application in terms of Section 91

- This box must only be completed if the PP is lodged to cover a deposit for a contravention and is not discussed here. If the depositor elects to be dealt with by the Commissioner in terms of Section 91, (in this case the amount of PP must be liquidated by the Excise team within thirty (30) days of accepting the PP).

- The application must, at all times be completed by inserting the name of the applicant.

- The full names (John Walker) and not only initials (J. Walker) of the person who signs the declaration, and on whose behalf he / she is acting e.g. DEF Clearing Agents must be legibly inserted in this box.

- The signature of the person whose name appears in the application must be inserted in this box.

- The capacity of the person signing must also be indicated.

- Only the applicant may sign the indemnity.

- If the depositor does not agree to sign this box because of a contravention, the deposit may not be accepted.

- In the case where an amount is called for to cover a penalty regarding VAT, a separate PP must be lodged.

- DA 70 number and date (For Official Use only)

- PPs are numbered numerically per financial year e.g. the first PP for the financial year, 1 April 2011 to 31 March 2012, will be numbered 01/2012.

- The (Customs / Excise Billing) CEB 01 case number allocated to the PP must also be endorsed on the bottom of the paper PP underneath the DA 70 number.

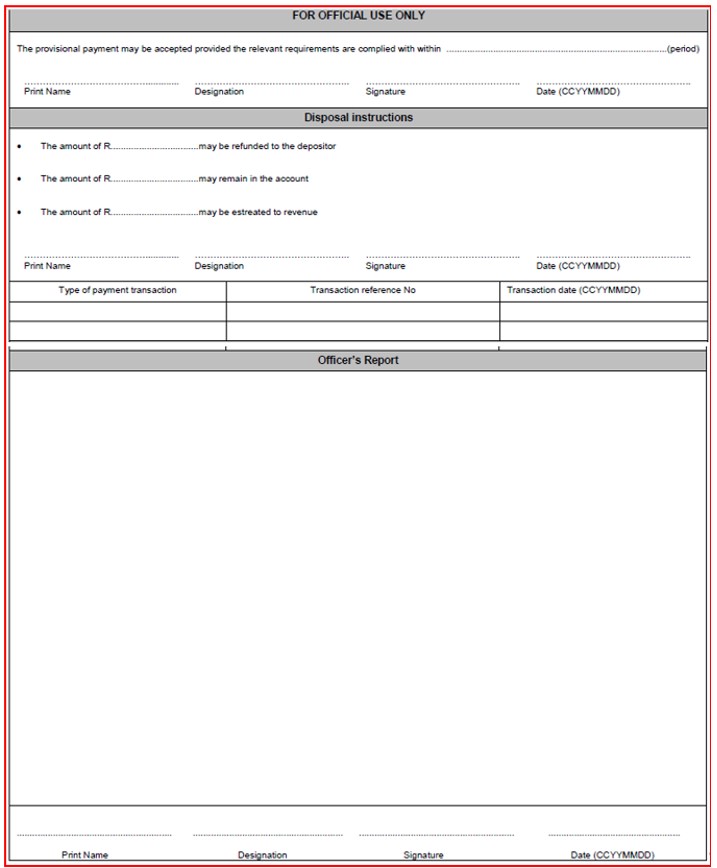

For official use only – (DA 70 – Page 2 of 2 – Reverse side)

- Acceptance by Branch Office

- This portion must be completed by the team requesting the PP or the EO if the letter issued to the client is attached.

- The period to be allowed within which the requirements of the PP are to be complied with, must also be inserted here.

- If the period is not specified on the PP, it may not be accepted. The PP must be rejected with reasons to the team.

- The EO completing the PP must print his / her name in full, insert his / her designation, sign and insert the date in the space provide e.g. Pieter Powder Excise Officer.

- Disposal Instruction

- The EO endorsing this box may not be the same officer who approved the PP e.g. Operations Manager (OPS Manager).

- The officer writing the report on the reverse side of PP [DA 70 – page two (2)] must not be the same officer completing this box.

- The officer must print his / her name in full, insert his / her designation, sign and insert the date in the space provided.

- Where the deposit should be liquidated in favour of the SARS, the team must complete the Officers report or disposal instruction on the DA 70.

- Type of payment transactions box is used:

- Only where the PP was made for unregistered clients; and

- To insert Electronic Funds Transfer (EFT) number used for refunding the money to the unregistered client.

- The EFT transaction number and date must be reflected on the PP referred to as the transaction.

Officer’s Report

- This box is completed by the officer when liquidating the PP (refer to SE-PP-01-A07).

- The Officer must print his / her name in full, insert his / her designation, sign and insert the date in the space provided.

- The report must include the reason why the PP is liquidated.

- In case of estreation, the reference number and date of the SE-PP-01-A03 must be endorsed to ensure that the PP has been approved for estreation. This must also be done on the copy of the DA 70.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.