Summary

The purpose of this webpage is to assist licensees of Manufacturing Warehouses (VM) in the Plastic Bag industry, to complete the quarterly DA 161A Environmental Levy Account for Plastic Bags and its annexures.

Plastic Bag Account Administration

Completion of the DA 161A Environmental Levy Account for Plastic Bags, Including the Electronically Submitted Excise Duty and Levy Return (EXD 01).

The Environmental levy account (DA 161A) requires the licensee (manufacturer) to declare all stock, production and removals (including removals under rebate) from the licensed VM that took place in the accounting period, which must be submitted quarterly via e-Filing.

The Environmental levy account DA 161A is the summarising document reflecting all production, stock, receipts and removals (duty paid and non – duty paid) of plastic bags subject to the levy, as well as the amount of plastic bag levy payable in respect of the accounting period.

In terms of Rule 54F.07, an accounting period shall be a fixed accounting period of three (3) months calculated from the first day of the month during which manufacturing of plastic bags subject to the levy commences, until the last day of the month on which such period ends.

The environmental levy account must be completed in full, i.e. the DA 161A with all the supporting schedules, if applicable, for that specific accounting period and a duly signed and dated copy for record and audit verification must be kept.

In order to make it administratively easier to do business with the South African Revenue Service (SARS), the DA 161A (the EXD 01 return must be utilized for this purpose which is the electronic version of the DA 161A) must be submitted i.e.:

- Electronically to the SARS Excise via the e-Filing platform; or

- Hand delivered for capturing should the client experience problems with eFiling.

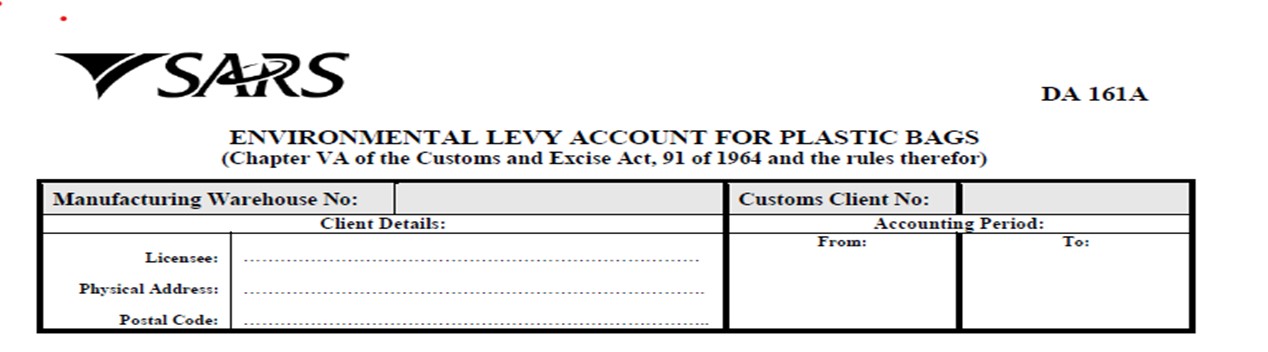

DA 161A– Environmental Levy Account for Plastic Bags

- The plastic carrier and flat bags under reference here are those bags mentioned under the tariff sub-headings reflected in the below paragraph Tariff Subheading / Item – The tariff sub-heading code as reflected in Part 1 and 3A of Schedule 1 must be inserted in this box only

- Manufacturing Warehouse No – This box is for the VM number.

- Customs client No – This box is for the client’s code number.

- Client Details – The name under which the VM is licensed must be inserted in this box.

- Physical Address / Postal Code – The street name, number, suburb, city and postal code of the VM must be inserted in these boxes.

Accounting Period From / To –

The opening and closing dates of an account must be shown.

The opening date of an account must follow immediately on the closing date of the previous account

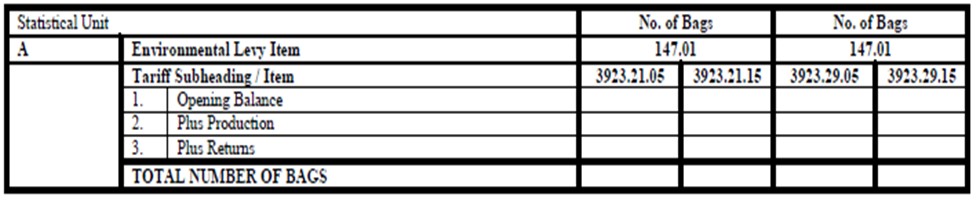

Explanation of Section A: (Must be reflected as number of bags)

Explanation of Section A: (Must be reflected as number of bags)

- Environmental Levy Item – The levy item code as reflected in Part 3A of Schedule 1 must be inserted in this box.

- Tariff Subheading / Item – The tariff sub-heading code as reflected in Part 1 and 3A of Schedule 1 must be inserted in this box.

- Opening Balance – Balance carried forward from previous period must be inserted in this box.

- Plus Production – Production during the three (3) months of the accounting period must be inserted in this box.

- Plus Returns –

- Returns from the local market for which credit notes have been issued must be inserted in this box.

- In the case of returns from Botswana, Eswatini, Lesotho, and Namibia (BELN countries), the Environmental levy thereon must have been paid on entry into South Africa (SA).

- Total number of bags – The total number of bags must be inserted in the relevant box(s).

Explanation of Section B: Less Sales, Removals and Rebates

- Sales: Republic – The quantity of plastic bags subject to the levy removed or sold must be inserted in this box.

- Sales: BELN countries – The quantity of plastic bags subject to the levy removed or sold to the BELN countries must be inserted in this box.

- Exports – The quantity of plastic bags subject to the levy exported (Rule 54F.03).

- Storage Warehouse – The quantity of plastic bags subject to the levy removed to a Special Storage Warehouse (SOS) – Rule 54F.03.

- Rebates –

- Item 680.01 – Goods supplied under rebate of duty as specified in the item.

- Item 680.02 – Goods lost or destroyed in the warehouse in circumstances of Vis major, etc.

- Item 680.03 – Goods manufactured in the licensed warehouse used for reprocessing of Environmental levy goods or the manufacture of other goods.

- Total – The total number of bags for section B must be inserted in the relevant box(s).

- A minus B: Closing Balance – The quantity of plastic bags subject to the levy on hand at the end of the accounting period must be inserted in this box.

Explanation of Section C

- Levy On Dutiable Total – The total of sales to the local market and to consignees in BELN countries must be multiplied by the rate of levy and inserted in this box. The rate is specified in Part 3A of Schedule 1.

Explanation of Section D

- Less Levy Paid or Payable – The levy paid on goods may be set-off under the following Rebate Items:

- Item 681.01- Removed to BLNS countries (only if proof of exit from South Africa has been obtained).

- Item 681.02 – Returns for re-cycling (goods off specification or otherwise defective) – credit notes must have been issued.

- Item 681.03 – Returns from purchasers to the local market for any purpose other than recycling – credit notes must have been issued and retained as proof.

- Total – The total of paragraph (j)(i)(A), (B) and / or (C) above, must be inserted in the relevant box(s).

- Less: Overpaid On Previous Account

- Should a licensee have overpaid on levy on the previous account, the amount so overpaid must be inserted in this box.

- A copy of the relevant account as well as an explanation of the overpayment must be attached to the new account.

- Plus: Underpaid On Previous Account

- Should a licensee have underpaid on levy on the previous account, the amount so underpaid must be inserted in this box.

- A copy of the relevant account as well as an explanation of the underpayment must be attached to the new account.

Explanation of Section E

- Nett Levy Payable – (Section C minus Section D minus less overpaid on previous account plus underpaid on previous account). The amount determined between the “levy payable” and the “over” or “underpaid”, whichever is applicable, must be inserted in this box.

Explanation of Section F

- Total amount of nett levy due – The total amount of nett levy which is the sum of the amounts reflected under items 147.01 / 3923.21.07, 3923.21.17 and 147.01 / 3923.29.40 and 3923.29.50 must be inserted in this box.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.