Summary

The webpage provides detailed instructions and clarifies requirements for completing the quarterly Ad valorem Excise duty account (DA 75) and its schedules:

- DA 75 Quarterly Ad Valorem Excise Duty Account;

- DA 75.20 Schedules of Excisable goods removed under rebate of duty in terms of items of Schedule 6 Part (including exports);

- DA 75.22 Schedule of Excisable goods removed in bond or for re-warehousing in terms of Section 18;

- DA 75.24 – Schedule of goods in respect of which duty has already been paid in terms of Rebate Items 534.00 or 632.02, respectively, of Schedules 5 and 6 (in order to prevent double taxation);

- DA 75.30 – Statement i.r.o. over and / or underpayments on previous account(s) i.t.o. Section 77;

- DA 75.32 – Schedule in respect of ordinary levy on Excisable goods supplied to any body, authority, institution or person specified in item 196.10 (ordinary levy) of Part 8 of Schedule 1; and

- DA 75.33 – Schedule of Ad valorem Excise duty in respect of motor vehicles manufactured and removed from licensed premises.

The webpage states the platform to use for submitting the quarterly Ad valorem Excise duty account (DA 75) and its schedules.

Completion of the DA 75 Quarterly AD Valorem Excise Duty Account and Annexures

- The completion of the DA 75 quarterly ad valorem excise duty account and annexures includes the electronically submitted excise duty and levy return (EXD 075).

- The Ad valorem Excise duty account (DA 75) is the summarising document reflecting all activities within the licensed Customs and Excise warehouse for Ad Valorem Excise purposes, including the movements of goods into and out of the warehouse, losses within the warehouse and sales information, as well as the amount of ad valorem Excise duty payable, in respect of all goods during the period, being accounted for i.e. quarterly.

- In order to make it administratively easier to do business with the South African Revenue Service (SARS), the DA 75 account must be submitted electronically to the SARS Excise via the e-Filing platform. The EXD 075 return must be utilised for this purpose which is the electronic version of the DA 75.

- The Ad valorem Excise duty account must be completed in full; i.e. the DA 75 with all the applicable schedules attached for that specific accounting period and kept for record and audit verification purposes. That is, the EXD 075 return must be completed via the e-Filing platform and submitted electronically quarterly. The DA 75 and its Schedules must be completed as required and retained by the licensee for audit verification purposes. It need not be submitted to the SARS, but must be available for verification when requested.

- If any column is not required for completion for that specific accounting period, the column must be crossed out by drawing a diagonal line across the face thereof, starting from the top left corner of the first box to the bottom right corner of the last box and writing Not Applicable “N / A” in the middle thereof.

- If there is no figure to be declared for a specific box in a column applicable for that specific accounting period, it must be indicated by declaring “0.00” in that box.

- If any schedule is not required for that specific accounting period, the applicable schedule does not have to be completed.

- Each schedule to the Ad valorem Excise duty account also serves as a continuation sheet for that specific schedule.

- Licensees may however elect to compile a schedule of receipts / removals, approved by the local Controller / Branch Manager, listing all the relevant receipts / removals and supporting documents pertaining to the specific schedule and attach that schedule of receipts / removals to the applicable schedule. In this case, only the total of the schedule of receipts / removals must be reflected in the appropriate box on the prescribed schedule.

- Excise Officers are not allowed to complete information on behalf of clients.

DA 75 Ad valorem Excise duty account

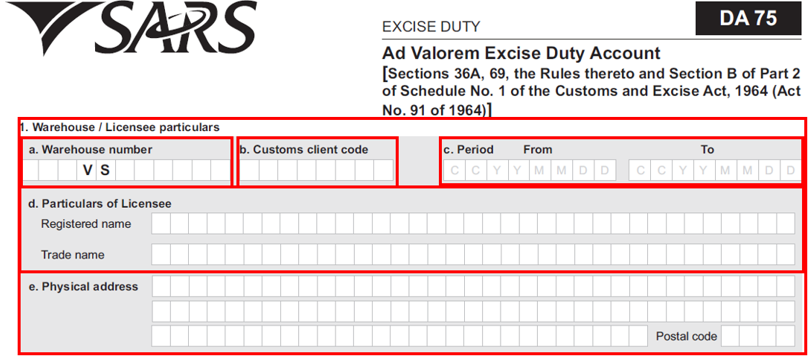

Warehouse / Licensee particulars:

- Warehouse number – The allocated warehouse number must be inserted here as shown in the following example:

| P | T | A | V | S | 3 | 2 | 1 | 0 |

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To).

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of an account must follow immediately on / after the closing date of the previous account.

- Particulars of Licensee.

- Registered Name – This must be the registered name under which the licensee is to manufacture or deal with Excisable goods.

- Trade Name – If trading under a different name then the registered name must be inserted here. This is compulsory.

- Physical address.

- This must be the address where the actual manufacturing / storage is taking place.

- The warehouse number is of vital importance for identification purposes and licensees must therefore ensure that the correct number is furnished.

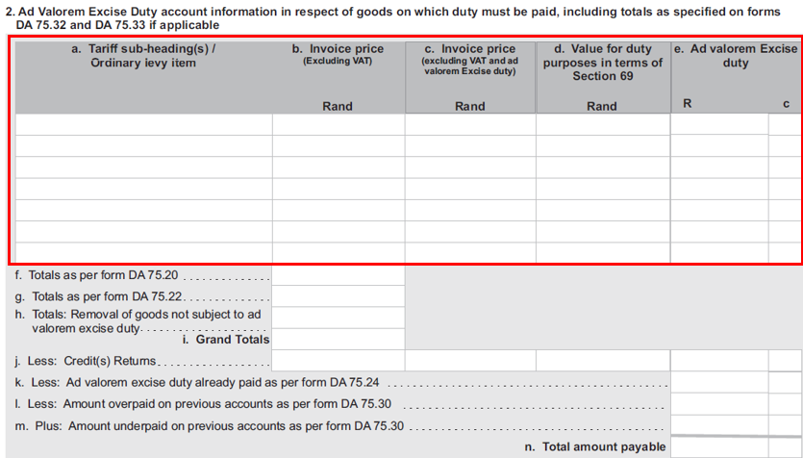

Ad valorem Excise duty account information in respect of goods on which duty must be paid, including totals as specified on DA 75.32 and DA 75.33, if applicable:

This section must reflect particulars of the Excisable goods in respect of which Ad valorem Excise duty must be brought to account.

Goods residing under different tariff sub-headings must be shown separately and goods residing under the same tariff sub-heading but subject to different rates of Ad valorem Excise duty must also be shown separately.

If a licensee manufactures or handles Excisable goods classifiable under more tariff sub-headings than there are lines provided for, a separate DA 75 must be completed.

Ad Valorem Excise duty account information in respect of goods on which duty must be paid, including totals as specified on DA 75.32 and DA 75.33, if applicable, must also be inserted on the DA 75.

Tariff sub-heading(s) / Ordinary levy item:

- The tariff sub-headings and / or ordinary levy Item to be inserted are those under which the Excisable goods are classifiable in terms of Section B of Part 2 and / or Part 8 of Schedule 1, e.g. 3304.99.90, 8415.10.10 and / or Item 196.10.

- Manufacturers / handlers of Excisable goods must be licensed with the SARS in respect of the tariff sub-headings reflected on Ad valorem Excise duty accounts.

- If a licensee manufactures/handles or intends to manufacture / handle Excisable goods classifiable under a tariff sub-heading in respect of which he / she is not licensed, immediate application must be made to the Controller / Branch Manager for an extension of his / her license.

- If a manufacturer ceases to manufacture goods classifiable under a certain tariff sub-heading for which he is licensed; the Controller / Branch Manager must also be advised immediately.

Invoice price [excluding Value-Added Tax (VAT)]:

- The total of the actual prices charged on the invoice(s) covering the removal of Excisable goods must be reflected against each tariff sub-heading.

- VAT, however, does not form part of the dutiable price and must not be included.

Invoice price (Excluding VAT and Ad valorem Excise duty):

- The total of the actual prices charged on the invoice(s) covering the removal of Excisable goods must be reflected against each tariff sub-heading.

- VAT and Ad valorem Excise duty, however, do not form part of the dutiable price and must not be included.

- The wording in this column does not mean that VAT can be deducted again, but merely refer to the VAT already excluded in 2b where-after Ad valorem Excise duty will be excluded, before completing 2c.

Value for duty purposes less deduction in terms of Section 69 – This column must reflect the total value for duty purposes less the deduction specified in Rule 69.01, if applicable.

Ad valorem Excise duty – The Ad valorem Excise duty reflected must be calculated by applying the rate of duty as prescribed in Section B of Part 2 of Schedule 1.

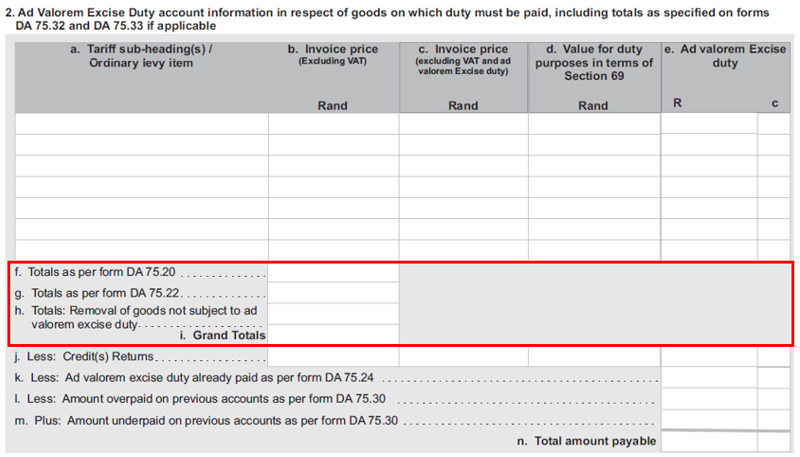

Totals as per DA 75.20 – The amount to be inserted in 2b on the DA 75 is the total of 2h appearing on the DA 75.20 [Schedule of Excisable goods removed under rebate of duty in terms of Schedule 6 (including exports)].

Totals as per DA 75.22 (In Bond) – The amount to be inserted in 2b on the DA 75 is the total of 2c appearing on the DA 75.22 (Schedule of Excisable goods removed in bond in terms of Section 18).

Totals: Removal of goods not subject to Ad valorem Excise duty:

- The total invoice price of all goods which do not attract Ad valorem Excise duty and which have not already been included in 2f and g must be reflected in 2b on the DA 75.

- If all the goods removed by a licensee during the accounting period are subject to Ad valorem Excise duty, the word “Nil” must be written in 2b which must then be reflected against 2h on the DA 75.

- If all the goods removed during the accounting period were not subject to Ad valorem Excise duty, an account must nevertheless be completed.

Grand Totals:

- The amount to be inserted is the sum of the amount(s) indicated in 2b and which is indicated against 2f, g and h and represents the total invoice price of ALL goods removed or used by the licensee during the accounting period.

- This total is exclusive of VAT and Ad valorem Excise duty.

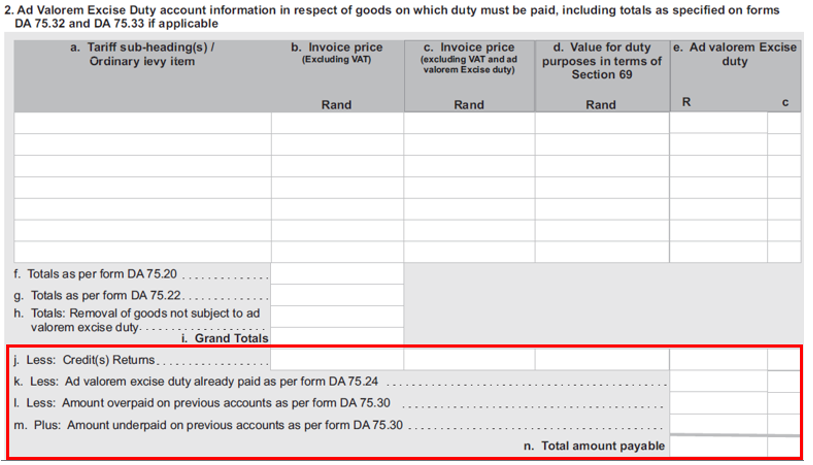

Less: Credit(s) Returns:

- Credit Notes – Goods returned to stock in respect of which credit notes were issued must be reflected against 2j on the DA 75.

- This number must be read with columns 2b, c, d, and e on the DA 75. The credit(s) / returns must reflect the relevant invoice number(s) and must be kept with the duty account for cross-reference purposes.

- Should the relevant invoice number(s) not be reflected on the credit note, such deductions will not be allowed.

Less: Ad valorem Excise duty already paid as per DA 75.24 – The amount to be inserted is the total amount (refer to 2h) appearing on the DA 75.24 (Schedule of goods in respect of which duty has already been paid in terms of Rebate Items 534.00 / 632.02).

Less: Amount overpaid on previous duty account(s) as per DA 75.30 – The amount to be inserted is the total amount overpaid (refer to 2c) against 2e on the DA 75.30 (Statement in respect of over/underpayments on previous duty accounts in terms of Section 77).

Plus: Amount underpaid on previous account(s) as per DA 75.30 – The amount to be inserted is the total amount underpaid (refer to 2d) against 2e on the DA 75.30 (Statement in respect of over / underpayments on previous duty accounts in terms of Section 77).

Total amount payable:

- This is the sub total(s) declared in 2e, less 2j, less 2k, less 2l plus 2m if applicable.

- This is the amount to be paid by the licensee by means of e-Filing.

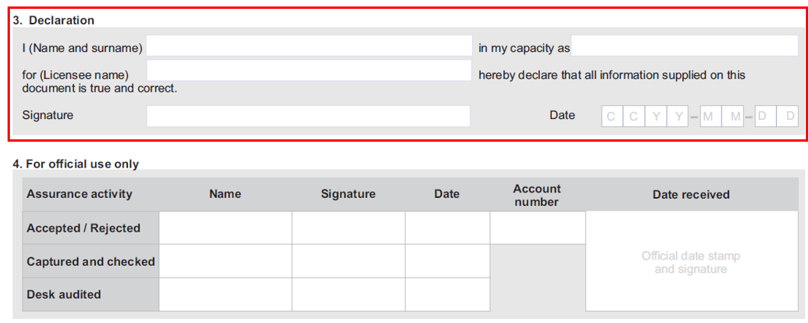

Declaration:

Interest on late payment / underpayments is no longer accounted for on the DA 75.

Although the DA 75 does not make provision for invoice serial numbers for accounting periods, a separate list of all serial numbers of invoices for the applicable accounting period must be attached to the DA 75.

Failure to adhere to the provisions of the Act is considered an offence and may render the client liable to monetary penalties.

The Licensee completes the fields under Declaration:

- I (Name and surname) – The name and surname of the person completing the form;

- In my capacity as – The capacity in which the person is declaring;

- For (Licensee name) –The name of the Licensee;

- Signature – The signature of the person completing the form; and

- Date – The date must be century, year, month and day i e 2020-05-18.

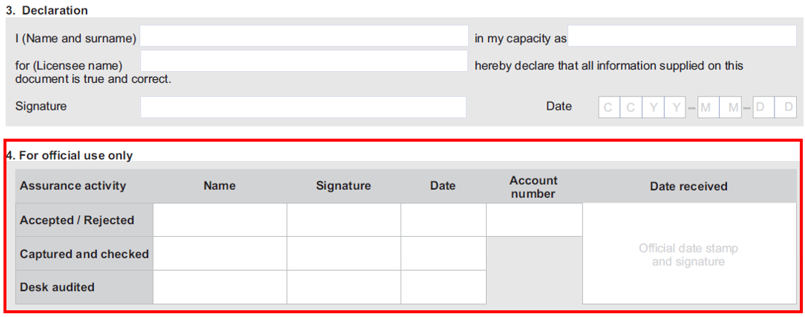

For Official Use Only

The SARS Officials complete the For official use only section upon the receipt.

The Excise Officers performed the below tasks must complete the fields:

- The Accepted / Rejected:

- Name – The name of the Excise Officer accepted or rejected the Ad valorem Duty Account;

- Signature – The signature of the Excise Officer accepted or rejected Ad valorem Duty Account;

- Date – The date must be century, year, month and day i e 2020-05-18; and

- Account Number.

- Captured and checked:

- Name – The name of the Excise Officer captured the Ad valorem Duty Account;

- Signature – The name of the Excise Officer captured the Ad valorem Duty Account; and

- Date – The date must be century, year, month and day i e 2020-05-18.

- Desk audited:

- Name – The name of the Excise Officer audited the Ad valorem Duty Account;

- Signature – The name of the Excise Officer audited the Ad valorem Duty Account; and

- Date – The date must be century, year, month and day i e 2020-05-18.

- Date received:

- The date Ad valorem Duty Account form received must be endorsed by the Official Date stamp; and

- It must be signed.

DA 75.20 – Schedule of Excisable goods removed under rebate of duty in terms of items of Schedule 6 Part 2 (including exports)

- Part 2 of Schedule 6 provides, for a rebate of Ad valorem Excise duty in respect of Excisable goods received as original equipment, Excisable goods destroyed and Excisable goods exported in terms of and in compliance with the provisions of the relevant Rebate Items.

- This form relates to the final products supplied / removed by the licensee under rebate of Excise duty and must not be confused with the DA 75.24.

- Full Ad valorem Excise duty is payable on goods removed on lease or on loan and such goods must not be entered on this form (refer to item 2 on the DA 75).

- Goods removed in bond must be entered on the DA 75.22.

- The Ad valorem Excise duty on Excisable goods exported is rebated in terms of Rebate Item 633.01. Removals into the Southern African Customs Union (SACU) i.e. the Republic of South Africa, the Republic of Botswana, the Kingdom of Lesotho, the Republic of Namibia and the Kingdom of Swaziland are not regarded as exports for ad valorem excise duty purposes and the full Ad valorem Excise duty must be brought to account on any such removals (refer to item 2 on the DA 75).

- Removals to organisations, bodies, etc. in these countries, which, are entitled to obtain goods under rebate of Excise duty, must, however, be reflected on this form.

- Copies of the invoice(s) covering Excisable goods supplied under rebate of duty or detailed schedules of such invoice(s) must be attached to the DA 75.20.

- When Excisable goods are exported under rebate of duty in terms of Rebate Item 633.01, a copy of the relevant clearance declaration (CD) must be attached to the DA 75.20 and retained with the schedule and presented upon request from the SARS.

- The invoice price as declared on the CD is the value that must be used for the purposes of the DA 75.20.

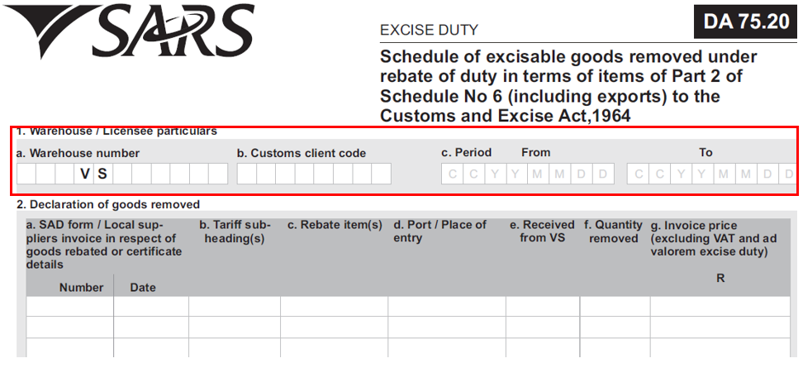

Warehouse / Licensee particulars.

The client completes the fields:

- Warehouse number – The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of an account must follow immediately on / after the closing date of the previous duty account.

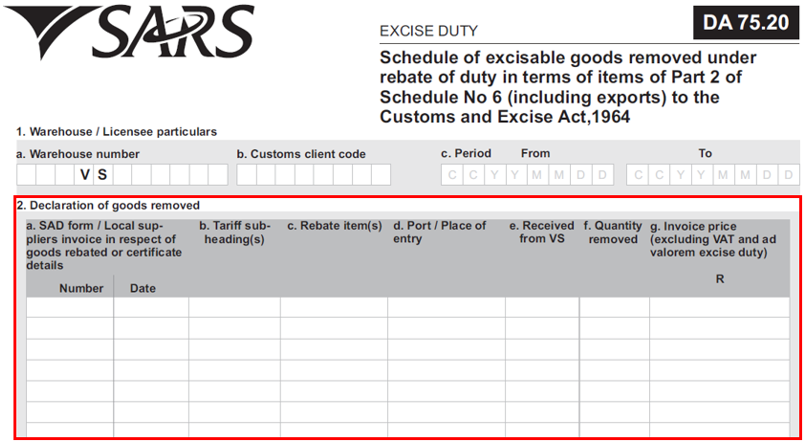

Declaration of goods removed.

CD / local suppliers invoice in respect of goods rebated or certificate details – The number and date to be inserted of the CD / local suppliers invoice in respect of goods rebated relating to the goods removed or destruction certificate (P 2.08).

Tariff sub-heading(s):

- The tariff sub-heading to be inserted is that which applies to the final Excisable goods received as original equipment, Excisable goods removed from and/or destroyed at the licensee’s premises.

- In respect of every combination of tariff sub-heading and Rebate Item only one (1) entry must be made on the DA 75.20.

Rebate Item(s) – The Rebate Item(s) is the item(s) in Part 2 of Schedule 6 in terms of which the relative Excisable goods may be received as original equipment / products, removed from and / or destroyed at the licensee’s premises without payment of the full Ad valorem Excise duty.

Port / Place of entry – The Port / Place of entry is compulsory and must be inserted in this information box.

Received from VS – The allocated VS number from where the original equipment / products are received from must be inserted here.

Quantity Removed – The quantity of Excisable goods received as original equipment / products from other VS’s, removed from and/or destroyed, is to be reflected here.

Invoice price (excluding VAT and Ad valorem Excise duty):

- The total of the actual prices charged on the invoice(s) covering the rebated Excisable goods must be reflected against each tariff sub-heading.

- VAT and Ad valorem Excise duty, however, does not form part of the dutiable price and must not be included.

Total – The total of 2h must be carried forward to the DA 75 and reflected against 2f (this total must be carried over to the EXD 075 against totals as per DA 75.20).

Note: If space is insufficient, attach additional pages.

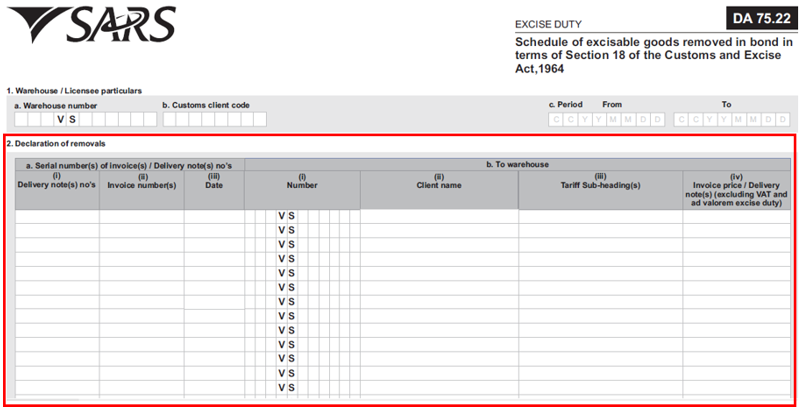

DA 75.22 – Schedule of Excisable goods removed in bond or for re-warehousing in terms of Section 18

General.

- Excisable goods may be removed with deferment of payment of the Ad valorem Excise duty from one (1) licensed special Customs and Excise warehouse for Ad valorem purposes to another such warehouse only (removal in bond). Particulars of removals must be entered on the DA 75.22.

- Removals in bond as detailed above must be effected under cover of invoice(s) and/or delivery note(s) (removal of Excisable / specified goods ex warehouse).

- Removals to Duty Free Shops, foreign going ships or aircraft, must also be effected on this form.

- Copies of the relevant invoice(s) and / or delivery note(s) must accompany the DA 75.22, or must be retained by the licensee for inspection / audit purposes by the SARS.

Warehouse / Licensee particulars:

- Warehouse number – The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of a duty account must follow immediately on / after the closing date of the previous duty account.

Declaration of removals:

Serial number(s) of invoice(s) / delivery note(s) numbers – The serial number(s) of the relevant invoice(s)/delivery note(s) must be reflected:

- Delivery note(s) no’s;

- Invoice number(s); and

- Date.

To warehouse – The following information must be reflected:

- Number: VS Number of company / licensee to which goods are being removed;

- Client name: Registered name of the licensee;

- Tariff sub-headings; and

- Invoice price / delivery note(s) (excluding VAT and Ad valorem Excise duty).

Total – The total of 2c must be carried forward to the DA 75 and reflected against item 2g (this total must be carried over to the EXD 075 against totals as per DA 75.22).

Note: If space is insufficient, attach additional pages.

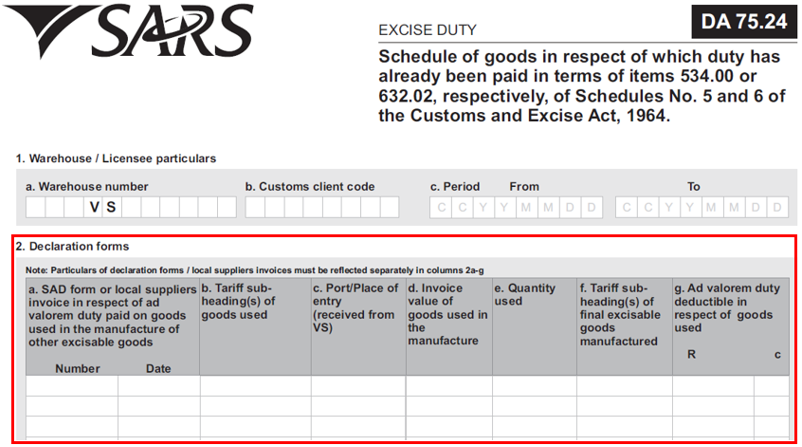

DA 75.24 – Schedule of goods in respect of which duty has already been paid in terms of Rebate Items 534.00 or 632.02, respectively, of Schedules 5 and 6 (in order to prevent double taxation)

General:

Rebate Items 534.00 (imported sourced goods) and 632.02 (domestically sourced goods) allows for Excisable goods on which Excise duty has been paid and which has been incorporated in unused condition, in any other Excisable goods manufactured in any special Customs and Excise warehouse to be subjected to a full rebate of duty.

Where such rebates are claimed, the onus vests with the claimant to present proof of such prior payment to the SARS upon request.

Goods for the licensee’s own use and damaged or returned goods must not be included in this form.

Warehouse / Licensee particulars:

- Warehouse number – The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of a duty account must follow immediately on / after the closing date of the previous duty account.

Declarations

CD or local suppliers invoice i.r.o. Ad valorem Excise duty paid on goods used in the manufacture of other Excisable goods.

- The number(s) and date(s) of the local supplier’s invoice or, in the case of imported goods, the CD number(s) and date of the relevant CD must be inserted against each separate pair of tariff sub-headings (i.e. of goods used and of goods manufactured).

- Copies of the relevant supplier’s invoice(s) / CD, of which the numbers and dates appear on this duty schedule, must be attached to this duty schedule or retained for audit verification by the SARS.

Tariff sub-heading(s) of goods used – The tariff sub-heading(s) of the goods on which Ad valorem Excise duty was paid and which were used as components or ingredients in the manufacture of other Excisable goods must be reflected against the tariff sub-heading(s) of each separate Ad valorem Excisable goods manufactured.

Port / Place of entry (received from VS) – The Port / Place of entry where the goods entered South Africa (SA) or VS number where components or ingredients were received from, is compulsory and must be inserted in this box.

Invoice value of goods used in the manufacture – The total of the Ad valorem Excise duty paid must be reflected. VAT, however, does not form part of the dutiable value and must not be included.

Quantity used – The quantity of goods imported or locally purchased and which is used in the manufacture must be reflected e.g. Litres or numbers of units.

Tariff sub-heading(s) of Excisable manufactured goods – The tariff sub-heading(s) of the Excisable goods manufactured, which incorporate other goods of 2b, in respect of which Ad valorem Excise duty has been paid, must be reflected separately against the tariff sub-heading(s) of the goods so incorporated.

Ad valorem Excise duty deductible i.r.o. goods used – The duty, which may be claimed as a refund, may not exceed the duty payable per quarter for Ad valorem Excise duty purposes.

Total – The total of 2h must be carried forward to the DA 75 and reflected against item 2k (this total must be carried over to the EXD 075 against totals as per DA 75.24).

Note: If space is insufficient, attach additional pages.

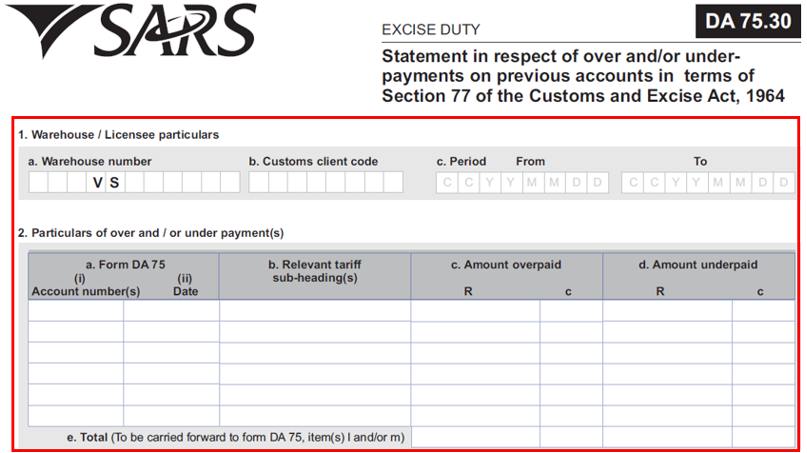

DA 75.30 – Statement i.r.o. over and / or underpayments on previous account(s) i.t.o. Section 77.

General:

When it is necessary to adjust the Ad valorem Excise duty paid on a previous account(s) because of errors or omissions resulting in overpayments and / or underpayments, the particulars of the duty account(s) being adjusted, the extent of the adjustment(s) and the reason therefore must be reflected on the DA 75.30.

This is permitted in terms of Section 77, with the compliance of the conditions stated therein. It is hence important for licensees to be familiar with this legislation when completing this form.

In terms of Section 77, the licensee may set-off the Ad valorem Excise duty he / she has paid on importation against Ad valorem Excise duty due, provided that such goods have been incorporated, in unused condition, in any Ad valorem Excisable goods manufactured in any special Customs and Excise warehouse.

When setting of Ad valorem Excise duty note must be taken of the following:

- The amount of the refund claim does not exceed the Ad valorem Excise duty payable per quarter for Ad valorem Excise duty purposes and the amount of the refund claim on a particular account against a specific tariff sub-heading does not exceed the amount of Ad valorem Excise duty payable in respect of that tariff sub-heading on the same account;

- A period of not more than two (2) years has expired since the payment of the Ad valorem Excise duty.

- The client may not set-off Ad valorem Excise duties paid on completed imported goods against locally manufactured goods.

- The client may not set-off ordinary Customs duty on goods; used in the manufacture of Ad valorem Excise duty goods.

- A refund is only claimed in respect of the duty paid on goods actually used in the manufacture of other Excisable goods.

Warehouse / Licensee particulars.

- Warehouse number- The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of a duty account must follow immediately on / after the closing date of the previous duty account.

Particulars of over and / or underpayment(s):

The duty account number(s)/ Financial Account Number(s) as per the EXD 075 and date(s) as allocated by the office of the Controller / Branch Manager must be inserted in 2a(i) and / or (ii):

- Account number(s); and

- Date.

Adjustments in respect of individual accounts must be shown separately.

Relevant tariff sub-heading(s):

- The tariff sub-heading(s), applicable to the goods in respect of which the adjustment is being made, must be inserted in this column.

- The particulars of each tariff sub-heading(s) must be shown separately.

Amount overpaid – The Ad valorem Excise duty overpaid on previous duty account(s) must be reflected in 2c.

Amount underpaid – The Ad valorem Excise duty underpaid on previous duty account(s) must be reflected in 2d.

Total – The total(s) of Ad valorem Excise duty over and / or underpaid on previous account(s) must be carried forward to ‘l’ and / or ‘m’ on DA 75 (this total must be carried over to the EXD 075 under totals as reflected on the DA 75.30).

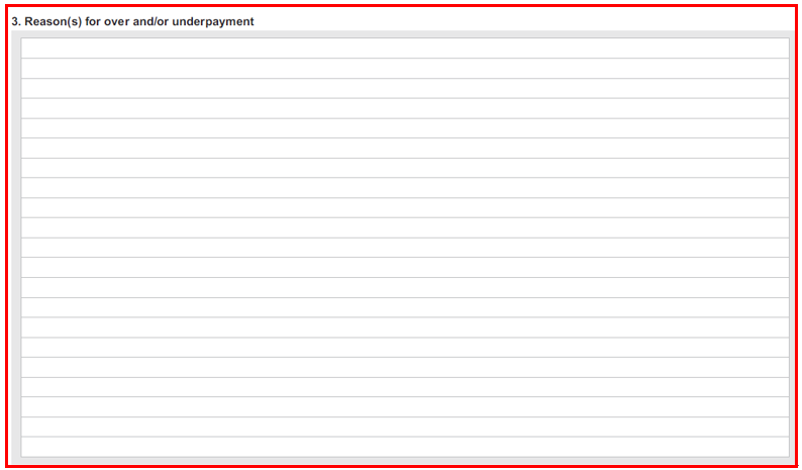

Reason(s) for over and / or underpayment.

- A full explanation must be given for every adjustment effected.

- Explanations must, where necessary, be supported by documentary evidence.

- Any documentary evidence substantiating any claim in this regard must be retained by the licensee for audit purposes by SARS

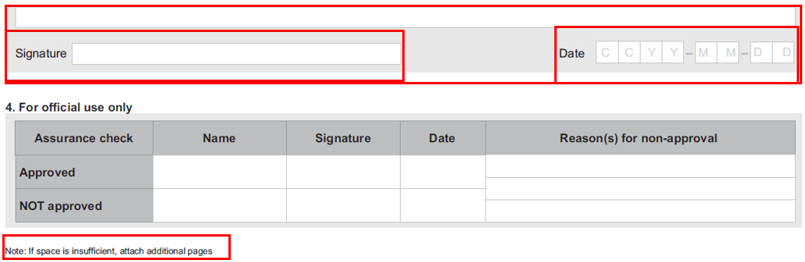

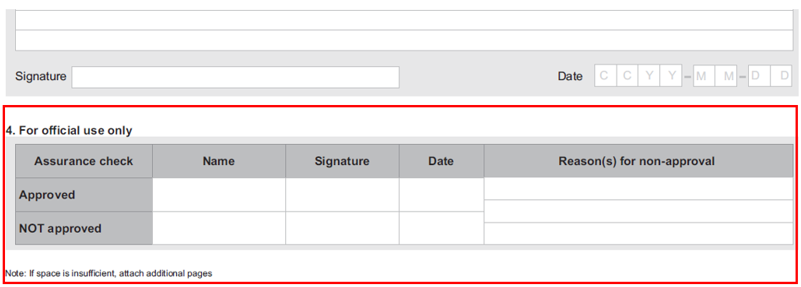

- Signature – The licencee must append their signature sign in the relevant field.

- Date – The licencee must insert the date starting with century, year, month and day i e 2020-05-18.

- Note: If space is insufficient, attach additional pages.

For official use only

The SARS Officials complete the For official use only section upon the receipt.

The Excise Officers performed the below tasks must complete the fields:

- Approved:

- Name – The name of the Excise Officer approved the Ad valorem Duty Account;

- Signature – The signature of the Excise Officer approved the Ad valorem Duty Account;

- Date – The date must be century, year, month and day i e 2020-05-18.

- NOT Approved:

- Name – The name of the Excise Officer different from the one who did not approve the Ad valorem Duty Account;

- Signature – The name of the Excise Officer who did not approve Ad valorem Duty Account; and

- Date – The date must be century, year, month and day i e 2020-05-18; and

- Reason(s) for non-approval – if the account is not approved, the Excise Officer must insert the reasons for non-approval.

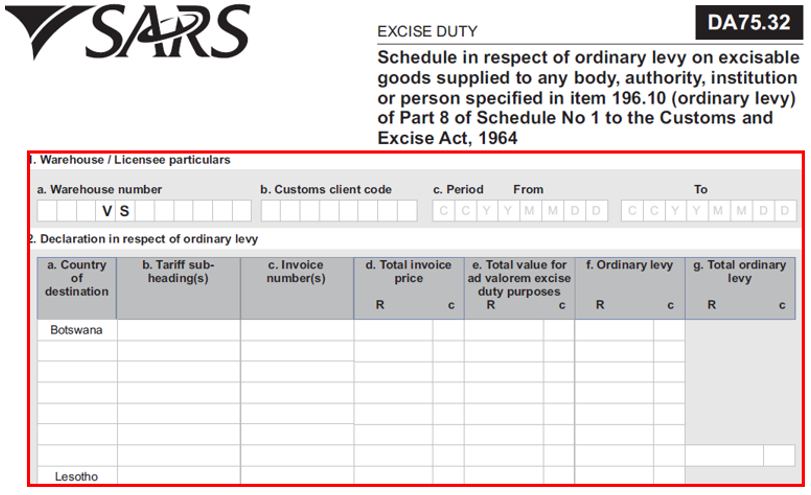

DA 75.32 – Schedule in respect of ordinary levy on Excisable goods supplied to any body, authority, institution or person specified in item 196.10 (ordinary levy) of Part 8 of Schedule 1.

General:

- In terms of Schedule 1, Part 8, an ordinary levy shall be levied on any item listed in this part and shall apply to any such goods which are manufactured in or imported into SACU and entered for home consumption by any body, authority, institution or person specified in such ordinary levy item.

- Ordinary Levy Item 196.10 is applicable to Ad valorem licensees. The description of said item is as follows: “Goods of any description, for the exclusive use by any department in the national or provincial sphere of government”. The rate of duty for such item is as follows: “The rate of duty specified of those goods in Parts 1 and 2 of Schedule 1.”

- The above means, in practical terms, that the rate of duty for the goods as described above will be that as noted in Schedule 1, Part 2B.

- All goods falling under Schedule 1, Part 8, must however be reflected as ordinary levy goods, and the applicable information boxes per EXD 075 / DA 75 must be used.

Warehouse / Licensee particulars:

- Warehouse number – The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of a duty account must follow immediately on / after the closing date of the previous duty account.

Declaration in respect of ordinary levy:

Country of destination – Removals under each tariff sub – heading must be grouped together under each country of destination as specified on the Schedule.

Tariff sub-heading(s) – Insert Schedule 1 Part 2B tariff sub-heading(s), 3304.10, 8518.40, etc.

Invoice number(s):

- Insert invoice number(s).

- Should the space provided prove insufficient, a separate sheet may be attached.

Total invoice price – Insert total invoice price for each tariff sub-heading per country of destination.

Total value for Ad valorem Excise duty purposes – Insert total value for Ad valorem Excise duty purposes for each tariff sub-heading(s) per country of destination.

Ordinary levy – Insert Ordinary levy payable for each tariff sub-heading(s) per country of destination. The value for Ad valorem Excise purposes and the ordinary levy due are calculated on the same basis as the value under schedule 1 Part 2B.

Total Ordinary levy – Insert total ordinary levy payable for each country of destination.

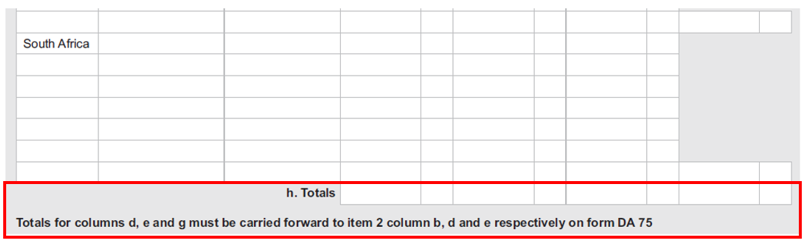

Totals – The total(s) of 2d, e and g must be carried forward to 2b, d and e respectively on the DA 75 (this total must be carried over to the EXD 075).

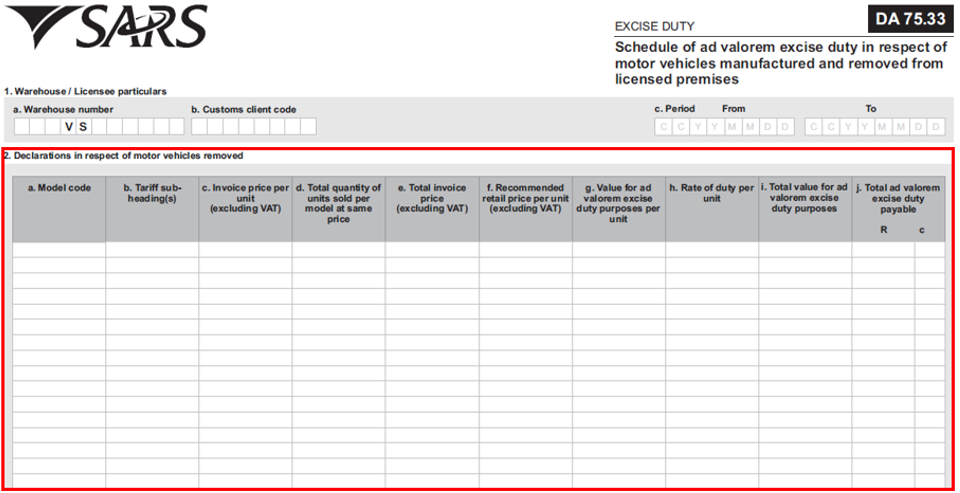

DA 75.33 – Schedule of Ad valorem Excise duty in respect of motor vehicles manufactured and removed from licensed premises.

Warehouse / Licensee particulars.

- Warehouse number – The allocated warehouse number must be inserted here.

- Customs Client Code – The allocated Customs / Excise client code must be inserted here.

- Period (From – To):

- The opening and closing dates of the applicable accounting period / quarter must be inserted here.

- The opening date of a duty account must follow immediately on / after the closing date of the previous duty account.

Declarations in respect of motor vehicles removed

- Model code – Insert model code of vehicle.

- Tariff sub-heading(s) – Insert tariff sub-heading(s).

- Invoice price per unit (excluding VAT) – Insert invoice price per unit (excluding VAT).

- Total quantity of units sold per model at the same price – Insert total quantity of units sold per model at the same price.

- Total invoice price (excluding VAT) – Insert total invoice price for each tariff sub-heading(s).

- Recommended Retail Price (RRP) per unit (excluding VAT):

- Insert RRP per unit (excluding VAT).

- The RRP excludes the environmental levies in terms of rules 54FB.01 and 54FC.01 respectively when declaring the Ad valorem Excise duty.

- Value for Ad valorem Excise Duty purposes per unit – Insert value for Ad valorem Excise duty purposes per unit.

- Rate of duty per unit – Insert rate of duty per unit.

- Total value for Ad valorem Excise duty purposes – Insert total value for Ad valorem Excise duty purposes.

- Total Ad valorem Excise duty payable – Insert total Ad valorem Excise duty payable.

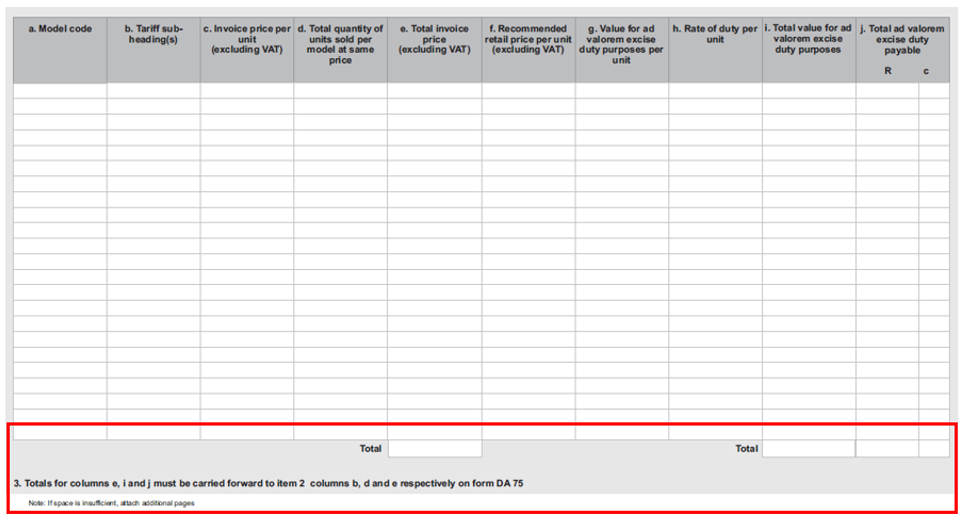

- Totals – The total(s) of 2e, i and j must be carried forward to 2b, d and e respectively on the DA 75 (this total must be carried over to the EXD 01 against totals as per DA 75.33).

Completion of the Comma-Separated Values (CSV) file

- The CSV file electronically completed and submitted through the e-Filing platform as part of the quarterly account for Ad valorem Excise duty applies only to the motor industry.

- The CSV file is an exact replica of the DA 75.33, hence must be completed in the same manner.

- The relevant totals as per the CSV file will automatically populate the corresponding totals of the EXD 075 as soon as the CSV file is submitted on e-Filing.

- Any discrepancy in the CSV file will be detected by the validation rules within the e-Filing system and the licensee notified of such, if any.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.