Summary

This webpage provides detailed instructions on how to complete the quarterly Environmental Levy Return and applicable schedules for tyres DA 178 and DA 178.01 to DA .178.04 for Licensees of:

- Manufacturing Warehouse (VM) in the Tyre Industry; and

- Customs and Excise Warehouse for Ad Valorem Excise Duty purposes.

This webpage includes:

- General Notes on the Environmental Levy Return for tyres;

- The process for declaring the production,

- Removal of tyres;

- Receipt of tyres; and

- Return of tyres.

It also outlines the steps for capturing and submitting the information via SARS e-Filing.

Completion of Environmental Levy Schedules: DA 178.01 to DA 178.04

General Notes: Environmental levy returns for tyres

The production of tyres by the VM, the removal of tyres to the VS, tyres received by the VS and/or tyres returned to the VM from the beginning to the end of the accounting period must be declared on the applicable schedule.

Asterisks were inserted on the DA 178 to assist with the manual completion of the return. The asterisks imply the following:

- * – Both the tyre manufacturer (VM) and motor vehicle manufacturer (VS) must complete this section

- ** – Only the tyre manufacturer (VM) must complete this section.

- *** – Only the motor manufacturer (VS) must complete this section.

Once the DA 178 and applicable schedules are completed, the client will be able to capture the information on e-Filing. All the fields will be visible but clients will not be able to capture any information in the fields that are not applicable to the specific industry.

The opening balance for the VM and VS manufacturers for the first quarter will be NIL

The first accounting period for the submission of the Tyre Levy account will be for the months of February to March 2017 which is due and payable in April 2017, after which the three (3) month quarterly accounting periods will commence on 1 April 2017.

In terms of Rule 54F.07, an accounting period shall be a fixed period of three (3) months calculated from the first day of the month during which manufacturing, removals, receipt and or return of tyres occur until the last day of the month on which such period ends.

The DA 178 and applicable DA 178.01 to DA 178.04 must be completed and the information must be captured and submitted via SARS e-Filing [Refer to Rule 119A.R101A (10) (d)]. The hard copies thereof must be kept for record purposes.

A referenced annexure can be attached to the DA 178.01 to DA 178.04 schedules, if the space is insufficient to declare the removal document reference numbers. The total number of tyres and kilogram net (KN) will be carried forward to the columns on the applicable DA 178.01, .02, .03 or .04. The referenced annexure must be compiled per tyre levy item.

A return must be submitted for each and every accounting period. e-Filing will not allow the capturing of a return if the previous return(s) was not captured and submitted (filed). This implies that NIL returns must also be submitted.

The assessed levy must be paid to the SARS on or before the 25th day of the month following the quarter to which the account relates. Should the said day fall on a Saturday, Sunday or public holiday such payment shall be made on the preceding official working day

Payments must be done on e-Filing. Other payment methods can only be used in exceptional circumstances. For the payment options refer to the Payments – GEN-PAYM-01-G01.

Environmental levy schedules: DA 178.01 to DA 178.04

The schedules must be completed before the DA 178 return as the totals on the schedules will be used to complete the production columns on the return.

Tariff classification is the process whereby any imported, exported or locally manufactured commodity is put into a certain category, by virtue of what it is, or how it is made or what it is used for. It is important that the number and KN of the specific tyres are declared correctly next to the relevant tyre levy item, tariff subheading and article description.

DA 178.01 – Environmental levy: Production sheet

- Only the VM must complete the DA 178.01.

- All the tyres manufactured in the accounting period must be declared on this schedule as per the relevant tariff subheadings.

- The totals of the levy items on the applicable schedule must be brought forward to section A of the tyre levy return (DA 178)

DA 178.02 – Environmental levy: Removal of tyres

- Only the VM must complete the DA 178.02.

- The warehouse number of the VM and VS must be inserted on the DA 178.02.

- All the tyres removed in the accounting period to the VS must be declared on this schedule as per the relevant tariff subheadings.

- The totals of the levy items on the applicable schedule must be brought forward to section A of the tyre levy return (DA 178).

DA 178.03 – Environmental levy: Receipt of tyres

- Only the VS must complete the DA 178.03.

- The warehouse number of the VM who supplied the tyres and the warehouse number of the VS who received the tyres must be inserted on the DA 178.03.

- All the tyres received from the VM in the accounting period must be declared on this schedule as per the relevant tariff subheadings.

- The totals of the levy items on the applicable schedule must be brought forward to section A of the tyre levy return (DA 178).

DA 178.04 – Environmental levy: Tyres returned to VM

- Only the VS must complete the DA 178.04.

- All the tyres found to be off-specification or otherwise defective that were returned to the VM in the accounting period must be declared on this schedule as per the relevant tariff subheadings.

- The totals of the levy items on the applicable schedule must be brought forward to section A of the tyre levy return (DA 178).

Completion of the Environmental levy return for tyres (DA 178)

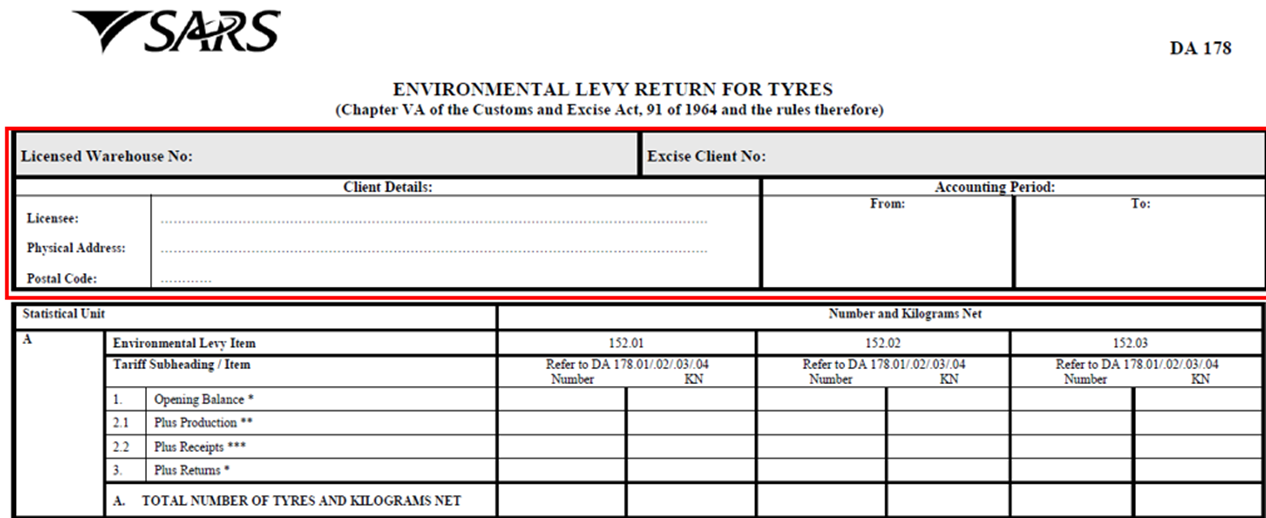

Warehouse particulars

The Licensee must complete the following return:

- Licensed Warehouse No: The allocated VM or VS number (e.g. PEZVM 01927).

- Excise Client No: The Excise number allocated to the company (e.g. 22684018).

- Licensee: The name under which the warehouse is licensed.

- Physical Address: The street name and number, suburb and city of the warehouse.

- Postal Code: The postal code of the warehouse.

Accounting period:

- From: The opening date of the accounting period (The opening date of the account must follow on the closing date of the previous account).

- To: The closing date of the accounting period.

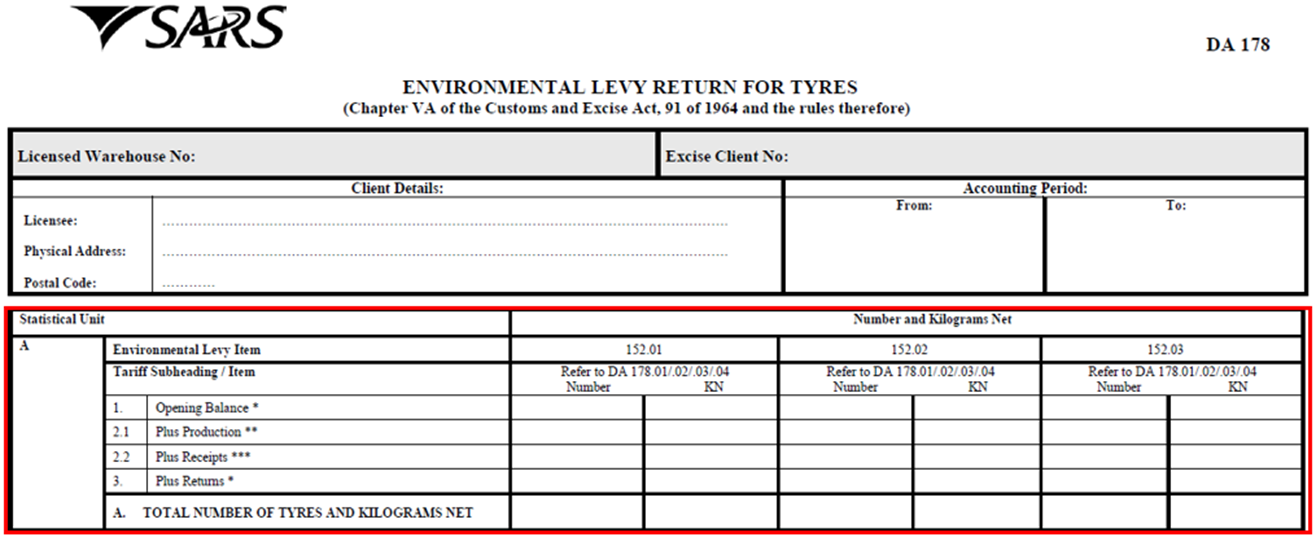

Statistical Unit

- Number: The total number of tyres for the accounting period.

- Kilograms Net: The total kilograms net (KN) of the tyres for the accounting period (The unit code as reflected in Schedule 1 of Part 3E).

A. – Environmental Levy Item (The tariff levy as reflected in Schedule 1 of Part 3E)

- Opening Balance: The balance carried forward from the account of the previous period must be inserted (VM and VS).

- Plus Production: The total production of tyres (number of tyres and KN) during the accounting period as per the totals from the DA 178.01 (VM only).

- Receipts: All leviable tyres (No. and KN) received from the VM which will be fitted to vehicles must be captured for declaration purposes on the DA 178.03 under the relevant tyre levy items and tariff subheadings (VS only).

Plus Returns:

- Returned stock from the local market (South Africa) or returns from the BLNS countries for which credit notes have been issued.

- In the case of returns from a BLNS country the environmental levy thereon must have been paid on entry into South Africa (VM and VS).

- Total No. and KN of Tyres: Total of points 1, 2 and 3 Below per Environmental Levy Item.

B. – Less sales, removals and rebates

- Sales: South Africa: Direct sales and/or removals from the licensed manufacturing warehouse on Delivery/Dispatch Notes (DN) to the local market (South Africa) (VM and VS).

- Sales: BLNS Countries: Direct exports from the licensed manufacturing warehouse including removals on Delivery/Dispatch Notes (DN) to the BLNS Countries (VM and VS).

- Exports: Direct exports beyond the BLNS countries as defined in Item 681.07 of Schedule 6 (VM and VS).

Rebates (Proof of delivery or used under rebate will be required for audit purposes):

- Item 680.01: Goods supplied under rebate of duty as specified in the item (VS only).

- Item 680.02:

- Goods lost or destroyed in the VM warehouse in circumstances of vis major, etc. (VM only)

- Goods cannot be set-off if claimed from insurance.

- Item 680.03: Goods manufactured in the licensed warehouse used for reprocessing of environmental levy goods or the manufacture of other goods (VM only).

- Removals from: Item 680.04: Tyres which have been moved from a licensed VM to a licensed VS to be used in the manufacturing of motor vehicles (VM only).

- Removals to: Item 680.05: Tyres found to be off-specification or otherwise defective by the VS and returned to the VM (VS only).

- Total number and KN of Tyres: Total of points 4.1 to 4.4 Below per Environmental Levy item.

A minus B

- Closing Balance (number of tyres and Kilogram net): – Closing balance at end of accounting period (A minus B).

- Stock taking records will be required for audit purposes.

C Levy on Dutiable Total (4.1 plus 4.2 X rate of levy)

- VM only: Sales (including DN) in South Africa (4.1), plus sales (including DN) to consignees in BLNS countries (4.2) plus exports (4.3) i.e. 4.1 KN + 4.2 KN +4.3 KN x rate of levy as per SCH1P3E; OR

- VS only: Receipts (2.2) plus Returns (3) less Item 680.01 (4.4) less Rebated Removal to (4.6) i.e. 2.2 KN + 3 KN – 4.4 KN – 4.6 KN x rate of levy as per SCH1P3E.

D. Less Levy paid or Payable on goods (Set-off)

Proved removals to BLNS Countries: Item 681.01:

- Goods have been removed to the BLNS countries. (VM and VS).

- Only if proof of exit from South Africa had been obtained – SAD 500 with required acquittal documentation within thirty (30) days of export.

Returns for Reprocessing: Item 681.02:

- Goods have been returned for reprocessing (goods off-specification or otherwise defective) (VM only).

- Credit note(s) must be issued and retained as proof.

Returns from South Africa (other than reprocessing): Item 681.03:

- Goods returned for purposes other than reprocessing.

- Credit note(s) must be issued and retained as proof.

Proved Exports: Item 681.03:

- Goods have been removed to a country outside the SACU.

- Credit note(s) must be issued and retained as proof.

Total amount to be set-off: Total of points 7.1 to 7.3 Below per Environmental Levy item.

E Less: Overpaid on previous account

- Should a licensee have overpaid the levy on a previous account, the overpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the overpayment. Attach the relevant documents to the DA 178 and file for audit purposes.

Plus: Underpaid on previous account

- Should a licensee have underpaid the levy on a previous account, the underpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the underpayment. Attach the relevant documents to the DA 178 and file for audit purposes.

- A report will only be required for points 8 and 9 if the over/under payment has a billing impact on the financial account.

F Nett Levy Payable (C minus D 8 plus 9 as above)

- Amounts due per levy item.

- Total amount of nett levy due: The total amount of nett levy is the sum of the amounts reflected under items 152.01, 152.02 and 152.03

Declaration

The licensee completes the declaration.

For Official Use Only

This section is for official use only and therefore should not be attended to in any way by the licensee or the public officer.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed via the following link: Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.