Purpose

This webpage provides the requirements and processes to follow by a foreign entertainer and sportsperson when reporting, registering and paying tax in South Africa.

Scope

- This webpage applies to:

- Foreign entertainers and sportspersons;

- The resident responsible for founding, organising or facilitating the specified activity in South Africa (Example: Promotor).

Tax on Foreign Entertainers and Sportspersons

Entertainer or Sportsperson

- An entertainer or sportsperson, also generally referred to as a visiting artist, is any person who is a non-resident that for reward:

- Performs any activity as a theatre, motion picture, radio or television artiste or a musician;

- Take part in any type of sport; or

- Takes part in any other activity which is usually regarded as of an entertainment character.

- A non-resident is an individual that is not ordinarily resident in South Africa.

- The activity must be performed in South Africa by an entertainer or sportsperson, either alone or with another person or persons. This includes a non-resident individual who makes use of a company for booking arrangements but performs any of the activities mentioned above.

- Where a resident is primarily responsible for the founding, organising or facilitating of the specified activity in South Africa for reward, directly or indirectly, such resident must notify SARS of such activity within 14 days after the agreement relating to the activity has been concluded. Such notification must include other details as may be required by SARS.

- Refer to the definitions of “entertainer or sportsperson” and “specified activity” in section 47A of the Income Tax Act No. 58 of1962 (Income Tax Act).

The Tax

- 15% tax must be levied on all amounts received or accrued to the entertainer or sportsperson (section 47B of the Income Tax Act).

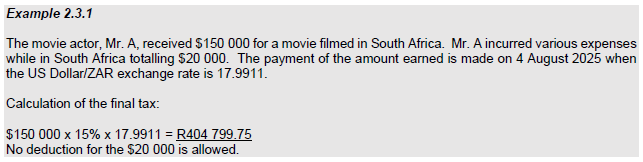

- The spot rate on the date of the payment must be used to convert the tax deducted from the amount received or accrued to the visiting artist when made in a currency other than South African Rands (Refer to section 47J of the Income Tax Act).

- This a final tax.

- The amount received or accruing to the entertainer or sportsperson is exempt from normal tax in South Africa (Refer to section 10(1)(lA) of the Income Tax Act).

- No allowances or deductions can be claimed by the entertainer or sportsperson against this amount of final tax.

- This 15% tax rate would not apply if the entertainer or sportsperson is:

- An employee of a South African employer; and

- Physically present in South Africa for a period exceeding 183 full days in aggregate during any 12 months period commencing or ending during the year of assessment in which the specified activity is performed.

- The foreign entertainer or sportsperson him/herself where the tax was not withheld by a resident.

Notification

- A NR01 (Notification of performance of foreign entertainer or sportsperson) must be submitted by:

- The person who is primarily responsible for founding, organising or facilitating a performance by a foreign entertainer or sportsperson in South Africa; or

- The foreign entertainer or sportsperson him/herself where the tax was not withheld by a resident.

- The NR01 form is available on SARS website www.sars.gov.za.

- The NR01 form must be submitted by email to [email protected].

- In terms of Section 47K, any resident who is primarily responsible for founding, organising or facilitating a performance by a foreign entertainer or sportsperson in South Africa must notify the Commissioner of the performance within 14 days after the associated agreement has been concluded with the entertainer or sportsperson.

- The following documentation must be submitted with the NR01:

- Signed copies of the agreements between the entertainer and sportsperson and the resident organiser/ promoter;

- Copies of the passport(s);

- Calculation of the tax;

- Confirmation of all income earned while in South Africa;

- Confirmation of the exchange rate provided by a South African commercial bank.

Register the Taxpayer

The foreign entertainer or sportsperson (taxpayer) will be registered for Income Tax purposes by SARS based on the information contained in the NR01 and a tax reference number will be allocated. Where the entertainer or sportsperson previously performed in South Africa the previously allocated tax reference number will be used.

Payment

- The tax must be paid over to SARS:

- Where the tax is paid by the entertainer or sportsperson him/herself:

- Within 30 days of the amount being received or accrued to the entertainer or sportsperson. A longer period may be approved by the Commissioner (refer to section 47C(1) of the Income Tax Act).

- Where the tax is withheld by a resident (Example: agent or promotor):

- Before the end of the month following the month during which the tax was deducted or withheld (refer to section 47E(1) of the Income Tax Act).

- Where the tax is paid by the entertainer or sportsperson him/herself:

- Where the tax is withheld by the resident, the following must be done:

- Pay the tax via EFT using the Income Tax reference number of the entertainer or sportsperson.

- Where the visiting artist is responsible for paying the tax, the visiting artist will remain liable until such payment is made.

- Where a resident does not withhold tax or withholds a tax amount which is less than the full amount of tax which should have been withheld or withholds the tax and fails to pay it over, both the resident and the visiting artist remains liable

- Where the one pays, the other one’s liability is discharged.

- Where a resident does not withhold tax or withholds a tax amount which is less than the full amount of tax which should have been withheld or withholds the tax and fails to pay it over, both the resident and the visiting artist remains liable

Liability to Withhold Tax

- The entertainer or sportsperson is personally liable for the tax unless the full amount of tax was withheld by a resident (per section 47C(1) of the Income Tax Act).

- The liability of the foreign entertainer or sportsperson is discharged where:

- The correct tax payable was withheld by a resident in terms of Section 47D for payment to the Commissioner on behalf of the foreign entertainer or sportsperson; or

- The tax was recovered from a resident who failed to withhold the tax and pay it over to the Commissioner.

- The liability of the foreign entertainer or sportsperson is discharged where:

- The resident (agent or promotor):

- Must deduct or withhold the 15% tax from all amounts received or accrued to the foreign entertainer or sportsperson.

- Where a resident does not withhold tax or withholds a tax amount which is less than the full amount of tax which should have been withheld or withholds the tax and fails to pay it over, both the resident and the visiting artist remains liable.

- Where the one pays, the other one’s liability is discharged.

- Where the visiting artist is responsible for paying the tax, the visiting artist will remain liable until such payment is made.

- It is a tax offence to withhold the 15% tax and not pay it over to SARS. If found guilty of an offence, the resident could face a fine or imprisonment up to two years upon conviction.

Assessment

- The income indicated on the tax calculation submitted with the NR01 will be used to issue an assessment for the 15% final tax. Since this is a final tax, no allowances nor deductions are allowed against it.

- Foreign amounts must be converted to South African Rands at the spot rate of the date the amount was deducted or withheld.

- These spot rates are available in the daily newspapers or on the website of the National Reserve Bank (www.resbank.co.za). Note that spot rate is defined in the Income Tax Act No. 58 of 1962 to mean the appropriate quoted exchange rate at a specific time by any authorised dealer in foreign exchange for the delivery of currency.

- A Letter of Finalisation will be issued as well as the Notice of Assessment.

Objections and Appeals

- If the taxpayer or the resident is not in agreement or is aggrieved by the assessment, he/she may object to the assessment.

- The taxpayer or the resident must complete a Notice of Objection (ADR1) and email it to the auditor indicated on the Letter of Finalisation.

- The auditor will consider the objection and deal with it accordingly.

- Where the taxpayer or resident is not satisfied with the outcome of the objection, he/she may submit a Notice of Appeal (ADR2) to the auditor via email within 30 days.

Tax Clearance and Tax Credit Certificate

- SARS will issue a tax clearance certificate on request from the taxpayer.

- SARS will issue a tax credit certificate once payment is received.

Offences and Penalties

- Section 234 of the Tax Administration Act states that any person that wilfully or negligently fails to adhere to any of the following, shall be guilty of an offence and will be liable, to a fine or to imprisonment for a period not exceeding two years on conviction:

- Inform the Commissioner of any specified activity as contemplated in Section 47K;

- Withhold any amount of tax on foreign entertainers and sportspersons;

- Pay the withheld tax over in terms of Sections 47D and 47E.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.