Summary

This webpage guides licensees of Manufacturing Warehouses (VM) in the sugary beverages Industry how to complete the monthly Health Promotion Levy (HPL) Return for Sugary Beverages (DA 179 and DA 179.01).

It provides a step-by-step instruction to completing the DA 179 form and schedule, essential for compliance with HPL regulations.

General Notes: Health Promotion Levy on Sugary Beverages Return

- The return information must be submitted on SARS eFiling on the EXD 01 return. The completed and signed DA 179 hard copy related thereto and supporting documents must be kept for record purposes [Refer to rule 119A.R101A (10)(d) (a – g)]. The DA 179.01 (CSV – file) must be attached to the DA 179.

- The individual line items on the Comma-Separated Values file (CSV – file) must be consolidated per tariff subheading and captured on the DA 179.

- All leviable sugary beverages removals must be captured on a DA 179.01 (CSV – file) and summarised on the DA 179.

- Amounts in column M on the DA 179 must all be indicated in Rands (R) and Cents (C).

- In terms of Rule 54I.05, an accounting period shall be a calendar month calculated from the first day of the month during which manufacturing and removals occur until the last day of the month on which such period ends.

- The first accounting period for the submission of the Health Promotion Levy return for sugary beverages will be for the month of April 2018 which is due and payable in May 2018.

- The DA 179 and DA 179.01 must be completed and the information must be captured and submitted via SARS eFiling [Refer to Rule 119A.R101A (10)(d)]. The hard copies thereof must be kept for record purposes. All the fields will be visible but clients will not be able to capture any information in the fields that are not applicable to the specific industry.

- A return must be submitted for each and every accounting period. eFiling will not allow the capturing of a return if the previous return(s) was not captured and submitted (filed). This implies that NIL returns must also be submitted.

- In terms of Rule 54F.07, the assessed levy must be paid to the SARS within thirty (30) days after the last day of the accounting period, but not later than the penultimate working day of the month following such last day.

- Payments must be done on eFiling. Other payment methods must only be used in exceptional circumstances. For the payment options refer to the Payments – GEN-PAYM-01-G01.

Completion of the DA 179 return and continuation sheet

The following information must be completed:

- Sections A, B, C and D on the DA 179 return; and

- Sections A, B and C on the continuation sheet.

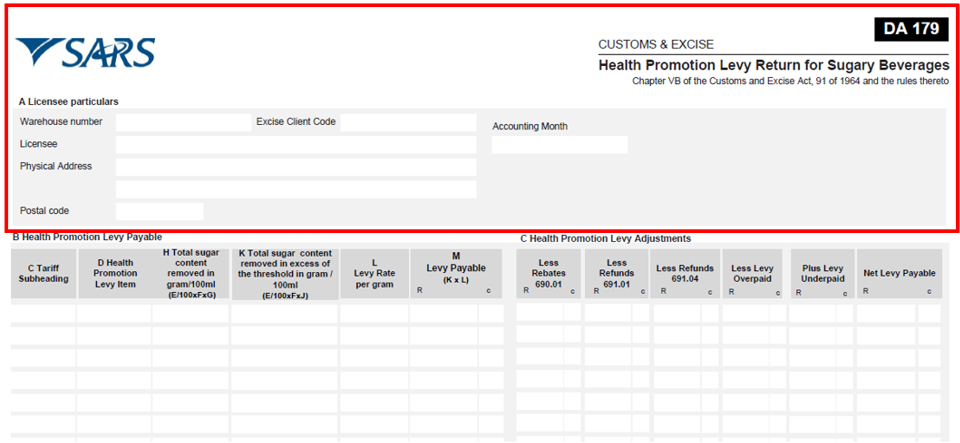

A Licensee particulars

- Warehouse number – The relevant warehouse number allocated to the licensed manufacturing warehouse (e.g. PEZVM 01927).

- Excise Client Code – The Excise code issued to the licensee / registrant (e.g. 22684003).

- Licensee – The name under which the manufacturing warehouse (VM) is licensed.

- Accounting Month – The month in which health promotion levy on sugary beverages goods have been removed from the manufacturing warehouse. A month starts on the 1st day and ends on the last day of that month, or part of a month, when the company started the removals of health promotion levy on sugary beverage goods, or when the company ceased to trade.

- Physical Address – The street name and number, suburb and city of the VM.

- Postal code – The postal area code of the licensed VM.

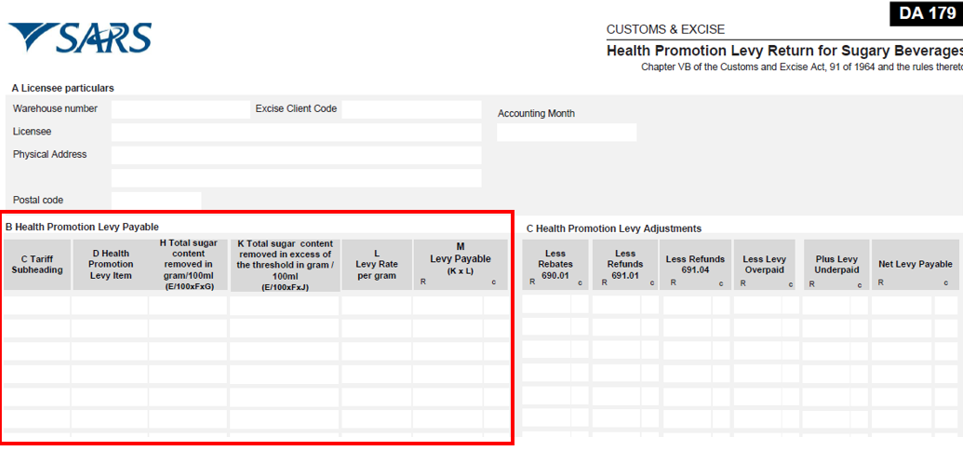

B Health Promotion Levy Payable

- Column C: Tariff subheading – Insert the relevant 8 digit tariff subheading as reflected in Schedule 1 Part 1 – e.g. 1806.10.05, etc.

- Column D: Health Promotion Levy Item – Insert the relevant 7 digit Health Promotion Levy item as reflected in Schedule 1 Part 7A – e.g. 191.01.05.

- Column H: Total sugar content removed g/100ml (E/100 x F x G) – The total sugar content removed in g/100ml as per Column H on the CSV – file. To calculate this amount, the following formula must be used – Column E divided by 100 (equals the number of 100ml units per package) multiplied by Column F (the number of units removed) multiplied by Column G (the total sugar content removed in excess of the threshold). Client to insert rounded off number without any decimals.

- Column K: Total sugar content removed in excess of the threshold in grams/100ml (E/100 x F x J) – The total sugar content removed in excess of 4 grams per 100ml for the accounting month as per Column K on the CSV – file. The amount will be the sugar content LESS the 4 grams per 100 ml threshold. To calculate this amount the following formula must be used – Column E divide by 100 (equals the number of 100ml units per package) multiplied by Column F (the number of units removed) multiplied by Column J (the sugar content leviable). Client to insert rounded off number without any decimals.

- Column L: Levy Rate gram – Insert the applicable levy rate as prescribed by Legislation (Schedule 1 Part 7A). The rate must be inserted on every line.

- Column M: Levy Payable (K x L) – To calculate this amount the following formula must be used – Column K (the total sugar content removed in excess of the threshold in g/100ml) multiplied by Column L (Levy rate g/ 100ml) which is 0.021 rounded off to the 2nd decimal rand value. The sugar content of the product must be certified on a valid test report obtained and retained from a testing laboratory accredited with and using methodology recognised by the South African National Accreditation System (SANAS) or the International Laboratory Accreditation Cooperation (ILAC). After the last Tariff Subheading line, the template must reflect the word “TOTAL” in Column A and in Column M the total amount (formula) will be inserted and calculated.

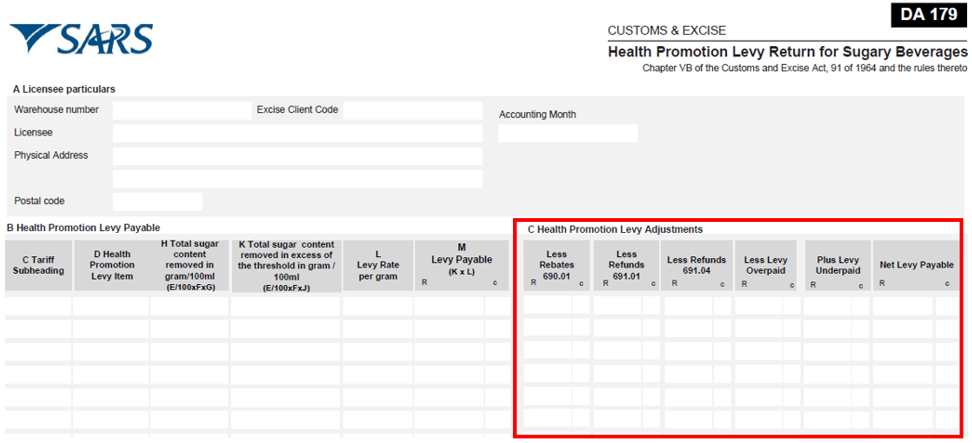

Health Promotion Levy Adjustment

Less Rebates – 690.01 – Goods lost or destroyed in the VM warehouse in circumstances of vis major.

Less Refunds – 691.01 – VM removals (exports) to BLNS countries (only if proof of exit from the Republic was obtained – SAD 500 form with required acquittal documentation within thirty (30) days of export).

Less Refunds – 691.04 – VM removals (exports) beyond the BLNS countries (only if proof of exit from the Republic was obtained – SAD 500 form with required acquittal documentation within thirty (30) days of export).

Less Levy Overpaid:

- Should a licensee have overpaid the levy on a previous account, the overpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the overpayment must be attached to the DA 179.

Plus Levy Underpaid:

- Should a licensee have underpaid the levy on a previous account, the underpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the underpayment must be attached to the DA 179.

Net Levy Payable – The subtotal plus the underpayment made on a previous account.

Exports are declared and sett-off on the DA 179 return as a non-levy removal and therefore cannot be claimed subsequently.

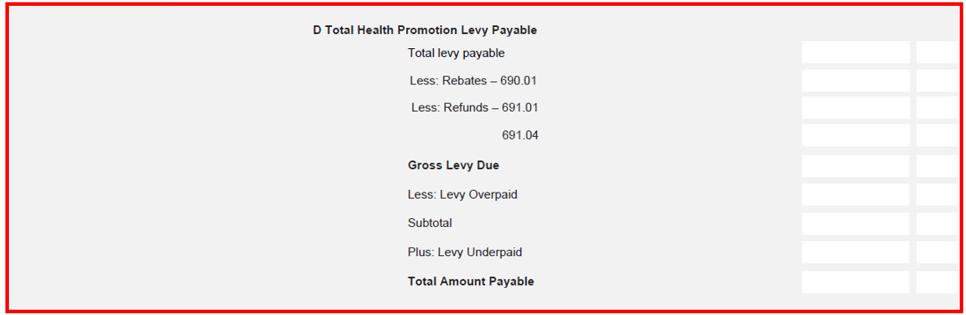

D Total Health Promotion Levy Payable (Section D is not applicable to the Continuation Sheet)

Total levy payable – The total amount of Nett levy payable as reflected in Column M.

Less Rebates – 690.01 – Goods lost or destroyed in the VM warehouse in circumstances of vis major.

Less Refunds – 691.04 – VM removals (exports) beyond the BLNS countries (only if proof of exit from the Republic was obtained – SAD 500 form with required acquittal documentation within thirty (30) days of export).

Gross Levy Due – The total minus the rebated / refund sett-off amounts.

Less: Levy Overpaid:

- Should a licensee have overpaid the levy on a previous account, the overpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the overpayment must be attached to the DA 179.

Subtotal – The gross levy due amount minus the over payment made on a previous account.

Plus: Levy Underpaid:

- Should a licensee have underpaid the levy on a previous account, the underpaid amount must be inserted per levy item.

- A separate report stating the particulars of the relevant accounting period(s) and an explanation regarding the underpayment must be attached to the DA 179.

Total Amount Payable – The subtotal plus the underpayment made on a previous account.

Declaration

The licensee or his duly appointed, by proxy, public officer must complete their personal particulars and signature with date of completion of the DA 179.

For Official use only

This section is for official use only and therefore should not be attended to in any way by the licensee or the public officer.

Completion of the fields on the DA 179.01 – CSV – File

- The following information must be completed on the CSV – file:

- The different packaging sizes (200ml 330ml, 440ml, 1 litre etc.) of the same product must be reflected on individual lines.

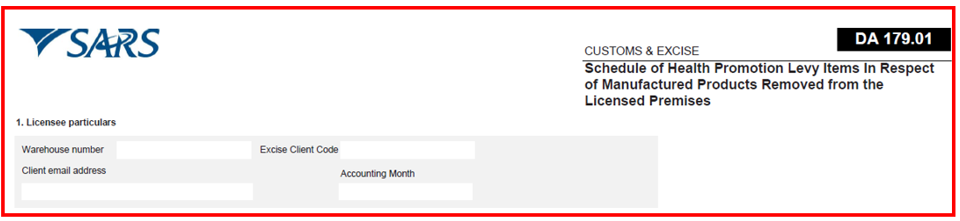

Licensee particulars

Warehouse number – The relevant warehouse number allocated to the licensed manufacturing warehouse (e.g. PEZVM 01927).

Excise Client Code – The Excise code issued to the licensee / registrant (e.g. 22684018).

Taxpayer e-mail address – E-mail address of the licensee.

Accounting Month:

- The month in which health promotion on sugary beverages levy goods have been removed from the manufacturing warehouse.

- A month starts on the 1st day and ends on the last day of that month, or part of a month, when the company started the removals of health promotion on sugary beverage levy goods, or when the company ceased to trade.

Declaration in respect of sugary beverage products removed

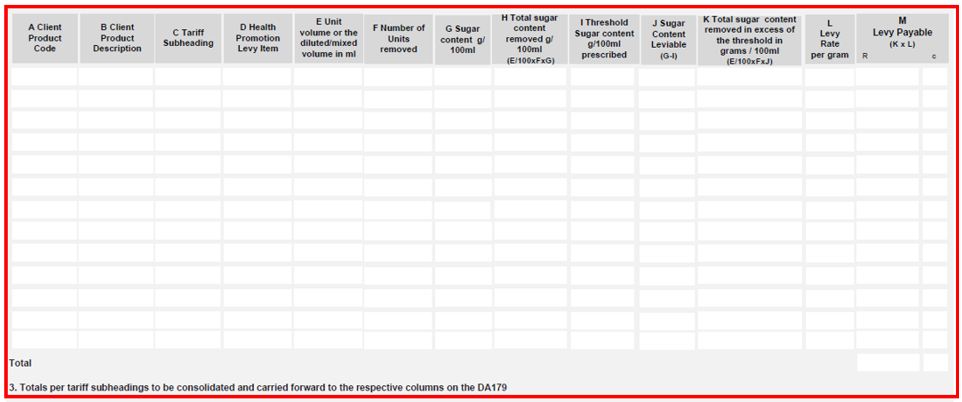

- Column A: Client Product Code – This is the specific product’s identification code normally printed on the product packaging.

- Column B: Client Product Description – This is the specific product’s trade name also printed on the packaging.

- Column C: Tariff Subheading – Insert the relevant 8-digit tariff sub-heading as reflected in Schedule 1 Part 1 – e.g. 1806.10.05

- Column D: Health Promotion Levy Item – Insert the relevant 7-digit Health Promotion levy item as reflected in Schedule 1 Part 7A – e.g. 191.01.05.

- Column E: Unit package volume in g/ml – This is the specific packaging size of the package in which the product is put up for retail sale, e.g. 330ml.

- Column F: Number of Units removed – This is the total number of units of a specific product and specific packaging removed from the VM.

- Column G: Sugar content in g/100ml:

- This sugar content amount must be obtained from a valid test report issued by a SANAS or ILAC approved laboratory.

- If the said report is not available upon the completion of this DA179.01 (CSV – file), the client must use the deemed sugar content of the sugary beverage that is assumed to constitute 20grams per 100 ml.

- Column H: Total sugar content removed g/100ml (E/100 x F x G):

- The total sugar content removed in g / 100ml as per Column H on the CSV – file.

- To calculate this amount the following formula must be used – Column E divided by 100 (equals the number of 100ml units per package) multiplied by Column F (the number of units removed) multiplied by Column G (the total sugar content removed in access of the threshold).

- Client to insert rounded off number without any decimals.

- Column I: Threshold Sugar content g/100ml prescribed – The threshold is reflected in Schedule 1 Part 7A.

- Column J: Sugar Content Leviable (G-I) – To calculate this amount the following formula must be used – Column G (Sugar content in g/100ml minus Column I (The threshold sugar content g/100ml prescribed).

- Column K: Total sugar content removed in excess of the threshold in grams/100ml (E/100xFxJ) – To calculate this amount, the following formula must be used – Column E (Unit package volume) divided by 100 multiplied by Column F (Number of units removed) multiplied by Column J (Sugar content leviable).

- Column L: Levy Rate per gram – This rate is reflected in Schedule 1 Part 7A.

- Column M: Levy Payable (K x L):

- To calculate this amount the following formula must be used – Column K (the total sugar content removed in excess of the threshold in g/100ml) multiplied by Column L (Levy rate g/100ml) which is 0.021 rounded off to the 2nd decimal rand value.

- The sugar content of the product must be certified on a valid test report obtained and retained from a testing laboratory accredited with and using methodology recognised by the South African National Accreditation System (SANAS) or the International Laboratory Accreditation Cooperation (ILAC).

Calculation examples of the DA 179 and DA 179.01

- Examples of the DA 179 – return and DA 179.01 – CSV – file may be found by using the below noted reference numbers:

- DA 179 – Reference number – SE-SB-03-A01; and

- DA 179.01 – Reference number – SE-SB-03-A02.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.