Summary

The purpose of this webpage is to assist provisional taxpayers with the following:

- Completion and submission of the Provisional Tax Return (IRP6)

- Calculation of the estimated taxable income for provisional tax payments

- Calculation of penalties and interest payable on late or incorrect payments of provisional tax.

This webpage is published for information purposes only, so that provisional taxpayers can understand their tax obligations.

- It should not be considered as specific tax advice for an individual taxpayer.

- Guidelines and tax tables presented in this webpage contain generic information to guide provisional taxpayers to correctly complete and submit the IRP6 return and to make the necessary payments on time.

- This webpage is intended to be used as a basic guide and is not for legal reference.

- Further guidance and assistance can be obtained from your nearest SARS or by calling Taxpayer Service on 0800 00 7277

General Information

A ‘provisional taxpayer’ is:

- A person (other than a company) who earns income which is not remuneration, an allowance or advance as contemplated in section 8(1) or who earns remuneration from an employer that is not registered for employees’ tax

- A company;

- A person notified by the SARS Commissioner that he/she is a provisional taxpayer.or

- A labour broker with an exemption certificate issued in terms of paragraph 2(5)(a).

The following are specifically excluded from the payment of provisional tax:

- Public Benefit Organisations (PBOs) approved by SARS

- Recreational clubs approved by SARS

- Any Body-Corporate, share block company or association of persons contemplated in section 10(1) (e)

- Any natural person who does not derive income from the carrying on of any business, if in that relevant year of assessment –

- Taxable income does not exceed the tax threshold; or

- The taxable income from interest, dividends, foreign dividends, rental from letting fixed

property and remuneration from an employer that is not registered for employees’ tax does

not exceed R30 000

- Non-resident owners or charterers of ships and aircraft who are required to make payments under section 33

- Any small business funding entity

- Deceased estates

Provisional Tax is not a separate tax, but merely a mechanism to pay the normal Income Tax liability during the tax year and is therefore an advance payment of a taxpayer’s normal tax liability.

A provisional taxpayer is generally required to make two provisional tax payments, one six months into the year of assessment and another at the end of the year of assessment. Taxpayers may make an additional payment, generally known as the third or top-up payment, after the end of the year of assessment for the purpose of preventing or reducing a liability for interest that would arise should their first two provisional payments be inadequate.

Provisional tax payments are calculated on estimated taxable income, including current taxable capital gains, for that particular year of assessment. These estimates of taxable income are submitted to SARS on an IRP6 return. An IRP6 return can be requested and submitted, even if the amount of the provisional tax payment is nil, via the following channels:

- SARS eFiling at www.sarsefiling.co.za

- Nearest SARS or by calling Taxpayer Service on 0800 00 7277

The normal tax payable on the estimated taxable income is calculated at the relevant rate of tax that is in force on the date of payment of provisional tax.

- This is the rate of tax as prescribed in the tax tables which are fixed annually by Parliament.

- The provisional tax tables/rates and instructions are for the 2026 year of assessment for Individuals, Trusts, and Small Business Corporation (1 March 2025 – 29 February 2026).

- Provisional tax payments cannot be refunded or reallocated to different periods.

- Provisional tax payments cannot be allocated to different taxpayers.

- The provisional tax payments, together with any PAYE withheld during the year will be offset against the liability for normal tax at the end of the year of assessment.

- Any excess may be refunded after the taxpayer has been assessed for the relevant year of assessment; and any shortfall is payable by the taxpayer to SARS.

- Interest is generally payable from the effective date by SARS (in the case of a refund) and by the taxpayer (in the case of a shortfall).

Paying the amounts due in terms of your provisional tax liability will prevent a large amount of tax (as well as penalties and interest) being due by you on assessment, as the tax liability will have been spread over a period of time prior to the issue of such assessment.

Section 9H of the Income Tax Act states that the date on which the taxpayer ceased to be a RSA resident must be manually completed on the IRP6, during the year of assessment where the income, deduction and tax credit overlaps between the period of residence and non-residence.

The prescribed rate of interest applicable to late payments or to the under or overpayment of tax according to s187 of (the TAACT) and may change from time to time.

Governing Legislation

- The applicable legislation is the Income Tax Act No. 58 of 1962 (the Act), specifically the Fourth Schedule thereto (the Fourth Schedule), and the Tax Administration Act No. 28 of 211 (the TAACT).

- Where not specified, references to paragraphs would be to paragraphs of the Fourth Schedule, and references to sections would be to sections of the Act, unless the context indicates otherwise.

Directors of Private Companies & Members of Close Corporations

- In terms of the definition of “employee” in subpar 1(g), directors of private companies (which include members of close corporations) are regarded as employees.

- Directors of private companies and members of close corporations are not automatically deemed to be provisional taxpayers unless they have other business income.

Estimates of Taxable Income

- Provisional taxpayers (other than a company)

- Provisional taxpayers must, during every period, submit an estimate of the total taxable income which will be derived by the taxpayer in respect of the year of assessment for which the provisional tax is payable. This estimate must not include any retirement fund lump sum benefits, retirement fund lump sum withdrawal benefit or any severance benefit received by or accrued to the taxpayer during the relevant year of assessment. The return must be submitted even if the provisional tax calculation results in a nil payment.

- The taxable portion of the aggregate capital gain for the current year of assessment must be included in both the first and second provisional tax calculations.

- The amount of estimate submitted by a provisional taxpayer shall not be less than the basic amount applicable to that particular estimate, unless the Commissioner after taking into account the circumstances of the case agrees to an estimate that is lower than the basic amount.

- The Commissioner may call upon a provisional taxpayer to justify any estimate, or to furnish particulars of the income and expenditure or any other particulars that may be required. If the Commissioner is dissatisfied with the estimate, he or she may increase it to what he or she considers reasonable, even if this is more than the basic amount. The increase of estimate is not subject to objection and appeal.

- The ‘basic amount’ is the taxpayer’s taxable income assessed by the Commissioner for the latest preceding year of assessment, not less than 14 days before the date the taxpayer submits the provisional tax return LESS:

- The amount of any taxable capital gain;

- Taxable portion of a retirement fund lump sum benefit or retirement fund lump sum withdrawal benefit or severance benefit (other than any amount included under para (eA) of “gross income”);and

- Any amount, including any voluntary award received or accrued contemplated in paragraph (d) of “gross income” (excluding a severance benefit).

- Company Provisional taxpayers must submit a return of an estimate of the total taxable income which will be derived by the company in respect of the year of assessment.

- Basic amount is the taxpayer’s taxable income assessed by the Commissioner for the latest preceding year of assessment LESS the amount of any taxable capital gain in that year of assessment.

- The basic amount for all taxpayers must be increased by 8% if the estimate is made more than 18 months after the end of the latest preceding year of assessment

- “year last assessed”, as shown on the IRP6 return, will refer to an assessment preceding the year of assessment for which the estimate is made, and for which a notice of assessment relevant to the estimate has been issued by SARS not less than 14 calendar days prior to the due date of such estimate.

- Estimates of taxable income and basic amount calculations:

Example 1:

- Statement for a provisional taxpayer with year of assessment ending on 28 February 2017:

- The notice of assessment for the 2016 tax year of assessment was issued on 15 August 2016

- The IRP6 for the 2017 tax year 1st period was submitted on the due date, 31 August 2016.

- The notice of assessment for the 2015 tax year of assessment was issued on 15 July 2015.

- Statement for a provisional taxpayer with year of assessment ending on 28 February 2017:

Solution:

- The notice of assessment of the 2016 year of assessment was issued 15 days before the date on which the provisional tax estimate for the first period of 2017 was submitted (the period between 15 August 2016 and 31 August 2016). Due to the 14 calendar days criteria being met, the latest preceding year is the 2016 tax year

- The estimate is not made more than 18 months (the period between 28 February 2016 and 31 August 2016)

- Since the estimate is not made more than 18 months, therefore the basic amount will not be increased by 8%.

- The taxpayer’s basic amount will be based on the taxable income as assessed in 2016.

Example 2:

- Statement for a provisional taxpayer with the year of assessment ending on 28 February 2017:

- The notice of assessment for the 2016 tax year assessment was issued on 19 August 2016

- The IRP6 for the 2017 tax year 1st period was submitted on the due date, 31 August 2016

- The notice of assessment for the 2015 tax year of assessment was issued on 15 July 2015.

Solution:

- The notice of assessment of the 2016 year of assessment was issued 11 days before the date on which the provisional tax estimate was submitted. Therefore, the 2016 assessment does not meet the 14 calendar days criteria, and therefore the latest preceding year of assessment is the 2015 tax year of assessment

- The estimate is not made more than 18 months after the latest preceding year of assessment (the period between 28 February 2015 and the 31 August 2016)

- Therefore, the basic amount will not be increased by 8%

- The basic amount will be the amount of taxable income as assessed in 2015.

Example 3

- Statement for a provisional taxpayer with the year of assessment ending on 28 February 2017:

- The notice of assessment was issued for the 2013 tax year on 30 June 2013

- The taxable income as assessed in 2013 was R260 000 and included a taxable R25 000 and severance benefit of R40 000

- The IRP6 for the 2017 tax year 1st period was submitted on the due date, 31 August 2016

- The 2014, 2015 and 2016 tax returns have not been submitted.

Solution:

- The 2013 notice of assessment was issued more than 14 calendar days before the date on which the provisional tax estimate was submitted on 31 August 2016.The 2014, 2015 and 2016 tax returns have not been submitted.

- The estimate is submitted more than 18 months (the period between 28 February 2013 and 31 August 2016) after the end of the last preceding year (2013)

- The basic amount for 2013 is calculated as follows:

- Taxable income assessed in 2013 R 260 000

- Less: Taxable capital gain R 25 000

- Less: Severance benefit R 40 000

R 195000

- The basic amount (R195 000) must be increased by 8% for each year from 2013 to 2017, therefore R257 400 [R195 000 + (R195 000 x 8% x 4)] is the basic amount for the 2017 tax year.

Justification of an Estimate by the Taxpayer

- In terms of paragraph 19(3), a provisional taxpayer may be asked to justify any estimate made or to furnish full particulars of income, expenditure and/or any other particulars that may be required

- If SARS is not satisfied with the response, the estimate may be increased to an amount which is considered reasonable.

- This increase of the estimate by SARS is not subject to objection and appeal.

- SARS will notify the taxpayer and issue a revised estimate which will be used to calculate your provisional tax liability.

- Refer to “Interpretation Note 1 (Issue 3) of 20 February 2019” which is available on the SARS website (www.sars.gov.za) for more information.

Form used to Capture Provisional Tax Calculations

- Both resident and non-resident taxpayers are required to complete an IRP6 return for provisional tax purposes. The IRP6 return can be completed for all types of taxpayers

- Individuals

- Trusts

- Companies

- A provisional taxpayer is required to request and submit a return (IRP6) for the first and second period even if, according to the result of the provisional tax calculation, the total amount of tax due and payable is ‘Nil’ (0).

Failure to Submit a Provisional Tax Return (IRP6)

- The Commissioner may estimate the taxable income and determine the amount payable; if the provisional taxpayer fails to submit an estimate for any particular period.

- The estimate made by the Commissioner is effective for the relevant period within which the provisional taxpayer is required to make the payment for provisional tax.

How is Provisional Tax Calculated

- There are two compulsory provisional tax payments in respect of a year of assessment based on the estimated taxable income.

- There is also a third “voluntary top-up” or “additional” provisional payment, but unlike the first and second payments, the third payment is often based on the actual taxable income for the year.

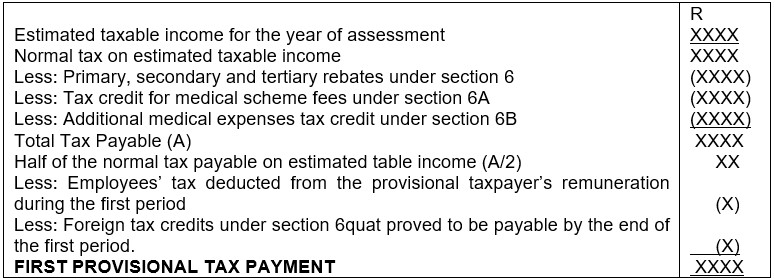

Provisional Taxpayers other than Companies

Note 1: Refer to the attached annexures for detailed calculations.

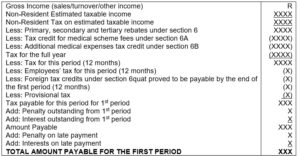

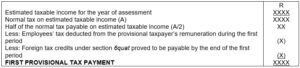

The first period provisional tax payment is calculated as follows.

Note 2:

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016.

- This means that the section 6quin deduction is not available from the 2017 year of assessment

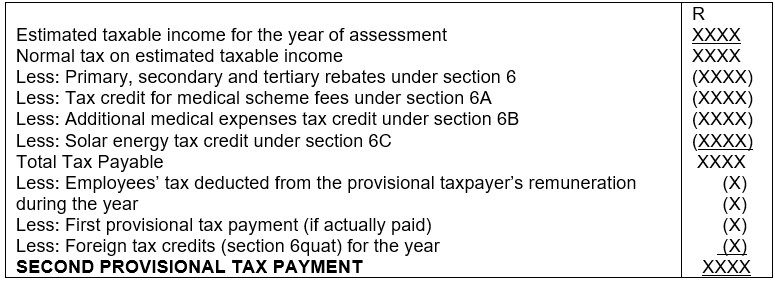

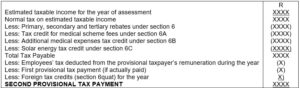

The second period provisional tax payment is calculated as follows:

Note 3:

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016.

- This means that the section 6quin deduction is not available from the 2017 year of assessment.

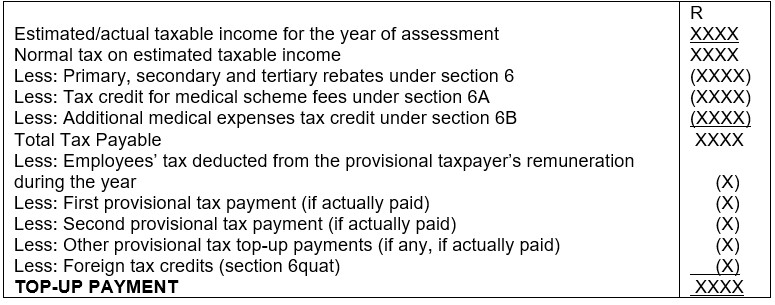

The third period (top-up/voluntary) provisional tax payment is calculated as follows:

Note 4:

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016.

- This means that section 6quin deduction is not available from the 2017 year of assessment.

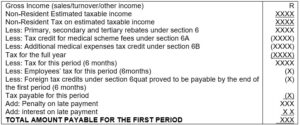

- The first period provisional tax payment for a non-resident is calculated as follows.

The second period provisional tax payment for a non-resident is calculated as follows.

Note 5:

The year of assessment of a natural person ends on the date on which the person ceases to be a RSA resident, and two assessments are created during the single year.

Foreign Tax Rebates

- Section 6quat

- Provides for foreign tax rebate in respect of foreign tax on income from a non-South African source.

- This rebate allows against South African tax, any foreign tax paid or payable (converted to rands) included in the South African taxable income of the resident

- Due to the deletion of section 6quin, provisional taxpayers will be granted a deduction in terms of section 6quat (1C) as opposed to a tax credit against tax

- In terms of section 6quat (1C), provisional taxpayers will be entitled to claim a deduction from income for services rendered in South Africa and taxed outside South Africa as from the 2017 year of assessment.

- In terms of section 6quat (1A)(a)(iii) a resident can claim foreign credit against capital gains tax paid on the disposal of the asset situated outside the Republic, included in the taxable income to prevent double taxation. Capital gain tax paid outside the Republic that is higher than the rate charge in the Republic, the full credit will be limited to the extent of the taxes paid in Republic in respect of the taxable capital gain.

- Section 6quin

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016

- Detailed information on foreign tax credit is accessible on the SARS website (www.sars.gov.za).

Medical Scheme Fees Tax Credit

- Effective from 1 March 2012 the current medical scheme contribution deduction for taxpayers below 65 years of age, was replaced by medical tax credit.

- With effect from 1 March 2014, persons over the age of 65 years or older are also entitled to the medical scheme fees tax credit contribution as a deduction.

- This rebate is deducted from the normal tax payable by a natural person.

- The medical scheme fees tax credit is applicable to fees paid by the person to a medical scheme registered under the Medical Schemes Act, or a fund which is registered under any similar provision contained in the laws of any other country where the medical scheme is registered.

- The tax credit is applicable in respect of fees paid by the taxpayer to a registered medical scheme.

- The number of persons (dependents) for whom the contributions to a medical scheme determines the value of credit, and the medical scheme contribution tax credit is as follows:

- R364 in respect of the person who has paid the contribution;

- R364 in respect of the person’s first dependent;

- R246 in respect of the benefits to each additional dependent.

- The number of persons (dependents) for whom the contributions to a medical scheme determines the value of credit, and the medical scheme contribution tax credit is as follows:

Additional Medical Expenses Tax Credit

- A further medical expenses tax credit amount in addition medical scheme fees tax credit is deducted from the normal tax payable by a person who is a natural person.

- A person who is 65 years or older or an individual, his or her spouse, or his or her child is a person with a disability is eligible for 33.3% of the aggregate of the full medical scheme contributions in excess of three (3) times the credit plus 33.3% of all other qualifying out of pocket medical expenses paid by that person (excluding medical scheme contributions).

- Persons below 65 years are entitled to 25% of the aggregate of the full medical scheme contributions in excess of four (4) times the plus all other qualifying out of pocket medical expenses (excluding medical scheme contributions), only to the extent that the amount exceeds 7,5% of the taxable income excluding retirement fund lump sums and severance benefits.

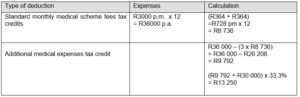

- Example – Person 65 years and older

Statement:

- Mr. ABE is 65 years old, and he has made R3000 contribution per month to a medical scheme for himself and his wife from 1 March 2024

- His qualifying medical expenses by 29 February 2025 is R30 000.

Solution:

- Therefore, Mr ABE’s tax liability will be reduced by R21 986 [R8 736 (medical scheme fees + R13 250 (additional medical expenses)]

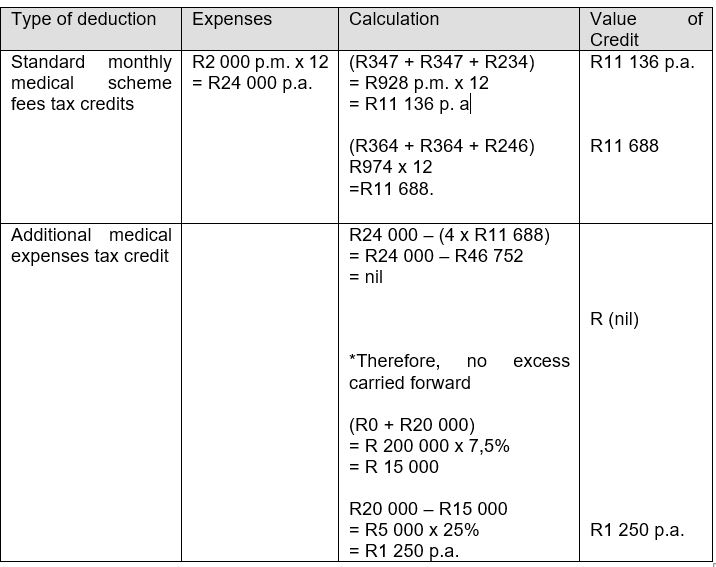

- Example – Person under 65 years

Statement:

- Ms. PAS is 45 years old and she has made R2 000 contributions to the medical scheme per month on behalf of herself and her two children

- By 29 February 2024 she incurred R20 000 in qualifying medical expenses

- Her taxable income for the 2024 tax year is R200 000.

Solution:

- Therefore, Ms. PAS’s tax liability will be reduced by R12 938 [R11 688 p.a. medical scheme fees) + R1 250 additional medical expenses)].

Solar Energy Tax Credit

- The solar energy tax credit has been introduced to encourage individual taxpayers to invest in new and unused solar photovoltaic panels acquired by the individual taxpayers and brought into use for the first time on or after 1 March 2023 and before 1 March 2024.

- The new or unused solar photovoltaic panels that qualify for the solar energy tax credit must not have generation capacity of less than 275W.

- The solar energy tax credit rebate amount is 25 per cent of the cost of the photovoltaic panels limited to R15 000.

- The solar panels must be installed and mounted on or affixed to the residence mainly used for domestic purposes by the taxpayer and must be connected to the distribution board of that residence.

- The electrical certificate of compliance must be issued on installation of the solar panels as contemplated by the Electrical Installation Regulations Act of 2009.

- The solar energy tax credit amount on the second period provisional tax payment is calculated as follows:

Provisional Taxpayers who are Companies

Note 1: Refer to the attached annexures for detailed calculations.

The first period provisional tax payment is calculated as follows:

Note 2:

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016.

- This means that section 6quin deduction is not available from the 2017 year of assessment.

The second period provisional tax payment is calculated as follows:

Note 3:

- The rebate available under section 6quin was deleted for years of assessment commencing on or after 1 January 2016

- This means that section 6quin deduction is not available from the 2017 year of assessment.

The third period (top-up/voluntary) provisional tax payment is paid in addition to the amounts that must be paid at the end of the first and second provisional tax periods. The payment is made to reduce the interest on underpayment of provisional tax prior to the effective date. The third period provisional tax payment is calculated as follows:

When must Provisional Tax be Paid

- In terms of paragraphs 21, 23, 23A, and 25(1) the due dates for payments are:

- First period: This payment must be made within six months from the commencement of the year of assessment in question.

This means that for the year of assessment that starts on the 1 March and end on the 28/29 February, the first period for which provisional tax becomes due will be the period ending 31 August - Second period: This payment must be made not later than the last day of the year of assessment in question.

This means that for the year of assessment that starts on the 1 March and end on the 28/29 February, the second period for which Provisional Tax becomes due will be the period ending on the 28/29 February.

- First period: This payment must be made within six months from the commencement of the year of assessment in question.

- The provisional tax return and payment for the “first” period is not required in instances where the duration of the year of assessment does not exceed a period of six months as a result of e.g. death, ceasing to be a tax resident, company being incorporated during the year or if there has been a financial year end change for the company

- In the case of individuals and trusts where a February financial year-end creates financial hardship and an approval has been obtained from SARS to submit financial statements to a date other than the end of February, such persons may also request approval to submit IRP6 returns in line with the approved financial year-end. All other income however remains in the year of assessment ending 28/29 February.

- Half of the Provisional Tax liability is payable within 6 months after the commencement of the year of assessment for companies, and it is based on the total estimated liability for the company. An amount that is equal to the total estimated liability is payable within the period ending on the last day of the year, less the amount paid for the first period, employees’ tax deducted by the taxpayer’s employer from the taxpayer’s remuneration, and any tax payable to the government of any country which will qualifies for a rebate.

- Payment of Provisional Tax upon an assessment notice issued by SARS must be done within the period specified in such notice.

- Example of payment dates

- The following example refers to a 28 February 2021 year-end (2021 tax year)

- First provisional tax payment due on 31 Aug 2020

- Second provisional tax payment due on 28 Feb 2021

- Third or voluntary payment due on 30 Sept 2021

- The following example refers to a 31 May 2021 year-end (2021 tax year):

- First provisional tax payment due on 30 Nov 2020

- Second provisional tax payment due on 31 May 2021

- Third or voluntary payment due on 30 Nov 2021

- The following methods to effect payments to SARS are available:

- At your bank

- Via eFiling

- Via Electronic Funds Transfer (EFT)

- Where payments are made electronically, provision must be made for your bank’s cut-off times and for a clearance period that could take between two and five days.

- Bank payments – taxpayers paying over the counter at any ABSA, FNB, Nedbank or Standard Bank branch will no longer need to supply a bank account number and bank code when making payments. This applies equally to all internet-banking clients of ABSA, Capitec Bank, FNB, Investec, Mercantile Bank, Nedbank and Standard Bank

- All that will be required is:

- The client’s 19-digit payment reference number

- The beneficiary ID/account number which is linked to a specific type of tax to make payments

- These details are reflected on the payment advice of the IRP6 return.

- Payments that do not comply with both the above-mentioned payment reference number and the beneficiary ID will not be accepted.

- If the last day for payment falls on a public holiday or weekend, the payment must be made on the last working day prior to the public holiday or weekend. For more details refer to the SARS website www.sars.gov.za

- For detailed information on payments refer to the ‘External Guide South African Revenue Payment Rules’.

Deferral of Payment – Instalment Payment Agreement (In Terms of s167 of Taact)

- A senior SARS official may enter into an agreement with a taxpayer in the prescribed form under which the taxpayer is allowed to pay a tax debt in one sum or in instalments, within the agreed period if satisfied that:

- Criteria or risks that may be prescribed by the Commissioner by public notice have been duly taken into consideration; and

- The agreement facilitates the collection of the debt.

- The agreement may contain such conditions as SARS deems necessary to secure collection of tax.

- SARS may terminate an instalment payment agreement if the taxpayer fails to pay an instalment or to otherwise comply with its terms and a payment prior to the termination of the agreement must be regarded as part payment of the tax debt.

- The agreement remains in effect for the term of the agreement except if:

- A senior SARS official may modify or terminate an instalment payment agreement if satisfied that either:

- The collection of tax is in jeopardy;

- The taxpayer has furnished materially incorrect information in applying for the agreement;

- The financial condition of the taxpayer has materially changed.

- A termination or modification

- Takes effect as at the date stated in the notice of termination or modification sent to the taxpayer; and

- Takes effect 21 business days after notice of the termination or modification is sent to the taxpayer.

Note: Section 167 of TAACT is only applicable to tax debt that arise as a result of the issued assessment. Therefore, the deferral of payment in terms of section 167 of TAACT does not apply to provisional tax.

Deferral of Payment – Criteria for Instalment Payment Agreement (in Terms of S168 OF TAACT)

- A senior SARS official may enter into an instalment payment agreement only if any of the following applies:

- The taxpayer suffers from a deficiency of assets or liquidity which is reasonably certain to be remedied in the future;

- The taxpayer anticipates income or other receipts which can be used to satisfy the tax debt;

- Prospects of immediate collection activity are poor or uneconomical but are likely to improve in the future;

- Collection activity would be harsh in the particular case and the deferral or instalment agreement is unlikely to prejudice tax collection; or

- The taxpayer provides the security as may be required by the official.

Interest on Underpayment of Provisional Tax

- 89bis interest

- Interest in terms of section 89bis is levied at the prescribed rate from 1 March 2025 to 30 April

2025 is 11.25%, from 1 May 2025 the prescribed rate is 11.00% per annum subject to changes

as published in Government Gazette is payable on late payments in respect of first, second and

third periods.

- Interest in terms of section 89bis is levied at the prescribed rate from 1 March 2025 to 30 April

- 89quat interest

- Interest in terms of section 89quat is either levied on an underpayment of tax or paid on an overpayment of tax from the ‘effective date’. See below for an explanation of the ‘effective date’.

- 89quat(2) interest

- Interest in terms of section 89quat(2), is payable by a provisional taxpayer if the normal tax exceeds the ‘credit amount’ (i.e. an underpayment of tax) and if in the case of:

- An individual or trust, the taxable income for the year of assessment exceeds R50000, or

- A company, the taxable income for the year exceeds R20 000.

- This interest is levied at the prescribed rate 1 March 2025 to 30 April 2025 is 11.25%, from 1 May 2025 the prescribed rate is 11.00% per annum subject to changes as published in Government Gazette in terms of section 89(2) and is calculated from the day following the ‘effective date’ to the day before the first due date on the relevant assessment notice

- Interest on underpayment of Provisional Tax paid by a taxpayer is not a tax-deductible expense.

- Example-89quat(2) interest:

- First due date on assessment notice is 1 December 2019,interest on underpayment for the 2019 year of assessment (February year-end) will be calculated from 1 September 2019 to 30 November 2019.

- Interest in terms of section 89quat(2), is payable by a provisional taxpayer if the normal tax exceeds the ‘credit amount’ (i.e. an underpayment of tax) and if in the case of:

Penalties

- Paragraph 20 penalty in the event of taxable income being underestimated:

- A penalty will be levied under certain circumstances where it has been determined that the actual taxable income is more than the taxable income estimated on the second provisional tax return.

- The penalty amount depends on whether the actual taxable income is more or less than R1 million

- The penalty may be levied even if the Commissioner has increased the estimate in terms of paragraph 19(3). The second estimate that has been submitted by the taxpayer is used to determine if the estimate is more or less than R1 million.

- If a person does not submit the final estimate (which is the 2nd IRP6) by the relevant due date, the taxpayer would be deemed to have submitted an estimate of an amount of nil taxable income unless the 2nd IRP6 is submitted within four months after the end of the relevant year of assessment.

- Certain once-off amounts such as a retirement fund lump sum benefit, retirement fund lump sum withdrawal benefit or severance benefit payments, are excluded from the calculation of the penalty, however any amount contemplated in paragraph (d) of the definition of ‘gross income’ is included in the penalty calculation.

- A penalty levied for the underestimation of actual taxable income on the second period; is reduced by the penalty imposed for the late payment of provisional tax under paragraph 27.

- If the Commissioner is satisfied that the failure to submit such an estimate timeously was not due to intent to evade or postpone the payment may remit the whole or any part of the penalty.

- Provisional taxpayers with a taxable income of up to R1 million

- Where the estimate is less than 90% of the actual taxable income and also less than the basic amount, a penalty is levied (deemed to be a percentage based penalty under Chapter 15 of the TAACT equal to 20% of the difference between

- The lesser of –

- The amount of normal tax calculated in respect of a taxable income equal to 90% of such actual taxable income (after taking into account any amount of deductible rebates); and

- The amount of normal tax calculated in respect of a taxable income equal to such basic amount (after taking into account any amount of deductible rebates); and

- The amount of employees’ tax and provisional tax paid by the end of that year of assessment.

- Any retirement fund lump sum benefit, retirement fund lump sum withdrawal benefit or severance benefit received/accrued should be excluded from the above penalty calculation.

Example – Provisional taxpayer with a taxable income of up to R1 million

- Statement relating to Mr. XY for year of assessment ending 28 February 2021:

- Mr. XY is a provisional taxpayer and he is required to submit his provisional tax returns for the 2015 year of assessment

- Mr. XY’s basic amount of R300 000 is based on the notice of assessment for the 2014 year of assessment

- His expected taxable income will be less than the basic amount as a result of poor trading conditions. He submitted his first and second period’s estimates with taxable income of R200 000 for the year

- On assessment Mr. XY’s final taxable income was determined as R280 000 for the year.

- His provisional tax payment for the year amounted to R38 408.00, and no employees’ tax was not paid.

Solution

- The first step – determine whether the final estimate of taxable income less than 90% of actual taxable income and less than basic amount?

Final estimate of provisional taxable income =R200 000

Basic amount (2014 YOA) = R300 000

Actual taxable income (2015 YOA) = R280 000

Therefore,

Actual taxable income is less than

90% of final provisional taxable income (R280 000 x 90% = R252 000) and basic amount (R300 000)

- The second step – determination of the penalty

20% of the difference between – the lesser of

tax on 90% of R252 000 taxable income = R51 408; and

tax on basic amount of R300 000 = R65 471

Therefore,

R52 408 less R38 408 (provisional tax payment) = R13 000

R13 000 x 20% = R2 600 (para 20(1)(b) penalty)

- Note – if the taxpayer had received a penalty in terms of para 27 for late payment of provisional tax, the above penalty must be reduced by para 27 amount (see para 20(2B))

Example:

Para 20(1)(b) penalty = R2 600

Para 27 penalty = R1 000

Therefore, final para 20(1)(b) penalty due by taxpayer = R1 600

- Provisional taxpayers with a taxable income above R1 million

- A penalty, which is deemed to be a percentage based penalty imposed under Chapter 15 of the TAACT; will be equal to 20% of the difference between –

- The amount of normal tax as determined in respect of such estimate, and the amount of normal tax calculated after taking into account any amount of deductible rebates, at the rates applicable in respect of such year of assessment, in respect of a taxable income equal to 80% of such actual taxable income; and

- The amount of employees’ tax and provisional tax paid by the end of that year of assessment. Any retirement fund lump sum benefit, retirement fund lump sum withdrawal benefit or severance benefits received/accrued should be excluded from the penalty calculation.

- A penalty, which is deemed to be a percentage based penalty imposed under Chapter 15 of the TAACT; will be equal to 20% of the difference between –

- Paragraph 20A penalty for failure to submit an estimate of taxable income timeously

- This penalty has been deleted with effect from years of assessment commencing on or after from 1 March 2015

- Paragraph 27 penalty on late payment of Provisional Tax

- A penalty, which is deemed to be percentage-based penalty imposed under Chapter 15 of the TAACT of 10% will be levied on any late payment of Provisional Tax in respect of the first and second periods.

Specific Definitions

- The ‘effective date’ is:

- Where the year of assessment ends on 28/29 February for any taxpayer, 7 months thereafter

- Where the year of assessment ends on 28/29 February, but the Commissioner approved a financial year end on a date other than 28/29 February, six months thereafter

- In any other case, six months after the relevant year of assessment

- The ‘credit amount’ in respect of a provisional taxpayer is the sum of:

- All Provisional Tax payments (1st, 2nd and 3rd) made

- Employees’ Tax paid

- Allowable Foreign Tax credits for the applicable year of assessment.

General Information on Trusts

- Section1 defines a Trust as:

- A trust consists of cash or other assets that are administered and controlled by a person, known as a trustee, who acts in a fiduciary capacity. Such person is appointed in terms of a deed of trust, by agreement or in terms of the will of a deceased person

- A Special Trust is:

- A trust created solely for the benefit of a person who has a disability as defined in 6B(1) of the Act, where such disability incapacitates such person from earning sufficient income to maintain him/herself; or is incapable of managing his/her own financial affairs.

- This Trust will no longer be deemed to be a special trust in respect of years of assessment ending on or after the date on which such person is deceased.

- Where such Trust is created for the benefit of more than one person, all persons for whose benefit the trust is created must be relatives in relation to each other.

- A Trust created in terms of the will of a deceased, solely for the benefit of beneficiaries who are relatives in relation to that deceased person and who are alive or conceived but not yet born on the date of the death of the deceased person, where the youngest of those beneficiaries is on the last day of the year of assessment of that trust under the age of 18 years.

- Trusts (including a special trust that is taxed according to sliding scale applicable to a natural person) do not qualify for interest exemption or personal rebates.

- Trusts are taxed at a flat rate of 45% except for Special Trusts which are taxed according to the tax rates applicable to natural persons. For additional examples of the taxable income calculation for a Trust refer to attached annexures.

- A trust created solely for the benefit of a person who has a disability as defined in 6B(1) of the Act, where such disability incapacitates such person from earning sufficient income to maintain him/herself; or is incapable of managing his/her own financial affairs.

COVID-19 Tax Relief – Provisional Tax

- The COVID-19 Tax Relief is the Government’s tax measure to relieve tax compliant small to medium sized businesses and micro-businesses.

- The COVID-19 Tax Relief is governed according to the Draft Disaster Tax Administration Relief Bill, dated 1 April 2020.

- A qualifying taxpayer is a company, trust, and individual that

- Conducts trade;

- The gross income not exceeding R100 million during the year of assessment starting on or after 1 April 2020 to 31 March 2021;

- The gross income for the year of assessment must not include more than 10 percent of income derived from interest, dividends, foreign dividends, rental from letting fixed property and any remuneration received from an employer;

- A micro business for the purpose of this process, is a micro business as defined in the Sixth Schedule to the Income Tax Act that:

- The qualifying turnover threshold of R1 Million for the year of assessment is applicable, and it must also not include the following:

- In the case of a company, the turnover for the year of assessment must not include more than 20 per cent income derived from annuities, interest, dividends, foreign dividends, rental from letting fixed property, royalties, or income of a similar nature as well as any proceeds derived from the disposal of financial instruments and income from the rendering of a professional service; or

- In the case of a natural person, the turnover for the year of assessment must not include more than 20 per cent income derived from the rendering of a professional service; and any remuneration received from an employer.

- A micro business will not qualify as a micro business if it holds shares or has any interest in the equity of a company barring certain exceptions;

- The qualifying turnover threshold of R1 Million for the year of assessment is applicable, and it must also not include the following:

AND

- A taxpayer as defined in section 151 of TAACT;

- That is tax compliant as referred to in section 256(3) of the TAACT, this means that the taxpayer must be fully tax compliant:

- The taxpayer must be registered for all applicable taxes;

- All tax returns across tax types must have been submitted; and

- No outstanding tax debts

- Unless there is valid payment agreement, approved suspension of payment pending an objection or appeal, or tax debt less than R100.

Deferral of Provisional Tax Payment

- The deferral of the provisional tax payment applies to qualifying taxpayers who are required to submit provisional tax returns for the period starting from 1 April 2020 to 31 March 2021.

- The first provisional tax payment due from 1 April 2020 to 30 September 2020 will be based on the 15 per cent of the estimated total tax liability.

- The second provisional tax payment from 1 April 2020 to 31 March 2021 will be based on the 65 per cent of the estimated total tax liability.

- The remaining 35% of the Provisional Tax liability will be deferred and payable when making the third provisional tax payment.

- Administrative penalties and interest will not be levied on deferred provisional tax liability for the first and second period.

- COVID-19 Tax Relief will not apply to provisional taxpayers failing:

- The tax compliance test;

- The gross income threshold;

- To pay the 15% or the 65% by the relevant due dates.

- Where discovered that the provisional taxpayer did not qualify for the COVID-19 tax relief, the relevant relief will be withdrawn and normal penalties and interest will apply to the provisional account.

- Below are the examples for two companies with different financial year-end (FYEs).

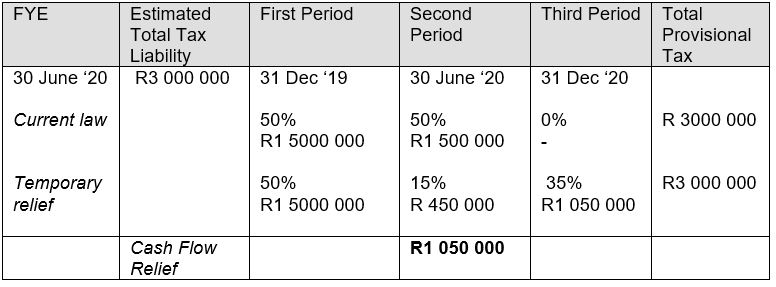

Example 1

- Company A has a financial year-end (FYE) of 30 June 2020. The company’s first Provisional Tax payment of 50 per cent of its estimated total tax liability of R3 million paid by 31 December 2019.

- The company’s second provisional payment will be due on 30 June 2020, which is a period that falls within the COVID-19 tax relief. Instead of a payment of R1,5 million (i.e. 50 per cent of R3 million) R450 000 (15 per cent of R3 million) will be payable, to ensure that the cumulative total of the first and second Provisional Tax payment is 65 per cent of the estimated total tax liability, instead of 100 per cent.

- The COVID-19 Tax Relief will provide the company with a cash flow benefit of R1 050 000 during the temporary relief period. Under normal circumstances, 31 December 2020 would have been the third top-up payment to avoid interest charges. The relief will allow the company to pay the outstanding balance (35 per cent or R10 50 00) by this date.

Company A with 30 June 2020 as a Financial Year End

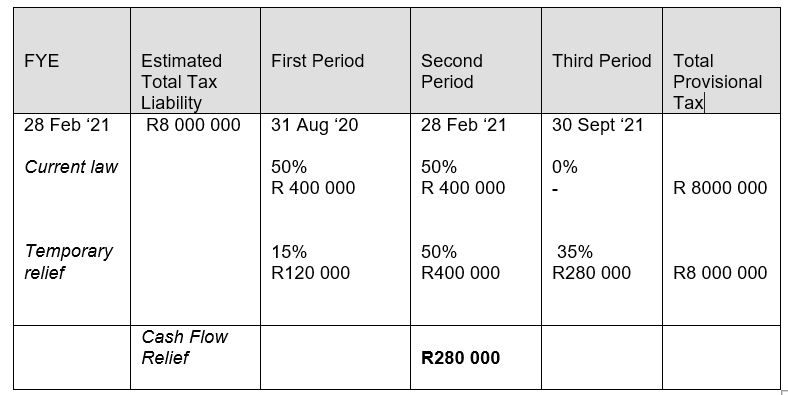

Example 2

- Company B’s financial year-end is 28 February 2021, therefore the first provisional tax payment falls within the temporary relief period.

- The first provisional tax payment is due on 31 August 2020, it amounts to R120 000, which is 15 per cent of the estimated total tax liability of R800 000 for the year. Instead of R400 000, allowing for a COVID-19 temporal relief of R280 000.A further relief measure of only 50 per cent of the estimated tax liability of R400 000 will be due on 28 February 2021.

- The cumulative total tax paid will be 65 per cent of the estimated total tax liability. The remaining balance of R280 000 is 35 per cent of the estimated tax liability is due on 30 September 2021 in order to avoid interest charges.

Company B with 28 February 2021 as a Financial Year End

Deferral of Interim Payment

- Qualifying micro businesses for the period starting from 1 April 2020 to 30 September 2020, with respect to the interim payments due and payable according to paragraph 11 of the Sixth Schedule to the Income Tax Act, pay 15 percent instead of 50 per cent of the amount of tax due.

- For the period commencing on 1 April 2020 to 28 February 2021 with respect to the interim payment payable in terms of paragraph 11(4) of the Sixth Schedule, pay 65 per cent instead of paying the calculated amount of tax in terms of this paragraph less the amount paid in terms of paragraph 11(1) of the Sixth Schedule

- Interim payment deferred are due and payable by micro businesses by the due date specified in a notice of assessment.

- The penalty relief applies to deferred interim payments according paragraph 11(6) of the Sixth Schedule, and interest will not be levied under paragraphs 11(3) and (5) on deferred interim payments that are payable on assessment.

- Refer to the SARS website (www.sars.gov.za) for further information.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.