Summary

This webpage provides guidelines regarding the completion of the Withholding Tax on Royalties return (WTR01), how to make payment on eFiling and apply for a refund using the Rev16 form.

- Please note that any reference to a section in this webpage, unless otherwise specified, refers to a section of the Income Tax Act No. 58 of 1962 (the Act).

- Where reference is made to an Act other than the Income Tax Act, it will be specified.

- Any reference to a paragraph in this webpage, unless otherwise specified, refers to the Section 49A to 49H to the Act and must be read in conjunction with Interpretation Note 116 on Withholding Tax on Royalties.

Introduction

Sections 49A-49H of the Income Tax Act of 1962 was introduced to deal with Withholding Tax on Royalties. It is common practice for a country to subject payments made to a foreign person (non-resident) to a withholding tax, such taxes are payable to SARS by the South African resident who pays the amount on behalf of the non-resident.

A “foreign person /non-resident” is defined in section 49A as “any person that is not a resident” in that country and it includes a natural person, a deceased estate, an insolvent estate, a company, and a trust.

A “royalty” is defined as “any amount that is received or accrues in respect of the:

- Use or right of use of or permission to use any intellectual property as defined in section 23I; or

- Imparting of or the undertaking to impart any scientific, technical, industrial or commercial knowledge or information, or the rendering of or the undertaking to render any assistance or service in connection with the application or utilisation of such knowledge or information”.

Any person making payment of any amount of royalties to or for the benefit of a foreign person must withhold an amount of Withholding Tax on Royalties from that payment.

Royalties paid or which became due and payable on or after 1 July 2013 but before 1 January 2015 attracted a withholding rate of 12% of the amount of royalties paid.

For all royalties paid or which become due and payable on or after 1 January 2015, the Withholding Tax is calculated at a rate of 15% of the amount of royalties paid.

Exemption / Reduced Rates for Withholding Tax on Royalties

A Withholding Tax on Royalties Declaration form (WTRD) must be completed by the foreign person and be submitted to the withholding agent before an exemption, or a reduced rate may be applied in the calculation of the Withholding Tax on Royalty amount to be paid.

A foreign person is exempted from Withholding Tax on Royalties if:

- That foreign person is a natural person who was physically present in the Republic for a period exceeding 183 days in aggregate during the twelve-month period preceding the date on which the royalty is paid; or

- The property in respect of which that royalty is paid is effectively connected with a permanent establishment of that foreign person in the Republic if that foreign person is registered as a taxpayer in terms of Chapter 3 of the Tax Administration Act; or

- That royalty is paid by a headquarter company in respect of the granting of the use or right of use of or permission to use intellectual property as defined in section 23I to which section 31 does not apply because of the exclusions contained in section 31 (5) (c) or (d).

The foreign person could qualify for a reduced rate of tax in terms of an Agreement for the Avoidance of Double Taxation (DTA) and Prevention of Fiscal Evasion between South Africa and the country of residence of the foreign person.

- A summary of the rates, the relevant provisions relating thereto and the full text of these Double Taxation Agreements & Protocols are available on the SARS website.

- Withholding Tax on Royalties – Summary of DTA Rates – Africa.

- Withholding Tax on Royalties – Summary of DTA Rates – Rest of the World.

Withholding Tax on Royalties Return (WTR01)

The client can obtain the Withholding Tax on Royalties (WTR01) form and/or REV16 form via the following channels:

- Accessing the SARS website.

- Visiting any SARS branch; or

- Call the SARS Contact Centre on 0800 00 SARS (7277).

The client when using the SARS website must:

- Click on the form/return.

- Complete the required information; and

- Print the form/return.

Clients can submit Withholding Tax on Royalties Return (WTR01), proof of payment and/or REV16 form:

- Withholding Tax on Royalties (WTR01) declaration forms together with the supporting documents may be submitted on the SARS Online Query System (SOQS), accessible on the website.

- Clients that are not large business, email to [email protected] (for individual taxpayers) or [email protected] (for Tax Practitioners)

- Clients dealing with Large Business or High Net Wealth Individual Taxpayer Segments, who prefer the email channel may use the relevant mailbox to make submissions.

- Visiting a SARS branch

Note: The taxpayer is not required to submit the WTRD to SARS. The receiver of the royalty will submit the WTRD to the withholding agent. Should the taxpayer be audited and there is a need to review the WTRD, it will be done by issuing a letter requesting such.

Completion of the Withholding Tax on Royalties Return (WTR01)

Royalty Payment Made To or For the Benefit of a Foreign Person

- Enter the “Period” (YYYY/MM) when the royalty was paid.

- Select the applicable entity type that made payment(s) from the below:

- Company/Close Corporation

- Trust

- Individual/Sole Property

- Other

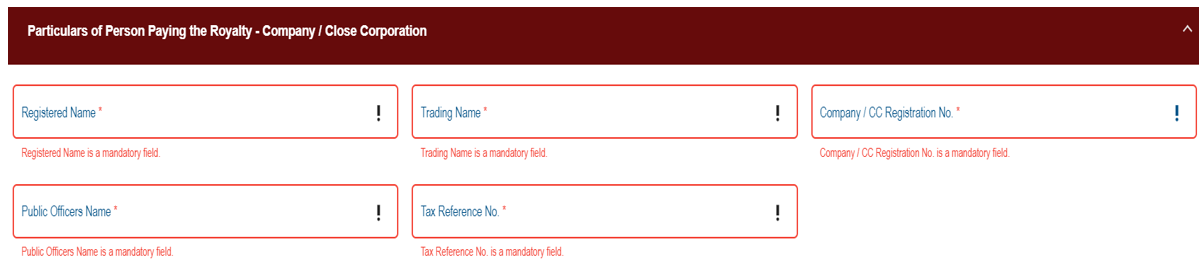

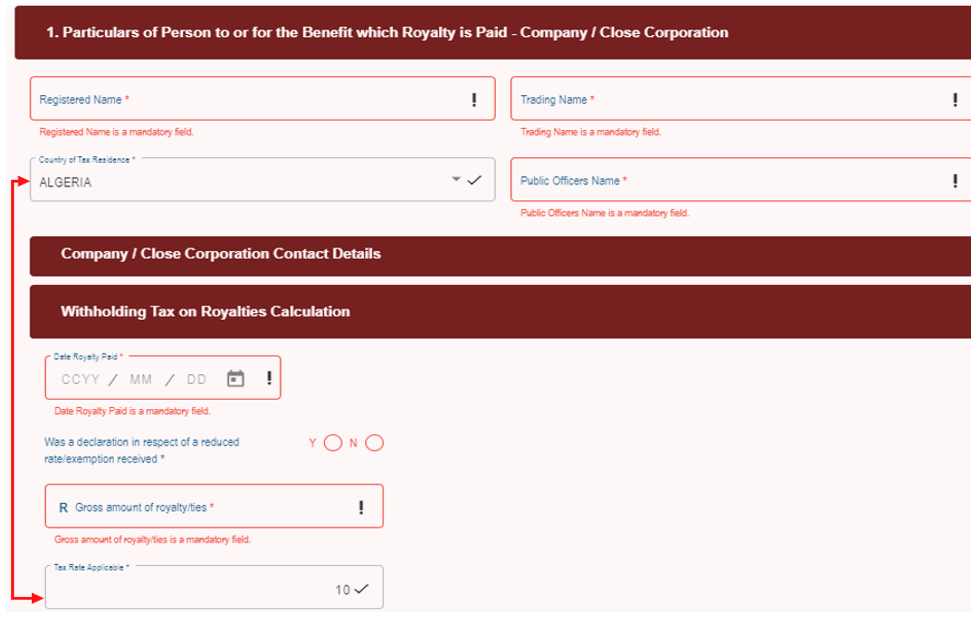

Particulars of the Person paying Royalty

- Company/Close Corporation/Trust /Other

- Complete the following mandatory details:

- Registered Name

- Trading Name

- Other Registration No. (applicable to “Other” entity only)

- Company/CC Registration No./Trust Registration No.

- Public Officer’s Name

- Tax Reference No.

- Complete the following mandatory details:

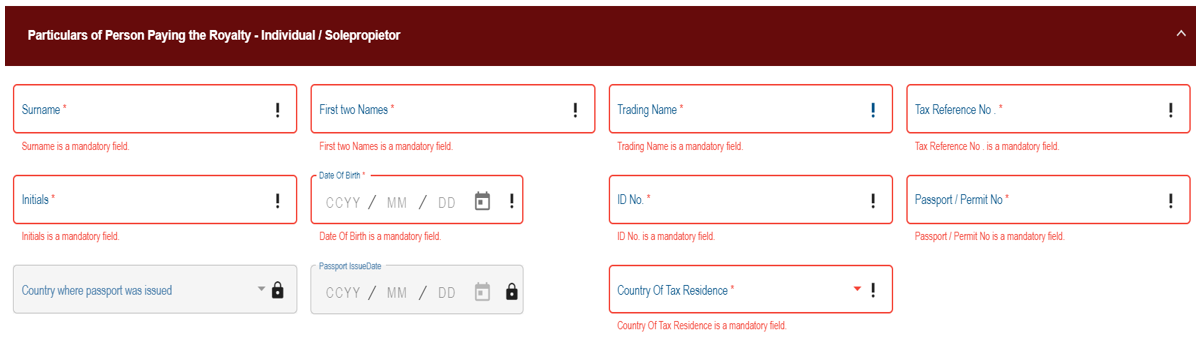

- Individual/Sole Propiertor

- Complete the following details:

- Surname;

- First two names;

- Trading Name;

- Tax Reference No;

- Initials;

- Date of Birth (CCYYMMDD);

- ID No;

- Passport/Permit No;

- Select the country where passport was issued from the dropdown list;

- Passport issue date (CCYYMMDD);

- Country of Tax Residence (e.g. South Africa = ZAF);

- Complete the following details:

Contact Details

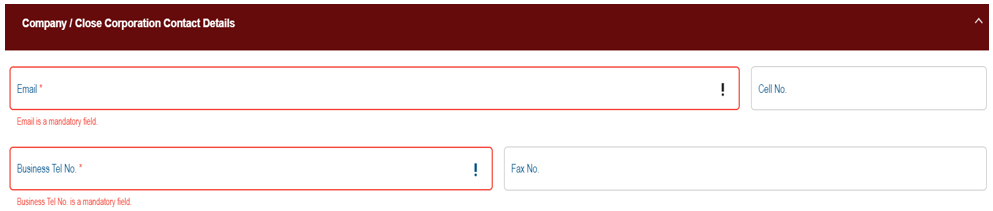

- Company/Close Corporation/Trust /Individual/Sole Proprietor/Other

- Complete the mandatory contact details which have a red border outline:

- email address

- Business Tel No.

- Cell No.

- Fax No.

- Complete the mandatory contact details which have a red border outline:

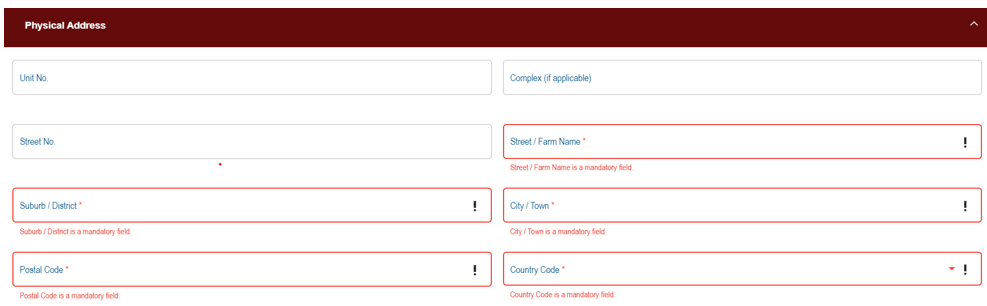

Physical Address

- Company/Close Corporation/Trust Contact Details/Individual/Sole Proprietor/Other

- The physical address is an address where an individual resides. In a case of the business, the details of the premises where the business is trading from must be completed.

- Complete the details. If the business is trading from a flat or townhouse unit, the number must be inserted. The name of the block or the block of flats or townhouse complex must be inserted in ‘complex’. Where the business does not trade from a flat, townhouse or complex these fields are left blank:

- Unit No.

- Complex (If applicable)

- Street No.

- Street/Farm Name;

- Suburb/District;

- City/Town;

- Postal Code; and

- Country code.

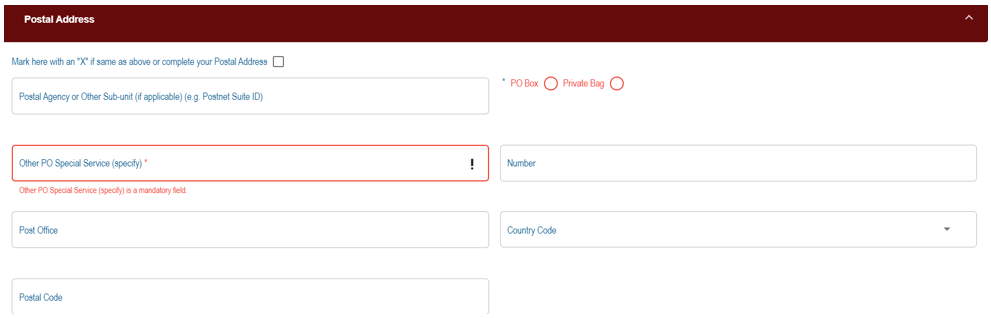

Postal Address

- Company/Close Corporation/Trust Contact Details/Individual/Sole Proprietor/Other

- This address is used by the business or individual to receive post. It may be the same as its business address or physical address above or it may be a post box number or other address. If it is the same as the physical address simply, mark the relevant box with an “X”.

- If the answer is ‘No’, the following fields will display as open and editable:

- Postal Agency or Other Sub-unit (if applicable) (e.g. Postnet Suite ID)

- PO Box: Indicate on applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’.

- Private Bag: Indicate on the applicable tick box if the postal address is ‘P.O. Box’ or ‘Private Bag’.

- Other PO Special Service (specify);

- Number;

- Post Office;

- Postal Code;

- Country Code;

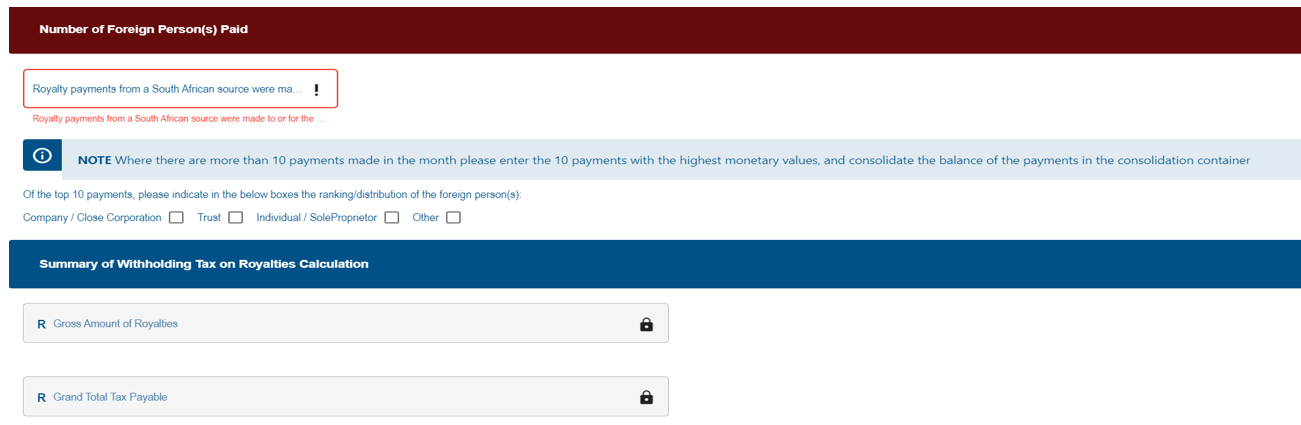

Number Of Foreign Person(s) Paid

- Enter the number of royalty payments from a South African source that were made to or for the benefit of how many foreign person(s).

- Select the applicable entity(ies) “Company/Close Corporation/ Trust/ Individual/Sole Proprietor/Other”. who made the payment(s).

- The maximum number of payments that can be detailed on a return form is limited to 10. Where there are more than 10 payments, the taxpayer should provide the details of the 10 highest payments and the corresponding entities.

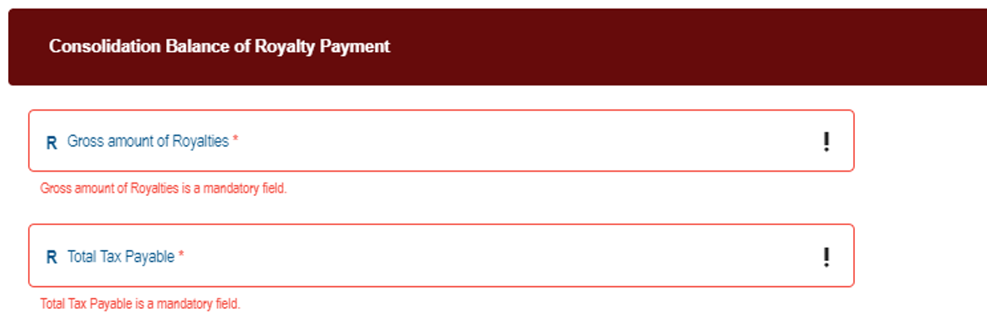

- In instances where more than 10 payments were made, the taxpayer should consolidate the balance of the transactions in the “Consolidation” container indicating the “Gross Amount of Royalties” and “Total Tax Payable”.

- Where there are more than 10 payments and the taxpayer does not wish to utilise the “Consolidation” container, they may submit the balance of the transactions on a separate WTR01 return form.

- The form has been designed to assist taxpayers by prepopulating known DTA rates for the selected “Country of Tax Residence”, however if the rate has changed or not applicable, the taxpayer can over-ride the pre-populated rate. Where there is no signed or valid WTRD, the rate of 15% should be used.

- As much as SARS tries to maintain the list of DTA rates per country, the onus is on the taxpayer to ensure that they use the correct rate.

Declaration

- After all the information fields have been completed, sign and date the completed return.

The Payment of the Withholding Tax on Royalties

The Currency Payments Made to The Commissioner

- If an amount withheld by a person is denominated in any currency other than the currency of the Republic, so withheld must, for the purposes of determining the amount to be paid to the Commissioner, translate the amount to the currency of the Republic at the spot rate on the date on which the amount was so withheld.

How to Make a Payment

- The eFiling payment method are available for the payment of the withholding tax on royalties:

- A payment cannot be made unless the entity is activated for WTR on eFiling.

- When a taxpayer creates a WTR payment request in eFiling, it will systematically generate a payment request transaction on the taxpayer’s online banking. The payment will need to be authorised by the taxpayer directly on the relevant online banking system.

- If you don’t have an eFiling profile account and/or you forgot your login details:

- For further assistance about eFiling registration, please refer to the “How to register, manage users and change user password on eFiling” which is available on the SARS website www.sars.gov.za.

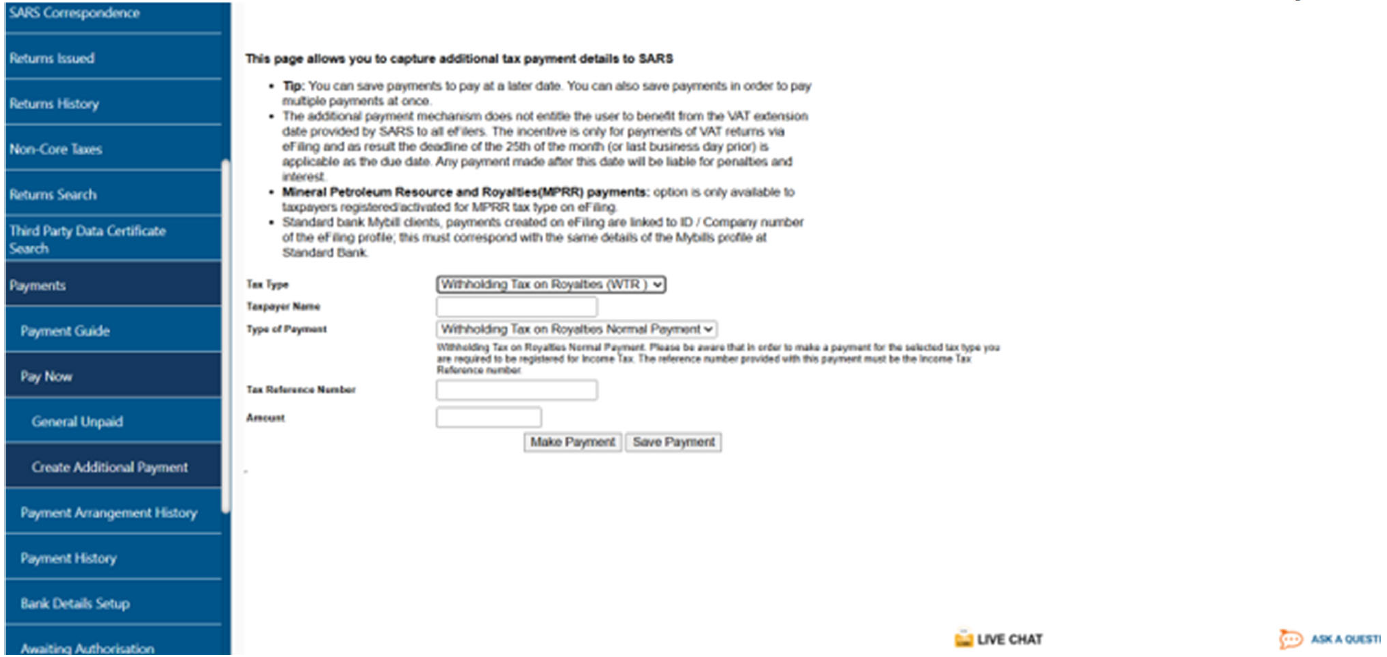

Making Payments via eFiling

- Continue to use ONLY eFiling process for making WTR payments.

- Log onto eFiling;

- Use the ‘Additional Payments’ tab; and

- Click on the ‘Create Additional Payment’ tab;

- On the “Tax Type”, click on the drop-down arrow and the tax types will be displayed.

- Select “Withholding Tax on Royalties (WTR)” on the drop-down arrow.

- Capture details as requested.

- Complete the WTR amount declared as per the WTR01 return.

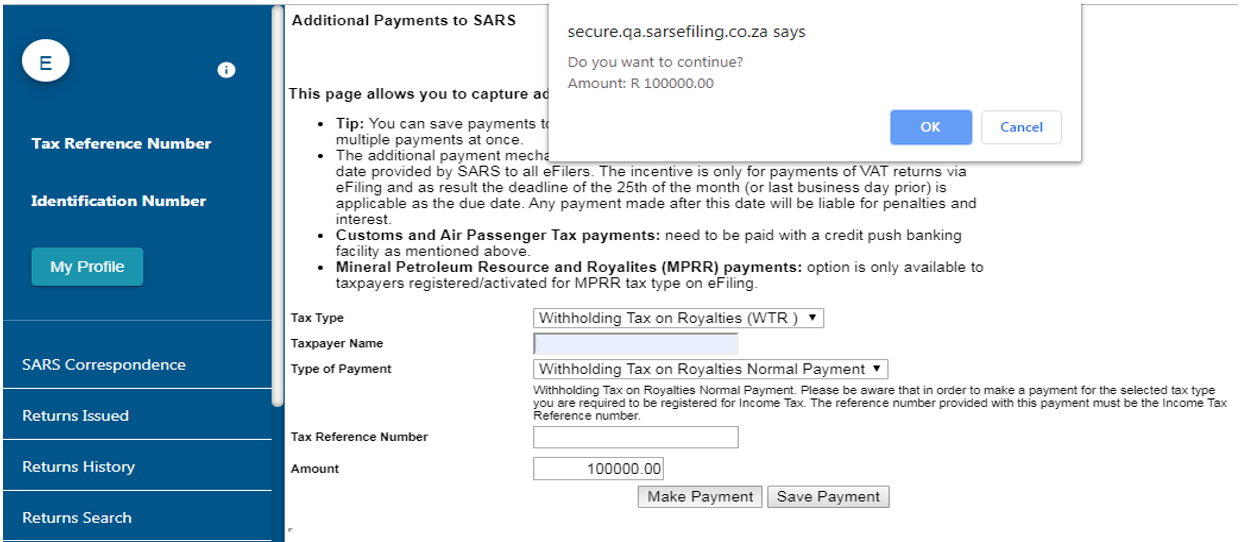

- Click on “Make Payment” button.

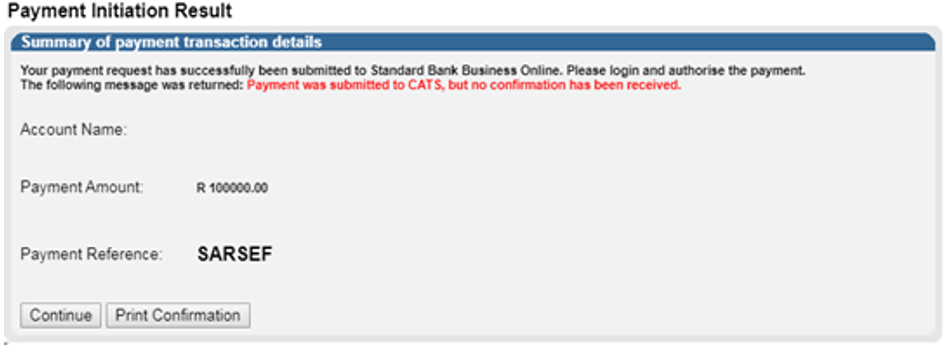

- Click “Ok” button from the displayed message confirming the payment amount to log onto banking online function and release the payment request from eFiling.

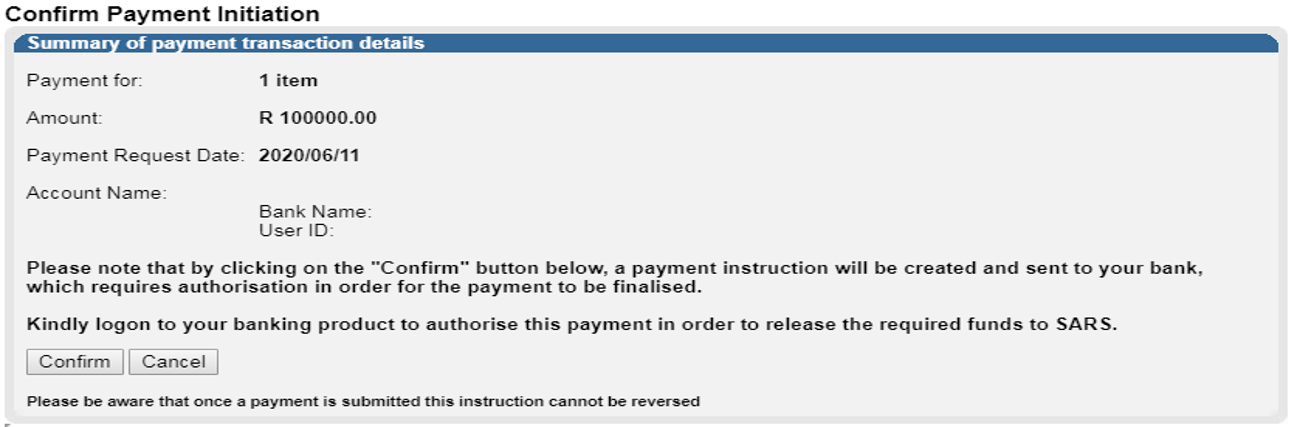

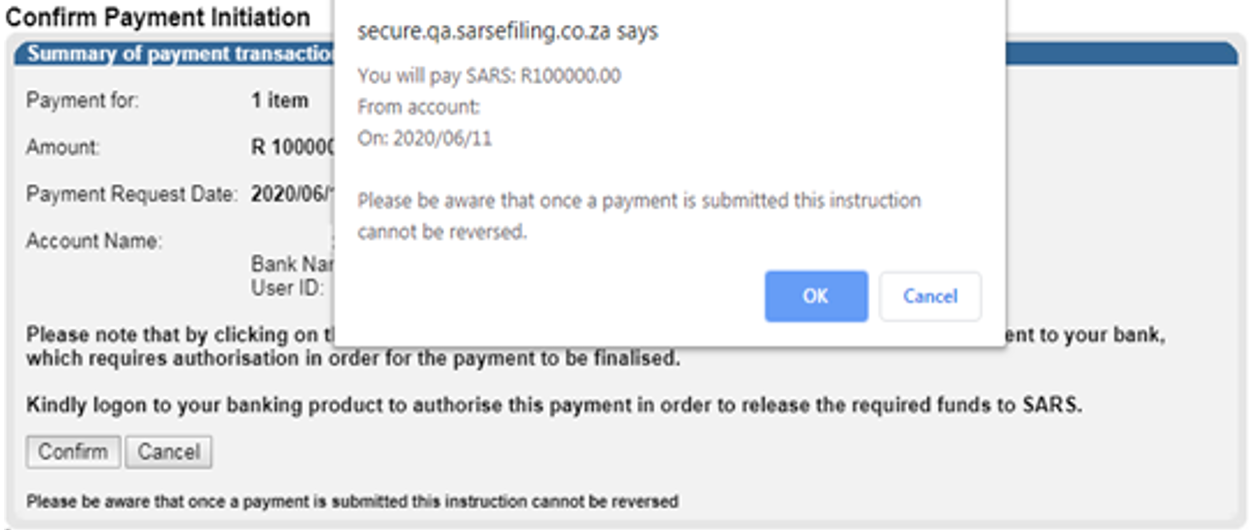

- Click “Confirm” button and a message “Please be aware that once a payment is submitted this instruction cannot be reversed” will display Click “OK”.

- Click on “Confirm” button and the following screen will display:

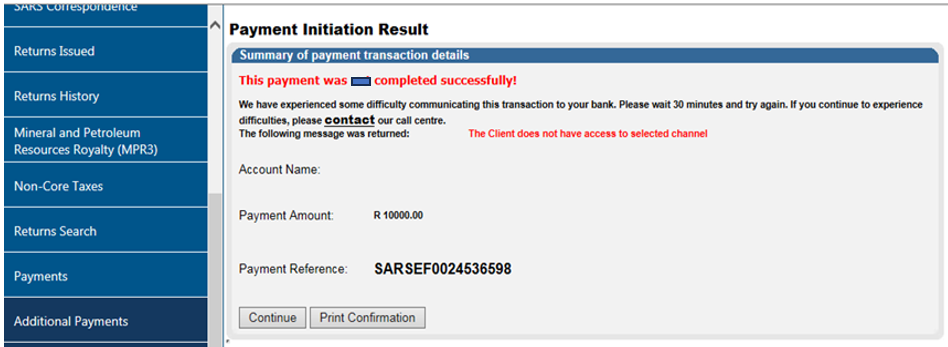

- Click “Continue “button and the following screen will display:

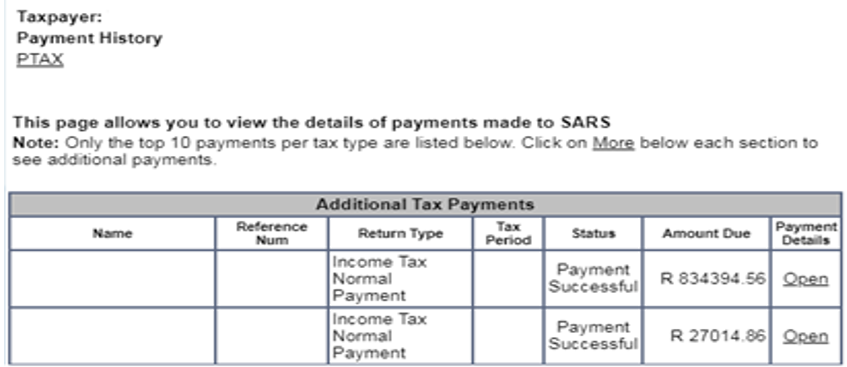

- Click “Continue” button when you need to view the payment history. The following screen will display:

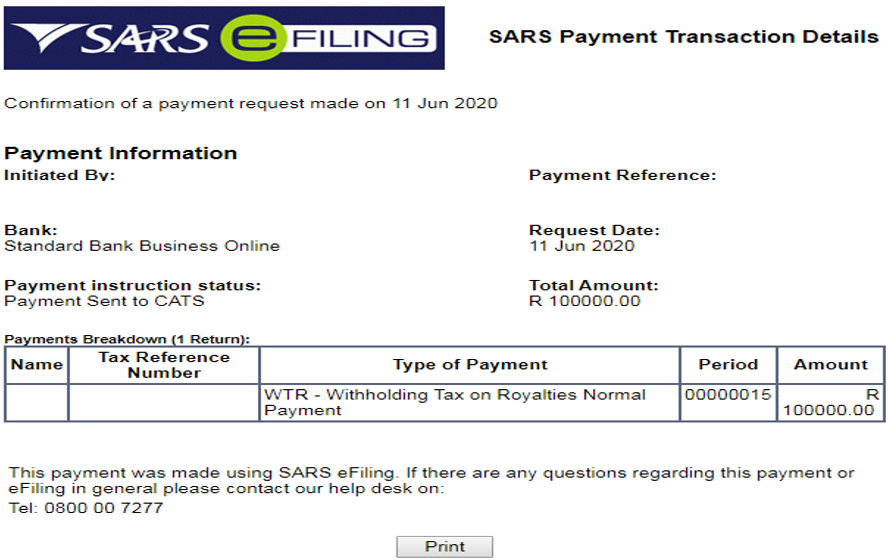

- Click “Print Confirmation” button to keep the receipts.

- If the last day for payment falls on a public holiday or weekend, the payment must be made on the last working day prior to the public holiday or weekend. For more details, refer to the SARS website www.sars.gov.za

- For detailed information on payments, refer to the “External Guide South African Revenue Payment Rules”.

The Refund for Withholding Tax on Royalties

- A withholding agent can claim refund of Withholding Tax under specified circumstances –

- The amount of Withholding Tax that is in excess of the amount that the foreign person would have paid had the declaration form been submitted is refundable to the foreign person if –

- An amount is withheld as required by section 49E(1);

- The declaration form referred to in section 49E(2) or (3) is not submitted to the person paying the royalty by the required date; and

- The declaration form is submitted to the Commissioner within three years after the royalty to which the declaration relates is paid.

- The amount of Withholding Tax that is in excess of the amount that the foreign person would have paid had the declaration form been submitted is refundable to the foreign person if –

- The refund procedure in section 49G takes precedence over the refund procedures in Chapter 13 of the TAAct.

- When a foreign person fails to submit the declaration form by the required date will have to pay the full rate of withholding tax on the royalties received or accrued.

- The withholding agent must complete a REV16 form for refund claims and submit it together with the tax declaration form (WTR01) and power of attorney to SARS.

- SARS will consider the claim and process it accordingly:

- The amount of any refund will usually be paid to the withholding agent and not directly to the recipient of the royalty.

- It is, however, possible for SARS to effect a refund directly to the foreign person, either by transferring the amount into the foreign person’s South African bank account (if available).

Completion of REV16 Form

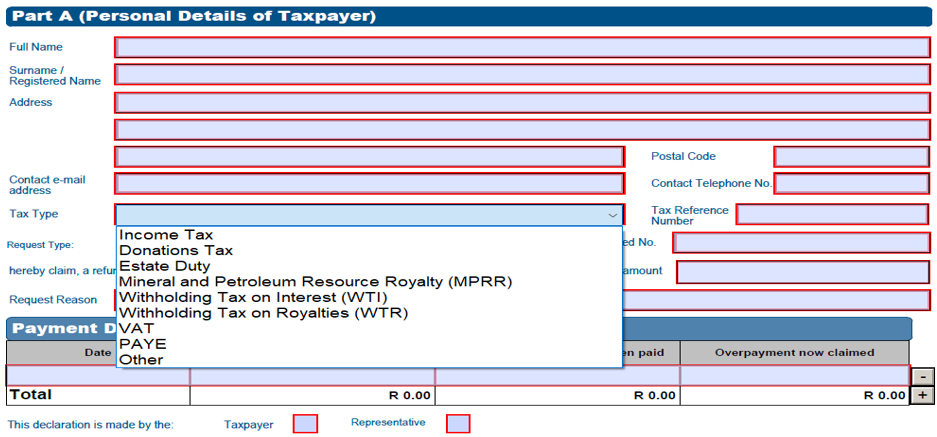

Part A: Claimant

Complete the following fields by the Claimant:

- Full Name(s);

- Surname / Registered Name

- Address

- Contact e-mail address

- Postal address

- Contact Telephone No.

- Tax Type: Select “Withholding Tax on Royalties” from the drop-down arrow.

- Tax Reference Number.

- Identity/Passport/Registered No.

- Select the “Request Type” from the following options:

- Refund

- Transfer to another tax account

- Enter a refund amount you want to claim and/or the amount of credit you want transferred.

- Enter the reason for the refund amount and/or the amount of credit you want transferred.

Complete the following Payment details:

- Date;

- Amount;

- Amount that which should have been paid;

- Overpayment now claimed;

- Mark the following tick boxes to indicate who made a declaration:

- Taxpayer

- Representative

Signature of taxpayer or authorised representative

- Date (CCYY-MM-DD)

- Signature

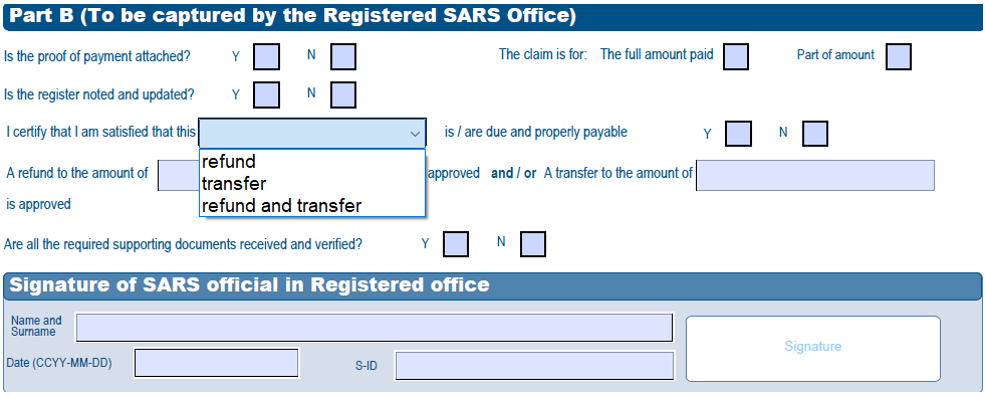

Part B: SARS Official at SARS Office

The SARS Official completes the following fields (indicate the applicable option with “x”.

- The original receipt.

- The claim is for:

- the full amount; or

- part of the amount and the receipts has been endorsed.

- Note and update the register

- Declaration that the request is for “refund/transfer/refund and transfer” and that it is due and properly payable.

- Indicate the approved /transferred refund amount.

- Indicate the reception and verification of supporting documents.

- The claim is for:

Signature of a SARS official in a Registered office

- Name and Surname

- Date (CCYY-MM-DD)

- S-ID

- Signature

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.