Summary

The purpose of this webpage is to assist the representative taxpayers of a trust with the completion and submission of the Income Tax Return for trust (ITR12T) via SARS eFiling. The webpage is structured as follows; the eFiling Channel is described, elaborating how to register and login to eFiling. The webpage explains the functions embedded in the system and how they can be used for submission purposes. This webpage must be read in conjunction with the following External Guide: Comprehensive Guide to the ITR12T Return for trust for detailed information on how to complete the ITR12T return.

The most common reasons for creating a trust are:

- To protect assets for minor children or disabled relatives;

- For Estate planning purposes; and

- As a mechanism to protect assets from creditors.

A trust is created by a founder, and is governed by a trust deed, which stipulates, inter alia the beneficiaries, the trustees, and the terms of the deed. It is formed in various ways based on the nature and type of the trust. The nature of a trust may differ in one of the following ways:

- In their method of formation namely, during the lifetime of a person or upon his death under a will.

- In the rights, they confer on beneficiaries. Under a vesting trust, the beneficiaries have a vested right to the income and/or capital of the trust. Under a discretionary trust, the trustees have the discretion as to whether and how much of the income or capital of the trust to distribute to the beneficiaries.

- In their purpose, namely trading trust, asset protection trust, charitable trust, or special trust. Two types of special trust exist for income tax purposes:

- A (Type A) trust is created for the benefit of a person with a disability.

- A (Type B) trust is created under the will of a person for the benefit of his relatives.

Trusts are taxed in terms of section 2(1) of the Rates and Monetary Amounts and Amendment of Revenue Laws Act 2013. This is with the exception of a “Special trust” which is defined in section 2(1) of the Act. As from 1 March 2017, trusts other than Special trusts are taxed at a rate of 45%. Revenue generated from a trust can either be retained, distributed to the beneficiaries or profits can be deemed to have been received by another person in terms of section 7 of the Income Tax Act. This income becomes taxable in the hands of the person who receives it. The tax implications of the trust and beneficiaries are based on section 25B and section 7 of the Income Tax Act. With reference to the Conduit Pipe Principle, revenue distributed from a trust retains its identity unless (under some circumstances) it is regarded as an annuity.

The source and nature of the income, the method of transfer of the assets to the trust as well as the status of all the relevant parties have an impact on the tax implications in respect of the receipts or accruals of income by the trustees. This revenue and additional required information must be recorded accurately on the trust (ITR12T) return and submitted to SARS.

A trust fund consists of cash or other assets which are administrated and controlled by a person acting in a fiduciary capacity of trust, where such person is appointed under a deed of trust, by agreement or under the will of a deceased person.

SARS values your contribution as taxpayers and your readiness in fulfilling your tax responsibilities, thus we are constantly enhancing our processes to ensure that the tax systems are functioning optimally and effectively so you can be confident in the process. Being able to complete and submit your trust return via eFiling is one such improvement and this webpage will assist you.

Benefits of using eFiling

- eFilers are given more time to make their submissions.

- Tax representatives can save the ITR12T form and submit it later, which will give them more time to review the information to be submitted to SARS.

- eFilers have a full history of all submissions, payments, and electronic correspondence available at a click of a button.

- The system allows a tax representative to view the history of submissions made of the ITR12T form on the system for their convenience.

- eFilers can receive SMS and email notifications to remind them when submissions are due.

- SMS and email notifications assist the tax representatives in the submission process by ensuring that the returns are submitted before the due date.

- The simplified submission of the trust return process results in fewer errors and creates a quicker processing cycle for individuals and business.

- There are embedded functions within the ITR12T return such as pre-populating fields, pop up warning messages when incorrect information is completed and the simplified navigation. These functions will result in few errors during your return process.

- eFilers can use the tax calculator function to receive a pre-assessment of their ITR12T submission before an original assessment is done.

- Tax representatives can access a pre – ITA34T before an original assessment is sent to assist them in determining accuracy of the information, which will be submitted to SARS.

Registration, Update Profile and Requesting ITR12T on eFiling

Overview

As described in the previous section, to access eFiling you must be registered as a tax representative/ tax practitioner and responsible for the submission of a specified trust on the system. This section will take you through the registration process, how to activate a trust on the system and further illustrate how to update your profile on eFiIing. Screenshots are applied to demonstrate the use of the system.

Job Access with Speech (JAWS) forms are accessible for visually impaired taxpayers and will be implemented on all returns as part of SARS’ strategy.

How to Register for the use of eFiling

- Navigate the website www.sars.gov.za, click ‘Register’ and follow the steps stipulated to complete the registration process.

- For further assistance with eFiling registration, refer to the “How to register for eFiling and Manage your user Profile” available on the SARS website.

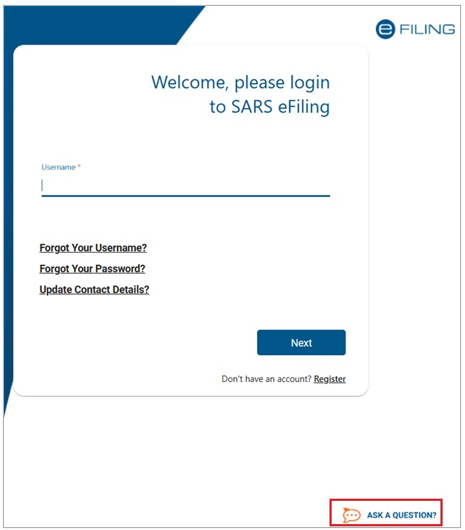

- Once registered, click on “Login”, enter your username, click “Next” to proceed and enter your password. Click “Login” to proceed to log into your eFiling profile.

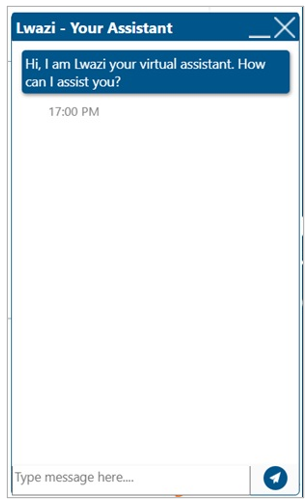

- SARS eFiling provide a chatbot, Lwazi, by selecting the “Ask A Question” tab to provide an instant support experience and automated answers to general queries.

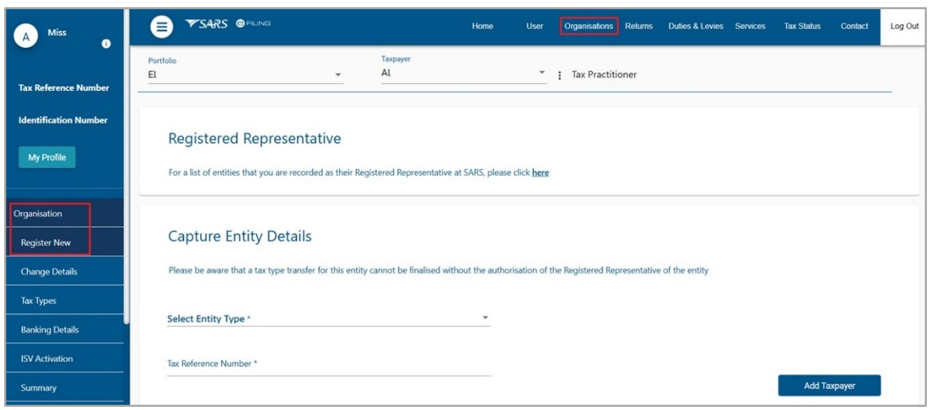

How to add a new Trust to the eFiling Profile

- Once you are successfully registered and successfully logged into your eFiling profile, proceed to activate the trust before you are allowed to request and submit an ITR12T return. The below section will demonstrate how to activate a trust on eFiling.

- Select “Organisations” on the left menu and then select “Register New”.

- The following screen will be displayed to the taxpayer to enable the capturing of ‘Entity Details’.

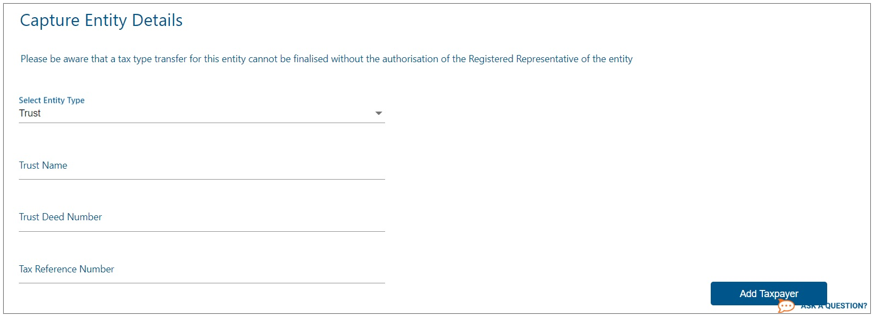

- Complete all the required information.

- Once all the fields have been completed, click the “Add Taxpayer” button to proceed.

How to activate a registered Trust

- To activate a registered trust, proceed as follows:

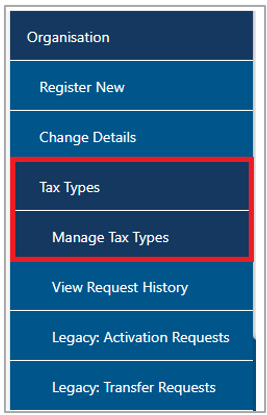

- Of the options below “Organisation” which are displayed on the left menu, click on “Tax Types” and “Manage Tax Types”.

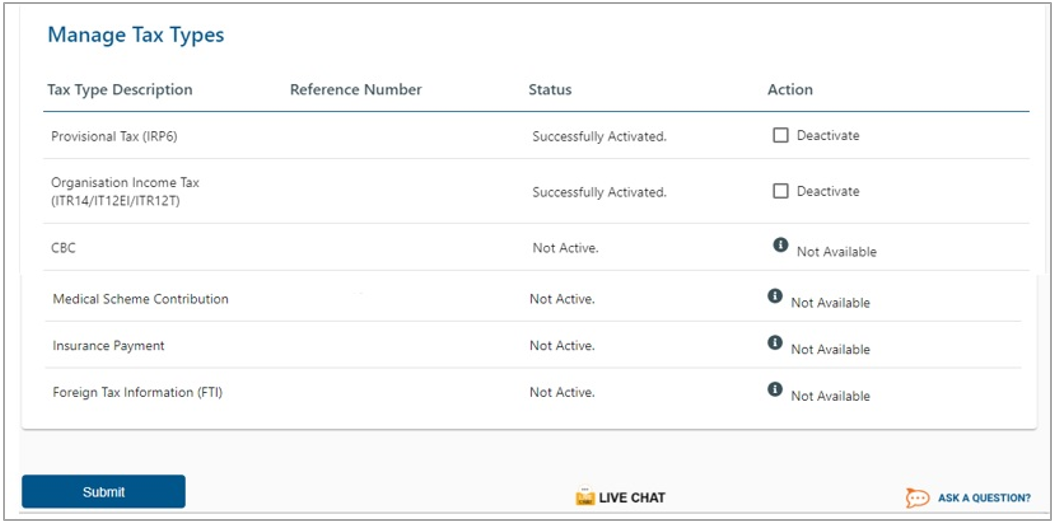

- Select the action tick box next to the relevant tax product to activate the tax type and click the “Submit” button to proceed. Below is an example of how the screen looks.

How to update user rights on eFiling

- This section will illustrate how to identify those who have access to the Trust submission and further verify whether the trust has been successfully registered.

- Click on “Right Groups” from the left side menu options.

- Select “Manage Groups”.

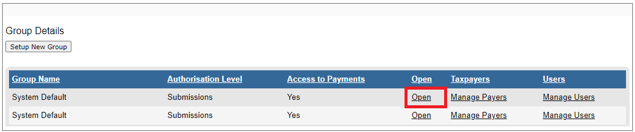

- The “Group Details” screen will be displayed. Click on the “Open” hyperlink to proceed.

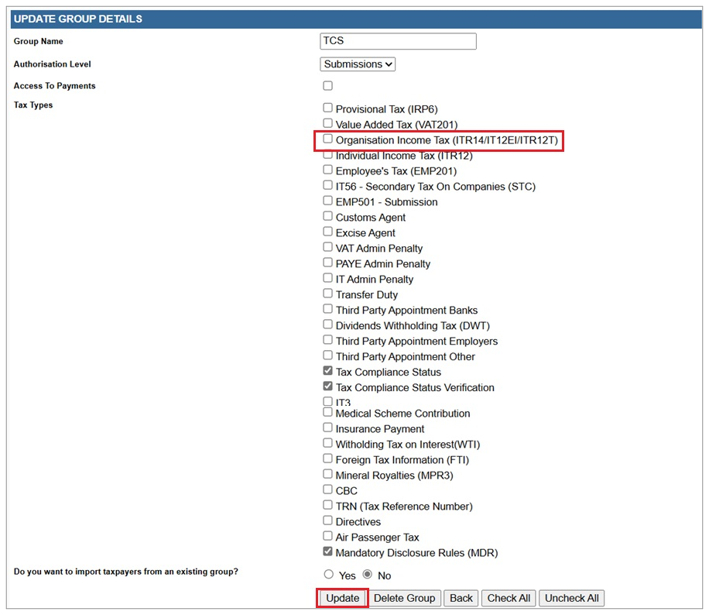

- The “Update Group Details” screen will be displayed.

- Select the tax type (Organisation Income Tax ITR14/IT12EI/ITR12T) by checking the appropriate tick box. Click “Update” to submit.

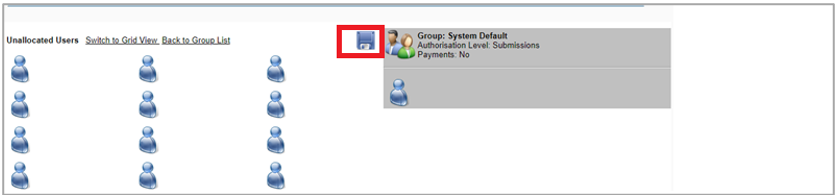

How to manage users

- To manage those in the group who have access to the Trusts submission proceed as follows:

- Click on “Right Groups” from the left side menu options.

- Select “Manage Groups” and the “Group Details” screen will be displayed.

- Select the hyperlink “Manage Users”.

- Ensure that the login name that you are logged in with is in the grey box on the right-hand side. To add users, drag and drop the users in the grey box and click on the save button (floppy disk icon) to save the required changes.

How to Request an ITR12T Return

Once you have registered and activated the trust, you should be able to access the return. This section will assist you in accessing the return via eFiling.

Requesting your ITR12T before Official Filing Season Phase

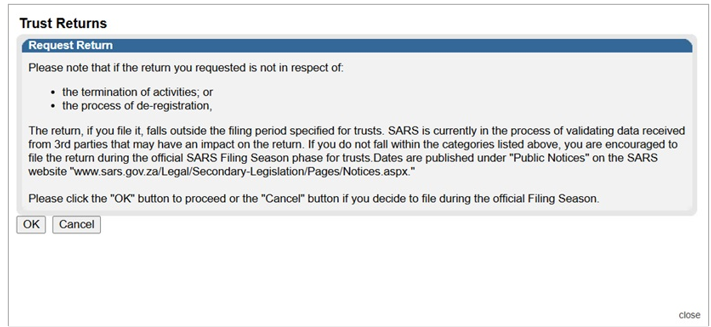

- Taxpayers /Tax practitioners are encouraged to file their return during the official Filing season phase for a trust. The filing dates are published under “Public Notices” on the SARS website.

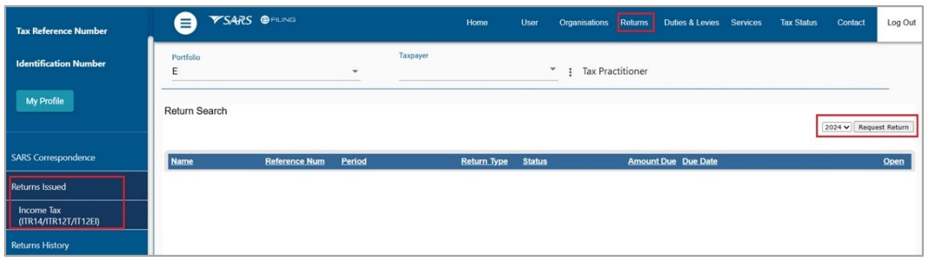

- Click on “Returns” and “Returns issued” displayed on the menu options.

- Select “Income Tax (ITR14/ITR12T/ITR12EI)” displayed as one of the categories of the left side menu option “Returns Issued”.

- When 2026 Tax year is selected, the following message will be displayed to confirm the termination of the trust services, which is in the process of being deregistered. Click “OK” to terminate the trust and alternatively click “Cancel” to go back to the “Request Return” page.

- Note that a similar message will be displayed when you request a return for Exempt Institutions that are registered as trusts prior to the Filing season period.

- Select the appropriate period of submission from the drop-down list displayed on the right side of the screen. Click the “Request Return” button and the “Returns Search” screen will be displayed indicating the return issued.

- Click the “Open” hyperlink and the “Income Tax Work Page” will be displayed.

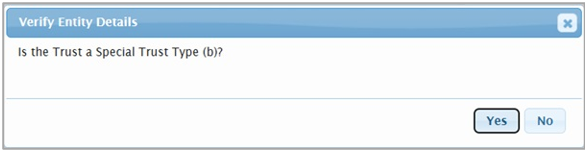

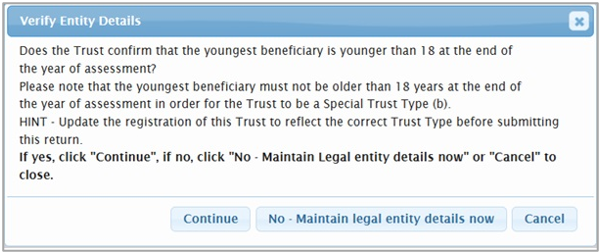

- A verification message will be displayed to confirm if the trust is special Type (b), as indicated below.

- If “Yes” is selected, the following subsequent pop up will be displayed for the user to confirm if the youngest trust beneficiary is still under the age of 18:

- If the youngest beneficiary is younger than 18 years at the end of the year of assessment, click “Continue” to proceed.

- If the youngest beneficiary is not younger than 18 years, click “No – Maintain legal entity details now” and proceed to complete the RAV01.

- Click “Cancel” to close the message to continue with the completion of the ITR12T return.

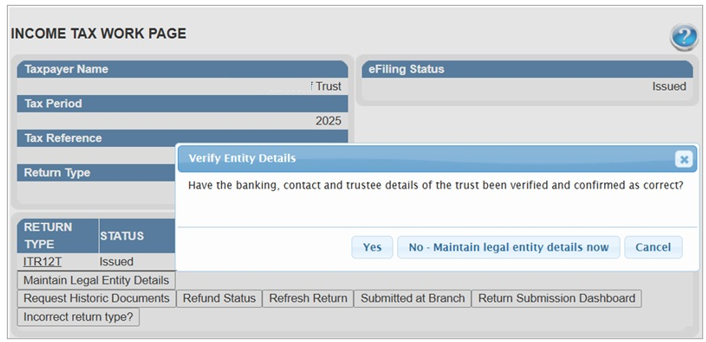

- If “NO” is selected to the question “Is the Trust a Special Trust Type (b)?”, the “Verify Entity Details” message will be displayed as indicated below.

- A verification message will be displayed to verify the banking, contact and trustee details.

- If all the information is the same as the previous year, click “Yes” or “Cancel” to close the message.

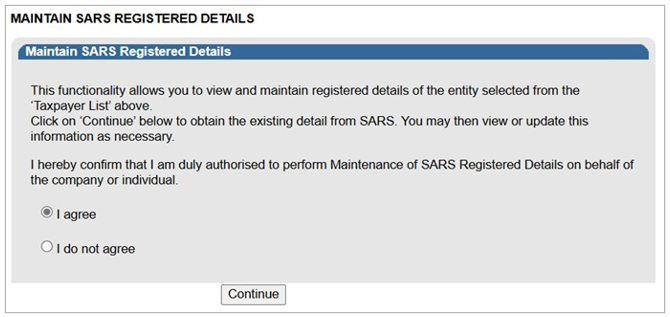

- Click on “No – Maintain Legal Entity Details now”, to verify and update any outdated legal entity information of the trust representative i.e., contact details, physical address, postal address, banking details and other particulars. The “Maintain SARS Registered Details” will be displayed.

- When the option “I do not agree” is selected, the “Continue” button will be greyed out and the return will not open for the maintenance of SARS registered details. When “I agree” is selected, the trust representative is duly authorised to perform Maintenance of SARS Registered Details on behalf of the company or individual.

- Refer to the external guide “How to complete the Registration amendments and Verification Form (RAV01)” for detailed information on how to confirm and verify the applicable company details. The guide can be accessed on www.sars.gov.za.

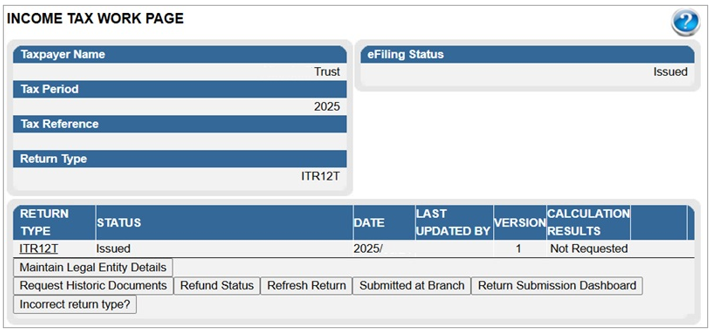

- You will be directed to the Income Tax Work Page and the following buttons will be displayed:

- Maintain Legal Entity Details – this will redirect you to the Legal Entity Registration function.

- Request Historic Documents – historic Notice of Assessments and Statements of Account may be requested by selecting this button.

- Refund Status – You will be able to check the refund status of the assessment if a refund is due to you.

- Refresh Return – this will request new pre-population of the return.

- Submitted at Branch – by selecting this button, eFiling will be updated to indicate that the return has been submitted through another channel, e.g., at a SARS Branch.

- Return Submission Dashboard – you will be presented with the return submission dashboard.

- Incorrect return type? – You will have the ability to change the return type if it is incorrect.

- Click on the “ITR12T” hyperlink to open the return for completion.

Step by Step Demonstration on the Completion and Submission of the ITR12T Return

Overview

This section will demonstrate how to complete and submit the ITR12T return by displaying step by step screen shots, which describe the process of submission and further highlight the details an eFiler should take into consideration whilst completing the return. Functions which may be used are also discussed and demonstrated for the ease and usage of eFiling.

Estimated Assessments

Once the filing period for trusts ends, SARS may raise original estimated assessments on Income Tax Returns for trusts (ITR12T) that were not officially filed by the taxpayer.

After the estimated assessment has been raised by SARS, the taxpayer will be allowed to request an original (new) return to be submitted to SARS. The same estimated return will be issued on eFiling or via SARS branch or email or post, with a new version number of the return to be completed. The taxpayer will be able to request a correction after the original return has been submitted. If SARS is still not satisfied with the outcome of the revised declaration, the taxpayer will be informed in writing.

Completion of the ITR12T Return

- To access the ITR12T Trust return, follow the steps mentioned in section Requesting your ITR12T before Official Filing Season Phase above.

Incorrect Return Type Request for Trust

- A rejection message will be displayed on eFiling when a taxpayer requests an “Income Tax return for a trust (ITR12T)” whilst being registered as an Exempt Institution (EI) or vice versa. If the taxpayer requests an incorrect return, the taxpayer will be guided to the relevant functionality to change the return type for a trust to EI or vice versa.

- For a trust registered as an EI – “Please note that the return type being requested is incorrect. You are requesting an ITR12T return, however the trust is registered as an “Exempt Institution”. Please request an ITR12EI return”

- For a trust that is not an EI – “Please note that the return type being requested is not correct. You are requesting an ITR12EI return, however the entity is registered as a “trust”. Please request an ITR12T return.

- Below is an example of one of the messages that could be displayed on eFiling.

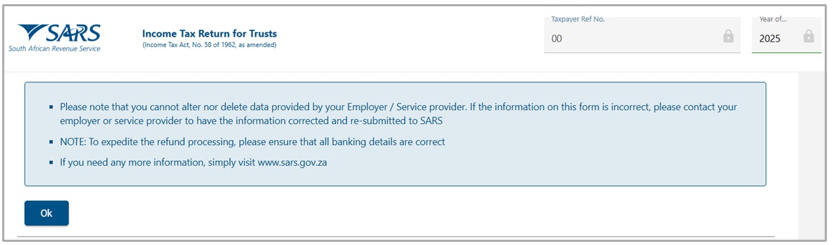

- To open the return, click the “ITR12T” hyperlink on the Income Tax Work Page.

- A warning message will be displayed to inform you that Employer/Service Provider information may not be altered. Once noted click “OK” to continue.

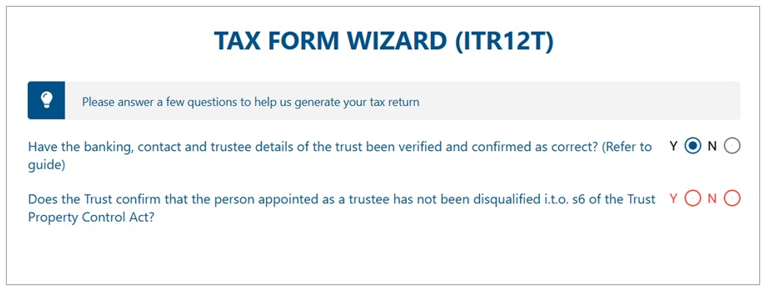

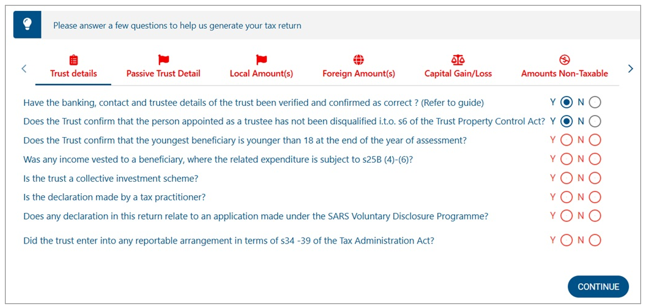

Tax Form Wizard (ITR12T) Page

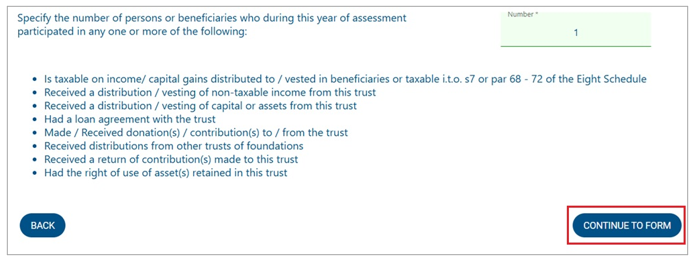

Standard and Comprehensive questions will be displayed as the first page of your ITR12T return. This wizard will aid in creating your customised trust return.

Complete all the wizard questions to create the required containers in the ITR12T return.

- Helpful hints to note whilst completing the ITR12T return:

- All mandatory fields on the ITR12T will be indicated in red.

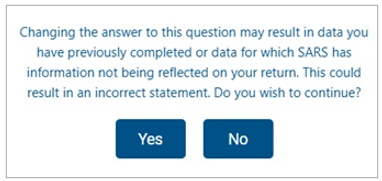

- If there are changes to the questions, a warning message will be displayed. Take note of the message and click “Yes” to continue.

- Note: If mandatory fields are not completed, an error message will be displayed and that implies that you will not be able to submit the ITR12T until it is completed.

- Depending on the answer provided to each question, subsequent questions may be displayed.

- Answer all the questions before commencing with the completion of the return.

- Click the “Continue” button to commence to the next question on the wizard or the “Back” button to proceed to previous question on the wizard.

- If any of the questions are changed after starting to complete the return, it may result in the following:

- Existing sections on the return may be removed. The form will display a warning message to alert you of any potential loss of data captured; or

- Additional sections may be displayed on the return for completion.

- Refer to the “Find a source code” tab on the SARS website to complete the source codes.

Once all the wizard questions have been completed, you will be presented with the “Continue to Form” button to proceed to complete the return.

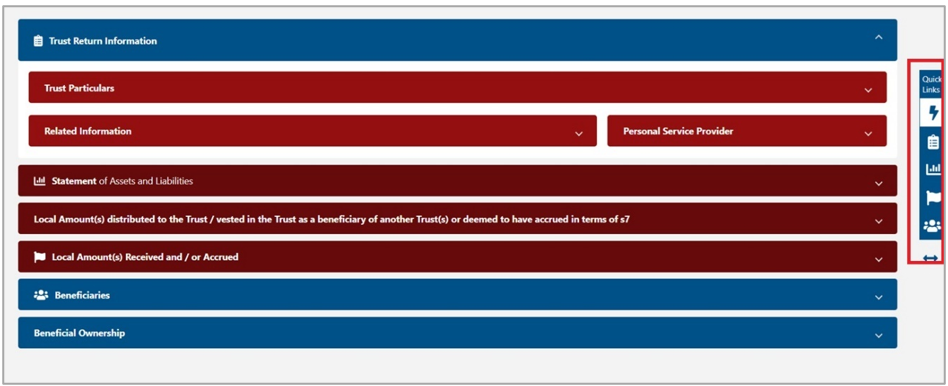

Upon scrolling down, you will be routed to your created ITR12T return.

Refer to the Comprehensive Guide to the Income Tax Return for Trusts (ITR12T) – External Guide on the SARS website for detailed information on how to complete the trust return.

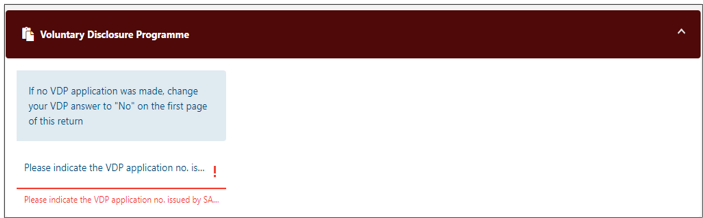

Voluntary Disclosure Programme

- If a taxpayer has applied for voluntary disclosure:

- A Taxpayer must remember to include all default amounts including previously understated income, previously overstated expenses that results in an understatement for the applicable tax year.

- The VDP application number completed on a tax return must be in respect of a validated VDP application meeting all of requirements of section 227 of the Tax Administration Act.

- A VDP submission may not result in a credit/refund due by SARS; if an assessment results in a credit/refund, the return will be rejected and the following message will be displayed:

- “The Return you are submitting does not meet the Voluntary Disclosure Programme legislative framework. Please contact the Voluntary Disclosure Unit for more information”.

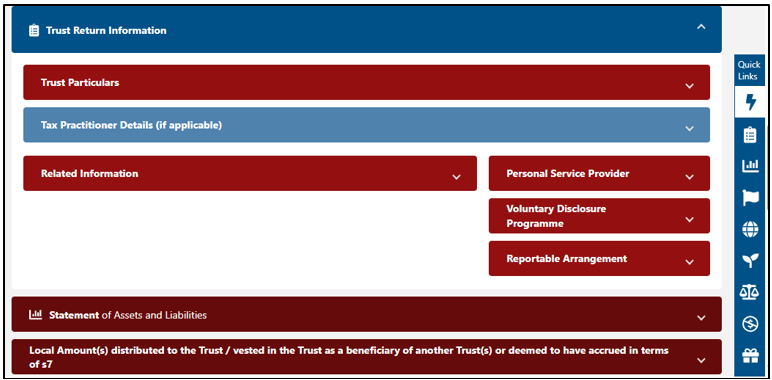

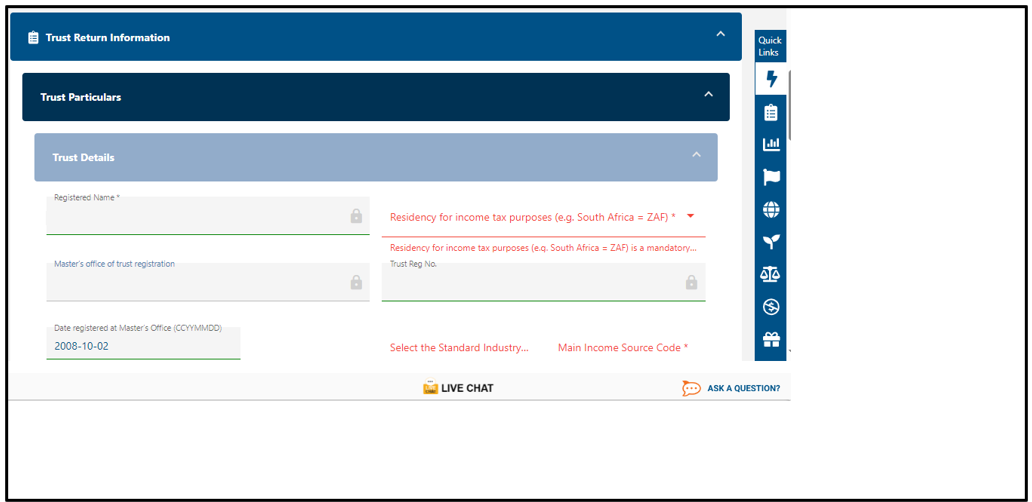

- The ITR12T will be pre-populated with the minimum demographic information of the trust.

- If all the mandatory fields are not completed, the menu tabs will be outlined in red showing that information still needs to be completed.

- Note to open each container/section of the ITR12T return, click on the “Arrow”

or “Arrow”

or “Arrow”  to close.

to close.

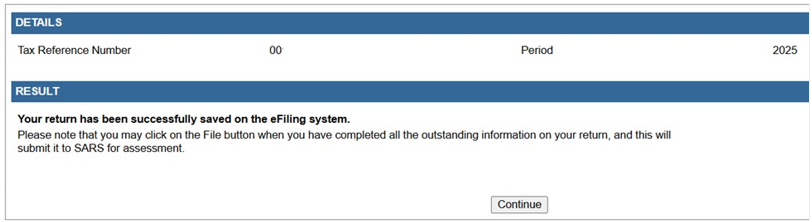

- After completing the ITR12T return, you may choose to Save the return by selecting the “Save” tab and click “Continue” on the below message to return to the main menu of the ITR12T return.

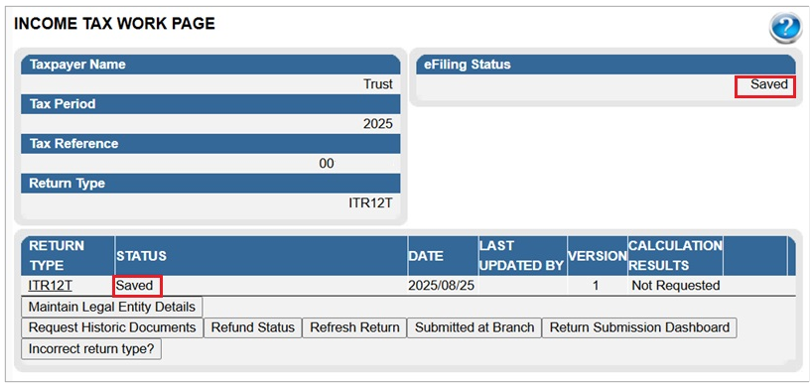

- Click on the “Continue” to proceed and the Income Tax Work Page status will be updated to indicate that the ITR12T is saved, as indicated in the below screen:

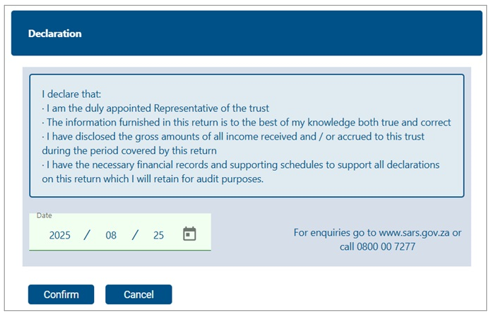

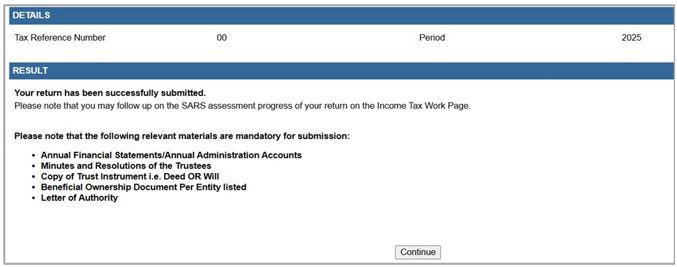

- To continue to submit the ITR12T to SARS, after completing the ITR12T return, click on the “Submit Return to SARS” button which will request you to make a declaration as indicated below:

- Click “Confirm” to proceed with the submission of the return or “Cancel” if you are no longer interested to submit at that time.

- Click “Continue” to proceed and the Income Tax Work Page status will be updated to indicate that you need to upload ITR12T supporting documents.

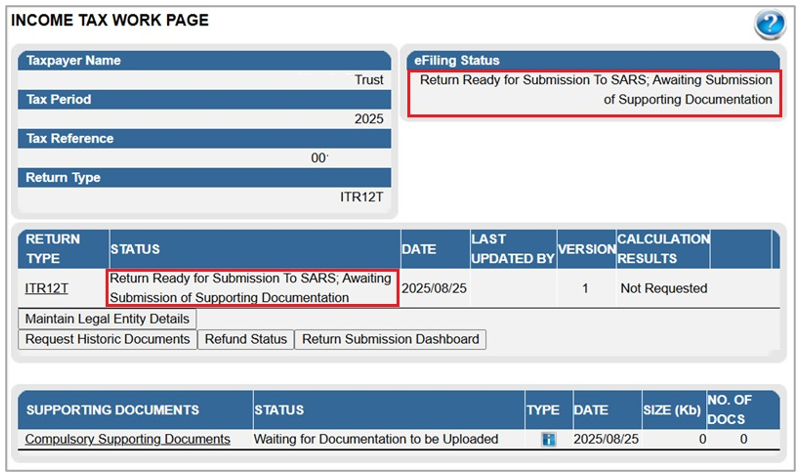

- The status of the ITR12T return will be updated to submitted and if supporting documents are required, the Income Tax Work Page status will be updated to indicate that the ITR12T is ready for submission to SARS, awaiting the submission of supporting documents as indicated in the below screen.

Uploading Supporting Documents with your ITR12T Return

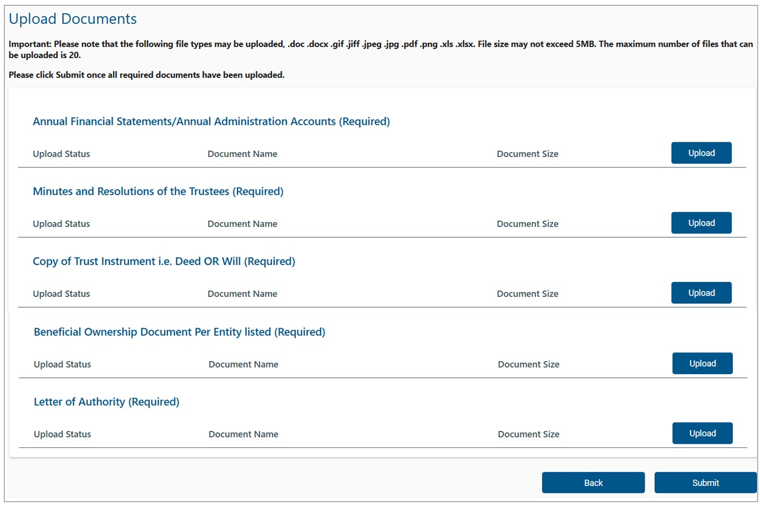

- When submitting a trust return, supporting documentation is required to determine whether the ITR12T submission should include supporting documents/schedules, the trust representative must evaluate the nature and the activities of the trust and determine which schedules are required. Refer to the Comprehensive Guide for mandatory documents that should be submitted with the return.

- eFiling permits the trust representative to upload these schedules and all relevant supporting documents together with the ITR12T return. However, note that documents can only be uploaded once the ITR12T return has been filed.

- Ensure that the following standards are adhered to when supporting documents are uploaded:

- The file type may be .pdf, .doc, .docx, .xls, .xlsx, .jpg and .gif to enable SARS to view the documents.

- The maximum allowable size per document may not be more than 5MB and a maximum of 20 documents may be uploaded.

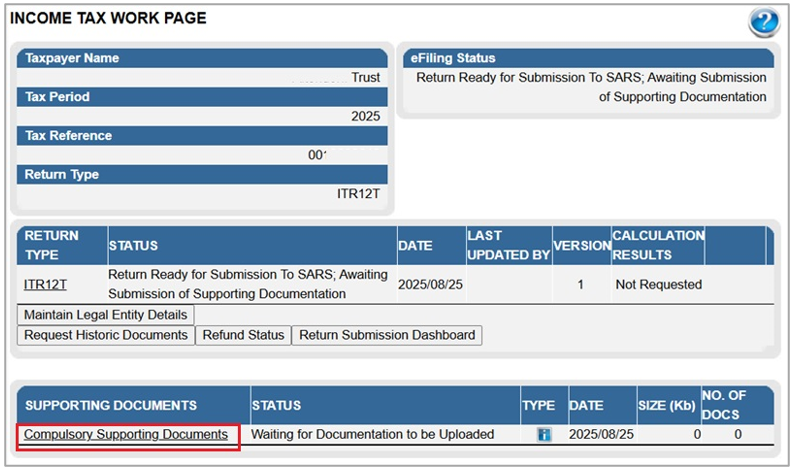

- Click on the “Compulsory supporting documents” hyperlink on the Income Tax Work Page and you will be able to submit the relevant supporting documents.

- The Upload Documents page will be displayed to upload all the required supporting documents.

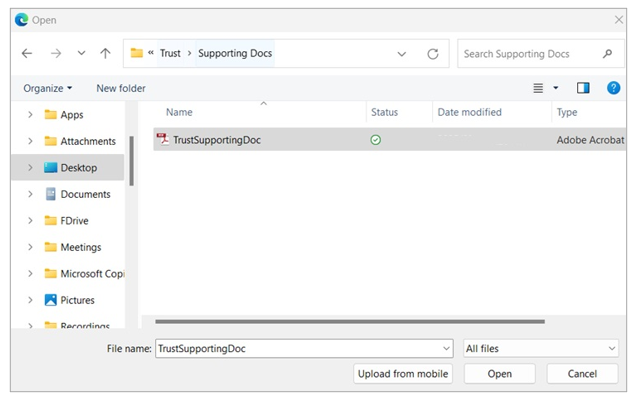

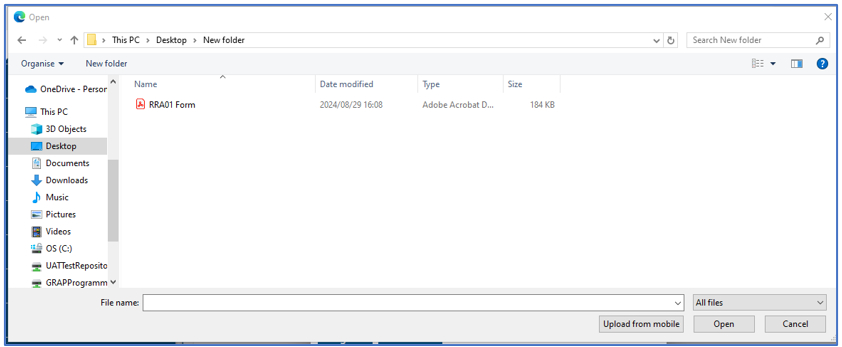

- To upload the required supporting documents, click on “Upload” icon’, the following screen will be displayed to you:

- Select the document you need to load and click “Open” to be uploaded and click submit button.

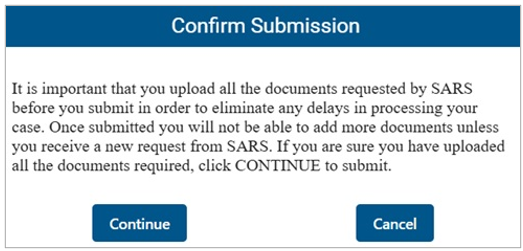

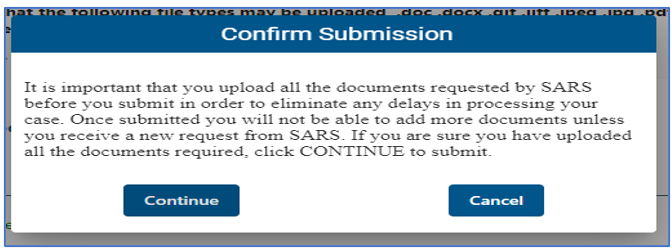

- A confirmation message will be displayed once you click the “Submit” button on the Upload Documents screen.

- Once the required supporting documents are all uploaded click “Continue” to proceed or “Cancel” if supporting documents are not uploaded as per request and you will be redirected to supporting documents landing page.

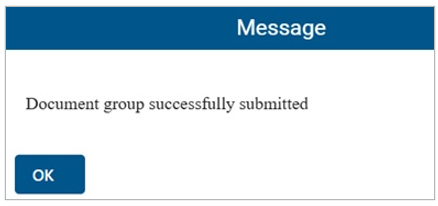

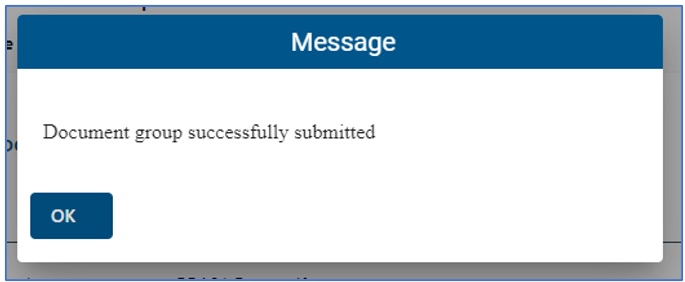

- Once all the supporting documents have been uploaded successfully click the “Ok” button on the pop- up message.

- The status on the Supporting Documents section on the “Income Tax Work Page” will be updated to “Supporting Documents Ready to be Submitted to SARS, Awaiting Return Success”

- Once all the required supporting documents have been uploaded and submitted, proceed to open the return to submit to SARS.

- The following buttons will be available for selection, namely “Back”, “Save”, “Submit Return to SARS”, “Calculate” or “Print” on eFiling.

![]()

- When all the required information has been provided on the return, click “Submit To SARS” to submit the return to SARS.

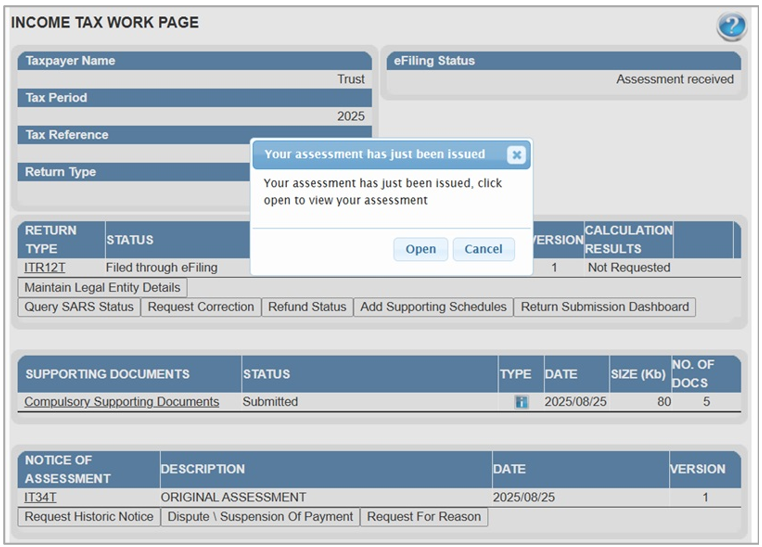

- The supporting documents status will be updated to “Submitted”. If additional supporting documents are required, an additional hyperlink may be displayed, to upload the required documents.

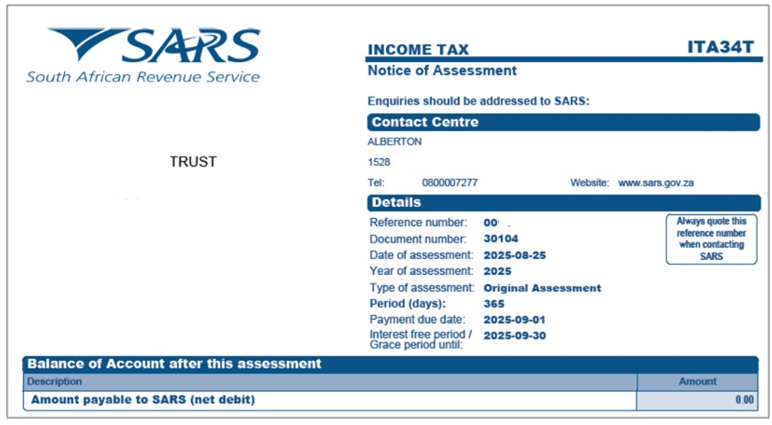

- The pop-up message will be displayed to you “Your assessment has just been issued, click open to view your assessment”.

Rejected Return due to Invalid Tax Directive

If taxpayer/tax representative submit the trust return with a lump sum amount on a IRP5 certificate, SARS will perform verifications and one of the following messages may be displayed if the verification is unsuccessful and the return may be rejected:

- IRP5 Tax Directive Number invalid

“Please note that this tax return was not processed, the Directive No. XXXXXXXXXXXXXXX captured on the IRP5 differs with the directive number issued by SARS. Please contact the Fund Administrator/Employer to rectify the error and resubmit the return.”

- IRP5 Lump sum accrual date invalid

“Please note that this tax return was not processed because the accrual date on the IRP5 certificate does not match the one issued by SARS, on Directive No. XXXXXXXXXXXXXXX. You can access a copy of the Tax Directive on eFiling or MobiApp. Urgently contact the Fund Administrator/Employer to correct the error and submit the corrected tax return.”

- IRP5 Lump sum source code Invalid

“Please note that this tax return was not processed because the Lump Sum source code on the IRP5 certificate does not match the one issued by SARS, on Directive No. XXXXXXXXXXXXXXX. You can access a copy of the Tax Directive on eFiling or MobiApp. Urgently contact the Fund Administrator/Employer to correct the error and submit the corrected tax return.”

- IRP5 Lump Sum amount invalid

“Please note that this tax return was not processed because the Lump Sum amount on the IRP5 certificate does not match the one issued by SARS on Directive No. XXXXXXXXXXXXXXX. Urgently contact the Fund Administrator/Employer to correct the error and submit the corrected tax return.”

- IRP5 Lump sum amount missing

“Please note that this tax return was not processed because SARS issued a Tax Directive No. XXXXXXXXXXXXXXX, but there is no Lump Sum amount declared on the return. You can access a copy of the Tax Directive on eFiling or MobiApp. Urgently contact the Fund Administrator/Employer to correct the error and submit the corrected tax return.”

- Directive number invalid for Taxpayer

Please note that this tax return was not processed because SARS does not have a Tax Directive issued to the taxpayer. Tax Directive No. xxxxxxxxxxxxxxx on your IRP5 is invalid. You can access a copy of the Tax Directive on eFiling or MobiApp. Urgently contact the Fund Administrator/Employer to correct the error and submit the corrected tax return.

Once the Fund Administrator or Employer has corrected the error either on the IRP5/IT3(a) certificate to correspond with the information on the tax directive or the directive has been corrected to correspond with the information on the IRP5/IT3(a) certificate with SARS, you will be able to proceed to submit the trust return. Ensure that you refresh the IRP5/IT3(a) data before completing the return.

Additional Functions on the Income Tax Work Page

This section will take you through the functions that are found on the Income tax work page and illustrate how you can use them for submission purposes.

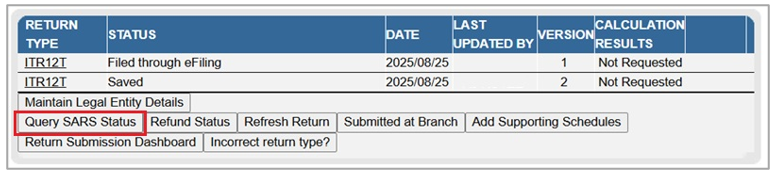

After submission of the return the following additional buttons will be visible to select:

- Query SARS Status – this button allows you to request the latest SARS status for the specific return

- Request Correction – this allows you to correct the return that has been submitted. A saved version of the return will be displayed to perform corrections.

- Add Supporting Schedules – this allows the submission of supporting schedules.

How to Request Historic Trust Submissions

To request historic submissions, proceed as follows:

- Click on “Return” displayed on the top menu.

- Click on “Return History” displayed on the left side menu.

- Select the hyperlink “Open” and the “Income tax work page” will be displayed.

Request Correction

- This function allows you to request a correction on the previously submitted ITR12T form and re-resubmit it to SARS.

- However, a request for correction will not be permitted in the following instances:

- If the return is on issued or saved state.

- If an active verification is in progress and one allowable RFC must be submitted.

- An active audit case is in progress.

- An agreed estimated or SARS estimation of an original return was performed by SARS for the trust.

- SARS has finalised an audit case or a Revised Declaration for the trust.

- If supporting documents for an active verification case have been submitted.

- If the trust representative does not agree with the assessment, a notice of objection must be lodged.

- Once the “Request Correction” has been submitted, no action will be taken on the previous return submitted, as it will be replaced by the new return.

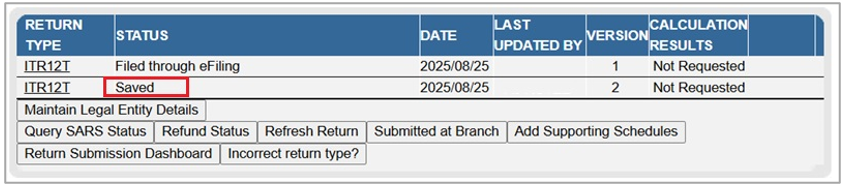

- On the “Income Tax Work Page” click on the tab, “Request Correction” displayed as one of the tab buttons below “ITR12T”.

- An additional row will be displayed on the “Income Tax Work Page” where the status is recorded as “Saved” and version is recorded as 2. Note that the version number is dependent on the number of corrections requested.

- Click “ITR12T” of the second version. Upon the selection of “ITR12T”, the ITR12T return will be displayed.

- Complete and submit the ITR12T return accordingly. Once you have filed the updated return, the “Income Tax Work Page” status will indicate that the ITR12T return has Filed through eFiling.

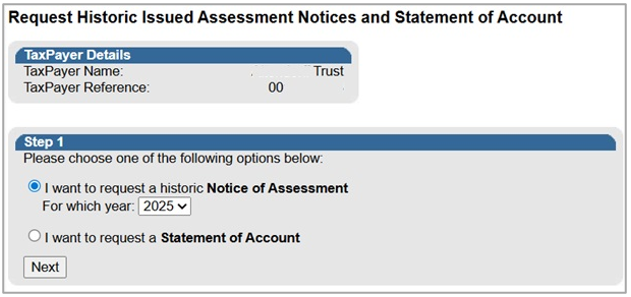

Request Historic Documents

- All returns filed to SARS are stored under “Returns History” under “Returns”. This function should be used to request historic information on your assessments.

- On the “Income Tax Work Page”, select “Request Historic Notice”.

- The “Request historic Issued Assessment Notices and Statement of Account” screen will be displayed.

- Select the appropriate year and click “Next” displayed at the bottom of the screen.

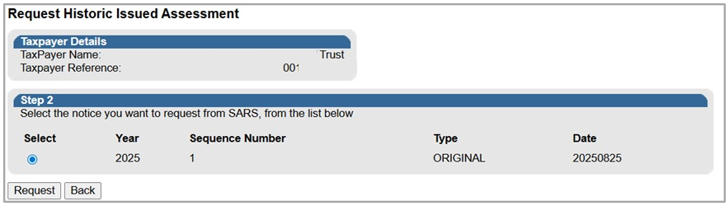

- The “Request Historic Issued Assessment” screen will be displayed indicating the selection of the year made.

- Click “Request” to continue.

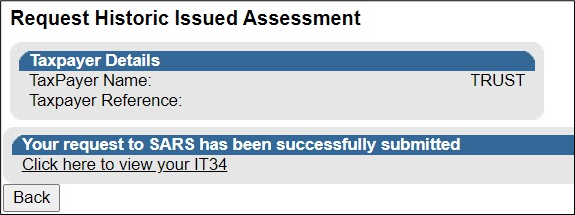

- Select “Click here to view your IT34” or click on “Back” to amend the chosen period.

- This will take the user to the ITA34T for the period of interest.

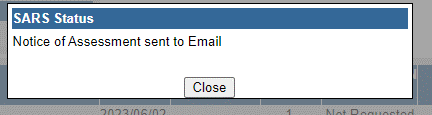

Query SARS Status

- This function should be used when enquiring the status of your ITR12T return.

- On the “Income tax work page” click on the tab button “Query SARS Status”.

- Depending on the status of the ITR12T, the screen that will be displayed will vary. Below is an example of one of the statuses.

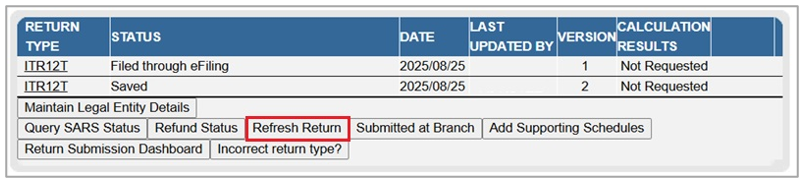

Refresh Return

- This function is to be used to update data.

- On the “Income Tax Work Page”, select “Refresh Return” tab.

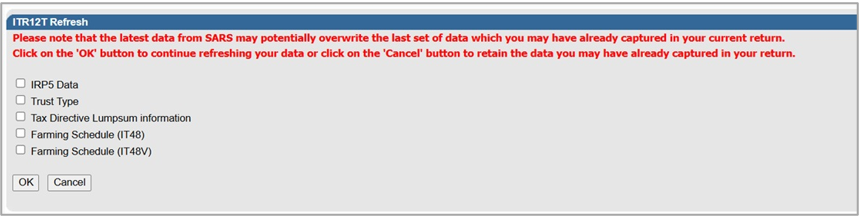

- The refresh return functionality has been updated to include farming information. Upon selecting the “Refresh Return” tab, the following warning message will be displayed.

- To refresh the return, select the option(s) that is applicable and click on “OK” to proceed to refresh the return.

- If there is Lumpsum information available for the trust, the following fields will be updated on the ITR12T return in the wizard section and on the “Lump Sum Benefits Received or Accrued” section, for each iteration of lump sum details:

- Lump sum Benefits Received or Accrued;

- How many lump sum benefits were received or accrued?;

- Gross Lump Sum (as per IRP5/IT3(a)) – Source Code 3915;

- Tax Directive Number (as per IRP5/IT3(a) certificate);

- IRP5/IT3(a) Certificate Number;

- PAYE on Lump sum Benefit.

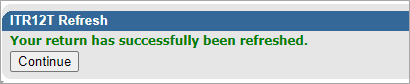

- The following message will be displayed indicating that your return was successfully refreshed.

- Click on “Continue” and you will be directed to the “Income Tax Work Page”.

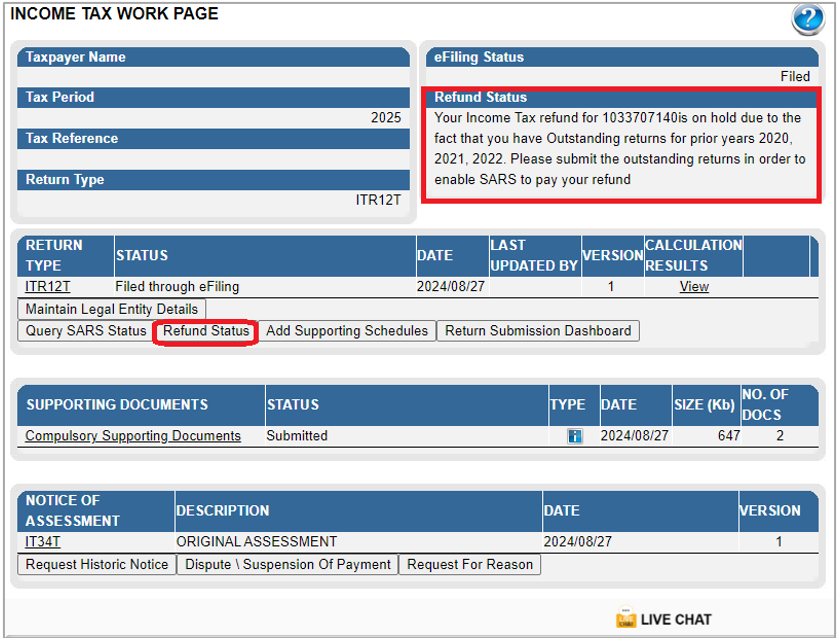

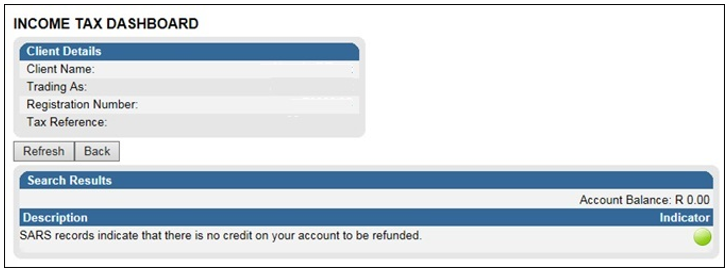

Refund Status

- This function may be used to check if you have a refund.

- On the “Income Tax Work Page”, click on “Refund Status”.

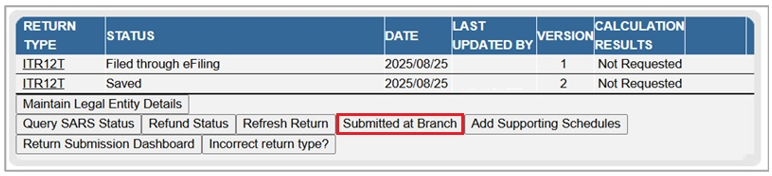

Submitted at Branch

- This function is to be used if you have submitted your return at a SARS branch.

- On the “Income Tax Work Page”, click on “Submitted at Branch”.

- The following message will be displayed.

- If the user selects “OK”, the status will be changed to filed through another channel.

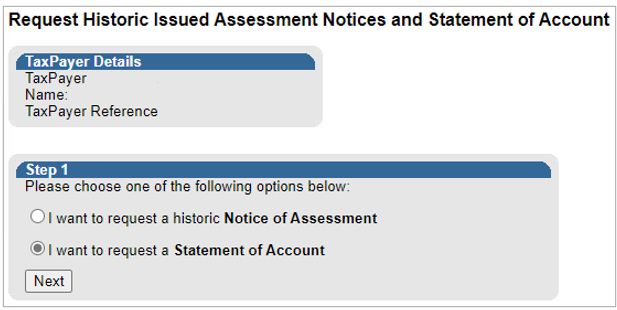

Request a Statement of Account

- This section will demonstrate how to request a statement of account. On the “Income Tax Work Page”, under the Notice of Assessment section, click the “Request Historic Notice” button.

- Select “I want to request a Statement of Account” and click “Next”.

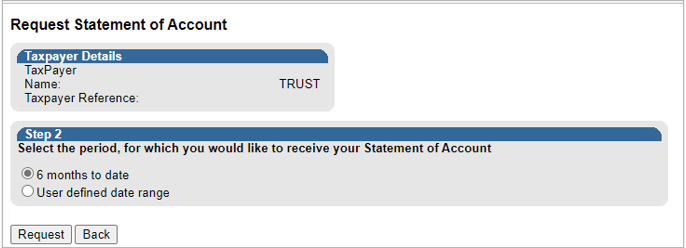

- Click the “6 months to date” option and “Request”.

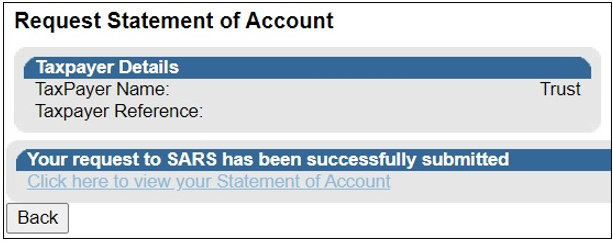

- Click on the hyperlink to view the statement of account for the ITR12T.

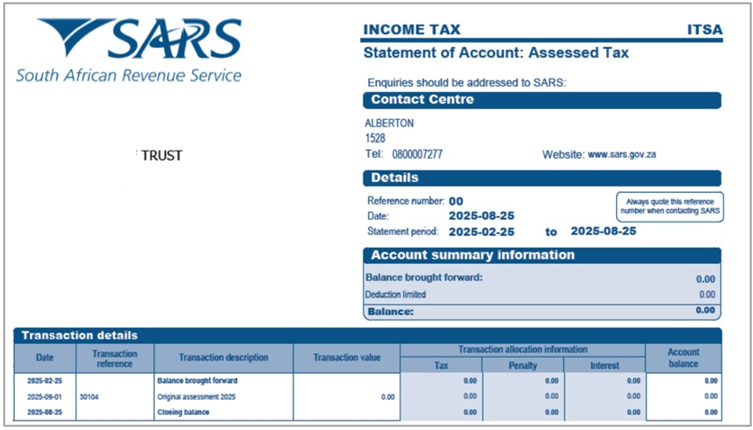

- Below is an extract of the statement of account.

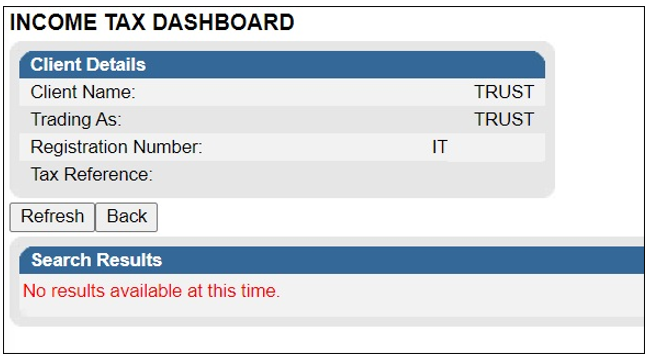

View Return Submission Dashboard

- This function will allow you to view your dashboard information.

- On the “Income Tax Work Page”, click on “Return Submission Dashboard”.

- The following screen will be displayed.

- Red – The taxpayer is required to action as per SARS status displayed.

- Amber – SARS is in progress with an action.

- Green – No action is required.

- If no indicators returned, the screen below is displayed.

Maintain Legal Entity Details

- This function is to be used when updating legal entity details of the trust representative such as contact details, banking details etc.

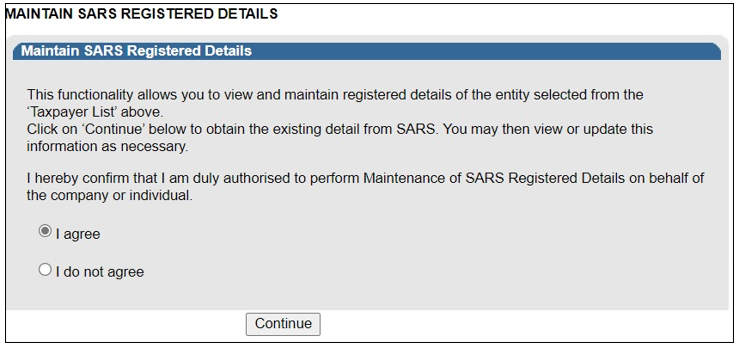

- On the “Income Tax Work page”, click “Maintain Legal Entity Details”.

- The “Maintain SARS Registered Details” screen will be displayed.

- Select “I agree” and click “Continue”.

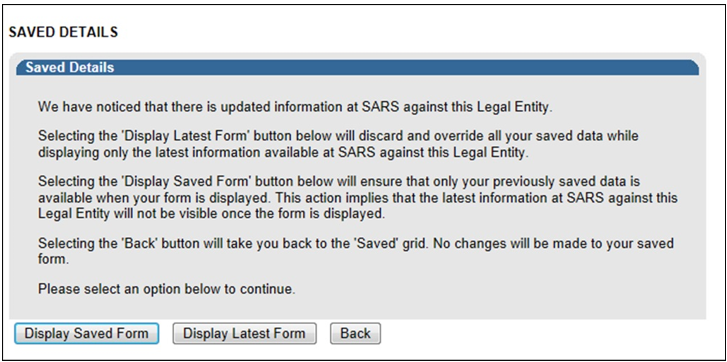

- The “Saved Details” screen will be displayed if SARS have updated information for the trust.

- If all the information of the Trusts is already updated, the RAV01 form will be displayed.

- Click on the appropriate form noting the warning message or select “Back” to go back to the “Maintain SARS Registered Details” screen.

Section 93 Reduced Assessment

- In terms of section 93 of the Tax Administration Act 28 of 2011 SARS may, despite the fact that no objection has been lodged or appeal noted, withdraw an assessment which—

- (a) was issued to the incorrect taxpayer;

- (b) was issued in respect of the incorrect tax period; or

- (c) was issued as a result of an incorrect payment allocation and to the extent that there is reasonable ground to believe that the return submitted was a fraudulent and/or fictitious submission for the reporting year of assessment.

- Total discharge refers to filed returns that were cancelled by SARS.

- The Taxpayer’, want to be able to make smaller or minor changes when a readily apparent undisputed error is found in his/her assessment or submitted return via the new Reduced Assessment process.

- If the return(s) was submitted via eFiling, the status of these return(s) will be updated to “Cancelled”. If there is more than one version of the return, all the versions’ statuses for the applicable year of assessment will be cancelled. These include returns that were filed through another channel and processed on eFiling.

- For assessments that have been totally discharged, you will not be allowed to request for correction, make payments or dispute the total discharged returns. If there is any supporting document group open, upon receipt of Total Discharge assessment notice, supporting document group will be closed since the associated return is cancelled.

- Since the return is cancelled in totality, you will be allowed to issue, capture, and submit a new return for the same year of assessment.

- When you attempt to file a dispute case (RFR/NOO/NOA/Condonation and Request for Reason/Request for Remission) while the total discharge is in progress or the assessment is withdrawn, the following message will be displayed:

- “Please note that a case to withdraw the assessment for the selected year of assessment is in progress. Therefore, you will not be allowed to file (RFR/NOO/NOA/CON/RFRE).”

- When you attempt to file a Request for Correction (RFC) while the total discharge is in progress or the assessment is withdrawn, the below message will be displayed:

- “Please note that a case to withdraw the assessment for the selected year of assessment is in progress. Therefore, you will not be allowed to file a Request for Correction”.

- When a Total discharge has been finalised and you request a dispute case (RFR/NOO/NOA/Condonation and Request for Reason/Request for Remission), the following message will be displayed:

- “No Assessment Found”.

- You may request SARS to withdraw the assessment based on the Financial Year-end changes, Fraud, Duplicate Registration/Tax Reference Number, or Incorrect taxpayer return submission.

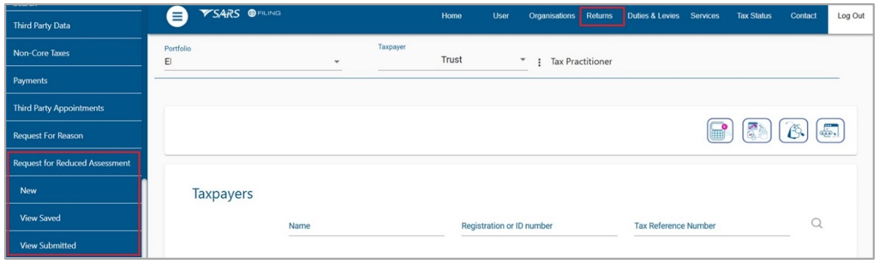

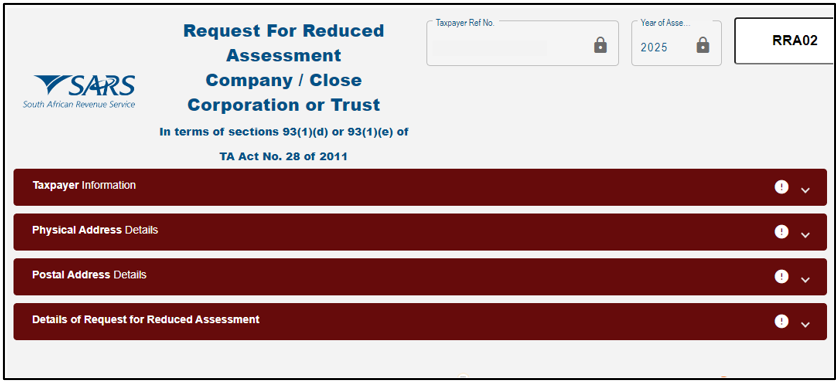

Request for Reduced Assessment

- To request a Reduced Assessment, click on “Returns”, then “Request for Reduced Assessment” from the side menu options and “New”.

- The following menu will be displayed on the sub-menu’s:

- New.

- View Saved.

- View Submitted.

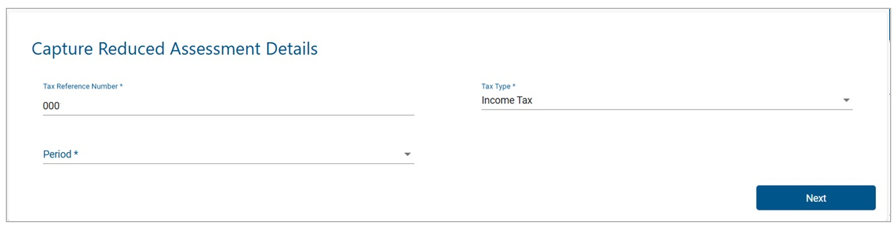

New Request for Reduced Assessment

When you select “New” in the sub-menu, the “Capture Reduced Assessment Details” screen will display:

- The following fields/items will be displayed on the new screen:

- Tax Type

- Prepopulated with trust tax number:

- Reference Number,

- Prepopulated with taxpayers’ Tax Reference number.

- Period:

- Selectable by taxpayer from 2019 to current Tax year +1.

- Next Button:

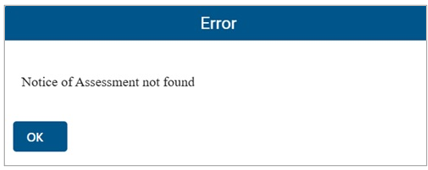

- When you click the “Next” button, the following checks will be done:

- eFiling will check if there is an assessment (ITA34T) raised for the selected Tax year:

- If no Assessment is found for the tax year selected, there will be a warning message displayed to you: “Notice of Assessment not found “and you will be prevented from continuing with the process.

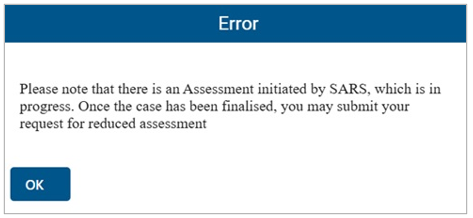

- If there is an active dispute case found, a warning pop-up message will be displayed to the you:

- “Please note that there is an Assessment initiated by SARS, which is in progress. Once the case has been finalised, you may submit your request for reduced assessment”.

- When you click on the “Ok” button is selected, you will be returned to the Request for Reduced Assessment (RRA) process search page, and you will not be allowed to continue with the process.

- “Please note that there is an Assessment initiated by SARS, which is in progress. Once the case has been finalised, you may submit your request for reduced assessment”.

- Note: The Dispute cases can be created regardless of whether there is an RRA case in progress or not.

- If there is an existing RRA case in progress, the following rejection pop-up message will be displayed to you:

- “Please note that Request for Reduced Assessment is in progress for the same assessment year”.

- An “Ok” button will be displayed to you which will redirect you back to the RRA process search page.

- If there is an existing Audit or RD case in progress, the following rejection pop up message will be displayed to you:

- “Please note that there is an Assessment initiated by SARS, which is in progress. Once the case has been finalised, you may submit your request for reduced assessment”.

- An “Ok” button will be displayed to you which will redirect the user back to the RRA process search page and you will not be allowed to request the return or continue with the RRA process.

- If there is an active Estimated Assessment (EA) or agreed estimate in progress for the selected year of assessment the following pop-up message will be displayed to you:

- “Please note that there is an Assessment initiated by SARS which is in progress, should you wish to continue to submit your request for Reduced assessment click Continue else close and exit the page”.

- A “Continue” and “Cancel” button will be displayed to you , where “Continue” button is selected, you will continue with the process as normal and where “Cancel” button is selected, you will exit the process.

- This warning message will not block the request of the Request for Reduced Assessment and you will be allowed to submit the Reduced Assessment as normal.

- If the assessment has been prescribed, the following pop-up message will be displayed to you:

- Please note that the assessment is older than 3 years, your request in terms of Section 93(1)(d) is not allowed.

- An “Ok” button will be displayed to you which will redirect you back to the RRA process search page and you will not be allowed to request the return or continue with the RRA process.

- When all the checks pass, an HTML5 interactive form will be opened to you to complete.

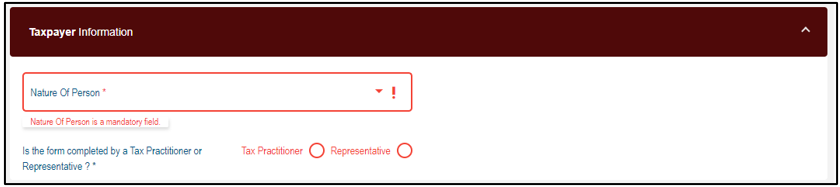

Taxpayer Information

- Complete all the fields on the container:

- Nature of Person,

- Tax Practitioner / Representative.

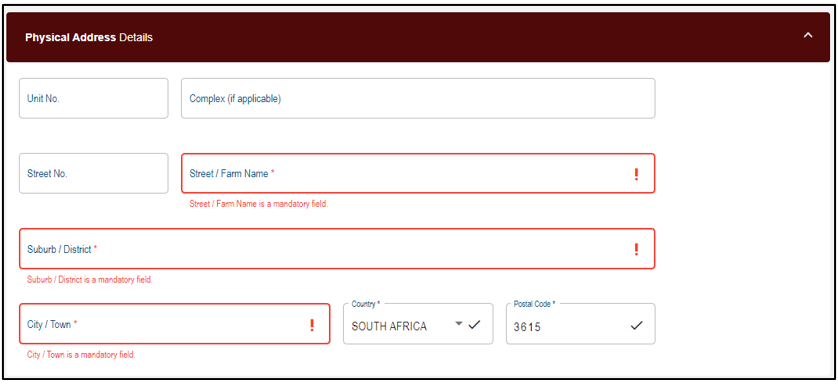

Physical Address Details

Complete all the fields on the container:

- Unit No.

- Complex (If applicable).

- Street No.

- Street/Farm Name.

- Suburb/District.

- Country.

- Postal code.

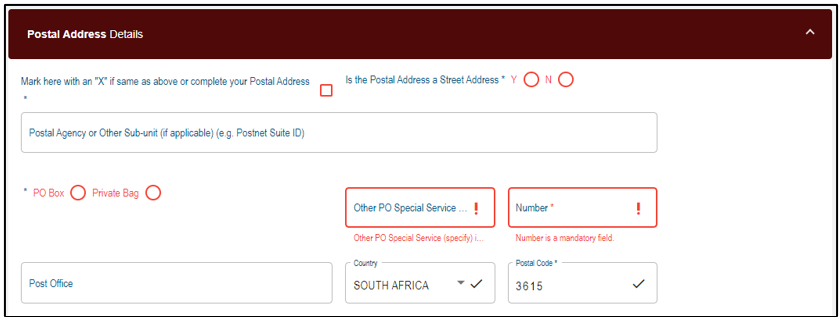

Postal Address Details

Complete all the fields on the container:

- Mark here with an “X” if same as above or complete your Postal Address.

- Is the Postal Address a Street Address Y/N.

- Unit No.

- Complex (If applicable).

- Street No.

- Street/Farm Name.

- Suburb/District.

- Country.

- Postal code.

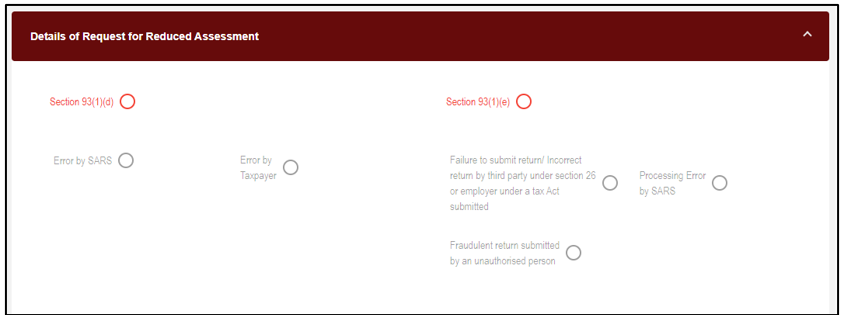

Details of Request for Reduced Assessment

Complete all the fields on the container:

- Section 93(1)d.

- Error by SARS.

- Error by Taxpayer.

- Section93(1)e.

- Failure to submit return/incorrect return by third party under section 26 or employer under a tax Act submitted.

- Processing Error by SARS.

- Fraudulent return submitted by an unauthorised person.

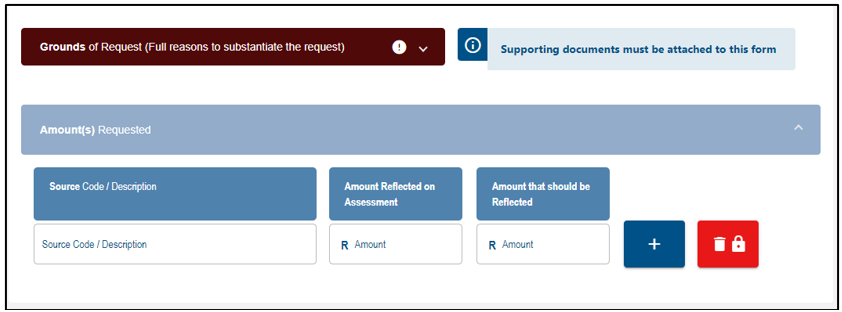

Grounds of Request (Full reasons to substantiate the request)

Complete all the fields on the container:

- Grounds of request.

- Supporting documents to be attached.

- Amounts.

- Source Codes.

- Amounts Reflected on Assessment.

- Amounts that should be Reflected on Assessment.

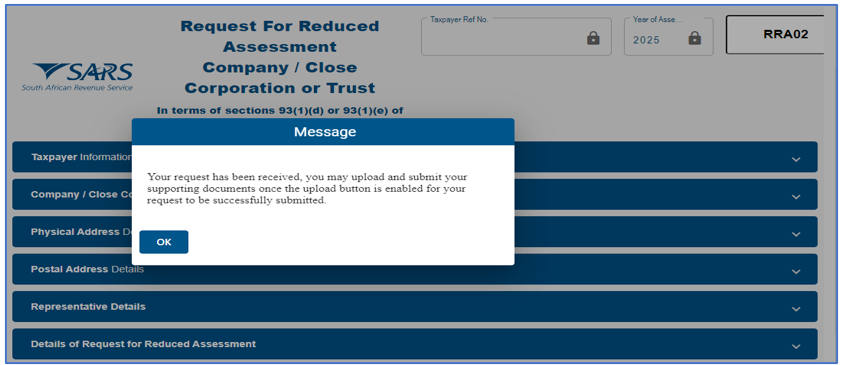

- Once the form is completed, you can submit the form and the following message will be displayed to you to upload supporting documents:

- “Your request has been received, you may upload and submit your supporting documents once the upload button is enabled for your request to be successfully submitted”.

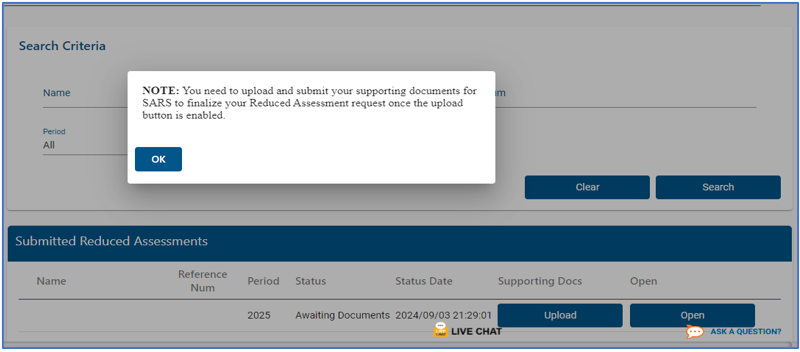

- When you click “OK”, subsequent message will be displayed to you:

- “NOTE: You need to upload and submit your supporting documents for SARS to finalize your Reduced Assessment request once the upload button is enabled”.

- Once the case number is received and processed, upload the supporting documents.

- Once Supporting Documents have been uploaded, you will be able to submit the supporting documents and only one Request for reduced assessment per tax period can be submitted.

- Once the form is successfully uploaded following message will be displayed:

- Once the Submission has been completed successfully, eFiling will send a new Receipt Confirmation letter as well as the subsequent Outcome letters that refers to as:

- Disallow.

- Allow.

- Partially Allow.

- You will be able to View the submitted application on the View Submitted sub-menu.

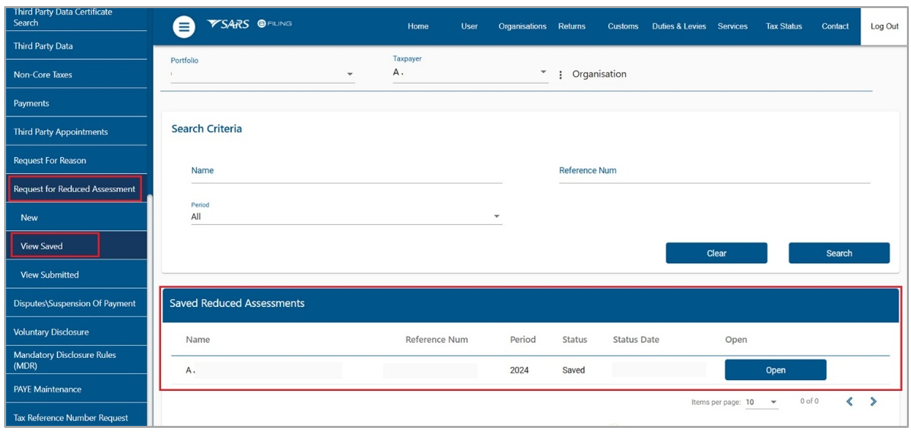

View Saved

- When the “View Saved” sub-menu is selected, a new page will be opened:

- A “Save” button on the form page will allow you to save the captured data.

- If you select “Save” button, the form information will be saved, and you will be able to open the Form from the “View Saved” sub-menu item.

- A “Save” button on the form page will allow you to save the captured data.

- The following fields/items will be displayed:

- Name of the trust Taxpayer:

- Name of the trust Taxpayer who is requesting Reduced Assessment.

- Reference Number:

- Reference number of the Company requesting Reduced Assessment

- Field must be prepopulated and locked.

- A search function will be presented on to your screen.

- The following fields/items will be displayed for the user to search for a particular submitted form:

- Company Taxpayer Name:

- Name of the trust Taxpayer who is requesting Reduced Assessment.

- Field will be prepopulated and locked.

- Reference Number:

- Reference number of the trust Taxpayer requesting Reduced Assessment.

- Field will be prepopulated and locked.

- Tax Period.

- Search Button:

- When you click the “Search”, the relevant submitted item will be returned for you to view with the above fields displayed.

- Status:

- The status will indicate “Saved”.

- Tax Period

- Status Date

- Date at which the form was last Saved.

- Open Form:

- Link/Button to open the selected Saved form.

- The saved forms will be listed and ordered from the earliest saved form to the latest.

- If this is selected, the form will open for the taxpayer to complete.

- Company Taxpayer Name:

- Name of the trust Taxpayer:

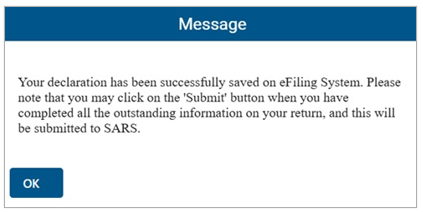

- Once the form is completed, you can save/submit the form and the following message will be displayed to you to upload supporting documents:

- A message will be displayed to you : “Your declaration has been successfully saved on eFiling System. Please note that you may click on the ‘Submit’ button when you have completed all the outstanding information on your return, and this will be submitted to SARS.”

- When you click “Submit” button: the below message will be displayed:

- “Your declaration has been successfully submitted”.

- Note: You need to upload and submit supporting documents for SARS to finalize the Reduced Assessment request, refer to Section – Submission of the Form.

- The form can be viewed in a read only format and flattened by stream serve by clicking the “Print” button.

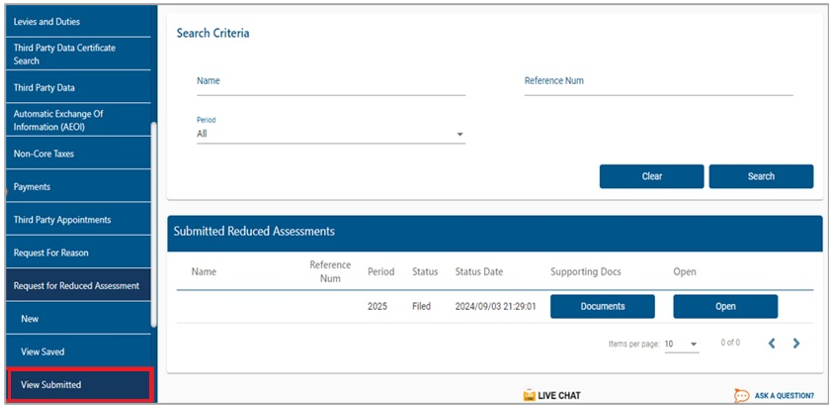

View Submitted

- When the “View Submitted” sub-menu is selected, a new page will be opened:

- The following fields/items will be displayed:

- Name:

- Name the trust Taxpayer who is requesting Reduced Assessment.

- Reference Number:

- Tax reference number of the trust Taxpayer requesting Reduced Assessment.

- Period:

- Tax year period of which the Request for Reduced Assessment was requested for.

- Status Date:

- Date on which the form was submitted.

- Link to the supporting documents:

- Status.

- In Progress.

- Awaiting Documents – this will be displayed to you when you have not uploaded supporting documents on eFiling to be sent to SARS.

- Submit Uploaded Documents – this will be displayed to you when you have uploaded support documents but has not yet submitted the SARS.

- Filed – this will be displayed to you once the uploaded supporting documents have been submitted to SARS.

- Open:

- The form will open the submitted RRA form in a read only format.

- Name:

- The following fields/items will be displayed:

SARS Notices

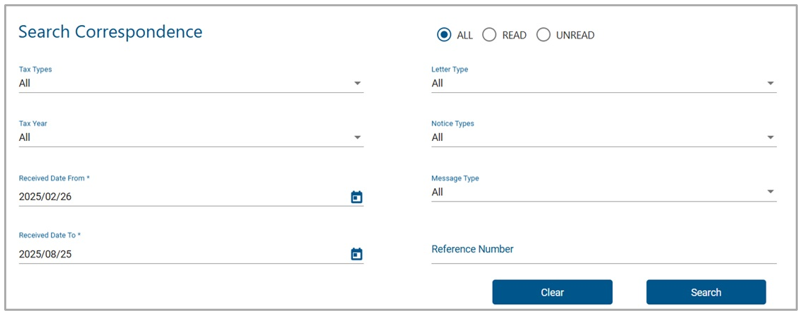

- To view notices or letters issued, under the “Returns” menu, select “SARS Correspondence”.

- Select “SARS Correspondence”, enter the tax type, tax year, and notice type.

- Select applicable option on the “Notice Type” and click “Search” to continue. All notices issued by SARS will be displayed. Click the relevant “View” tab and the notice will be displayed.

- The results section will list all the correspondence issued for the selected information completed in the search correspondence step above.

- Acknowledgement letter.

- Request for Relevant Material.

- Disallow Letter.

- Partially Allow letter.

- Allow letter.

Definitions, acronyms and abbreviations

The definitions, acronyms and abbreviations can be accessed here – Glossary webpage.

Legal disclaimer: In the event of conflict or inconsistency between this webpage and the PDF version of the guide, the latter shall prevail.