This 7th edition of the SMME Connect comes as most companies have just finalised and submitted their Company Income Tax Returns (ITR14) and their second-period Provisional Returns (IRP6). To these companies, we at SARS extend our heartfelt gratitude on behalf of all South Africans who benefit from the taxes paid. We also want to remind companies that have missed the deadline that they can still complete and submit their returns. This issue offers simple guides to help you meet your tax obligations.

Remember to File Your Annual Returns with the Companies and Intellectual Property Commission (CIPC)

Law requires companies and close corporations to file their annual returns with CIPC each year within 30 business days after the anniversary date of the business’s incorporation.

Annual returns enable CIPC to confirm that a registered business is still in business, trading, or if it will be in business soon. If CIPC receives no annual return on time, it will assume that the business is inactive and begin to deregister the company. If a company or close corporation is not registered with CIPC, it cannot be recognised as a legal entity.

How to File Your Company’s Annual Return with CIPC

To file annual returns, visit the CIPC website.

- Log in as a customer or register a new customer code (if you do not have login details).

- Click on “File Annual Returns”.

- Click on “Annual Return Calculator” to calculate outstanding annual returns and their years, or choose “File Annual Returns” if you want to file. Type in your enterprise number in the “Enterprise Number” field, click “Validate”, and then “Turnover” to calculate your filing fee.

- Confirm if the registration number given by CIPC corresponds with the details of your company that the website displays. If not, reconfirm your registration number by typing it into the “Enterprise Number” field and click “Validate”. If correct, click “Continue”.

- The “Paid” and “Outstanding Annual Returns” will now appear. Under the “Outstanding Annual Returns” heading, type in the turnover amount in the “Turnover” field. Click “Calculate Outstanding Amount”.

- The CIPC website will first calculate and display the annual-return fee payable and then check if your company submitted annual financial statements (AFS) or the Financial Accountability Supplement (FAS) for the applicable year. If your company did not submit AFS or FAS, click on either “Capture AFS” or “Capture FAS”, depending on the document you should upload.

- File and pay for your annual returns.

Once you have filed your annual return, print or save the filing confirmation and certificate as proof of filing.

For assistance, visit CIPC website and select “Enquiries”.

Remember to include up-to-date details of your business with your annual CIPC return:

- Corporate information, such as directors, auditor, address, financial year-end, and company name.

- Financial record-keeping and financial information (through AFS or FAS).

- Level of compliance with Companies Act.

- Beneficial owners.

- Operational information, such as the number of employees, dormancy, and main business activity.

Keep in mind that your obligations with SARS are separate from your obligations with CIPC. SARS compliance focuses on tax matters, whereas CIPC oversees company registration, compliance with the Companies Act, and issues related to intellectual property.

Corporate Income Tax

Income Tax Return (ITR14)

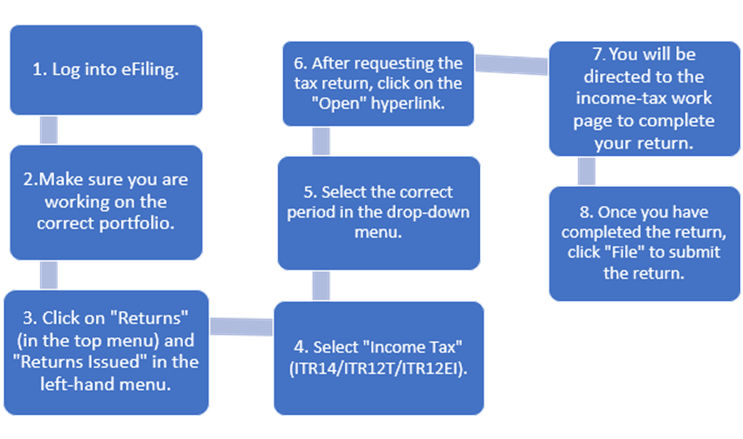

For those companies who still need to complete and submit their returns, remember, you can use SARS eFiling to submit your return (ITR14) and pay your debt online. To use eFiling, you must register as an individual and add your company under your profile. You can also view your statement of account and pay through eFiling.

Here are the steps to file your ITR14:

Need help to complete your ITR14 return? Visit SARS’s YouTube channel and watch the video on How to Submit Your Income Tax Returns for Companies ITR14 on eFiling. For more information, visit SARS website, where you can find answers to frequently asked questions.

Turnover Tax

SARS encourages micro-businesses that find the cost of compliance too high to register for Turnover Tax. This replaces Income Tax, Value-added Tax (optional), Provisional Tax, Capital Gains Tax, and Dividend tax for micro-businesses with a qualifying annual turnover of R1 million or less. Turnover tax simplifies record-keeping for micro-businesses, which are not required to keep records of expenses such as petrol slips and rank fees.

To register for Turnover Tax, download and complete the application (TT01) form from the SARS website (Turnover Tax Webpage). You can email your completed form to [email protected] or submit it at a SARS branch after booking an appointment.

Steps | TT01 (Registration for Turnover Tax | TT02 (Payment Remittance) | TT03 (Tax Return for Turnover Tax) |

1. | Download the form and submit it through e-mail or make an appointment to submit it through a SARS branch. | Download TT02 and complete it. | Download TT03, complete it, and print it for submission. |

2. | Register before the beginning of the financial year (1 March) or within two months from the date of commencement. | Pay and use the correct Payment Reference Number (PRN). | Submit by email ([email protected]) or through a SARS branch (by appointment). |

Turnover Tax returns (TT03) must be submitted each year from 1 July to 31 January.

Turnover Tax involves three payments:

- First payment on or before 31 August with the TT02 – Payment Advice for Turnover Tax.

- Second payment on or before 29 February through the TT02.

- The final payment is due after the annual TT03 is submitted and processed.

SARS will register small businesses not eligible for Turnover Tax under the Income Tax regime. If your company’s financial year-end is February, you must submit your ITR14 form on or before the last day of February.. This is the Income Tax–return deadline for companies. ITR14 shows your company’s income, expenses, assets, liabilities, and tax payable for the year of assessment.

Pay any outstanding debt on or before the ITR14 due date to avoid penalties and interest. If you are unable to pay your outstanding debt, you can apply for a deferred-payment arrangement or a debt compromise. If you have no income and are unable to pay, please contact SARS via email at [email protected] for options.

If your company did not trade for the year of assessment or it made a loss, you must still submit a return to avoid non-compliance penalties.

Administrative Penalties

Penalties will be imposed when the company has failed to submit an Income Tax return for years of assessment ending in the 2009 and subsequent calendar years.

The non-compliance administrative penalty for the failure to submit a return are fixed-amount penalties based on a taxpayer’s taxable income. Penalties can range from R250 up to R16 000 for each month of non-compliance. If you do not agree with the penalty, submit the outstanding return and Request for Remission (RFR) to dispute the penalty levied over non-compliance. Taxpayers must give reasons for the non-compliance for SARS to consider the request.

How to Pay SARS Debt?

If you owe SARS money, you have options to settle your debt or to request payment arrangements. You can:

- Pay or request payment arrangements using SARS eFiling by clicking the “Non-compliance” option under “My Compliance Profile”.

- Pay with SARS Mobi-App and SARS Online Query system.

- Pay on or before the due-date, unless:

- The due date falls on the weekend, in which case you should pay a working day before the weekend.

- The due date falls on the public holiday, then you should pay a working day before the public holiday.

Important note: If you pay on the due date, make sure that you pay in the morning so that the transaction can reflect on the SARS system on time to avoid penalties and interest.

We always recommend the payment to be done before the due date to avoid bank transaction errors.

SARS is committed to help small businesses to comply with their tax obligations by giving them the information, assistance, and incentives they need. SARS encourages small businesses to be honest and cooperative, and to keep accurate and complete records of their income and expenses.

By working together, SARS and small businesses can ensure a fair and efficient tax system that enables the state to provide for the well-being of the country.

VAT Enhancements for Estimated Assessments

SARS can now generate an estimated assessment for VAT. If a vendor does not provide the relevant material requested by SARS during the VAT-verification process, SARS may raise an estimated assessment in terms of section 95(1)(c) of the Tax Administration Act. Please note the following regarding estimated assessments:

- The details of the estimated assessment can be viewed on the notice (VAT217) issued to the vendor.

- A Request for Correction will not be allowed if SARS has raised an estimated assessment for VAT in the same period.

- If vendors do not agree with SARS’s estimated assessment, they should submit the required within 40 business days from the date the VAT217 notice was issued.

- The vendor can submit the outstanding relevant material through eFiling, at a SARS branch, or through the SARS Online Query System (SOQS).

- Vendors can request an extension if the relevant material cannot be submitted within 40 business days.

- If SARS approves the Request for Extension, the vendor will have until the date of extension, or five years plus 40 business days, to submit the relevant material.

- The vendor can submit a Request for Suspension of Payment if SARS’s estimated assessment shows an amount payable for the period stipulated in the VAT217 notice.

- The vendor cannot submit a Notice of Objection because an estimated assessment issued in terms of section 95(1)(c) is not subject to dispute.

See the following updated external guides available on the SARS website:

PAYE Employer Reconciliation 2025

PAYE Employer Reconciliation BRS for the 2025 tax year was published on the 7th of March.

The changes include:

- New source code (3926) for the Withdrawal from a Retirement Fund from the Savings Component/Pot

- Amendment of descriptions and/or validation rules for:

- Unclaimed benefits (source code 3909)

- Certificate Number (source code 3010)

- Directive Number (source code 3230)

- Directive Income Source Code (source code 3232)

- Transfer of Unclaimed Benefits (source code 3923)

- NED Directors / Audit Committee Member Fees (source code 3620/3670)

The submission dates:

- Interim: 16 September – 31 October 2024

- Annual: 1 April – 31 May 2025

List of Scams

Beware the latest email scam titled “SARS Tax Review”. Please ignore it and do not click on any links. If in doubt, send an email to [email protected].

Good to Know

We encourage your business to take advantage of SARS’s tax incentives. They include:

- Turnover Tax for micro-businesses that have a turnover of R1 million and less.

- Small Business Corporation status for small businesses with an annual turnover of up to R20 million. These businesses may qualify to pay less income tax.

- Employment Tax Incentive to incentivise employers to hire young job seekers.

For more information, go to the SARS website homepage and select the Small Business tab.

Learn about the benefits of joining the National Small Business Council. Visit www.nsbc.africa/member benefits.

#YourTaxMatters www.sars.gov.za