What’s New?

- 20 March 2026 – Budget 2026 Frequently Asked Questions

Key Turnover Tax changes from Budget 2026: FAQs on the Turnover Tax changes - 25 February 2026 – Turnover Tax threshold increase

The Turnover Tax threshold has increased from R1.to R2.3 million as per the Budget Speech, 2026. The tax-free threshold has been adjusted to R600 000. The effective date for the increase is 1 April 2026.

Top Tips!

You can now register for Turnover Tax on SARS Online Query System SOQS!

Please also read the updated micro businesses guide and Frequently Asked Questions(FAQs).

What is it?

Turnover tax is a simplified system aimed at making it easier for micro business to meet their tax obligations. The turnover tax system replaces Income Tax, VAT, Provisional Tax, Capital Gains Tax and Dividends Tax for micro businesses with a qualifying annual turnover of R2.3 million or less. A micro business that is registered for turnover tax can, however, elect to remain in the VAT system (from 1 March 2012).

Turnover tax is worked out by applying a tax rate to the taxable turnover of a micro business. Year of assessment ending on any date between 1 March 2026 and 28 February 2027:

| Turnover (R) | Rate of tax (R) |

| 0 – 600 000 | 0% |

| 600 001 – 950 000 | 1% of each R1 above 600 000 |

| 950 001 – 1 400 000 | 3 500 + 2% of the amount above 600 000 |

| 1 400 001 – 2 300 000 | 12 500 + 3% of the amount above 1 400 000 |

Who is it for?

- Individuals (sole proprietors)

- Partnerships

- Close corporations

- Companies

- Co-operatives

How to register?

- Do a quick test to see if you qualify for turnover tax

- For more information on how to register

How to submit?

The following channels can be used to submit Turnover Tax returns:

How to book an appointment for Turnover Tax

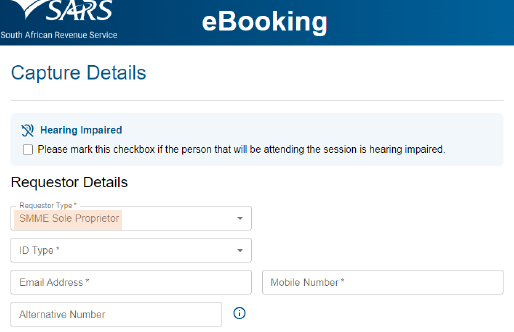

Step 1: On the eBooking system complete the requestor details and complete the following fields as per your selection:

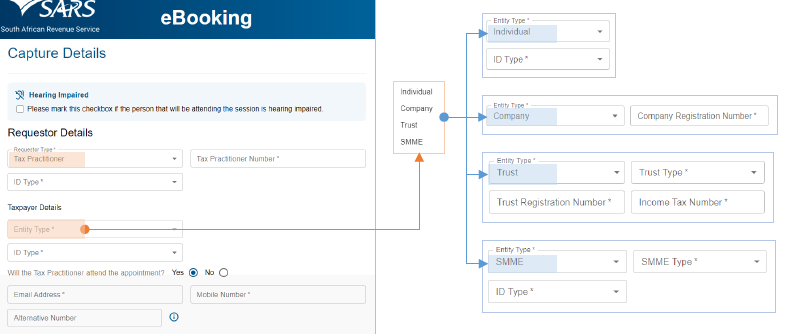

Or if you are a Tax Practitioner, select Tax Practitioner, then complete the fields as per your selection:

Step 2: To ensure that the booking is initiated by a human and not a machine/computer, you are required to insert a security code (also known as a CAPTCHA code):

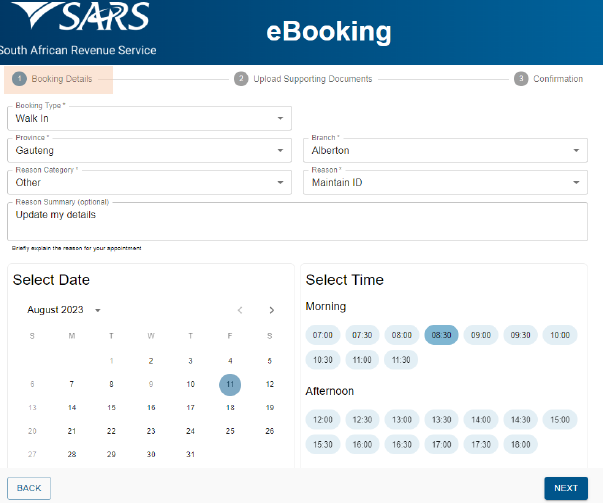

Step 3: Complete the”Create Booking” screen, and the appointment information:

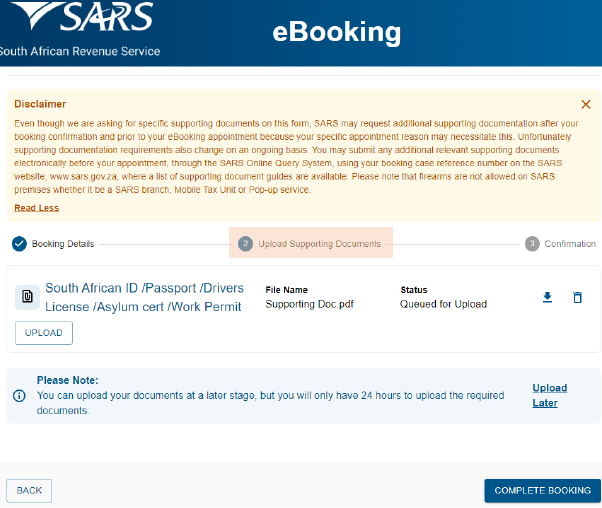

Step 4: Upload supporting documents:

The following types of documents are required for an eBooking appointment:

- Supporting documents to authenticate the person who will be attending the appointment

- Supporting documents related to specific eBooking reasons. For more information, please refer to the SARS website.

How to pay?

- 1st payment is in the middle of the tax year on the last business day of August i.e. 29 August 2014 on the TT02 – Payment Advice for Turnover Tax

- 2nd payment is at the end of the tax year on the last business day of February i.e. 27 February 2015 on the TT02 – Payment Advice for Turnover Tax

Final payment is after the annual TT03 – Turnover Tax Return is submitted and processed. The submission of TT03 turnover tax returns is in line with the submission of the annual income tax returns, between 1 July and 31 January of the following year.

Top tip: Making Turnover Tax payments on the payment advice (TT02):

- Payments can be made at banks or electronically using internet banking.

- When payment is made, it is essential that the ‘Beneficiary ID’ and ‘Payment Reference Number’ are quoted. The Payment Advice (TT02) will assist with this and other matters relating to interim payments.

Note: The TT02 payment advice is the taxpayer’s record. It must not be submitted to SARS for TT purposes.

Where any day specified for any payment to be made under the provisions of the Act falls on a Saturday, Sunday or public holiday, the payment must be made no later than the last business day before the Saturday, Sunday or public holiday.

Click here for more information on how to pay and submit.

What records should be kept?

1. Records of all amounts received;2. Records of dividends declared;3. A list of each asset with a cost price of more than R10,000 at the end of the year of assessment as well as of liabilities exceeding R10,000.