Financial Action Task Force (FATF) Update and Feedback

As previously communicated in the EI Connect Q3, a survey was conducted with the Non-Profit Organisations (NPOs) as part of the FATF South African (SA) Non-Profit Organisations (NPO) Terrorism Financing (TF) Sectoral Risk Assessment (SRA). This survey aimed to assess the inherent risk of South African NPOs being knowingly or unknowingly used or abused for terrorism financing (TF).

Since the survey’s completion, the outcomes have been drafted into Part I of the FATF SA NPO TF SRA report. In addition to this initial report, the Government, in conjunction with the NPO Sector, has also been working on the Part 2 of the report, which will highlight how all impacted stakeholders can prevent the abuse / use of NPOs as vehicles for TF.

The full FATF SA NPO TF SRA report will be launched on 18 and 19 April 2024. The various Government Departments and Civil Sector Organisations that participated in compiling the report will also make the document available on their respective websites.

Third-Party Data Submissions to SARS — IT3(d) Update

From May 2024, Section 18A approved entities must provide SARS with their S18A third-party data submissions. This means that all Section 18A approved entities that have issued Section 18A tax deductible receipts to their donors from 1 March 2023 to 29 February 2024, must submit this data to SARS. If an approved entity has not issued any S18A receipts for the period, they must submit a NIL declaration. Section 18A entities are encouraged to contact [email protected] for assistance with the onboarding process.

SARS remains available to assist entities who require assistance with the onboarding information on submission channels/platforms and guides. This ensures that when official submission starts, taxpayers are comfortable with their ability to submit the data to SARS. Entities required to submit IT3(d) S18A tax deductible receipts third-party data must read through the business requirement specification (BRS), which indicates the required information and fields.

SARS has developed a micro-learning video which informs taxpayers how to register for IT3. The first step to register for IT3(d) is that the S18A entities must be registered on eFiling, and the registered representative must be updated on eFiling. This micro-learning video is available on the SARS website and YouTube Channel (SARS TV). In the coming months, SARS will develop more micro-learning videos to help taxpayers submit IT3(d) information.

World NGO Day — 27 February 2024

The 27th of February is the World Non-Governmental Organisation (NGO) Day, celebrated annually in more than 89 countries and six continents. World NGO Day is an international day that recognises and honours all non-governmental and non-profit organisations and the people behind them. We celebrate and acknowledge the providers, helpers, and the givers who serve society. This year SARS joined the celebration of the work done by the South African NGO Sector.

The theme for this year’s World NGO Day was “Building a Sustainable Future: the Role of NGOs in Achieving the United Nations Social Development Goals (SDGs)”.

Many countries recognise the significant role NGOs play in building a strong, caring, and well-functioning society as they contribute to employment, welfare, and economic growth. These countries provide tax incentives or tax relief to those organisations and their donors. South Africa has an enabling tax system for NGOs that offers certain tax incentives. This special tax dispensation is applicable only if the NGO has applied for it and once SARS approves it, in which case the NGO will be known as a Public Benefit Organisation.

Did you know?

- More than 10 million NGOs operate worldwide, employing more than 50 million non-profit workers.

- Data from Statistics South Africa’s Quarterly Labour Force Survey indicate that the biggest job gains were recorded in the NGO sector, which created 206 000 sustainable job opportunities (from the last quarter of December 2022 to the last quarter of 2023). When other sectors were losing jobs, the NGO sector recorded a 5% growth in employment, with the proportion of employed women growing by 15.5%.

For more PBO facts click here.

Taxation of Bodies Corporate, Share Block Companies, and Home Owners’ Associations

The article below provides an overview on the duties and responsibilities of Home Owners Associations. Because of similarities in the governing legislation, we also discuss the taxation of Bodies Corporate, Share Block Companies, and Other Associations of Persons (commonly known as Home Owners Associations, Residents’ Associations and Property Associations). For ease of reference, we will refer to these Other Associations of Persons as Home Owners Associations.

The Income Tax Act lays out provisions for the taxation of Bodies Corporate, Share Block Companies, and Home Owners Associations.

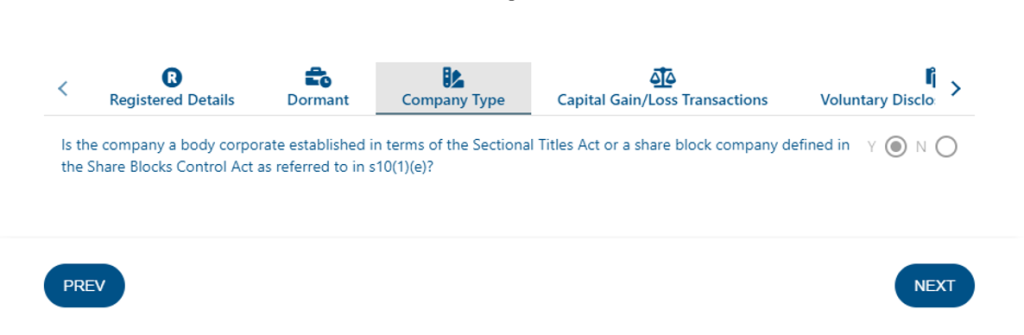

Typically, levies collected by these entities for day-to-day operations, capital improvements, building penalty levies, or stabilisation funds are exempt from normal tax in terms of section 10(1)(e) of the Act. A basic exemption of R50 000 also applies to other receipts and accruals of these entities that are not levies.

Establishment and Registration

Although these entities enjoy exemptions in terms of the same provisions of the Act, there is a distinct difference as to the administration of these entities are administered. Entities established as Bodies Corporates and Share Block Companies have specific registration requirements in contrast with the Other Associations of Persons. For example, . This act requires Body Corporates to register with the Deeds Office, and Share Block Companies to register with the Companies and Intellectual Property Commission (CIPC). The establishment of Home Owners Associations, by contrast, is voluntary and not prescribed by a specific law and may follow common-law principles. Voluntary Associations established by adopting a written Constitutions or the committees or persons managing such associations can formally register them as a non-profit company (NPC) with the CIPC. Despite their registration with CIPC, Home Owners Associations should not be confused with Bodies Corporates or Share Block Companies because Home Owners’ Associations are not established under the specific acts mentioned.

Entities established as Bodies Corporate and Share Block Companies automatically enjoy tax exemption under this provision of the Act, but Home Owners Associations must first lodge an exemption application and be approved by SARS to benefit from this exemption.

Annual Submission of Returns

Bodies Corporates and Share Block Companies must submit ITR14 returns annually and should make the relevant selection under the “Company Type” section to activate the exemptions.

Home Owners Associations that have not been approved by SARS must also submit ITR14 returns, but may not make the selection available to Bodies Corporates and Share Block Companies. This means that all the receipts and accruals of these entities, including levies, will be subjected to tax.

Home Owners Associations that have applied and obtained approval in writing from SARS must submit IT12EI returns annually. Home Owners Associations must also comply with the legislative requirements to maintain their Income Tax exemption, which includes the annual submission of returns and payments of any amounts due.

For further information, please refer to Interpretation Note 64 available on the SARS website.

Please click here for a Home Owner’s Association fact sheet

For information on How to Apply for Exemption, please refer to the TEI Webpage on SARS Website.

Queries and Escalations

To receive timely service and response to queries and escalations, taxpayers should take note of the two different, but complementary divisions in SARS, namely:

- Operations in the Gauteng North Region (formerly known as the Tax Exemption Unit or TEU) whose primary focus is to provide services to taxpayers.

- The Tax Exempt Institutions Segment (TEI Segment) which is responsible for oversight and systemic escalations.

Gauteng North Operations can assist taxpayers with:

- Progress on application as a tax exempt institution

- Progress on application for Section 18A status

- Confirmation of PBO status and number

- Confirmation of Section 18A status

- Re-issue of approval letters

- Following up on assessments and related disputes

- Debt and account maintenance (payments and refunds)

Queries related to the above matters should be sent to [email protected].

The Tax Exempt Institutions (TEI) Segment is responsible for overseeing the exempt institutions segment. The role of the TEI is to:

- Develop insights and understanding of the TEI segment to recognise their unique needs (including tax contribution).

- Identify risks specific to the segment.

- Develop engagement models to achieve voluntary compliance based on insights.

- Act as a segment owner and ambassador for the segment internally and externally.

The TEI Segment will offer segment specific engagement, communication, and education that will support increased compliance within the segment. TEI works closely with other SARS segments to deliver on:

- Tax product/system changes/improvements

- Service-channel changes/improvements

- Legislation or tax-regime change proposals

- Tax register improvements

- Revenue insights and enhancements

To engage the TEI Segment, please feel free to send an e-mail to [email protected].