Purpose

The purpose of this webpage is to assist employers with the completion of a Tax Directive Application form to obtain a Tax Directive (IRP3) before a lump sum can be paid to an employee.

The forms that will be addressed in this guide are:

- IRP3(a) – Application for a Tax Directive: Gratuities and Two-Pot Savings Withdrawals Benefit; and

- IRP3(s) – Application for a Tax Directive: Section 8A or 8C amount (Section 8A has been repealed with effect from 1 April 2026).

Scope

This webpage does not apply to the following tax directive applications:

- Request for a Tax Deduction Directive: Pension and Provident funds (Form A&D.)

- Request for a Tax Deduction Directive: Pension and Provident funds Transfer (Form B).

- Request for a Tax Deduction Directive: Retirement Annuity funds (Form C).

- Request for a Tax Deduction Directive: After Retirement and Death Annuity Commutations (Form E).

- For above mentioned forms refer to the ‘Guide to Complete the Tax Directive Application Forms’ on SARS website.

- Application for Tax Directive: Fixed percentage [IRP3(b)].

- Application for Tax Directive: Fixed Amount [IRP3(c)].

- Application for Tax Directive: Fixed percentage -Freelance Artist [IRP3(pa)].

- Request for a Directive – Variation in the Deduction / Withholding of Employees’ Tax [IRP3(q)]

- Request for a Directive: Provision for Doubtful Debt [IRP3(f)].

- Application by Non-Resident for a Tax Directive for Relief from South African Tax for Pensions and Annuities in terms of a Double Taxation Agreement (RST01).

General Information

Who must Complete and Submit a Tax Directive Application Form?

In some instances, an employer will pay a lump sum to an employee as a direct result of their employment or due to the employment being terminated. In addition, payments may be made by retirement funds to fund members from the two-pot retirement savings withdrawal component from 01 September 2024. Tax directives must be obtained for these types of payments.

To give effect to the two-pot retirement system the following components will be created:

- Vested Component.

- This is the total value of the member’s interest (per policy/contract if applicable) as at 31 August 2024, less 10% of that value, capped at R30 000 to be allocated to the Savings Component as once-off seed capital.

- The payment of the remaining balance in the Vested Component as a lumpsum benefit, will not be impacted by the two-pot retirement system. Members of preservation funds will still be entitled to the once off allowable withdrawal from the Vested Component.

- Savings Component.

- Effective from1 September 2024, one-third of the retirement fund contributions made by and on behalf of a member, will be allocated to the Savings Component and will be available for withdrawal by the member. This is in addition to the once off seed capital amount, which is 10% of the Vested Component, capped at R30,000, whichever is lower

- The member can withdraw up to the maximum value available in the member’s Savings Component. Withdrawals can be made once per tax year for pension and provident funds, or once per retirement fund, per tax year per policy/contract in respect of preservation funds and retirement annuity funds. These withdrawals from the Savings Component are called Savings Withdrawal Benefits.

- The member is allowed to withdraw the balance in the member’s savings component in the pension fund or provident fund if the membership in that fund is terminating, irrespective of whether the member has already accessed their one withdrawal for that specific tax year

- The member is allowed to withdraw the remaining balance in the member’s savings component per policy in the preservation fund or retirement annuity fund if the membership in that fund is terminating, irrespective of whether the member has already accessed their one withdrawal for that specific tax year.

- Upon retirement, any remaining balance in the Savings Component will not be subject to compulsory annuitisation and may be added to the retirement fund lump sum benefit to be taken in cash, if the member elects to do so

- Retirement Component.

- Starting 1 September 2024, two-thirds of the retirement fund contributions, made by or on behalf of a member, will be allocated to the Retirement Component. This component will be used to pay the member a pension or purchase an annuity and/or a living annuity upon retirement, subject to certain exceptions.

- This amount cannot be taken as a lump sum if the member terminates membership in the fund before retirement as a result of resignation, dismissal, withdrawal or retrenchment and must be transferred to another fund.

From 11 September 2025 a fund can submit a savings withdrawal benefit tax directive application for members that are not SA tax residents with a valid SA tax number who require a DTA to be taken into consideration.

Employers are required in terms of paragraph 9(3) of the Fourth Schedule to the Income Tax Act No.58 of 1962, as amended (‘the Act’) to apply for a Tax Directive in respect of any lump sum payable by way of a severance benefit, gratuity or any other amount.

- An employee cannot complete and submit an IRP3(a) or IRP3(s) Tax Directive Application form.

- Tax Directives completed by the employee in their personal capacity should not be accepted by the employer. Only the employer can complete the tax directive application form and apply for tax directives on behalf of the employee.

SARS will prescribe the amount of employees’ tax that has to be withheld from the specific lump sum payment and subsequently paid over to SARS.

- The date of accrual, the annual remuneration on the tax directive application form and the reason selected will determine the tax treatment of the amount payable and the rate of tax to be used to calculate the employees’ tax

Employers have to submit a Tax Directive Application form irrespective of the amount payable

With effect from 22 April 2022 a reason ‘Severance benefit – Paid by a non-resident employer’ will be only available on the IRP3(a) tax directive application form on eFiling. This reason can only be used where a non-resident employer that is not registered in SA or has not appointed an Agent in SA and pays a lump sum as a result of termination of employment in terms of paragraph (c) of the definition of “severance benefit” in section 1(1) of the Act. The severance rates can only be calculated if a tax directive application is submitted. In this case the taxpayer’s tax practitioner will be able to submit a tax directive through eFiling to determine the employees’ tax payable, that has to be included in the taxpayer’s provisional tax payments.

- For more information regarding the submission of the income tax return since no IRP5/IT3(a) tax certificate for this lump sum will be available refer to the ‘Comprehensive Guide to The ITR12 Income Tax Return For Individuals – IT-AE-36-G05’ on SARS website.

In an instance where the employee exercises a share option (section 8A gain or section 8C amounts) or certain dividends, the amount must be included as remuneration in terms of paragraphs (e) and (g) of the definition ‘remuneration’ in the Fourth Schedule to the Act, read with paragraph 11A.

In terms of paragraph 11A(4) of the Fourth Schedule, the employer must ascertain from the Commissioner the amount to be deducted or withheld from:

- section 8A gains (Repealed effective 1 April 2026);

- amounts referred to in section 8C;

- amounts received or accrued by way of dividends in;

- paragraph (dd) of the proviso to section 10(1)(k)(i);

- paragraph (ii) of the proviso to section 10(1)(k)(i);

- paragraph (jj) of the proviso to section 10(1)(k)(i); or

- paragraph (kk) of the proviso to section 10(1)(k)(i).

Where to Obtain a Tax Directive Application Form?

The updated Tax Directive Application forms can be obtained through any of the following channels:

- eFiling:

- If your organisation is not registered as an eFiler, please log on to www.sarsefiling.co.za to register and for assistance refer to the guide: ‘How to Register for eFiling and Manage Your User Profile’. Once the employer is registered as an organisation on eFiling the tax directive applications can be submitted through eFiling.

- Electronically (via an Interface)

- An employer can register as an interface agent or use established interface agents to capture the application forms online. The interface agent will submit the data as required by SARS to process the Tax Directive applications.

- The interface specification ‘IBIR-006- Tax Directive and the INF001 form to register to get access to SARS Interface are on SARS website.

- To submit Tax Directives in ‘bulk’ the employer must register as an interface agent (Complete INF001) and set up their system to submit the applications in bulk.

- The SARS website www.sars.gov.za

- The latest version of the manual (hard copy) application forms is available.

- The updated manual forms on the SARS website must only be used for a manual tax directive applications in extreme circumstance where the employer could not obtain a tax directive electronically and there is evidence of previous rejected submission. If a rejected submission could not be found on the SARS system the tax directive application form will be sent back with a request to submit the tax directive application through eFiling or an Interface Agency.

- The latest version of the manual (hard copy) application forms is available.

How to Submit a Tax Directive Application Form?

A completed application form can be submitted through any of the following channels:

- eFiling: Registered eFiling Employers can complete the tax directive forms online and obtain the directive once the application has been processed or view the reason the application was declined.

- Electronically: Through the employer’s own interface or use established interface agency.

- Email: Only in extreme circumstance where the employer cannot obtain a tax directive through eFiling or an Interface Agency can the employer email the hardcopy IRP3(a) or IRP3(s) to [email protected] as instructed by a SARS official Additional information is available on SARS website under ‘Contact Us’. The tax directive application will be returned if there is no declined tax directive application on the tax directive system.

Completing the Tax Directive Application Form

The layout of the application form referred to in this webpage is based on the manual application form available on SARS website. The information in this webpage is also applicable to the completion of the electronic application forms.

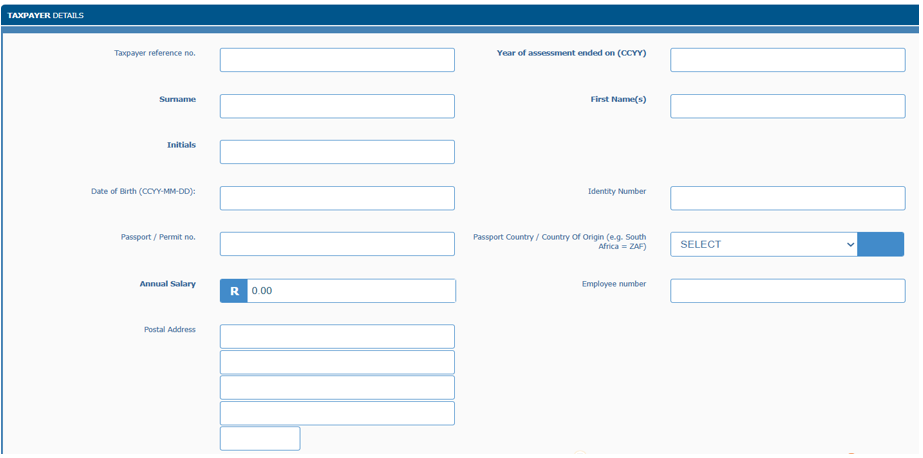

Taxpayer Details

This part of the form is generic to the IRP3(a) and IRP3(s) Tax Directive Application forms.

Under the ‘Taxpayer Details’ container provide the personal details of the employee who will receive the lump sum payment.

- The information in this container must be similar to the information used to issue an IRP5/IT3(a) tax certificate for the lump sum amount paid.

Taxpayer’s Reference Number:

This number is also referred to as income tax reference number and is allocated by SARS to the taxpayer when registering for income tax purposes. This number must also be reflected on the IRP5/IT3(a) tax certificate.

- The income tax reference number can only start with and 0, 1, 2 or 3 and must have 10 digits.

- The error message ‘Invalid reference number for applicant’ or ‘Contact SARS – Tax No on application differs from Client DB’ (data base) will be displayed where:

- The employer has used the incorrect income tax number on the tax directive application form;

- The employee has more than one active income tax reference number; or

- The identity (ID) number on the tax directive application form does not correspond with the ID number on SARS’s system.

- Where an employee has registered for Income Tax purposes, an income tax reference number was issued and the employer submits the tax directive application form without the income tax reference number, the SARS tax directive system will decline the application.

- The income tax reference number is mandatory and must be provided where the directive reason is ‘Savings Withdrawal Benefit’. This applies to all taxpayers, including minors and non-South African Tax residents.

- The employee/member must provide the employer/fund with the correct income tax reference number. The employee / member may be required to register for tax to obtain this number, if not registered, where the reason for the directive is “Savings Withdrawal Benefit”. The member can use the following channels to apply for a tax number

- Register on SARS Online Query System (SOQS) on the following link: Use our Digital Channels | South African Revenue Service (sars.gov.za).

- Register using SARS WhatsApp number 0800 11 7277.

Year of assessment ended on (Tax Year)

This is the period commencing on 1 March of a particular year to the end of February of the following year.

- The date of accrual will determine the ‘Year of Assessment’ on the IRP5/IT3(a) tax certificate and must fall within the ‘Year of assessment ended on’ or the ‘Tax year’

- The date of accrual must fall within the year.

- For example, if the date of accrual is 25 April 2025 the ‘Tax year’ or ‘Year of assessment ended on’ will be 2026-02-28. The tax year on the Tax Directive will be 2022 and the ‘Year of assessment’ on the IRP5/IT3(a) tax certificate must be 2026.

- If the date of accrual is 21 February 2025 on the tax directive application form and the tax directive application form was submitted on the 14th of March 2025, the ‘Tax year’ or ‘Year of assessment ended on’ will be 2025-02-28 (2025) on the tax directive application form and the ‘Transaction year’ on the IRP5/IT3(a) tax certificate will be 2026 due to the fact that the PAYE indicated on the tax directive was and could only be paid over to SARS after the directive was received on 14 March 2025. The ‘Year of Assessment’ on the IRP5/IT3(a) certificate must be 2025 as the date of accrual is 21 February 2025 that falls within the 2025 year of assessment and the ‘Transaction Year’ must be 2026 when the PAYE was paid over to SARS.

- In the above scenario the Employer has to provide the taxpayer with a manual IRP5/IT3(a) tax certificate within 14 days after the payment of the lump sum, to enable the taxpayer to submit the 2025 return. The certificate will not be prepopulated on the taxpayer’s tax return because the final certificate will only be submitted to SARS when the employer submits the bi-annual reconciliation in October 2025 for the 2026 ‘Transaction Year’.

- Therefore, the taxpayer has to manually add this certificate (increase the number of certificates on the form wizard) on the tax return to avoid the rejection of the return and to enable SARS to allow the PAYE on the certificate as a PAYE deduction.

- Even if the bi-annual reconciliation was submitted when the taxpayer submitted the annual return, the IRP5/IT3(a) tax certificate will not prepopulate on the return, the taxpayer has to manually add the certificate to the return by increasing the number of certificates. A blank certificate will be available, and the taxpayer must capture the IRP5/IT3(a) tax certificate detail including the directive number to avoid the rejection of the return.

Taxpayer’s personal details

- Surname: This is a mandatory field.

- Use the surname as contained in the identity document or passport.

- First name and other name: This is a mandatory field.

- Enter the employee’s name(s). Use the name(s) as contained in the identity document or passport.

- Do not use nicknames to avoid the tax directive being rejected.

- The names must correspond with the information on SARS’s records.

- The “Initials” are mandatory for electronically submitted application forms and must correspond with the names.

- Date of birth:

- This is a mandatory field.

- The date of birth must correspond with the first six digits of the ID number where the ID number is provided.

- If a passport/permit/visa/dompass number is used in the ‘Other Identification’ field the date of birth must correspond with the date of birth on the passport.

- Identity number:

- This is a mandatory field.

- The ID number must correspond with the latest issued identity document or identity card issued by the South African Department of Home Affairs.

- One of the reasons for the rejection ‘Income tax reference number invalid for applicant’ can be due to the ID number on the application form not matching the ID number on SARS’ records. Employer is using the incorrect tax number or captured the incorrect ID number.

- Passport / Permit no.

- This other ID number must only be completed where the taxpayer does not have a South African ID number.

- The other ID number can be a passport/permit/visa/dompass number.

- If the taxpayer is registered for Income Tax, the “Passport / Permit no.” on the tax directive application form must match the other identification number that the taxpayer has used to register for Income Tax with SARS.

- If the passport number has changed and the current passport number differs from the passport number on SARS’s records, the taxpayer must first contact SARS to update the passport number on the taxpayer’s registered details before the application form can be submitted.

- If the taxpayer is an Asylum Seeker, the Asylum Seeker Permit Number must be entered in the ‘“Taxpayer other ID number” field.

- The resident country’s ID number can be used if the employee does not have a passport.

- Passport Country / Country of Origin (e.g. South Africa = ZAF)

- Only mandatory if the passport / permit no. field is used and the application form is completed on eFiling.

Annual remuneration:

The annual remuneration field is mandatory and where the reason is “Savings Withdrawal Benefit”, where it is optional. For a Savings Withdrawal Benefit a Nil amount will be accepted.

- The term remuneration income is defined as follows:

- For members who are only in employment: “remuneration” as defined in the Fourth Schedule in respect of all employers; or

- For members who are only in employment: the “balance of remuneration” as set out in par 2(4) of the Fourth Schedule in respect of all employers; or

- For anyone else, “taxable income” as defined in section 1 of the Income Tax Act.

- Annual remuneration means all income from employment, an insurer or retirement fund, i.e. salary remuneration, emoluments, wages, bonus, leave pay, fees, gratuities, commission, pension, overtime payments, stipend, allowances and benefits annuities, compensation, honorarium etc.

- The annual remuneration must exclude the amount on the tax directive application form to be processed, for example the severance benefit amount, the leave payment, CCMA award, savings withdrawal benefits etc.

- If the annual remuneration amount is not completed correctly, the tax calculation will be incorrect, where the annual payment / bonus calculation is used to determine the tax payable. Incorrect completion of the annual remuneration might cause financial hardship for the employee on assessment.

- It is the responsibility of the employee/fund member to provide the employer/fund with all the relevant information that will enable the employer/fund to capture the correct annual remuneration on the application form.

- If the employee has terminated employment with the employer that is applying for the tax directive, and the employer is unable to obtain the relevant employee’s current annual remuneration data, the employer must use the annual remuneration of the employee as at the date of termination of employment, annualised for the full year of assessment.

- Where the tax directive reason is ‘Savings Withdrawal Benefit’ and no annual remuneration amount is provided to the fund, a nil amount will be accepted on the application. This field may not be left blank.

Employee Number/Policy Number:

- The policy number is only mandatory for ‘Savings Withdrawal Benefit’ tax directive applications (Policy number).

- The Employee number is only mandatory if reason is ‘Backdated (Antedated) salaries and/or Pensions’.

Residential address and postal code:

- This field is only available on the IRP3(s).

- The Residential address and postal code fields are mandatory.

- Provide both the employee’s residential address and the postal code.

- Do not use symbols or other characters in the address field. Only complete numerical and alphabetical characters.

Postal address and postal code:

- This field is optional on IRP3(a) if the reason for the tax directive is “Savings Withdrawal Benefit”.

- These fields are mandatory on the IRP3(s) and can be the same as the residential.

- Provide both the employee’s postal address and postal code.

- Do not use symbols or other characters in the address field. Only complete numerical and alphabetical characters.

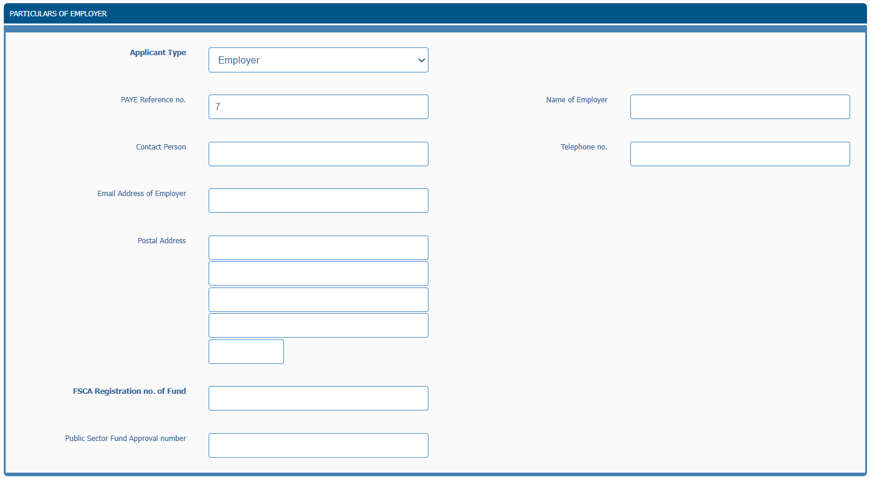

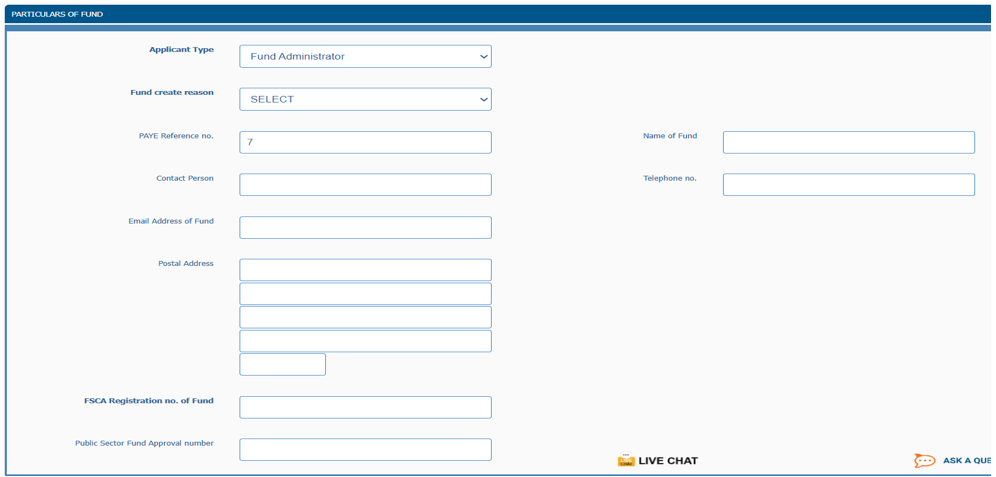

Particulars of the Employer/Fund

- This part of the form is generic to the IRP3(a) and IRP3(s) Tax Directive Application forms where the employer is the applicant type.

- This part of the form is only applicable to the IRP3(a) if the Fund Administrator is the applicant type.

Applicant Type

Select one of the following:

- Employer; or

- Fund Administrator.

PAYE Reference number

The Employer’s PAYE number is mandatory.

- This number starts with a 7 and consists of 10 digits. This is the Pay-As-You-Earn (PAYE) reference number issued by SARS when the employer registers for PAYE with SARS.

- The tax liability on the tax directive must be paid over to SARS with reference to this number and the employer must issue an IRP5/IT3(a) tax certificate.

- Paragraph 13(1) of the Fourth Schedule prescribes that an employer must furnish an employee, to whom remuneration is paid or has become payable and from which employees’ tax in respect of a tax period was deducted or withheld, with an IRP5/IT3(a) certificate within the prescribed period.

- The prescribed period in terms of paragraph 13(2) is fourteen (14) days after an employee has left the employer’s service or 60 days after the end of that year of assessment if that person remains an employee of the employer.

In instances where a non-resident employer pays a retrenchment severance lump sum to an SA tax resident for service rendered in SA, and the reason ‘Severance Benefit – Paid by a non-resident Employer‘ is selected, the employer’s PAYE is not compulsory

Name of the employer:

This field is mandatory if applicant type is ‘Employer’.

- Enter the name of the employer paying the lump sum amount.

Name of the Fund:

This field is mandatory if applicant type is ‘Fund Administrator’.

- Enter the name of the fund administrator paying the lump sum amount

Contact person:

- This field is mandatory.

- Provide the name of the person to be contacted when more information regarding the tax directive application is required.

Contact person’s telephone number:

- Provide the telephone number of the person to be contacted when more information regarding the tax directive application is required.

The employer/fund e-mail address:

- It is a mandatory field and must contain an “@” sign and a domain.

The employer/fund business address and postal code:

Provide the employer’s business address.

- Do not use symbols or other characters in the address field. Only complete numerical and alphabetical characters.

The employer/fund postal address and postal code:

This address is mandatory.

- Provide the employer’s postal address.

- Do not use symbols or other characters in the address field. Only complete numerical and alphabetical characters.

- This address is used to post the manual tax directive if the tax directive application form was submitted manually

Fund specific particulars

Where the reason “Savings Withdrawal Benefit” is selected, the applicant type must be a “Fund Administrator” on the IRP3(a).

FSCA registration

If the fund created reason is “Approved fund”, the Financial Sector Conduct Authority (FSCA) registration number is mandatory.

- To avoid the delay in the issuing of the tax directive ensure that the correct FSCA number is used, that the number is in the correct format and corresponds with the name of the fund provided (Refer to the ‘Active Fund’ list on the FSCA website). For Active Funds: – Home / Regulated Entities / List of Regulated Entities and Persons / Retirement Fund / Registered Active Funds. Do not use the ‘Search’ function to populate this field because the spelling could be different.

- This is the registration number, as allocated by the FSCA. The number must be provided in the correct format 12/8/0000000/999999, where 0000000 is the registered umbrella fund number and must consist of 7 digits. The 999999 represents the participating employer number and must be replaced with the correct participating employer number.

- In cases where the ‘FUND NO.’, on the FSCA list, is less than 7 digits, populate the rest of the field with ‘0’ before the number, e.g. where the FSCA registration number is 12/8/123 capture the registration number as 12/8/0000123/000000. (Refer to the ‘Registered Active Funds’ list on the FSCA website. Do not use the ‘Search’ function to populate this field because the spelling could be different.)

- If the Fund is a free-standing fund (not a type-A umbrella fund or a retirement annuity fund) the last 6 digits must be zeroes and the participating employer name must be blank. The number must be entered with the ‘/’.

- The last 6 digits of a retirement annuity fund will always be 6 zeroes e.g., 12/8/0000222/000000.

- An error message ‘4187 – Invalid format of FSCA registration number’ and or ‘Participating employer name must be provided’ will be displayed where:

- The FSCA number is not in the correct format;

- Where the last 6 digits are greater than ‘0’ and no ‘Participating employer name’ was entered the error message ‘4555 -The Fund Name provided does not match the FSCA database’ will be returned if:

- The name entered in the ‘Registered Name of Fund’ field or the name of the ‘Participating Employer’ submitting the tax directive application does not match the FSCA list, (including special characters, spaces, numbers, etc.);

- The name of the receiving fund or the name of the participating employer receiving the benefit does not matching the FSCA list, (including special characters, spaces, numbers, etc.); or

- The FSCA registered number provided does not match the fund name on the FSCA list.

Fund Approval number

If the fund create reason is “Public Sector Fund”, the Fund approval number or FSCA registration number is mandatory.

- The fund approval number must be blank if the Fund is an approved fund.

- Only public sector funds that are not registered with the FSCA must use the Fund approval number.

- Where the Public Sector Fund completes the approval number, the FSCA registration number field must be blank.

- The Fund approval number format is 18204 (followed by 6 digits) e.g. 18204000909.

- If the public sector fund is registered with the FSCA, the FSCA registration number (previously FSB) must be used. Refer to paragraph ‘FSCA registration number’ in this webpage below.

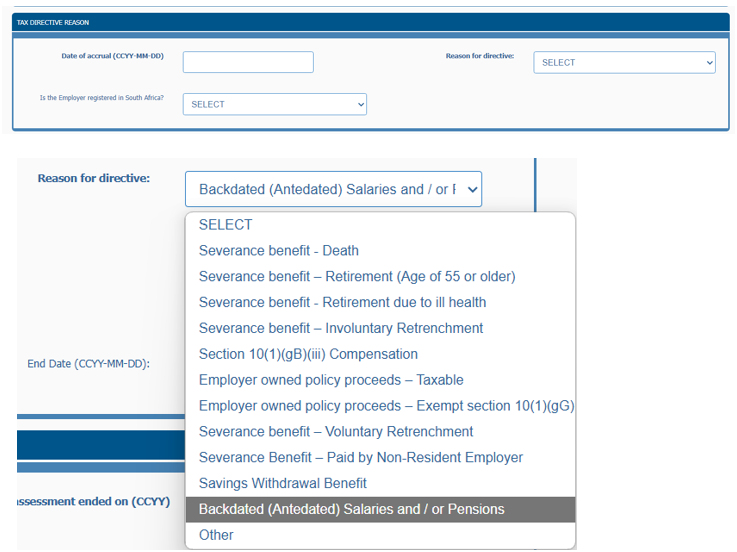

IRP3(A) Application Form – Tax Directive Reason

- This part of the application form is not generic, although certain fields are generic but will be dealt with under each application form type.

- In this part of the application form, the employer has to indicate the reason(s) for submitting the tax directive application. The reason indicates why the lump sum / amount is payable.

- The ‘Reason for directive’ selected on a tax directive application form will determine the applicable rate of tax that must be applied to the taxable portion of the amount payable by the employer.

- Therefore, only one reason per application form can be used.

- Leave payments and pro-rata bonus fields must not be completed if one of the ‘Severance benefit’ fields are selected as different tax rates are used to determine the tax payable.

- f the reason field ’Other’ is selected, a list of amounts applicable can be provided under ‘Other (Specify other payment separately)’.

- Leave payment and pro-rata bonus fields can be completed on one application form and can be included with the amounts ‘Other (specify other payment separately)’. However, the source code 3907 must be reflected on the IRP5/IT3(a) tax certificate and only the total amount on the directive must be entered on the IRP5/IT3(a) tax certificate.

Date of accrual (CCYYMMDD):

The date of accrual is a mandatory field and must be completed in order to comply.

- The accrual date is the date the benefit accrues to the employee, e.g. the date of death, the date of retirement, etc.

- If an amount is payable after date of death the date of accrual for that taxpayer cannot be after the date of death. The date of accrual must then be equal to the date of death.

- If the reason “Savings Withdrawal Benefit” is selected, then the date of accrual may not be before 01 September 2024.

- Where more than one tax directive has to be submitted per employee, add or subtract one day from the ‘date of accrual’ on the original submitted tax directive application to avoid the application being declined as a duplicate directive application.

- The date of accrual (not the date when amount will be paid) must be within the relevant tax year / year of assessment.

- This date will determine the ‘Year of Assessment’ on the IRP5/IT3(a) tax certificate and must fall within the ‘Year of assessment ended on’. The date of payment of the PAYE will indicate the transaction year on the IRP5 certificate.

- For example, if the date of accrual is 25 April 2025 the ‘Tax year’ or ‘Year of assessment ended on’ will be 2026-02-28. The ‘Tax Year’ on the Tax Directive will be 2026 and the ‘Year of assessment’ on the IRP5/IT3(a) tax certificate must be 2026.

Mark the applicable reason for the directive application request with an X:

Below is a detailed description of each available reason on the tax directive application form. On the eFiling system, a drop-down list of reasons for the directive will display, only one reason may be selected

The reason for the directive is a mandatory field and the employer must select a reason for the tax directive application.

- The employer must analyse the nature of the lump sum payment(s) that will be made to the employee and select the appropriate reason(s) provided on the tax directive application form.

- Below is a detailed description of each available reason on the application form; and

- A diagram (under each reason) showing the corresponding payment / amount field to be completed on the form based on the reason selected.

- The reason selected will determine the tax rate applicable or if the amount is exempt from tax.

Severance benefit – Death

This option must be used for a lump sum amount paid as a direct result of termination of employment due to death only.

- Leave pay and notice payments – a separate directive application must be completed. Refer to the reason ‘Other’ as well as ‘Date of Accrual’.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form4.png)

- The source code to be used for dates of accruals after 01 March 2011 for the gross amount is code 3901 on the IRP5/IT3(a) tax certificate. The code 4115 must be used for the employees’ tax withheld in terms of the tax directive.

- The lump sum amount will be taxable in terms of the applicable severance benefits tax rates.

Severance Benefit – Retirement (Age of 55 or older)

This is a lump sum paid as a direct result of termination of employment due to the employee or office holder having reached the age of 55 years at the time when the amount is received or accrued.

- If this option is selected then the person must be 55 years or older on the date of accrual

- Therefore, if this benefit is payable to a person under 55 years of age, the SARS tax directive system will decline the tax directive.

- The payment must be treated as normal income and the reason ‘Other’ with the description on the tax directive application form must be used on the IRP3(a) application form.

- In the ‘Specify the reason’ field indicate it is due to early retirement.

- Leave pay and notice payments – a separate tax directive application must be completed. These payments are taxed as normal income and do not qualify for the rates of tax applicable to severance benefits. Refer to the reason ‘Other’ as well as ‘Date of Accrual’.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form5.png)

- The source code to be used for dates of accruals after 01 March 2011 for the gross amount is code 3901 on the IRP5/IT3(a) tax certificate. The code 4115 must be used for the employees’ tax withheld in terms of the tax directive.

- The lump sum amount will be taxable in terms of the severance benefits tax rates applicable.

Severance benefit – Retirement due to ill health

Lump sum paid as a result of termination of employment due to ill health, injury or similar incapacity.

- This option may be used regardless of the employee’s age.

- For Leave pay and notice payments – a separate tax directive application must be completed. These payments are taxed as normal income and do not qualify for the rates of tax applicable to severance benefits. Refer to the reason ‘Other’ as well as ‘Date of Accrual’.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form6.png)

- The source code to be used for dates of accruals after 01 March 2011 for the gross amount is code 3901 on the IRP5/IT3(a) tax certificate. The code 4115 must be used for the employees’ tax withheld in terms of the directive.

- The lump sum amount will be taxable in terms of the severance benefits tax rates applicable.

Severance benefit – Involuntary retrenchment

The reason must only be used where the employer is planning to stop trading or due to a general reduction of staff. This reason cannot be used for dismissals or restructuring.

- The application must be in terms of paragraph (c) of the definition of “severance benefit” in section 1(1) of the Act.

- This option may be used regardless of the employee’s age.

- Leave pay and notice payments – a separate directive application must be completed. These payments are taxed as normal income and do not qualify for the rates of tax applicable to severance benefits. Refer to the reason ‘Other’ as well as ‘Date of Accrual’.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form7.png)

- The source code to be used for dates of accruals after 01 March 2011 for the gross amount is code 3901 on the IRP5/IT3(a) tax certificate. The code 4115 must be used for the employees’ tax withheld in terms of the directive.

- The lump sum amount will be taxable in terms of the severance benefits tax rates applicable.

Severance benefit – voluntary retrenchment

The reason must only be used where a lump sum is paid as a result of restructuring or other termination of employment in terms of paragraph (c) of the definition of “severance benefit” in section 1(1) of the Act and the employee voluntarily leaves the employer’s employment before the involuntary retrenchments are implemented.

- Leave pay and notice payments – a separate directive application must be completed. These payments are taxed as normal income and do not qualify for the rates of tax applicable to severance benefits. Refer to the reason ‘Other’ as well as ‘Date of Accrual’.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form8.png)

- The source code to be used for the gross amount is code 3901 on the IRP5/IT3(a) tax certificate. The code 4115 must be used for the employees’ tax withheld in terms of the directive.

- The lump sum amount will be taxable in terms of the severance benefits tax rates applicable.

Section 10(1)(gB)(iii) Compensation

From 1 January 2006, if any lump sum compensation is paid by the employer as a direct result of a work-related death of an employee, these payments must be in terms of the Compensation for Occupational Injuries and Diseases Act, 1993. They must further meet the requirements of section 10(1)(gB)(iii) of the Act.

- The compensation will qualify for an exemption in terms of section 10(1)(gB)(iii), to the extent that the compensation

- Was paid in addition to any compensation paid in terms of the Workmen’s Compensation Act, 1941 or the Compensation for Occupational Injuries and Diseases Act, 1993;

- Does not exceed an amount of R300 000; and

- Was paid by the employer of that person.

- A tax directive must be obtained from SARS for the full benefit payable. The applicable exemption shall be determined by SARS on the processing of the tax directive application.

Such amount which becomes payable in consequence of / or following the death of a person must be deemed to accrue to such person immediately prior to his or her death.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form9.png)

- The source code to be used for dates of accruals after 01 March 2011 for the gross amount is code 3922 on the IRP5/IT3(a) tax certificate. Tax certificate reason code 04 ‘Non-taxable earnings (including nil tax directives)’ must be used in the ‘Reason for no tax deducted’ field if this amount is the only amount on the IRP5/IT3(a) tax certificate.

Employer owned policy proceeds – Taxable

This is a lump sum paid as a direct result of an insurance policy, which the employer enters into for the benefit of employees or directors, or for their dependants / nominees.

- A tax directive application must be submitted:

- Where the policy proceeds are received by the employee, or the dependant or nominee of the employee; or

- Where the policy proceeds will be received directly (from the insurer) or indirectly (from the employer).

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form10.png)

- The source code to be used for dates of accruals after 01 March 2012 for the gross amount is code 3907 on the IRP5/IT3(a) tax certificate. The code 4102 must be used for the employees’ tax withheld in terms of the tax directive.

Employer owned policy proceeds – exempt s10(1)(gG)

The employee will be entitled to an exemption in terms of section 10(1)(gG) to any employer owned policy proceeds if:

- The premiums payable by the employer were included in the employee’s gross income and taxed as a fringe benefit ; or

- In the case of employer owned income protection risk policy, if the premiums were allowed as a deduction to the employee, the exemption will not be applicable to the employee.

NOTE: An employer is required to apply for a tax directive if any lump sum amount in respect of an employer owned policy proceeds is payable to an employee.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form11.png)

- The source code to be used for dates of accruals after 01 March 2012 for the gross amount is code 3908 on the IRP5/IT3(a) tax certificate. The tax certificate reason code 04 ‘Non-taxable earnings (including nil tax directives)’ must be used in the ‘Reason for no tax deducted’ field if this amount is the only amount on the IRP5/IT3(a) tax certificate.

NOTE: Source code 3908 must only be used where the proceeds are payable to the employee and the policy premiums were included in the gross income of the employee as a fringe benefit and the premiums were not allowed as a deduction to the employee.

Severance benefit – paid by a non-resident Employer

This reason can only be used where a non-resident employer, that is not registered in SA for PAYE purposes, that did not appoint an agent in SA and is paying a lump sum as a result of termination of employment (excluding dismissal and or where a contract ends) in terms of paragraph (c) of the definition of “severance benefit” in section 1(1) of the Act.

- The non-resident employer will not be able to submit a tax directive application therefore, the taxpayer’s tax practitioner will be able to submit a tax directive application through eFiling.

- A taxpayer who did not appoint a tax practitioner can request SARS to capture a tax directive application on behalf of the non-resident employers.

- ONLY in a case where a non-resident is paying a severance benefit, can the employee complete the hard copy IRP3(a) tax directive application available on the SARS website. A letter from the non-resident employer clearly indicating the retrenchment benefit amount, must be submitted with the tax directive application form.

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/form12.png)

The lump sum amount will be taxable in terms of the severance benefits tax rates applicable and a tax directive (IRP3e) will be issued with source code 3925 and will reflect the tax amount that the taxpayer must include in the provisional tax return (IRP6).

- For more information on how to declare the Lump sum amount on the ITR12 return where no IRP5/IT3(a) tax certificate for severance lump sum is available, refer to the ‘Comprehensive Guide to the ITR12 Income Tax Return For Individuals – IT-AE-36-G05’ on SARS website.

NOTE: Source code 3925 cannot be used on an IRP5/IT3(a) tax certificate by any other employer. A tax certificate will fail the PAYE validations.

Leave pay and any notice payment payable by the non-resident employers should not be included in the severance benefit lump sum payment. A separate tax directive application is also not required. The leave pay and notice payment must only be included in the ITR12 income tax return as normal income.

Savings Withdrawal Benefit – Two Pot Retirement System

The reason “Savings Withdrawal Benefit” may only be used by a pension fund, pension preservation fund, provident fund, provident preservation fund or retirement annuity fund when paying Savings Withdrawal Benefits from the savings component.

An IT88L stop order will be issued when there is debt on the taxpayer’s account. SARS may allocate all of the amount payable after tax to the debt that the taxpayer is owing. It is therefore possible that the taxpayer may receive nothing from the Savings Withdrawal Benefit as it could all be allocated to debt.

- If there is a valid deferment of payment arrangement or a suspension of payment (active or pending) in place an IT88L stop order will not be issued.

- If there is no valid deferment of payment arrangement or a suspension of payment (active or pending) in place an IT88L stop order will be issued.

There will be no tax cancellation of the Savings Withdrawal Benefit tax directive due to the tax amount being higher than the member expected or due to the member not being aware of the tax debt on their account.

It is the members responsibility to understand the tax implications of the benefit payment before submitting an application for the payment of the benefit.

- A Savings Withdrawal Benefit tax directive calculator (under Lump Sum Calculator) is available to a member who is registered as an eFiler or the member’s tax practitioner, to determine the tax implications before a request / an option form is submitted to the Fund Administrator in order to mitigate requests for tax directive cancellations where the taxpayer is unhappy with the amount of tax withheld and/or amount used to pay off debt, due to the cancellation policy as set out in paragraph ‘Cancellation of Tax Directives’ of this webpage. The lump sum calculator is available on the following channels and will provide the member with the tax amount payable and debt outstanding that will be deducted from the Savings Withdrawal Benefit.

- Log on to their eFiling profile link eFiling (sarsefiling.co.za).

- Request on SARS Online Query System (SOQS) under ‘Two Pot Tax Calculator’’ on the following link: Use our Digital Channels | South African Revenue Service (sars.gov.za).

- Request using SARS WhatsApp number 0800 11 7277.

- SARS Mobi-app.

- Below is an example of the calculation results that may be received when the member used the channels provided.

andIRP3(s)Forms/newForm3.png)

If the Fund / Fund administrator offers this service to members, the fund may also first request for a simulated tax directive in order to determine the exact amount of tax that the taxpayer will be liable to pay on the Savings Withdrawal Benefit. This can be done before the fund submits the actual tax directive in order to mitigate requests for tax directive cancellations where the taxpayer is unhappy with the amount of tax withheld and/or amount used to pay off debt, due to the cancellation policy as set out in paragraph ‘Cancellation of Tax Directives’ of this webpage. Please note that the IT88L will not be provided with the tax directive simulator results. However, a ‘Two-Pot Tax calculator’, has been made available for the fund to request a two-pot simulated calculation that will provide both the tax amount payable and debt amount that will be deducted from the Savings withdrawal Benefit.

For illustrative purposes, see examples below:

- Example 1: No Debt outstanding

andIRP3(s)Forms/newForm5.png)

- Example 2: Debt outstanding

andIRP3(s)Forms/newForm6.png)

- Example 3: Debt outstanding higher than amount receivable

andIRP3(s)Forms/newForm8.png)

Reason to be selected and the amount field to be completed:

andIRP3(s)Forms/newForm9.png)

Below is the amount field to be completed on eFiling

andIRP3(s)Forms/newForm10.png)

A new container ‘Non-Resident Service Rendered Inside the Republic [Section 9(2)(i)]’ has been added to allow for a DTA or services rendered outside of the country to be taken into account of the tax directive.

- The two questions below under ‘Taxpayer details’ must be responded to before the non-resident container is completed.

The container ‘Non-Resident Service Rendered Inside the Republic [Section 9(2)(i)]’ must be completed if the DTA must be taken into account even if the non-resident did not render any services in SA.

Complete the ‘Non-Resident Service Rendered Inside the Republic [Section 9(2)(i)]’ container as follows:

- Select ‘Yes’ or No’ to the question ‘Were any services rendered inside / outside the Republic during the period of membership of the fund?’

- If ‘Yes’ is selected enter the required information for the following fields:

- Total number of months services were rendered while contributing to fund;

- Total number of months services were rendered inside of the Republic while contributing to fund; and

- Total number of months services were rendered outside the Republic while contributing to fund.

- Where the Fund is satisfied that the DTA is applicable and the SWB should be fully exempted from tax in South Africa, a Nil amount of months must be captured under ‘Total number of months services were rendered inside of the Republic while contributing to fund’.

- The following documents must be attached:

- A certificate of residence; and

- detailed history of employment, on the letterhead of the employer. The detailed history of employment letter must clearly indicate the start day / month / year and an end day / month / year of employment and where the services were rendered while contributing to the fund.

- If this container is completed a case will be created for manual review by a SARS auditor.

The Savings Withdrawal Benefit amount will be treated as normal employment income, and it will be taxed using the annual payment / bonus calculation method including the allowable rebates. No retirement rates, exemptions or tax-free amounts will be used in this calculation.

- The tax directive will reflect source code 3926 and this code must be used on the IRP5/IT3(a) tax certificate. The source code 4102 must be used for the employees’ tax withheld in terms of the tax directive application and the tax directive number must be captured as well.

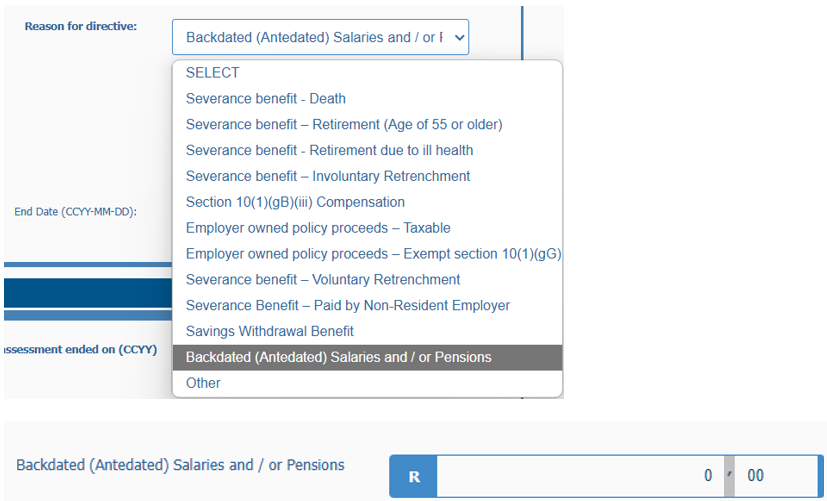

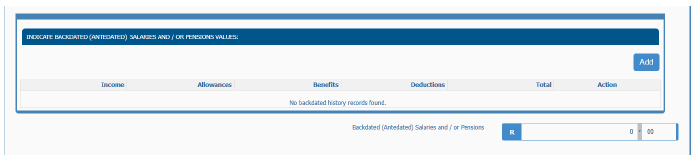

Backdated (Antedated) Salaries and/or Pensions

These are amounts that are paid in terms of Paragraph 9(3)(a) of the Fourth Schedule and section 7A and include a settlement agreement or arbitration award or court-order that relates to previous years where employees tax has accrued in the prior tax year(s).

If the selected directive application reason is ‘Backdated (Antedated) Salaries and/or Pensions’, only the amount field for “backdated salaries/pensions” must be specified. No other amount fields may be specified.

Reason to be selected and the amount field to be completed:

Provide a breakdown of the antedated salary and/or pension into the following cartegories:

- Income

- Allowances

- Benefits

- Deductions

Provide the start date and end date of the accrual period for the antedated salary and/or pension.

The directive will be declined for the following reasons:

- The date of accrual is before 1 March 2025;

- The backdated (Antedated) Salaries and/or Pensions amount has not been specified;

- Any other amount field has been specified;

- The end date of the accrual period is not the same as the date of accrual; and

- The start date of the accrual period is in the same year of assessment or greater than the year of assessment on the directive application.

The tax directive will reflect source code 3623 for local income and 3673 for foreign income and this code must be used on the IRP5/IT3(a) tax certificate. The source code 4102 must be used for the employees’ tax withheld in terms of the tax directive application and the tax directive number must be captured as well.

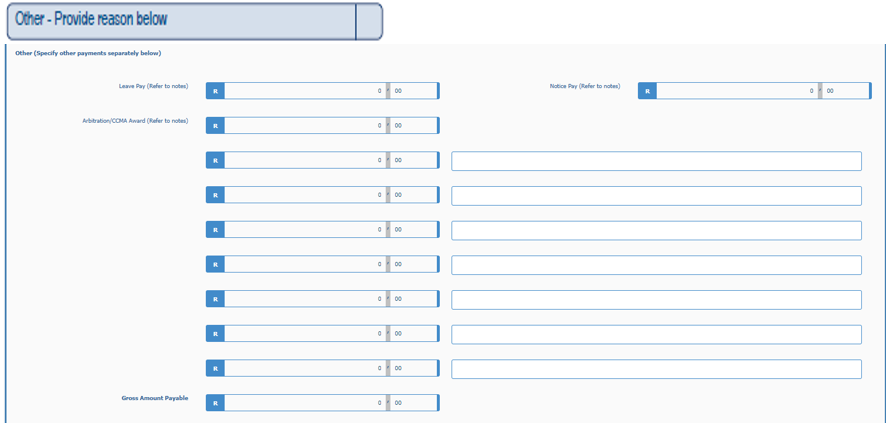

Other – provide reason below

This reason may be selected where the lump sum payment does not fall within the specified reasons as set out on the application form.

- This reason will include for example, amounts that are paid in terms of CCMA awards, leave pay, bonus payments, etc.

- From 12 April 2025, the reason ‘Other’ may not be used for Backdated (Antedated) Salaries and/or Pensions as a new reason ‘Backdated( Antedated) Salaries and/or Pension’ is available as a standalone selection on the form, see Backdated (Antedated) Salaries and/or Pensions above.

- Where the reason ‘Other’ is selected and the description is different from leave payment, a notice payment and Arbitration / CCMA Award; the specific description and the relevant amount should be captured in the required fields.

- If the tax directive reason ‘Other’ is used the amount will be treated as normal income and it will be taxed using the annual payment / bonus calculation method.

- From April 2021 the Arbitration / CCMA Award field will be available and is hard coded on the application form. The employer will not be able to use or add any ‘Other’ description or amount if an amount was entered next to ‘Arbitration / CCMA Award’.

Reason to be selected and the amount field to be completed:

- The above fields cannot be used if any of the severance benefit reasons are used since the tax calculations differ.

- This amount must not be included in the annual remuneration amount. Only include this amount in the annual remuneration amount where another payment has to be paid after this tax directive was issued, for example where a taxpayer has multiple contracts in the same fund from which they wish to withdraw a Savings Withdrawal benefit in the same tax year.

- The source code to be used for the gross amount on the IRP5/IT3(a) tax certificate must be obtained from either the ‘Guide for Employers in Respect of Employees’ Tax’ or from the ‘PAYE Business Requirement specifications’ to match the description used. The directive will reflect the generic source code 3907. The code 4102 must be used for the employees’ tax withheld in terms of the tax directive.

- Where the Arbitration / CCMA Award field was used,

![]()

- the tax directive will reflect source code 3608 and this code must be used on the IRP5/IT3(a) tax certificate. The code 4102 must be used for the employees’ tax withheld in terms of the tax directive.

NOTE: Source code 3901 must never be used if the reason on the tax directive application is ‘Other’. If source code 3901 was used and the directive reason was ‘Other’ the taxpayer’s ITR12 return will be rejected.

IRP3(s) – Application for a Tax Directive: Section 8A (repealed) or 8C Amount or Dividends Arising from Instruments under those Sections

- The IRP3(s) must be used for gains made in respect of rights to acquire marketable securities, and amounts in respect of the vesting of equity instruments.

- Section 8A of the Income Tax Act has been repealed effective 1 April 2026 as section 8C has modernised and consolidated the rules contained in section 8A for taxing equity instruments acquired due to employment.

Mark the applicable reason for the directive application request with an X

The employer must analyse the nature of the payment(s) that will be made to the employee and select the appropriate reason(s) provided on the tax directive application form.

Below is a detailed description of each available reason on the application form.

andIRP3(s)Forms/form15-2.png)

On eFiling the system will display a list and the correct reason must be selected:

andIRP3(s)Forms/form16.png)

Date of accrual (CCYYMMDD):

The date of accrual is a mandatory field and should be completed to comply.

- The accrual date is the date the benefit accrues to the employee, e.g. the date of death, the date of retirement, etc.

- In cases where an amount is payable after date of death, the date of accrual for that taxpayer cannot be indicated as after the date of death. The date of accrual must then be equal to the date of death.

- Where more than one tax directive must be submitted per employee, add or subtract one day from the ‘date of accrual’ on the original submitted tax directive application to avoid the application being declined as a duplicate directive application.

- The date of accrual (not the date when amount will be paid) must be within the relevant tax year / year of assessment

- This date will determine the ‘Year of Assessment’ on the IRP5/IT3(a) tax certificate and must fall within the ‘Year of assessment ended on’. The date of payment of the PAYE will indicate the transaction year on the IRP5 certificate.

- For example, if the date of accrual is 25 April 2021 the ‘Tax year’ or ‘Year of assessment ended on’ will be 2022-02-28. The tax year on the Tax Directive will be 2022 and the ‘Year of assessment’ on the IRP5/IT3(a) tax certificate must be 2022

Revenue gain i.r.o rights to acquire marketable securities in terms of section 8A (Repealed including source codes related to Section 8A)

Reason to be selected:

![]()

- Enter the amount next to ‘Gross value of gain / amount’.

- The gross value of the gain must be reflected under code 3707 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102.

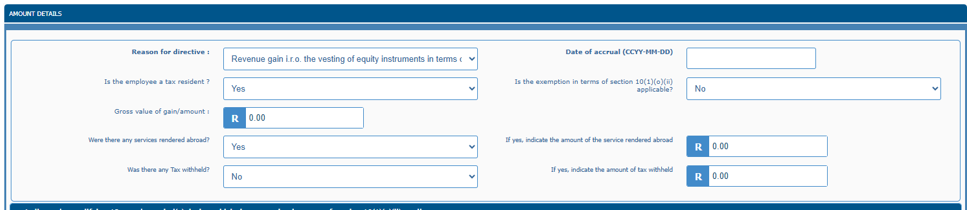

Revenue gain i.r.o the vesting of equity instruments in terms of section 8C

Reason to be selected:

![]()

- Enter the amount next to ‘Gross value of gain / amount’.

- The gross value of the gain must be reflected under code 3718 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102.

Revenue gain i.r.o the vesting of equity instruments in terms of section 8C

Reason to be selected:

![]()

- Enter the amount next to ‘Gross value of gain / amount’.

- The gross value of the gain must be reflected under code 3718 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102.

Gross value of gain / amount

![]()

- This is a mandatory field.

- The employer must enter the gross value of the gain or the dividend amount payable in terms of paragraph (g) of the definition ‘remuneration’ in the Fourth Schedule to the Act in the amount field.

Is the Employee a tax resident?

Select ‘Yes’ or ‘No’ to indicate if the application is for an employee who is a tax resident in terms of the definition of ‘resident’ in section 1(1) of the Income Tax Act.

- For more detailed information regarding ‘resident’ refer to Interpretation Note 3 – ‘Resident: Definition in relation to a natural person – ordinarily resident’ and Interpretation Note 4 – ‘Resident: Definition in relation to a natural person – physical presence test’ on SARS’s website.

If the response to this question is ‘Yes’ the next question is mandatory. The source period relating to the section 8A / 8C revenue gain can only be completed if the employee is a tax resident.

Is the exemption in terms of section 10(1)(o)(ii) applicable?

If the answer is ‘No’ to the question ‘Is the exemption in terms of section 10(1)(o)(ii) applicable?”. The new fields that must be completed will be displayed:

- Select ‘Yes’ or ‘No’ next to the question ‘Were there any services rendered abroad?’.

- If the answer is ‘Yes’ capture the amount relating to the services rendered abroad.

- The gross value of the gain will be reflected under code 3707 for section 8A and code 3718 for section 8C on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102. In addition, a foreign source code 3757 for section 8A and source code 3768 for section 8C will be reflected where the amount for services rendered abroad is specified.

- These changes will assist the employer to report the correct information when submitting the IRP5/IT3(a) tax certificate to SARS and will ensure that the taxpayer is able to submit their tax returns with no rejections due to incorrect source codes.

- Below is an example the IRP3e issued with the two source codes:

andIRP3(s)Forms/newForm11.png)

- Select ‘Yes’ or ‘No’ next to the question ‘Was any tax withheld?’.

- If the answer is ‘Yes’ to the question capture the amount of tax withheld.

- For the relief of double taxation, the taxpayer must still use the ‘IRP3(q) – Request for a Directive – Variation in the Deduction / Withholding of Employees’ Tax’ application form on eFiling to apply for the necessary relief.

If the answer is ‘Yes’ to the question ‘Is the exemption in terms of section 10(1)(o)(ii) applicable?’ at least one of the fifteen (15) qualifying period fields must be completed.

andIRP3(s)Forms/form21-1.png)

- The questions ‘Were there any services rendered abroad?’ and ‘Was any tax withheld? Will NOT be displayed.

- Indicate if the exemption in terms of section 10(1)(o)(ii) is applicable.

- If the exemption is applicable provide the ‘start date’ and ‘end date’ for each qualifying 12-month period in the source period where service was rendered outside SA.

- Start with the oldest period first and the dates must be chronological.

- On eFiling the system will only allow the capturing of the ‘Start date’ and ‘End date’ in the container ‘Indicate the qualifying 12 months period(s) during which the exemption in terms of section 10(1)(o)(ii) applies’ if the answer is ‘Yes’ to the question ‘Is the exemption in terms of section 10(1)(o)(ii) applicable?

- If the exemption is applicable provide the ‘start date’ and ‘end date’ for each qualifying 12-month period in the source period where service was rendered outside SA.

andIRP3(s)Forms/form22.png)

-

- Only the qualifying 12-months periods during the source period must be completed.

- The days from the ‘Start date’ to the ‘End date’ cannot be more than a 12-month period. The ‘End date’ must end a day before the ‘Start date’ of the next qualifying 12-months periods.

- The 12-months periods must fall within the source period. Refer to the field ‘Please provide source period relating to the section 8A / 8C revenue gain’:

- These fields must only be completed where service was rendered outside South Africa during the source period relating to the section 8A or 8C revenue gain

- The total days of these 12 month periods must correspond with the days in the ‘Number of work days outside SA during the source period’ field. If there is a difference in these days the application will be rejected with an error message ‘Outside SA days – 12 month period differs from source period totals’

- Where services were not rendered outside SA these fields must be blank.

- These fields are not applicable to the following reasons:

- Amounts in terms of par (dd) of the proviso to section 10(1)(k)(i) dividends;

- Amounts in terms of par (ii) of the proviso to section 10(1)(k)(i) dividends;

- Amounts in terms of par (jj) of the proviso to section 10(1)(k)(i) dividends; or

- Amounts in terms of par (kk) of the proviso to section 10(1)(k)(i) dividends.

- Only the qualifying 12-months periods during the source period must be completed.

andIRP3(s)Forms/form23.png)

Please provide source period relating to the section 8A / 8C revenue gain

The source period fields are mandatory if the employee worked outside SA during the source period.

- The number of workdays outside SA must be zero / blank if the answer is ‘No’ to the question ‘Is the exemption in terms of section 10(1)(o)(ii) applicable?’

The information in these fields must and will be used to determine the exemption under section 10(1)(o)(ii) applicable to the period where the service was rendered outside SA and is a summary of the qualifying 12-month period in the source period.

- The ‘Total number of workdays during above qualifying period’ and ‘Number of workdays outside SA during above qualifying period’ must fall within the source period.

- For old schemes entered into before and up to 2018 year of assessment where the ‘working days’ are not available the calendar days can be used. For schemes with a start date after 1 March 2017 only working days can be used.

- If the total number of all the fields ‘Number of workdays outside SA during above qualifying period’ (entered in the 12 month period fields), differs from the days entered in ‘Number of workdays outside SA during the source period’ field the application will be rejected with an error message ‘Outside SA days – 12 month period differs from source period totals’.

- For old schemes entered into before and up to 2018 year of assessment where the ‘working days’ are not available the calendar days can be used. For schemes with a start date after 1 March 2017 only working days can be used.

andIRP3(s)Forms/form24.png)

The above fields must only be completed if the employee has worked outside SA during the source period.

The fields on eFiling are greyed out and cannot be completed. The system generates the information according to what is captured in the container ‘Indicate the qualifying 12month period(s) during which the exemption in terms of section 10(1)(o)(ii) applies‘.

andIRP3(s)Forms/form25.png)

The following fields must also be completed if the answer is ‘Yes’ to the question ‘Is the exemption in terms of section 10(1)(o)(ii) applicable?’. At least one set of the following fields must be completed if one of the qualifying source period fields were completed:

- Year of Assessment in source period;

- Total workdays in source period during Year of Assessment

- Total workdays outside SA in source period during Year of Assessment

- Deemed accrual for sec 10(1)(o)(ii) calculation (Total workdays in yoa / Tot. workdays in source period X Gross gain amount);

- How much of the exemption was used during each year of assessment up to date of vesting?; and

- Portion of the gain qualifying for exemption ( workdays outside SA in yoa / Tot. workdays in source period X Gross gain amount).

andIRP3(s)Forms/form26.png)

- Year of Assessment in source period;

- The oldest year of assessment in source period must be completed first and the years must be chronological.

- Where the ‘Start date’ of the source period is 1 November 2019, the first year will be 2020 for ‘Year of Assessment in source period’.

- The oldest year of assessment in source period must be completed first and the years must be chronological.

- Total workdays in source period during Year of Assessment (YOA);

- The total number of days captured on for ‘Total workdays in source period during the YOA’ must correspond with ‘Total number of workdays during the source period’.

- If the days captured under question ‘Total workdays in source period during the YOA’ is more or less than the ‘Total number of workdays during the source period’ the application form will be rejected.

- The total number of days captured on for ‘Total workdays in source period during the YOA’ must correspond with ‘Total number of workdays during the source period’.

- Total workdays outside SA in source period during YOA;

- The total number of days captured under question ‘Total workdays outside SA in source period during the YOA’ must correspond with ‘Number of workdays outside SA during the source period’

- If the ‘Total workdays outside SA in source period during the YOA’ is more than the ‘Total workdays in source period during the YOA’ the application form will be rejected.

- The total number of days captured under question ‘Total workdays outside SA in source period during the YOA’ must correspond with ‘Number of workdays outside SA during the source period’

- Deemed accrual for sec 10(1)(o)(ii) calculation (Total workdays in YOA / Tot. workdays in source period X Gross gain amount);

- The total of all these fields must correspond with the ‘Gross value of gain / amount’ to avoid the rejection of the tax directive application.

- For application completed on eFiling, the system will determine the ‘Deemed accrual for sec 10(1)(o)(ii) calculation’.

- How much of the exemption (after 1 March 2020) was used during each year of assessment up to date of vesting?

- Pre 1 March 2020 the exemption must be null if the year of assessment is before 2021 year of assessment.

- The exemption cannot be more than R1.25 million from 1 March 2020.

- If the full exemption (R1.25 million) for the year of assessment was not utilised (salary and bonus) when the tax directive application is submitted, the difference must be entered in the next field under ‘Portion of the gain qualifying for exemption’.

- For example, if R750 000 was entered as the exempt amount that was used in the year of assessment, then the difference of R500 000 must be reflected in the ‘Portion of the gain qualifying for exemption’ amount field for that year. The two amounts must not be more than R1.25 million.

- Refer to 2021 year of assessment in the below example where the ‘Deemed accrual for sec 10(1)(o)(ii) calculation’ amount is R1 972 125.67, the exemption during the year used is R1 250 000.00, therefore the amount in the ‘Portion of the gain qualifying for exemption’ must be zero, even if the calculated exemption was R1 475 150.00 (187 / 250 x R1 972 125.67).

- Portion of the gain qualifying for exemption (Tot. workdays outside SA in YOA / Tot. workdays in source period X Gross gain amount)

- The total amount must be entered in the amount field for ‘Exempt amount of the gain / amount under section 10(1)(o)(ii)’.

Example:

- The source period for this example is from 1 July 2019 to 30 June 2022. According to the information the employer provided, the total working days in the source period is 748 days.

- During the source period the employee rendered service outside SA.

- The gross value of the gain is R5 900 600.

andIRP3(s)Forms/form27.png)

- According to the employer, of the 748 days, the total number of working days in the source period, the employee provided 494 working days of service outside SA.

andIRP3(s)Forms/form28.png)

andIRP3(s)Forms/form29.png)

Exempt amount of the gain / amount under section 10(1)(o)(ii)

- If the exemption under section 10(1)(o)(ii) is applicable, the employer must calculate the exemption and enter the exempt amount in this field.

- The SARS tax directive system will calculate and verify the exempt amount is in accordance with the information provided in all the applicable fields. The tax directive application will be declined if the difference exceeds R1.

Amounts in terms of par (dd) of the proviso to section 10(1)(k)(i) dividends

Reason to be selected:

![]()

- Enter the amount on the field ‘Gross value of gain / amount’.

- The gross amount must be reflected under code 3719 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102.

Amounts in terms of par (ii) of the proviso to section 10(1)(k)(i) dividends

Reason to be selected:

![]()

- Enter the amount next to ‘Gross value of gain / amount’.

- The gross amount must be reflected under code 3720 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102.

Amounts in terms of par (jj) of the proviso to section 10(1)(k)(i) dividends

Reason to be selected:

![]()

- Enter the amount next to ‘Gross value of gain / amount’.

- The gross amount must be reflected under code 3721 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the tax directive, under code 4102. tax

Amounts in terms of par (kk) of the proviso to section 10(1)(k)(i) dividends

Reason to be selected:

andIRP3(s)Forms/form33.png)

- Enter the amount on the field ‘Gross value of gain / amount’

- The gross amount must be reflected under code 3723 on the IRP5/IT3(a) tax certificate and the employees’ tax withheld in terms of the directive, under code 4102.tax

Paragraph 11A(5) of the Fourth Schedule

The employer must first submit a tax directive application and attach the IRP3 tax directive to the correspondence regarding paragraph 11A(5) of the Fourth Schedule:

- The correspondence must indicate where the employer is registered for PAYE purposes; and

- The reason or explanation why the employer is unable to deduct the PAYE should be indicated on the IRP3 tax directive, and request the Commissioner to absolve the employer from its obligation to deduct or withhold employees’ tax under paragraph 2(1) of the Fourth Schedule.

Process the Tax Directive Application

The SARS tax directive system will validate that the minimum required information is captured via the various submission channels and that the information is correct according to the validations built into SARS’s tax directive system.

Where the tax directive could not be issued due to errors on the application form or other validations, the employer will be notified as follows:

- Application submitted through an Interface Agency will get the error responses electronically in a responses file.

- Where the application was submitted through eFiling the error will be displayed on eFiling.

Minimum Information Required on an Application Form

- Tax Year

- Taxpayer Surname

- Taxpayer First names

- Taxpayer Initials (only applicable to electronic submissions)

- Taxpayer Date of Birth

- Taxpayer ID number or other unique number if the person is not a SA citizen

- Reason for non-registration (Unemployed or ‘Other’ specified) if no reference number entered.

- Taxpayer’s physical address and postal code

- Taxpayer’s postal address and postal code

- Annual remuneration

- The PAYE number of the Employer.

- The name of the Employer.

- The Employer’s postal address and postal code.

- Employer’s email address.

- One of the amount fields must be completed.

- Date of accrual.

- The reason for the tax directive.

Tax Directive

When the tax directive application is captured and successfully processed on the SARS tax directive system, a tax directive (IRP3) will be issued to the employer who requested the directive:

- For tax directive applications that were submitted electronically, the tax directive issued information will be sent electronically. The Interface Agent will generate the tax directive. The tax directive may only be reproduced by registered Interface Agents in the prescribe format set out in the IBIR-006 – Tax Directive Interface Specifications on the SARS website > I want a tax directive and only in respect of electronic certificates approved for that particular Interface Agent.

- Where a tax directive application was submitted manually and captured by a SARS user on SARS tax directive system, due to the fact that the employer could not obtain a tax directive through an Interface Agency or eFiling, the tax directive will be emailed to the employer.

IT88L (Notice attached to the tax directive)

The IT88L attached to the tax directive will contain all outstanding tax amounts to be paid over to SARS. Taxes outstanding can include Assessed Tax, Provisional Tax and Administrative Penalties.

- The ‘Tax amount’ (PAYE) to be withheld in relation to the lump sum or any other amount, will be indicated on the tax directive (IRP3). If the amount on the directive is greater than R 0, the amount must be deducted from the lump sum amount and paid over to SARS with the monthly EMP201 return. The employer has to issue an IT3(a) if no tax is to be withheld and an IRP5/IT3(a) tax certificate where tax (PAYE) is to be withheld from the lump sum or any other amount payable.

- The IT88L is an instruction to the employer to deduct and pay over an additional amount after the ‘Tax amount’ on the tax directive was deducted. This amount must not be reflected on the IRP5/IT3(a) tax certificate.

- The amounts indicated on the IT88L must be paid to SARS under the relevant income tax reference numbers indicated (taxpayers account) on the IT88L.

- Payments to SARS must be itemised per taxpayer reference number. A single payment per group of taxpayers must not be made electronically, i.e. via bank transfer, as it is not possible to itemise the tax reference numbers.

- If payment is done electronically, it must be done individually per stop order (IT88L). Refer to the External Guide South African Revenue Service Payment Rules – GEN-PAYM-01-G01.

If payment is done electronically, it must be done individually per stop order (IT88L). Refer to the External Guide South African Revenue Service Payment Rules – GEN-PAYM-01-G01.

If the taxpayer has an arrangement for outstanding taxes or indicates the amount on the IT88L must not be withheld, a letter from SARS Debt collection is required to instruct the employer on the amount to be paid over to SARS, where debt was settled or reduced, to ignore the IT88L.

Additional Details

Cancellation of Tax Directives

The process for the submission of the tax directive application is as follows:

- The employer is obligated to submit a tax directive application for any lump sum amount payable.

- SARS will issue a tax directive indicating the PAYE tax amount to be withheld, relating to the requested lump sum benefit.

- If a severance benefit is payable, all previous lump sums (i.e. the aggregation principle applicable to severance lump sums) will be taken into account when the tax is determined; or

- If the reason ‘Other’ was selected, tax will be calculated according to the annual payment / bonus method using the normal rate of tax.

- If an employee has outstanding taxes, SARS will issue an IT88L (stop-order) for the outstanding debt; and

- Once a tax directive has been issued, the tax directive status on SARS tax directive system will be shown as ‘FINALISED’.

Once a tax directive has been issued, the employer, to avoid hardship to the employee, may not cancel it.

The cancellation of a tax directive can only be considered in the following instances:

- Where the reason ‘Severance Benefit – Death’ was selected instead of Severance Benefit – Retirement’ or ‘Severance Benefit – Retirement due to ill-health’. Although the same tax rate is applicable, the SARS tax directive system would have classified the income tax reference number of the employee as an estate and no directive applications from employer / fund administrator will be allowed since the date of accrual cannot be after the date of the estate; or

- Where the reason ‘Other’ was used instead of ‘Severance Benefit – Voluntary retrenchment’. The directive has to be cancelled as the tax rates differ.

- The incorrect date of birth was used in circumstances where the taxpayer does not have a SA ID number and a passport number was used in the ‘Other Identification’ field. The correct date of birth is required to determine the correct PAYE to be withheld from the lump sum benefit.

- The incorrect income tax reference number was used on the tax directive application form.

- In circumstances where a duplicate tax directive application was submitted, the duplicate tax directive must be cancelled, e.g. the employee number and PAYE number are the same, only the date of accrual will differ