Purpose and Scope

- This webpage is to assist Fund Administrators / Long-term Insurers and / or employers on how to complete the various tax directive application forms in order to obtain a tax directive notice (IRP3e) before a lump sum benefit can be paid to a member.

- Should any aspect of this webpage be in conflict with the applicable legislation the legislation will take precedence.

- This webpage does not address the following applications:

- Maintenance orders. For more information on Maintenance order refer to the Interpretation Note 89 – ‘Maintenance orders and the tax-on-tax principle’;

- Maintenance order cannot be deducted from lump sum payments. The steps in Interpretation Note 89 must first be applied. Thereafter, the remaining part of the benefit may be paid as a lump sum or may be transferred.

- The Fund Administrator / Long-term Insurer cannot submit a tax directive application for maintenance orders.

- Directives for lump sums paid by employers and Fund Administrators. Refer to the ‘IT-AE-41-G01 – Completion Guide for IRP3(a) and IRP3(s) Form – External Guide’.

- Hardship directives. The following hardship tax directive applications can only be submitted by a taxpayer or the taxpayer’s tax practitioner through eFiling:

- ‘Application for Tax Directive: Fixed percentage [IRP3(b) for commission / Freelance Artist / Personal Service Provider]’;

- ‘Application for Tax Directive: Fixed Amount [IRP3(c)]’.

- For more information regarding the hardship directive refer to the ‘Guide to the Tax Directive functionality on eFiling’.

- Submission of Recognition of Transfer (ROTs). Refer to the ‘Guide to Complete, Submit and Cancel a Recognition of Transfer’.

- ‘Request for a Directive – Variation in the Deduction / Withholding of Employees’ Tax. Refer to the ‘Completion guide for IRP3(q) Directives’;

- ‘Request for a Directive: Provision for Doubtful Debt [IRP3(f)]’;

- Directive for Relief from South African Tax [RST01]. Not applicable to Lump sum tax directive applications.

- Maintenance orders. For more information on Maintenance order refer to the Interpretation Note 89 – ‘Maintenance orders and the tax-on-tax principle’;

General Information

Who must complete and submit a tax directive application form?

- Employers (including an Administrator of a pension fund, pension preservation fund, provident fund, provident preservation fund, retirement annuity fund defined in section 1(1) and Long-term Insurers) are required, in terms of paragraph 9(3) of the Fourth Schedule, to the Income Tax Act 58 of 1962, as amended (‘the Act’) to apply for a tax directive in respect of any lump sum benefit payable.

- From 1 September 2024 the two-pot retirement system comes into effect and the value in the fund will consist of the following components:

- Vested Component.

- This is the total value of the member’s interest (per policy/ contract if applicable) as at 31 August 2024, less 10% of that value, capped at R30 000, to be allocated to the Savings Component as once-off seed capital.

- The payment of the remaining balance in the Vested Component as a lump sum benefit, will not be impacted by the two-pot retirement system. Members of preservation funds will still be entitled to the once-off withdrawal.

- Savings Component.

- Effective 1 September 2024, one-third of the retirement fund contributions made by and on behalf of a member, will be allocated to the Savings Component and will be available for withdrawal by the member. This is in addition to the once-off seed capital amount, which is 10% from the Vested Component (per policy/ contract if applicable), capped at R30,000, whichever is lower.

- The member can withdraw up to the maximum value available in the member’s Savings Component. Withdrawals can be made once per tax year for pension and provident funds, or once per tax year per policy/contract, if applicable, in respect of preservation funds and retirement annuity funds. These withdrawals from the Savings Component are called Savings Withdrawal Benefits.

- The member can make a second withdrawal of up to the value of the remaining balance in the member’s savings component on termination of membership in the Fund, if the member has already accessed their one withdrawal for that tax year.

- Upon retirement, any remaining balance in the Savings Component will not be subject to compulsory annuitisation and may be added to the retirement fund lump sum benefit to be taken in cash, if the member elects to do so.

- Retirement Component.

- Starting 1 September 2024, two-thirds of the retirement fund contributions, made by or on behalf of a member, will be allocated to the Retirement Component. This component will be used to pay the member a pension or purchase an annuity and/or a living annuity upon retirement, subject to certain exceptions.

- This amount cannot be taken as a lump sum if the member terminates membership in the fund before retirement as a result of resignation, dismissal, withdrawal or retrenchment and must be transferred to another fund.

- Vested Component.

- From 1 September 2024 the two-pot retirement system comes into effect and the value in the fund will consist of the following components:

- A Fund Administrator or a Long-term Insurer must submit a tax directive application form for any lump sum payable by a SA retirement fund irrespective of the amount payable.

- A tax directive application form must be submitted where the member has requested that the double taxation agreement between SA and the country where the member resides must be taken into account.

- The RST01 application form (Directive for Relief from South African Tax) must be completed by a non-resident requesting relief from South African Tax in terms of Double Taxation Agreement is only applicable to annuities and / or pensions payable monthly / quarterly / yearly / etc.

- This ‘Directive for Relief from South African Tax’ (RST01) is not applicable to tax directives on lump sums and CANNOT be accepted as a tax directive for lump sum payments.

- The RST01 application form (Directive for Relief from South African Tax) must be completed by a non-resident requesting relief from South African Tax in terms of Double Taxation Agreement is only applicable to annuities and / or pensions payable monthly / quarterly / yearly / etc.

- A member of a fund / the member’s tax representative / a tax practitioner / financial advisor cannot complete and submit any tax directive application form that is stated in this webpage. Only the Fund Administrator and / or the Long-term Insurer can submit Lump sum tax directive application forms.

- If the Fund Administrator / Long-term Insurer receives a tax directive (IRP3e) where the Fund Administrator / Long-term Insurer has not submitted the tax directive application or the information on the tax directive does not correspond with the option form completed by the member, the tax directive must be cancelled.

- The person who has submitted the tax directive, if not submitted by the Fund Administrator / Long-term Insurer must request the cancellation of the tax directive to avoid the rejection of the return due to duplicate tax directives.

Tax directive simulator

- From the 20th of April 2018, the Fund Administrator / Long-term Insurer can first request a simulation of the tax directive result, before submitting the actual tax directive application in order to determine the tax liability on the lump sum benefit. This will assist the member to make an informed decision before an election is made in respect of the benefit.

- Simulations (quoting system) and actual tax directive application forms will be processed frequently throughout the day.

- The Fund Administrator / Long-term Insurer must ensure that the actual tax directive is used when the PAYE is paid over to SARS and the correct tax directive number and source code must be reflected on the IRP5/IT3(a) tax certificate.

- The simulation is used to provide the member the most accurate estimate of what the tax obligation will be based on the taxpayer information available on SARS’ system at that time. Fund Administrators/Long-term Insurers are encouraged to make use of the simulation to prevent the unnecessary cancellation of tax directives that can cause hardship to the member.

- The tax directive simulator will not return an IT88L for outstanding debts. It is the responsibility of the member to request the Statement of Account (SOA) from SARS to determine the possible debt deduction from their lumpsum payment. The SOA can be requested using the following channels.

- Log on to their eFiling profile link eFiling (sarsefiling.co.za).

- Request on SARS Online Query System (SOQS) under ‘SARS Notices’ on the following link: Use our Digital Channels | South African Revenue Service (sars.gov.za).

- Request using SARS WhatsApp number 0800 11 7277.

- SARS Mobi-app.

NOTE: Simulations / quotes are not stored or reflected on SARS systems, therefore the Call Centre / Branch offices cannot assist with queries regarding the Simulations / quotes.

Lump sum calculator

- The Lump Sum calculator is available from the 6th of December 2021 to a taxpayer that is registered as an eFiler or the member’s tax practitioner to determine the tax implications before a request / an option form is submitted to the Fund Administrator / Long-term Insurer.

- The member or the member’s tax practitioner can also obtain tax directives issued in previous years on eFiling. Refer to the section titled ‘Request Previous Years Directives’ in the external guide ‘Guide to the Tax Directive Functionality on eFiling – IT-AE-41-G04’ on the SARS website.

- The lump sum calculator will not return an IT88L for outstanding debts. It is the responsibility of the member to request the Statement of Account (SOA) from SARS to determine the possible debt deduction from their lumpsum payment. The SOA can be requested using the following channels.

- Log on to their eFiling profile link eFiling (sarsefiling.co.za).

- Request on SARS Online Query System (SOQS) under ‘SARS Notices’’ on the following link: Use our Digital Channels | South African Revenue Service (sars.gov.za).

- Request using SARS WhatsApp number 0800 11 7277.

- SARS Mobi-app.

How to obtain a tax directive application form?

- The updated tax directive application forms can be obtained through any of the following channels:

- eFiling:

- If a Fund Administrator / Long-term Insurer is not registered as an eFiler, please log on to www.sarsefiling.co.za to register as an organisation and refer to the guide: ‘How to Register for eFiling and Manage Your User Profile’.

- A tax directive can only be obtained from an organisation’s profile not from a taxpayer’s or tax practitioner’s profile.

- A taxpayer or tax practitioner cannot complete a tax directive application form for lump sums payable by Fund Administrators / Long-term Insurers. Fund Administrators / Long-term Insurers are responsible for submitting the tax directive application forms. On receipt of the tax directive (IRP3e) the Fund Administrators / Long-term Insurers are responsible for the payment of the employees’ tax as indicated on the tax directive (IRP3e). If an IT88L (Third Party Appointment) was attached to the tax directive, the amount(s) indicated on the IT88L must be paid over to SARS on the taxpayer’s account.

- Electronically (via an Interface or eFiling)

- Fund Administrators / Long-term Insurers can either be registered as an Interface agent or use established Interface agents to capture the tax directive application forms online.

- The interface specification IBIR-006 and the INF001 form to register to get access to SARS Interface are available on the SARS website.

- Fund Administrators / Long-term Insurers can either be registered as an Interface agent or use established Interface agents to capture the tax directive application forms online.

- The SARS website www.sars.gov.za.

- The latest version of the tax directive application forms is available on SARS website.

- eFiling:

How to submit a tax directive application form?

- A completed tax directive application form can be submitted through any of the following channels:

NOTE: It is recommended that the Fund Administrator / Long-term Insurer makes use of either eFiling or the electronic submission of tax directive application forms through the Interface agencies to obtain a tax directive.

- Electronically: Through an Interface agent.

- Electronically: Through eFiling. Fund Administrators / Long-term Insurers registered on eFiling can complete the forms online and obtain the finalised tax directive online.

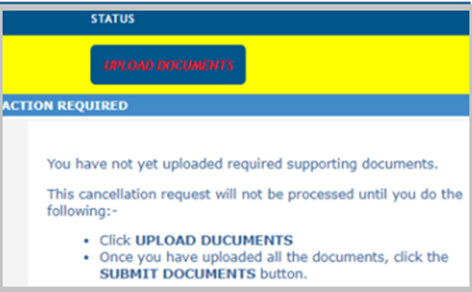

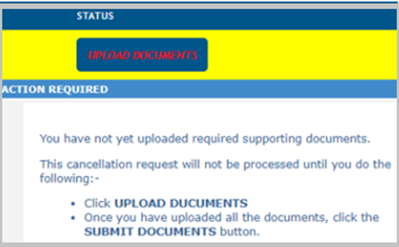

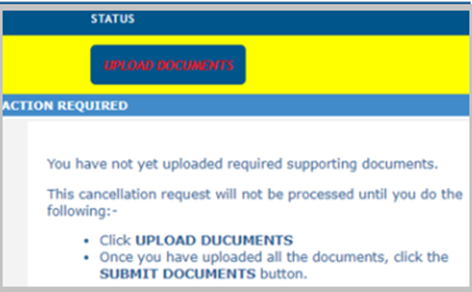

- From 9 December 2019 the Fund Administrators / Long term Insures can submit tax directive applications that requires supporting documents through eFiling only.

- Tax directive applications for non-residents, the ‘Emigration Withdrawal’, ‘Cessation of SA Residence’ or ‘Visa Expiry’ or ‘Par.(eA) Living Annuity Commutation Termination of a Trust’ tax directive application forms that requires supporting documents must be submitted through eFiling. The Fund Administrator / Long-term Insurer must be registered as an eFiler to submit these tax directive applications through eFiling.

- For more information on the required documents that must be uploaded refer to paragraphs:

- ‘Is the taxpayer a non-resident?’; and

- The paragraphs addressing the different ‘Reason for directive’ and

- the containers that must be completed will also indicate the required supporting documents to be uploaded / attached to the tax directive application form to prevent the rejection of the tax directive application form; or

- Email: Manual tax directive application (hard copy or paper copy) forms can only be submitted under extreme circumstances. One such circumstance arises when an electronic tax directive application is submitted through the Interface agency or eFiling and is rejected due to SARS system constraints.

- The manual tax directive application (hard copy or paper copy) will be returned as unprocessed if:

- There is no rejected / declined tax directive application on the SARS tax directive system that was submitted electronically, or

- The reason provided for the manual tax directive application form, is not clear and detailed enough to allow for the request to be captured manually on the SARS system.

- The Fund Administrator / Long-term Insurer can email the hard copy, paper copy or the PDF format of the completed tax directive application form downloaded from eFiling, to [email protected]. The manual tax directive application (hard copy or paper copy) must correspond with the latest version on SARS website.

- The manual tax directive application (hard copy or paper copy) will be returned as unprocessed if:

- On submission of the tax directive application form for non-residents on eFiling, the system will prompt the Fund Administrator / Long-term Insurer to upload the certificate of residence or acceptable alternative document(s) and any other required supporting documents. Ensure that ONLY the required documents are uploaded to avoid the rejection of the tax directive application. Please ensure that only the relevant supporting documents to satisfy the requirements of the three-year continuous period is requested from the member when the reason on the tax directive is ‘Cessation of SA residence’.

- Once the tax directive application form with the correct supporting documents is submitted through eFiling a case will be created on the SARS system. A SARS official will, within 21 working days, verify the completed application form and ensure that the correct supporting documents were uploaded.

- If incorrect supporting documents were uploaded or the tax directive application form was not completed in full, a SARS official will reject the tax directive application.

- The rejection reasons will be available on eFiling when the Fund Administrator / Long-term Insurer enquires on the progress of the tax directive application submitted.

- The Fund Administrator / Long-term Insurer will only have access to the tax directive applications submitted through eFiling. The Fund Administrator / Long-term Insurer will not be able to access or obtain a tax directive if the tax directive application form was:

- emailed (hard copy or paper copy) to SARS; or

- submitted it through an Interface agency.

- The Fund Administrator / Long-term Insurer will only have access to the tax directive applications submitted through eFiling. The Fund Administrator / Long-term Insurer will not be able to access or obtain a tax directive if the tax directive application form was:

Completing the Tax Directive Application Form

- The format of this webpage is based on the manual tax directive application forms (hard copy / paper copy) available on SARS’s website and the tax directive application forms on eFiling. The information in this webpage is also applicable to information required for the completion of the electronic tax directive application forms submitted through an Interface agent.

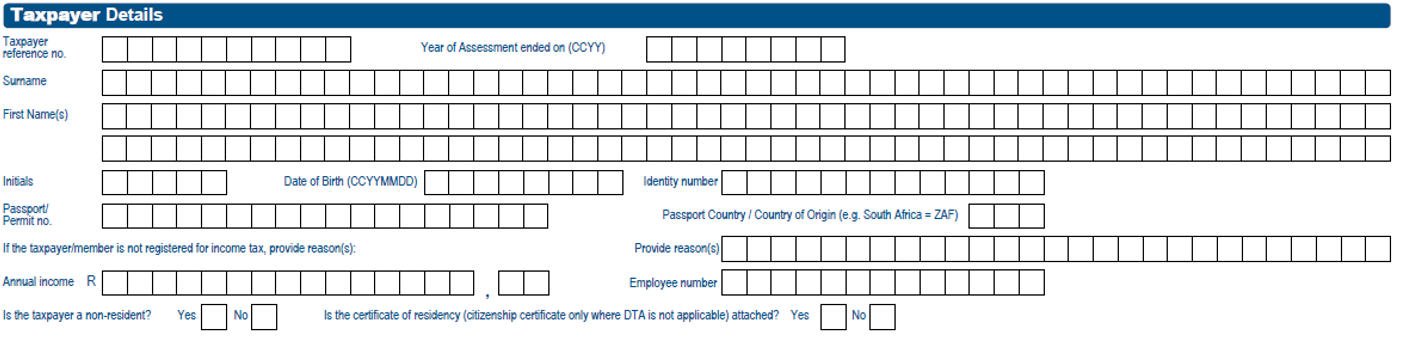

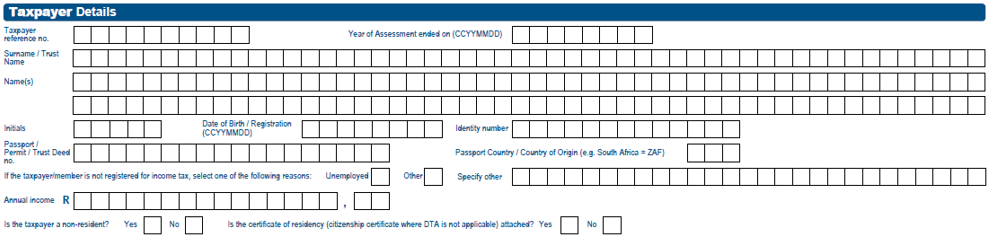

Taxpayer Details

- This part of the form is generic to all the tax directive application forms (Form A&D, Form B, Form C and Form E).

- Under the ‘Taxpayer Details’ container provide the personal details of the member / person / taxpayer who will receive the lump sum benefit payment.

- If the tax directive application form is submitted and the directive reason ’31 – Divorce – transfer’ or ’32 – Divorce non-member spouse’ is selected on the tax directive application form and the date of accrual is after 1 March 2009, the personal details of the spouse who will receive the lump sum benefit must be completed under this container.

- The ‘Taxpayers Details’ in this container must be used to issue an IRP5/IT3(a) tax certificate for the lump sum benefit amount paid.

Taxpayer reference number

- This number is also referred to as income tax reference number (TRN) and is allocated by SARS to the taxpayer when registering for income tax purposes. If a TRN was entered on the tax directive application form, the same TRN must be entered on the IRP5/IT3(a) tax certificate. If a TRN was not used in the tax directive application form, the Fund Administrator / Long-term Insurer cannot use a tax reference number on the tax certificate when the reconciliation is due. The information on the IRP5/IT3(a) tax certificate must correspond with what was completed on the tax directive application form and reflected on the tax directive (IRP3e) to prevent the taxpayer’s return being rejected.

- In the case of a divorce order a tax directive submitted for divorce orders after 1 March 2009 (regardless of the date of divorce), the income tax reference number of the spouse who will receive the benefit must be provided on the tax directive application form.

- The income tax number can only start with and 0, 1, 2 or 3 and must have 10 digits.

- The taxpayer can provide the Fund Administrator / Long-term Insurer with the top part of the ITA34 – ‘Notice of Assessment’ or an IT150 – ‘Notice of Registration’. The reference number is the number to be entered in the ‘Taxpayer reference number’ field.

- There is a function on eFiling that allows the Fund Administrator / Long-term Insurer to request the income tax reference number. The guide ‘How to request your clients Tax Reference Number (TRN) via eFiling – External Guide’ on SARS’s website will also assist the Fund Administrator / Long-term Insurer to obtain a member’s income tax reference number where the member cannot provide an income tax reference number.

- The error message ‘Invalid reference number for applicant’ or ‘Contact SARS – Tax No on application differs from Client DB’ (data base) will be displayed if:

- The member has more than one active income tax reference number according to the SARS’s data base; or

- The Fund Administrator / Long-term Insurer submits the tax directive application without the income tax reference number, indicating that ‘the reason taxpayer / member is not registered’ is ‘unknown’ or any other reason was provided, but there is a tax reference number on SARS system. The taxpayer must provide the Fund Administrator / Employer / Long-term Insurer with the correct income tax reference number.

NOTE 1: If a member has more than one active income tax reference number, the Fund Administrator / Long-term Insurer can only submit a manual tax directive application (hard copy / paper copy) where the taxpayer cannot resolve the issue with the duplicate tax reference number or any other error that prevents the successful electronic submission of the directives. On receipt of the manual application form with a duplicate number SARS will then select the correct number to be used to capture the tax directive application.

- A tax reference number is mandatory if the following directive reasons are selected:

- Two Pot-Transfer: All Components (Inter-Fund Transfer)

- Two Pot-Divorce Transfer: All Components (Inter-Fund Transfer

- Two Pot-Par (eA) Transfer/ Payment : All Components (Inter-Fund Transfer)

- Two Pot-Transfer Prior to Retirement: All Components (Inter-Fund Transfer)

- The tax reference number requirement is not mandatory for the reason codes 48 and 54 for tax directive applications with a date of accrual on or after 1 September 2024.

- Tax reference number is not mandatory if the member:

- Is a domestic worker; or

- Left SA before 1999 and the number was de-activated and is no longer on a SARS system; and

- According to SARS records there is no active or inactive number on SARS systems.

NOTE 2: For SA residents, if the TRN has been de-activated (in-active), it must first be re-activated before the directive can be submitted electronically, to prevent the declined error message ‘0273 -Taxpayer is inactive’. For a non-resident, the TRN must NOT be re-activated, however the indicator’ is the taxpayer non-resident’ must be set to ‘Yes’ on the tax directive application.

- If a tax directive was submitted without a TRN and the member provides the Fund Administrator / Long-term Insurer with a TRN once the directive was finalised, the tax directive must be cancelled and submitted with the tax number to prevent the rejection of the taxpayer’s annual return.

- If the tax directive is submitted with a tax reference number that is in-active and the taxpayer falls into the following categories, the tax directive will be processed if there are no other errors on the tax directive application:

- Tax reference number has been coded as an estate (Death and insolvency)

- A tax reference number belongs to a non-resident, provided that the indicator ‘Is the Taxpayer a non-resident?’ is set to ‘Yes’.

- The reason for directive is ‘Transfer – Unclaimed Benefit’) or

- The reason for directive is ‘Transfer – Inactive Member with Insufficient Information’)

Year of assessment ended on (Tax Year):

- This is a mandatory field that must be completed.

- This is the period commencing on 1 March of a particular year to the end of February of the following year.

- The date of accrual will determine the ‘Year of assessment ended on’ or the ‘Tax year’.

- The date of accrual must fall within the ‘Tax year’.

- For example, if the date of accrual is 25 April 2021 the ‘Tax year’ or ‘Year of assessment ended on’ will be 2022-02-28. The tax year on the tax directive will be 2022 and the ‘Year of assessment’ on the IRP5/IT3(a) tax certificate must be 2022. The ‘Year of assessment’ is reflected on the directive (IRP3e).

- If the date of accrual is 21 February 2021 on the tax directive application form and the tax directive application form was submitted on the 14th of March 2021 the ‘Tax year’ or ‘Year of assessment ended on’ will be 2021-02-28 (2021) and the ‘Transaction year’ on the IRP5/IT3(a) tax certificate will be 2022 due to the fact that the PAYE indicated on the tax directive was and can only be paid over to SARS after the directive was received on 14 March 2021. The ‘Year of Assessment’ on the IRP5/IT3(a) certificate must be 2021 as the date of accrual 21 February 2021 falls within the 2021 year of assessment and the ‘Transaction Year’ must be 2022.

- The Fund Administrator / Long-term Insurer must provide the member with a manual IRP5/IT3(a) tax certificate within 14 days after the payment of the lump sum, to enable the taxpayer to submit the 2021 return. The certificate will not prepopulate on the taxpayer’s return due to the fact that the certificate will only be submitted to SARS when the Fund Administrator / Long-term Insurer submits the bi-annual reconciliation in October 2021 for the 2022 ‘Transaction Year’.

- Therefore, the taxpayer must manually add the certificate on the tax return to avoid the rejection of the return and to enable SARS to allow the PAYE on the certificate as a PAYE deduction.

- If the bi-annual reconciliation was submitted before the taxpayer submits his / her annual return, the IRP5/IT3(a) tax certificate will also not be prepopulated on the return. The taxpayer has to add the certificate by increasing the number of certificates on the return wizard. A blank certificate will be available, and the taxpayer must capture the IRP5/IT3(a) tax certificate detail (as reflected on the manual / duplicate certificate obtained from the Fund Administrator / Long-term Insurer), including the tax directive number in order to avoid the return being rejected.

Taxpayer’s Personal Detail

NOTE: This is the information that must be used on the IRP5/IT3(a) tax certificate.

- Surname:

- This is a mandatory field that must be completed.

- Name(s):

- This is a mandatory field that must be completed.

- Enter the member’s name(s). Use the name(s) as specified on the ID document, ID card, passport document, Visa document or Dompass document.

- Do not use nicknames to avoid the tax directive from being rejected.

- The names must correspond with the information on the SARS register for taxpayers.

- The Initials are mandatory for electronically submitted tax directive application forms and must correspond with the name(s).

- A name must consist of at least two characters. Where the initials are used instead of full names, the tax directive application may be rejected.

- Date of birth:

- This is a mandatory field that must be completed.

- The date of birth must correspond with the first six digits of the ID number if the ID number is provided.

- Identity number:

- This is a mandatory field that must be completed.

- The identity number must correspond with the latest issued identity document or identity card by the South African Department of Home Affairs.

- Other ID.:

- This field is mandatory if the ID number is not provided.

- The SA number provided by Home Affairs must never be entered in this field.

- The ‘Other ID number’ must only be completed if the taxpayer does not have a South African ID number.

- The ‘Other ID number’ may be one of the following:

- Passport number

- Permit number

- Visa number

- Dompass; or

- Trust registration number.

- If the taxpayer is registered for income tax purposes, the other ID number on the tax directive application form must match the number that the taxpayer has used to register for income tax purposes.

- If the other ID number has changed and the other ID number differs from the other ID number on SARS’s records, the onus is on the taxpayer to visit SARS to update the other ID number.

- If the taxpayer is an Asylum Seeker Refugee, the Asylum Seeker Permit Number must be entered in this field.

- This field is mandatory if the ID number is not provided.

- Passport Country / Country of Origin

- This field is mandatory if a ‘Passport / Permit/Visa Number.’ is captured.

- May not be captured if a South African Identity number is captured.

- The value will be validated against the information available on SARS website under Country Codes | South African Revenue Service (sars.gov.za).

- If a member is an asylum seeker / refugee, the passport country must be ‘OTH (Other)’, a valid permit number must be provided in the ‘Passport / Permit No.’ field.

- On the Form E the passport country may not be specified where the application is for a Trust who is an owner of a living annuity.

- If the taxpayer / member is not registered for income tax, provide a reason:

- Mandatory if tax reference number is not provided.

- A readable and understandable reason must be provided. The free text cannot be more than 65 characters.

- Not allowed if the tax directive reason is:

- Two Pot-Transfer: All Components (Inter-Fund Transfer)

- Two Pot-Divorce Transfer: All Components (Inter-Fund Transfer

- Two Pot-Par (eA) Transfer/ Payment: All Components (Inter-Fund Transfer)

- Two Pot-Transfer Prior to Retirement: All Components (Inter-Fund Transfer)

- The tax reference number requirement will still not be mandatory for the reason codes 48 and 54 for tax directive applications with a date of accrual on or after 1 September 2024.

NOTE: If the Fund Administrator / Long-term Insurer submits the tax directive application without the income tax number and indicates that ‘the reason taxpayer / member is not registered’ is ‘unknown’ or any other reason where a member is registered for income tax purposes and an Income Tax reference number was issued, SARS’s tax directive system will decline the tax directive application. The taxpayer must provide the Fund Administrator / Employer / Long-term Insurer with the correct income tax reference number if registered for income tax purposes.

Annual income

- This field is only mandatory if:

- The reason on the tax directive application is ‘Par (eA) Transfer / Payment’ or ’Two Pot-Par (eA) Transfer/Payment: All Components (Inter-Fund). Only applicable to public sector funds. Refer to paragraph ‘Par (eA) Transfer / Payment’ or paragraph ’Two Pot-Par (eA) Transfer/Payment: All Components (Inter-Fund)’ for more information in this webpage.

- The tax directive application is for an unapproved fund (‘Other’ type is selected next to the field ‘Indicate whether this fund is’).

- Form B and Form E is used and where the date of accrual is prior to 1 March 2009; or

- Form A&D and Form C, where the date of accrual is prior to 1 October 2007.

- The annual income must reflect all income received by or which accrued to the taxpayer during the year of assessment, e.g. salary, remuneration, earnings, emolument, wages, bonuses, fees, gratuities, commission, pension, overtime payments, royalties, stipend, allowances and benefits, interest, annuities, share of profits, rental income, compensation, honorarium, etc.

- If the annual income amount is not correctly completed the tax calculation will be incorrect and this will cause hardship to the taxpayer when the final assessment is processed.

- The annual income must exclude the lump sum amount on the tax directive application form.

- Employee number:

- This field is not mandatory.

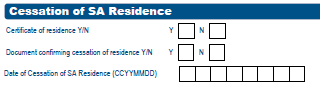

Is the taxpayer a non-resident?

NOTE 1: If the tax directive application is for a non-resident, only the tax directive application forms on SARS eFiling can be used. To access the tax directive application form on eFiling the Fund Administrator / Long-term Insurer must be registered as an organisation. (Refer to the guide: ‘How to Register for eFiling and Manage Your User Profile’).

NOTE 2: To avoid unnecessary cancellations of tax directives, if the taxpayer is a non-resident, the Fund Administrator / Long-term Insurer should ensure that the taxpayer has reviewed and received adequate advice on the application of a Double Taxation Agreement (DTA) provisions on the lumpsum, if applicable, before the Fund Administrator / Long-term Insurer submits the tax directive application. However, for instances where the DTA was not considered, and the Fund is satisfied that the DTA is applicable, the taxpayer can request the Fund to cancel the tax directive, and resubmit the application to SARS for the DTA to be taken into account

- This field is only mandatory if the tax directive application is for a non-resident who is a contributing member of an SA retirement fund:

- The non-resident rendered services inside and / or outside SA while being a contributing member of the SA fund container should be completed; or

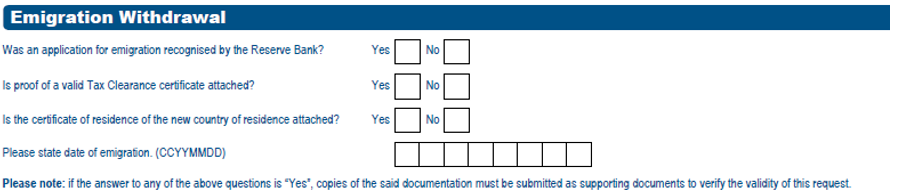

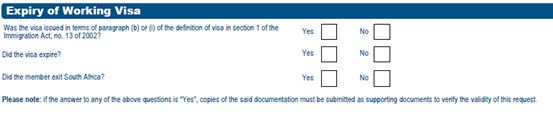

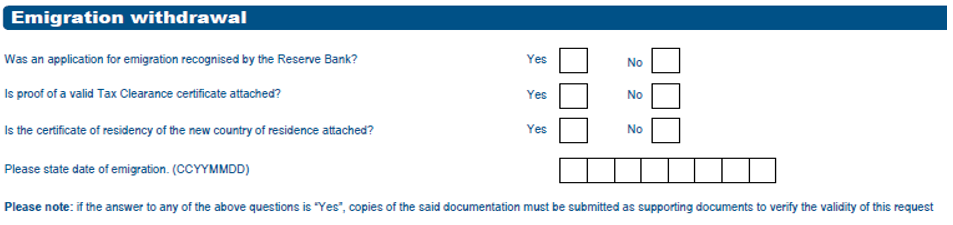

- The tax directive application is for ‘Emigration Withdrawal’ / Cessation of SA residence / ‘Visa Expiry’.

- Select ‘Yes’ or ‘No’.

- On the eFiling form this is a mandatory field and ‘Yes’ or ‘No’ must be selected.

- The Fund Administrator / Long-term Insurer must indicate “Yes” if the taxpayer is not a resident in terms of the definition of ‘resident’ in section 1(1) of the Income Tax Act.

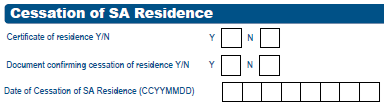

- A certificate of residence (not older than 12 months) must be attached to the tax directive application form. (Refer to paragraph ‘Is the certificate of residence attached?’ in this webpage for more detail.)

- The detailed history of employment, on the letterhead of the employer, must be attached to the tax directive application if:

- the tax directive application is from an occupational fund or a preservation fund; or

- the non-resident wants to transfer from a local fund to a fund registered in a foreign jurisdiction. Refer to subparagraph under ‘Transfer’, in this webpage.

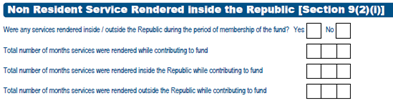

- Where section 9(2)(i) of the Act is applicable the questions in the container ‘Non-Resident Service Rendered Inside Republic [Section 9(2)(i)]’ must be completed.

- The detailed history of employment letter must clearly indicate the start day / month / year and end day / month / year of employment and where the services were rendered while contributing to the fund.

- Where the Double Taxation Agreement (DTA) must be taken into account, a letter must be attached indicating that the DTA must be taken into account and the ‘Non-Resident Service Rendered Inside Republic [Section 9(2)(i)]’ container must be completed.

NOTE 3: The ‘Non- Resident Service Rendered Inside / outside Republic [Section 9(2)(i)]’ container must always be completed and the history of employment, on the letterhead of the employer, must be attached to the tax directive application form where the tax directive application is submitted by an occupational fund or a preservation fund. Prior to 17 April 2026, these fields were not available on the Form C, and a manual (hard copy / paper copy) Form C tax directive application was required to be completed and emailed to SARS with all the relevant supporting documents. Refer to paragraph below for the new supporting documents to be provided as well as the new fields to be completed on the Form C for the DTA to be applied on the lumpsum for the reasons ‘Discontinued contributions’, ‘Divorce – Member spouse’, ‘Divorce Non-member spouse’ and ‘Cessation of SA Residence’.

Is the certificate of residence (citizenship certificate only where DTA is not applicable) attached?

- This is mandatory if the member is a non-resident.

- Select ‘Yes’ or ‘No’.

- On the eFiling form this is a mandatory field and ‘Yes’ or ‘No’ must be selected.

- Select ‘Yes’ if the application is for a non-resident taxpayer.

- Select ‘No’ if the application is for a resident taxpayer.

- The certificate of residence must be in English.

- If the certificate of residence is in a foreign language, it must be accompanied by a translated English version.

- A certificate of residence (not older than 12 months) must be attached to the tax directive application form emailed to SARS, or if the eFiling tax directive application is completed the certificate must be uploaded.

- A certificate of residence is issued by the Tax Authority where the taxpayer resides and where there is a DTA in place between South Africa and the country of residence (an assessment alone does not confirm that the taxpayer is a tax resident).

- If the foreign tax authority is unable to issue a certificate of residence, the following documents may be acceptable, when considered individually:

- Letter/document/form from the tax authority indicating that the non-resident is registered for tax in the country of residence.

- Identification Document issued by the equivalent of the South African Department of Home Affairs (DHA).

- Residence Visa or Working Visa issued by the other country.

- Complete scan of the passport (not only stamped pages).

- Any communication from an International Relations Department such as the High Commission or Embassy in the other country that citizenship has ceased in South Africa.

- If the taxpayer is unable to provide the documents listed above, the alternative documents listed below, if applicable to the taxpayer’s circumstances, may be acceptable when considered collectively.

- Latest Assessed Tax Return (ITR12 equivalent) Notice of Assessment (ITA34 Notice of Assessment);

- Rates and Taxes Bill;

- Lease agreement contract (should cover a continuous period of at least two years); or a letter confirming lodging if residing with a parent or spouse;

- Letter from an employer confirming residency, if employed;

- Registration at an educational institution in the foreign country; and

- Bank account(s) in the foreign country.

- If the foreign tax authority is unable to issue a certificate of residence, the following documents may be acceptable, when considered individually:

- Where a DTA is in place and the certificate of residence is not issued by the Tax Authority where the taxpayer resides and / or the certificate of residence is not attached to the tax directive application and / or acceptable alternative documentation is not attached to the tax directive application, the tax directive application will be rejected / declined.

- Where a certificate of residence could not be obtained from the Tax Authority of the country in which the member resides, a document from the Tax Authority indicating that a certificate of residence cannot be issued should be attached to the application form, and

- The alternative document(s) must be attached to prove the taxpayer’s residence status.

- When the tax directive application form on eFiling is completed in full and the <Submit> button is selected, the system will prompt the upload of the certificate of residence and the other relevant supporting documents, if required.

- Select ‘Yes’ or ‘No’.

Taxpayer’s addresses

- Taxpayer’s Residential address and Postal code.

- These fields are required only on Form E.

- Do not use symbols or other characters in the address field. Only use numbers and alphabetical letters.

- Taxpayer’s Postal address and Postal code.

- These fields are mandatory and can be the same as the residential address.

- The tax directive (IRP3) will not be issued to the taxpayer but only to the Fund Administrator or Long-term Insurer who requested the tax directive.

- Do not use symbols or other characters (no special characters) in the address field. Only use numbers and alphabets.

Particulars of the Fund

NOTE 1: Most of the information required in this part of the form is generic to all the tax directive application forms (Form A&D, Form B, Form C and Form E). Where certain information was completed, that is not required on the specific tax directive application form, it will be indicated as such, and the application will be rejected.

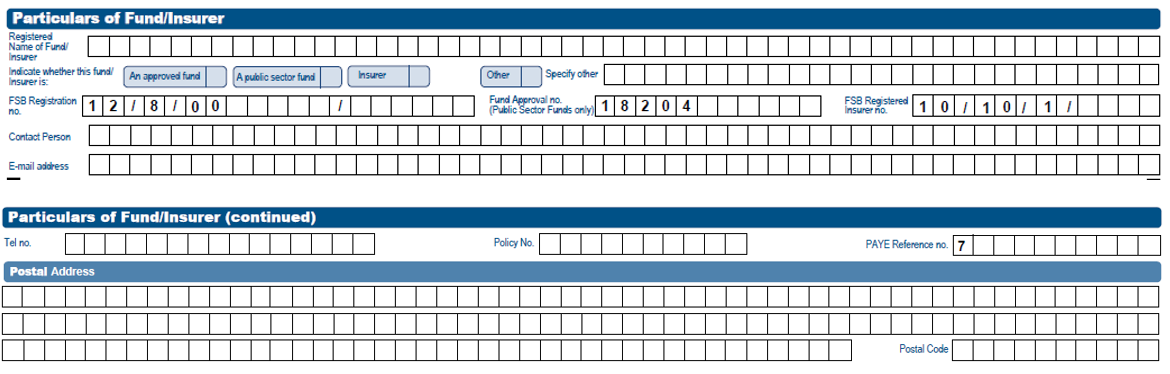

Registered Name of Fund

- Mandatory field.

- Enter the Fund name as reflected in the rules of the Fund that are registered with the Financial Sector Conduct Authority (FSCA) [Previously the Financial Services Board (FSB)].

- Fund Administrators and Long-term Insurers (on Form E) must ensure that the correct registered FSCA number, Fund Name, Participating Employer Name and Long-term Insurer Name as indicated on the FSCA website, are used from mid-September 2022, when completing the tax directive application forms, to avoid the rejection of the tax directive applications.

- The SARS tax directive system will validate that:

- The ‘Registered Name of Fund’ entered on the tax directive application form matches the ‘FUND NAME’ in the ‘Active Fund’ field on the FSCA list. This means that the spelling, special characters etc. must be exactly the same as on the list;

- The ‘FSCA Registration No.‘on the tax directive application form matches the ‘FUND NAME’ and the ‘FUND NO’ as it appears on the FSCA website;

- The status of the fund is active or in a state that allows the fund to transfer a lump sum benefit to another approved fund and pay or receive a lump sum benefit;

- If a lump sum benefit is transferred to another approved fund and the receiving fund name on the FSCA list is in Afrikaans or in any other language or has numbers and / or special characters in the fund name, then the exact spelling in the ‘FUND NAME’ field on the FSCA list MUST be used.

- The complete FSCA list can be found on www.fsca.co.za. For Active Funds: – Home / Regulated Entities / List of Regulated Entities and Persons / Retirement Fund / Registered Active Funds. Do not use the ‘Search’ function to populate this field because the spelling could be different.

- SARS system will validate if the ‘Registered Name of fund’ and the FSCA number does correspond, and that the ‘Registered Name of fund’ does correspond exactly with the FSCA list, if not the directive application will be rejected with the error message 4554 – ‘The FSCA Registered Insurer Number not valid as per FSCA’.

- On the Form E, where a Long-term Insurer submits the tax directive application form, the Long-term Insurer’s name must be provided in the ‘Registered Name of Fund / Insurer’ field and must be captured as displayed on the list, for example if limited is only ‘limit / li’ on the list.

- The complete FSCA list can be found on www.fsca.co.za. For Long term Insurers list: Home / Regulated Entities / List of Regulated Entities and Persons / Insurance. Do not use the ‘Search’ function to populate this field because the spelling could be different.

- The tax directive system will reject the tax directive application and return the following error messages where the information on the FSCA website was not used to complete the tax directive application form:

- Error message ‘4556 – The status of Transferor (From) Fund not valid as per FSCA’ will be returned if:

- the fund status on the FSCA list indicates that the fund is not an ‘Active’ fund or

- is in a state that does not allow the fund to transfer a lump sum benefit to another approved fund; or

- to pay a lump sum benefit.

- Error message ‘4557 – The status of Transferee (Receiving) Fund not valid as per FSCA’ will be returned if:

- the Receiving fund status on the FSCA list indicates that the fund is not an ‘Active’ fund or

- is in a state that does not allow the fund to receive a lump sum benefit, e.g. where the fund is the process of liquidation.

- Error message ‘4554 – The FSCA Registered Insurer Number not valid as per FSCA’ will be returned if:

- The Long-term Insurer number 10/10/1/followed by 4 digits on the tax directive application form does not match the name of the registered Long-term Insurer on the FSCA website;

- The Long-term Insurer name provided on the tax directive application does not match the data on the FSCA website, (including special characters, spaces, incomplete words, etc.). Do not use the ‘Search’ function to populate this field because the spelling could be different.

- Error message ‘4556 – The status of Transferor (From) Fund not valid as per FSCA’ will be returned if:

- Once the errors have been rectified, the tax directive application can be submitted again.

- Enter the Fund name as reflected in the rules of the Fund that are registered with the Financial Sector Conduct Authority (FSCA) [Previously the Financial Services Board (FSB)].

NOTE 2: Where the Fund Administrator or the Long-term Insurer must submit an ROT01 or ROT02 for tax directive applications submitted before mid-September 2022, the SARS ROT system will ONLY, on submission of the ROT, validate that the ROT information corresponds with the tax directive information. This means, the ROT system will not validate that the information corresponds with the FSCA data. Therefore, it is crucial that the Fund Administrator or Long-term Insurer must ensure that the information on the ROT matches one hundred percent with the information that the Transferor fund has completed on the tax directive application form.

- Contact person:

- Provide the name of the person to be contacted if more information regarding the tax directive application is required. Please avoid providing call centre details.

- E-mail address;

- This is the email address of the Fund Administrator. On the Form E the Long-term Insurer’s email address must be provided.

- It is a mandatory field and must contain an “@” sign and a domain.

- Telephone number:

- Enter the telephone number of the person who must be contacted should more information be required.

- Only capture numeric characters.

- Fund PAYE number:

- Mandatory field to be completed.

- This number starts with a 7 and consists of 10 numbers.

- This is the reference number that the Fund uses to pay over the PAYE, indicated on the tax directive to be deducted from the lump sum to SARS.

- This number must not be used to pay over the amount indicated on an IT88L (Third Party Appointment) to SARS. For more information regarding the IT88L. Refer to paragraph IT88L (Notice attached to the tax directive) in this webpage. The amount on the IT88L refers to outstanding taxes on the taxpayer’s record(s).

- The fund approval number must be blank if the Fund is an approved fund.

- Only public sector funds that are not registered with the FSCA must use the Fund approval number.

- Where the Public Sector Fund completes the approval number, the FSCA registration number field must be blank.

- The Fund approval number format is 18204 (followed by 6 digits) e.g. 18204000909.

- If the public sector fund is registered with the FSCA, the FSCA registration number (previously FSB) must be used. Refer to paragraph ‘FSCA registration number’ in this webpage below.

NOTE: The Commissioner of SARS has delegated the function to approve the rules of funds to the FSCA (previously the FSB) from 1 April 2012. New Funds approved from this date will not have a SARS approval number and therefore approved funds can only enter the FSCA registration number on the tax directive application form and the ‘Fund approval number’ field must be left blank.

FSCA registration number of Funds

- Mandatory for approved funds.

- To avoid the delay in the issuing of the tax directive ensure that the correct FSCA number is used, that the number is in the correct format and corresponds with the name of the fund provided (Refer to the ‘Active Fund’ list on the FSCA website. For Active Funds: – Home / Regulated Entities / List of Regulated Entities and Persons / Retirement Fund / Registered Active Funds. Do not use the ‘Search’ function to populate this field because the spelling could be different.

- This is the registration number, as allocated by the FSCA. The number must be provided in the correct format 12/8/0000000/999999, where 0000000 is the registered umbrella fund number and must consist of 7 digits. The 999999 represents the participating employer number and must be replaced with the correct participating employer number.

- In cases where the ‘FUND NO.’, on the FSCA list, is less than 7 digits, populate the rest of the field with ‘0’ before the number, e.g. where the FSCA registration number is 12/8/123 capture the registration number as 12/8/0000123/000000. (Refer to the ‘Registered Active Funds’ list on the FSCA website. Do not use the ‘Search’ function to populate this field because the spelling could be different.)

- If the Fund is a free-standing fund (not a type-A umbrella fund or a retirement annuity fund) the last 6 digits must be zeroes and the participating employer name must be blank. The number must be entered with the ‘/’.

- The last 6 digits of a retirement annuity fund will always be 6 zeroes e.g. 12/8/0000222/000000.

- An error message ‘4187 – Invalid format of FSCA registration number’ and or ‘Participating employer name must be provided’ will be displayed where:

- The FSCA number is not in the correct format;

- Where the last 6 digits are greater than ‘0’ and no ‘Participating employer name’ was entered the error message ‘4555 –The Fund Name provided does not match the FSCA database’ will be returned if:

- The name entered in the ‘Registered Name of Fund’ field or the name of the ‘Participating Employer’ submitting the tax directive application does not match the FSCA list, (including special characters, spaces, numbers, etc.);

- The name of the receiving fund or the name of the participating employer receiving the benefit does not matching the FSCA list, (including special characters, spaces, numbers, etc.); or

- The FSCA registered number provided does not match the fund name on the FSCA list.

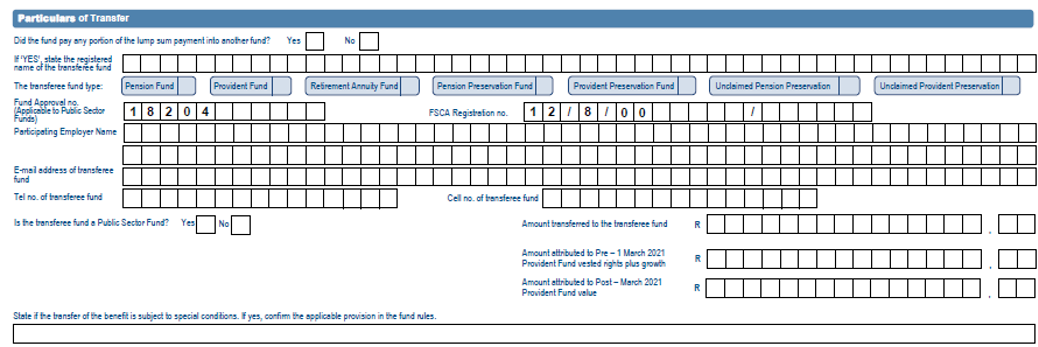

NOTE: The Fund Administrator / Long-term Insurer submitting the tax directive application must ensure that the FSCA registration number completed on the tax directive application is correct (aligned with the number obtained from the FSCA website) to avoid the ROT being declined, if the tax directive application is for a transfer of or purchase of an annuity.

Participating Employer Name

- ONLY Mandatory if any of the last six digits of the FSCA registration number is greater than zero e.g. 12/8/0012345/000006) the participating employer name must be provided.

- The name of the employer who participates in a registered type-A umbrella fund. The participating employer name must correspond with the name as registered by the FSCA. (Refer to the ‘Registered Active Participating Employers’ list on the FSCA website. For Active Participating Employers: – Home / Regulated Entities / List of Regulated Entities and Persons / Retirement Fund / Registered Active Participating Employers. Do not use the ‘Search’ function to populate this field because the spelling could be different.

Membership number (on Form A&D and Form B) / Policy number (on Form C and Form E)

- Mandatory field to be completed.

- The number which the Fund Administrator / Long-term Insurer has allocated to the member of the Fund.

- Where an additional amount is payable an ‘A’ can be added to the membership number to avoid the tax directive application being declined as a duplicate tax directive application.

Type of fund

- Mandatory field to be completed.

- On the Form A&D and Form B the Fund Administrator can select one of the following types:

- Pension fund;

- Provident fund;

- Pension preservation fund; or

- Provident preservation fund.

- On Form C only ‘Retirement Annuity’ fund type can be selected, and this fund type cannot be used on the Form A&D and Form B.

- On the Form A&D and Form B the Fund Administrator can select one of the following types:

Postal address and Postal code

- Mandatory field to be completed.

- This is the address to be used to inform the Fund of the status of the tax directive application.

- When the tax directive application was successfully captured and processed a tax directive (IRP3) will be sent to the Fund Administrator / Long-term Insurer that requested it as follows:

- Tax directive application that was submitted electronically, the tax directive information will be sent electronically. The interface agent will generate a tax directive as prescribed by SARS.

- Where the hard copy / paper copy of the tax directive application is manually submitted and captured by a SARS official on SARS’s tax directive system, a tax directive will be emailed to the applicant.

- If the Fund Administrator / Long-term Insurer has used eFiling to submit the tax directive application form the tax directive will be available on eFiling.

NOTE: SARS does not send printed tax directive copies through the post.

- Mandatory field to be completed.

- On the Form A&D and Form B the Fund Administrator can select one of the following types:

- A public sector fund – established by law and some municipal funds, (paragraphs (a), (b) and (d) of the definition of “pension fund” or paragraph (a),(b) and (c) of the definition of “provident fund” in section 1(1) of the Act);

- An approved fund – also known as private sector funds. The rules of the Fund approved by the Commissioner of SARS and the FSCA are in compliance with the requirements of paragraph (c) of the definition of “pension fund”, paragraph (d) of the definition of “provident fund”, the definition of “pension preservation fund”; the definition of “provident preservation fund”, or the definition of “retirement annuity fund” in section 1(1) of the Act.

- On the Form A&D and Form B the Fund Administrator can select one of the following types:

NOTE: The Commissioner of SARS has delegated the function to approve the rules of a fund to the FSCA since 1 April 2012.

- Other: If ‘other’ is selected the Fund Administrator must specify why the reason ‘other’ is selected, e.g. the Fund is not yet approved.

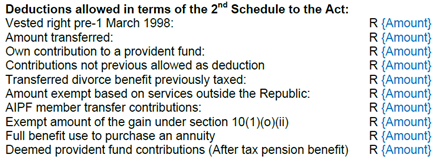

- No deduction in terms of the Second Schedule will be allowed and the benefit will be taxed as normal income.

- The source code on the tax directive will be 3907. The amount in ‘Gross amount of lump sum payment’ must be reflected in the amount field for source code 3907 and the employees’ tax (PAYE) in the amount field for source code 4102 on the IRP5/IT3(a) tax certificate.

- Other: If ‘other’ is selected the Fund Administrator must specify why the reason ‘other’ is selected, e.g. the Fund is not yet approved.

- On the Form C the Fund Administrator / Long-term Insurer can only select:

- An approved fund. Refer to sub-paragraph under paragraph ‘Indicate whether the Fund is’ above; or

- Other. Must provide a reason why ‘other’ is selected, e.g. the Fund is not yet approved.

- No deduction in terms of the Second Schedule to the Act will be allowed and the lump sum benefit will be taxed as normal income.

- The source code on the tax directive will be 3907. The amount in ‘Gross amount of lump sum payment’ must be reflected in the amount field for source code 3907 and the PAYE in the amount field for source code 4102 on the IRP5/IT3(a) tax certificate.

- On the Form E the Fund Administrator / Long-term Insurer can select one of the following types of funds:

- An approved fund. Refer to sub-paragraph under paragraph ‘Indicate whether the Fund is’ above;

- A public sector fund. Refer to sub-paragraph under paragraph ‘Indicate whether the Fund is’ above.

- Insurer – The Long-term Insurer must be a Long-term Insurer registered with the FSCA. The FSCA Long-term Insurer registered number starting with 10/10/1/xxxx (if only one digit is on the letter from the FSCA, zeros must be entered before the digit, e.g. 10/10/1/0004). (Refer to the ‘Insurance’ list on the FSCA website). Do not use the ‘Search’ function to populate this field because the spelling could be different.

- Other – If the Fund Administrator / Long-term Insurer has selected ‘Other’, a reason must be provided for selecting ‘Other’, e.g. the Fund Administrator / Long-term Insurer is not yet approved or registered as a Long-term Insurer at the FSCA.

- No deductions in terms of the Second Schedule will be allowed and the benefit will be taxed as normal income.

- The source code on the tax directive will be 3907 and the tax must be reflected in the amount field for source code 4102 on the IRP5/IT3(a) tax certificate.

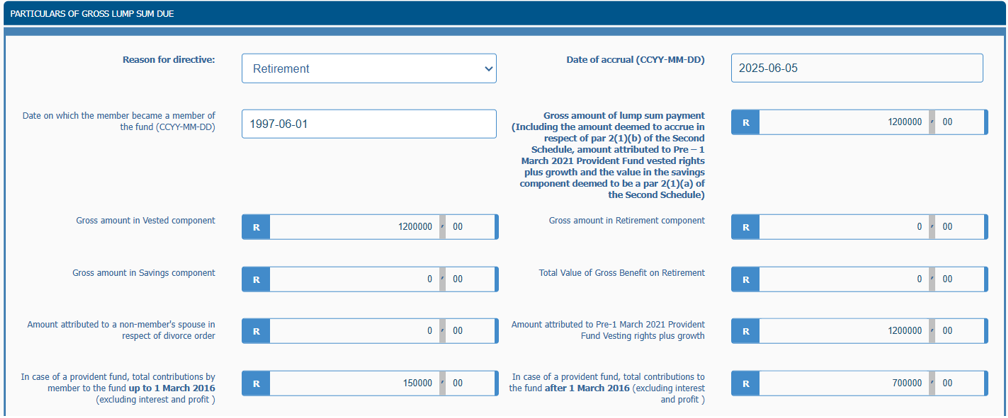

Particulars of the Gross Lump Sum due

- The information in this part of the tax directive application form is not generic, although certain fields are generic, but will be dealt with under each tax directive application form type.

- In this part of the tax directive application form, the Fund Administrator must indicate the reasons for submitting the tax directive application form. The reason indicates why the lump sum is payable or how the Fund Administrator must deal with the member’s lump sum benefit.

- The ‘Reason for directive’ selected on a tax directive application will determine the deductions to be allowed in terms of the Second Schedule to the Act, as well as the applicable rate of tax that must be applied to the taxable portion of the lump sum.

Form A&D

- The Form A&D must only be used for the retirement exit events or for death before retirement.

- The Fund Administrator must analyse the nature of the lump sum payment(s) that will be made to the member and select the appropriate reason provided on the tax directive application form.

- The pension, pension preservation, provident, and provident preservation fund administrators or trustees must use the Form A&D if the reason for the tax directive is due to:

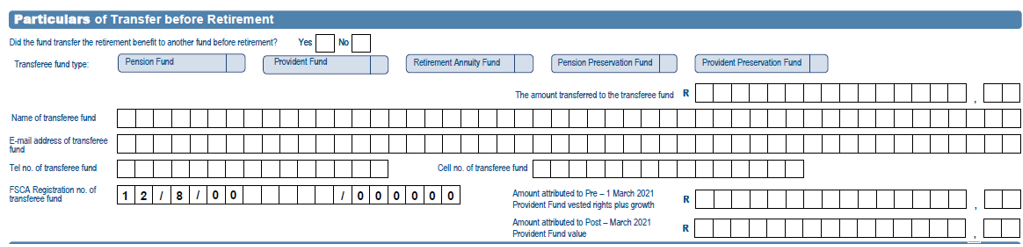

- The reason “Retirement” must be used where the member has reached the retirement age according to the rules of a pension fund or provident fund and has elected to retire from that Fund. Furthermore, the member has either elected to take a portion in cash and / or purchase an annuity or annuities from a Long-term Insurer and / or receive a pension from the Fund and / or a Long-term Insurer with the remaining balance of the full benefit. The member cannot transfer a portion or the two-thirds of the benefit to a retirement annuity fund if the reason ‘Retirement’ is selected.

- Only the full benefit can be transferred after attaining normal retirement age, as stated in the rules of the fund, but before electing to retire from a Pension Fund or Provident Fund to the Retirement Annuity Fund / Pension Preservation Fund / Provident Preservation Fund and then the member can retire from the Retirement Annuity Fund / Pension Preservation Fund / Provident Preservation Fund. Refer to paragraph ‘Transfer before Retirement [Par 2(1)(c)]’.

- Only the full benefit can be transferred after attaining normal retirement age, as stated in the rules of the fund, but before electing to retire from a Pension Preservation Fund or Provident Preservation Fund from 1 March 2024 to the Retirement Annuity Fund / Pension Preservation Fund / Provident Preservation Fund and then the member can retire from the Retirement Annuity Fund / Pension Preservation Fund / Provident Preservation Fund. Refer to paragraph ‘Voluntary Transfer before Retirement [Par 2(1)(c)]’.

- Only the full benefit can be transferred after attaining normal retirement age, as stated in the rules of the fund, but before electing to retire from a Pension fund or Provident Fund to another Pension Fund / Provident Fund from 1 March 2024 and then the member can retire from that Pension Fund or Provident Fund. Refer to paragraph ‘Involuntary Transfer before Retirement [Par 2(1)(c)]’.

- The rules of a pension or provident fund and the profession (line of work) of the member determines the retirement age.

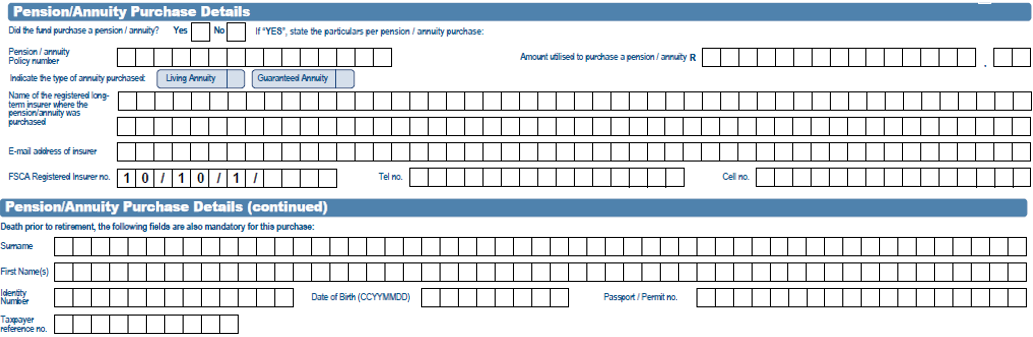

- From 1 March 2015 where the member reached retirement age in terms of the rules of the Fund, the member can elect whether the retirement benefit must be paid as a lump sum, be used to purchase an annuity from a Long-term Insurer or as a combination.

- From 1 March 2022 the member can elect a combination of whether the retirement benefit must be paid as a lump sum and the remaining amount must be used to purchase a living / guaranteed annuity from a Long-term Insurer and / or receive an annuity directly from the fund.

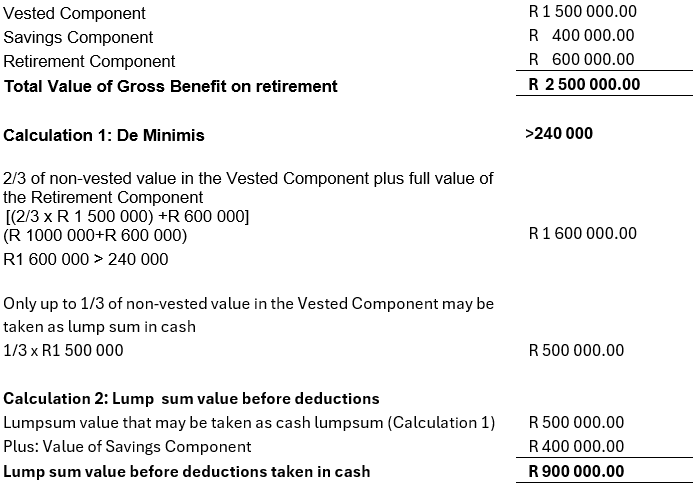

- If more than one annuity (living and / or guaranteed annuity) is purchased then the amount that remains in the fund after commuting a portion into a lump sum payable in cash must be R165 000 or more, but cannot be less, except if the total value of two thirds of the retirement interest is less than R165 000.

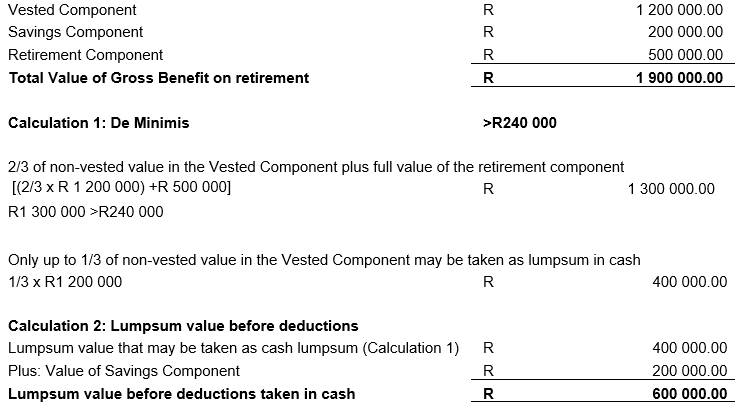

- From 1 September 2024 the amount that remains in the Fund is made up of the two-thirds of the non-vested value in the Vested Component and the full value of the Retirement Component.

- If more than one annuity (living and / or guaranteed annuity) is purchased then the amount that remains in the fund after commuting a portion into a lump sum payable in cash must be R165 000 or more, but cannot be less, except if the total value of two thirds of the retirement interest is less than R165 000.

- From 1 September 2024 the member can still elect a combination of a portion of up to one-third of the non-vested value of the Vested Component to be paid as a lump sum and the remaining amount in the Vested Component and the full value in the Retirement Component must be used to purchase a living / guaranteed annuity from a Long-term Insurer and / or to receive an annuity directly from the fund.

- If more than one annuity (living and / or guaranteed annuity) is purchased then the amount that remains in that fund after commuting a portion into a lump sum payable in cash must be R165 000 or more, but cannot be less, except if the sum of the value of two-thirds of the non-vested value in the Vested Component and the total value in the Retirement Component is equal or less than R165 000 at retirement.

- Any remaining balance in the Savings Component on retirement is excluded from the compulsory annuitisation requirement in (A) but does form part of the lump sum that may be taken in cash.

- For tax purposes, members of a pension preservation fund and provident preservation fund can only retire from the age of 55 years (minimum). If a date of accrual is prior to 1 March 2023 a member of provident fund could only retire from the age of 55 years.

- From 1 March 2022 when a member of a pension preservation fund or provident preservation fund reaches retirement age (55 years), the member can elect to transfer the benefit to another preservation fund. Refer to paragraph ‘Voluntary transfer on Retirement [Par 2(1)(c)]’.

- Where the Fund type is pension or pension preservation fund, only one-third of the total value of the benefit can be taken as a lump sum on retirement from the fund if the date of accrual is on or before 31 August 2024, subject to certain exceptions. From 1 September 2024 only up to one-third of the non-vested value in the Vested Component plus the full vested value in the Vested Component can be taken as a lump sum on retirement from the fund, subject to certain exceptions. In addition, the member can elect to receive the balance in the Savings Component at retirement as a lump sum. The amount in the Savings Component must therefore be added to the lump sum but this amount will be excluded from the compulsory annuitisation requirement on retirement.

- Prior to 31 August 2024, if the total value of the benefit is less than R247 500, the full benefit can be taken as a lump sum, or any other amount can be taken as a lump sum in cash.

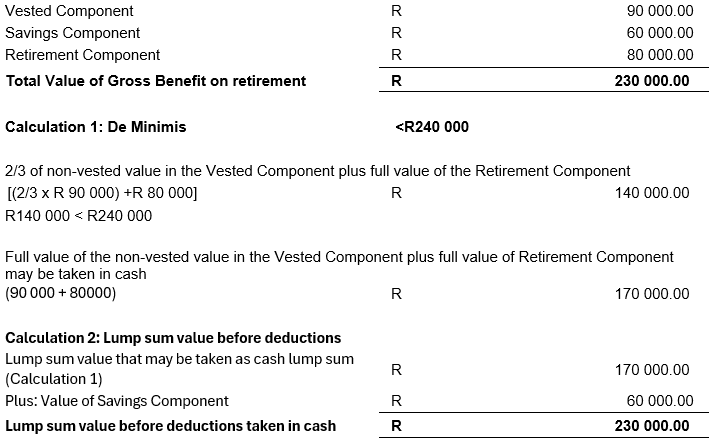

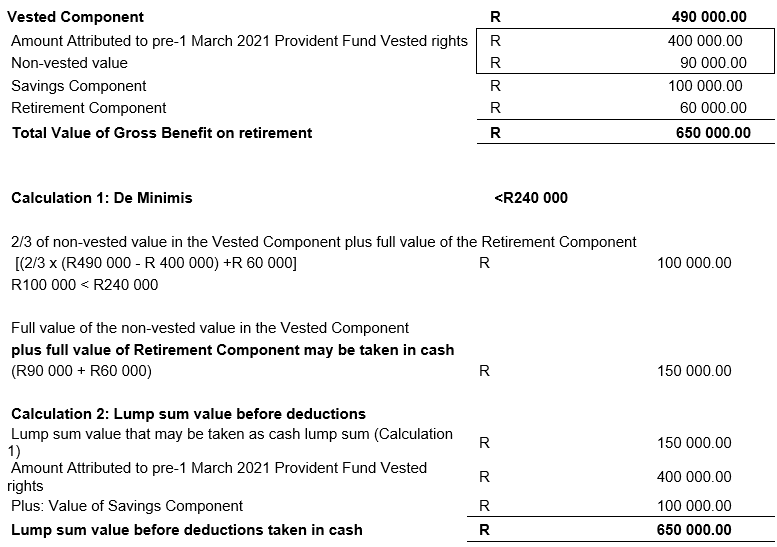

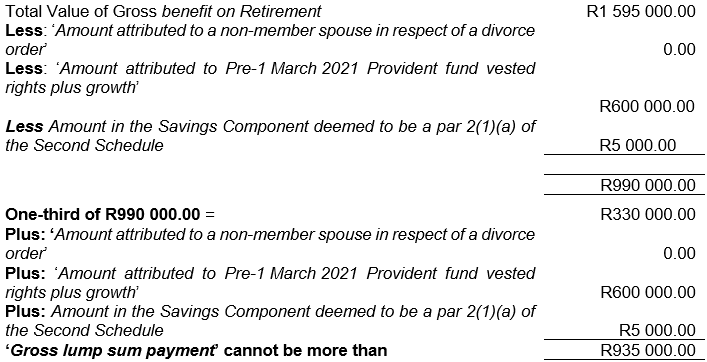

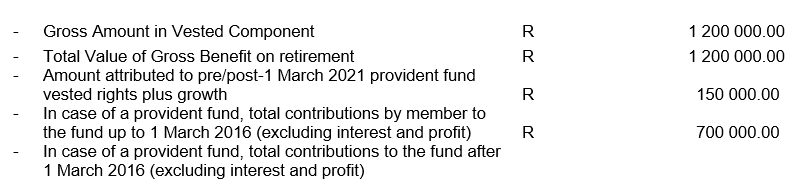

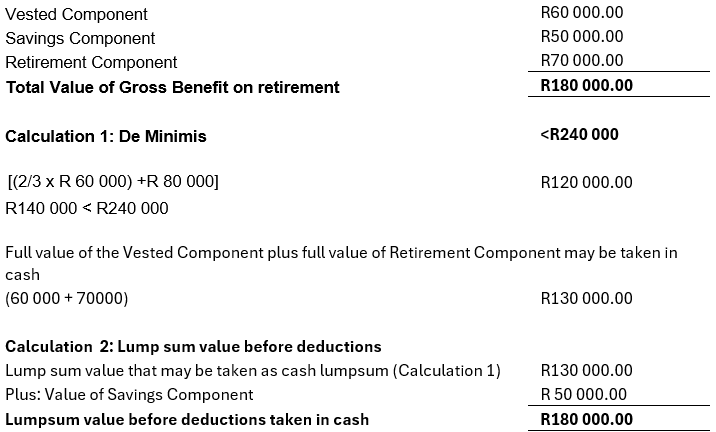

- From 1 September 2024 if two-thirds of the non-vested value of the Vested Component plus the full value in the Retirement Component is less than or equal to R165 000 (up to 28 February 2026) and R240 000 from 1 March 2026, the full benefit consisting of the full value in the Vested Component and Retirement Component can be taken as a lump sum, including any remaining balance in the Savings Component.

- From 1 March 2021 contributions to a provident fund, on or after 1 March 2021 and the non-vested benefits in a provident preservation fund, will be treated the same as contributions to a pension fund.

- Up to 31 August 2024, if a portion of the total benefit relates to an amount transferred from a provident or provident preservation fund of which the member was a member on 1 March 2021, the following value of the transferred amount will not be subject to compulsory annuitisation on retirement:

- If the member was younger than 55 on 1 March 2021, only the pre-1 March 2021 contributions to a provident fund and / or the value of the benefit in the provident preservation fund, including growth thereon; or

- If the member was 55 years or older on 1 March 2021, all contributions and growth (that is, both pre- and post-1 March 2021) to a provident fund or transfers to a provident preservation fund (relating to vested benefits in a provident fund) up to the date of transfer and growth thereon.

- From 1 September 2024, if a portion of the Vested Component relates to an amount transferred from a provident or provident preservation fund of which the member was a member on 1 March 2021, the following portion of the Vested Component will remain not subject to compulsory annuitisation on retirement:

- If the member was younger than 55 on 1 March 2021, only the pre-1 March 2021 contributions to a provident fund and / or the value of the benefit in the provident preservation fund, including growth thereon: or

- If the member was 55 years or older on 1 March 2021, all contributions and growth (that is, both pre- and post-1 March 2021) to a provident fund or transfers to a provident preservation fund (relating to vested benefits in a provident fund) up to the date of transfer and growth thereon.

- From 1 September 2024, the member can elect to receive any remaining balance in the Savings Component as a lump sum on retirement. The value must be included in the value of the lump sum to be taken but will not be subject to the compulsory annuitisation on retirement.

- Where the Fund type is provident or provident preservation fund, with effect from 1 March 2021, provident and provident preservation funds are aligned to pension, pension preservation and retirement annuity funds, in that, on retirement the member of a provident or provident preservation fund must purchase an annuity (this is, the two-thirds to be annuitised and one-third still available as a cash lump sum). However, note that all contributions to a provident fund pre and post-1 March 2021 and the value of the benefit in a provident preservation fund relating to pre-1 March 2021 transfers, including any growth thereon, are protected and can still be taken as a lump sum. Pre and post-1 March 2021 contributions to a provident fund and the value of the benefit in the provident preservation fund on 1 March 2021 relating to pre and post-1 March 2021 transfers are regarded as vested and are protected in the following manner –

- Where the member is or was a member of a provident or provident preservation fund on 1 March 2021 and is or was 55 years or older on 1 March 2021, all contributions and growth (that is, both pre- and post-1 March 2021) to a provident fund or transfers to a provident preservation fund (relating to vested benefits in a provident fund) and growth thereon are protected and is not subject to compulsory annuitisation. The member can take the full retirement interest as a lump sum in cash.

- However, if the member transfers to another provident fund after 1 March 2021, he / she loses this full protection and any contribution and growth after the date of transfer to any other fund will be subject to the compulsory annuitisation requirements on retirement.

- From 1 September 2024, if the member elects to contribute to the Savings Component and Retirement Component on or after 1 September 2024, while remaining in the same provident fund, the pre-1 March 2021 and all contributions up to the date of election, including growth thereon, will be included in the Vested Component. All contributions from the date that the member elected into the two-pot retirement system will be split into the Retirement Component and Savings Component and will be subject to the compulsory annuitisation requirements on retirement.

- However, if the member transfers to another provident fund after 1 September 2024, he/she loses the full protection and any contribution and growth in the Vested Component from the date of transfer to any other fund and will be subject to the compulsory annuitisation requirements on retirement and the member’s contributions will be allocated to the Savings and Retirement Components.

- From 1 September 2024 the members pre-1 March 2021 vested benefit and the contributions and/or transfers after 1 March 2021 and up to 31 August will be included in the Vested Component.

- Where the non-vested value in the Vested Component at retirement and the total value in the Retirement Component is equal or less than R165 000 the full value in the Retirement Component can be taken as a lump sum, if the date of accrual is after 1 September 2024.

- The member can also elect to receive any remaining balance in the Savings Component as a lump sum on retirement. The value must be included in the value of the lump sum to be taken in cash but will not be subject to compulsory annuitisation on retirement.

- From 1 September 2024, the member can elect to receive any remaining balance in the Savings Component as a lump sum on retirement. The value must be included in the value of the lump sum to be taken but will not be subject to compulsory annuitisation on retirement.

- Where the member is or was a member of a provident or provident preservation fund and is or was younger than 55 years on 1 March 2021, only the pre-1 March 2021 contributions to a provident fund and / or the value of the benefit in the provident preservation fund, including growth thereon is protected. These vested benefits are protected and not subject to compulsory annuitisation. All contributions to a provident fund from 1 March 2021, and transfers to provident preservation fund after 1 March 2021 not relating to vested benefits, including any growth thereon, will be subject to compulsory annuitisation on retirement.

- If the member decides to transfer to another provident fund after 1 March 2021, the portion of the amount transferred that relates to contributions and growth after 1 March 2021 as well as any new contributions and growth from the date of transfer to the new fund will be subject to compulsory annuitisation.

- Where the total value of provident fund contributions or the total value in a provident preservation fund, after 1March 2021, including any growth thereon, is R247 500 or less when the member reaches retirement, irrespective of his / her age, the entire retirement interest in the fund that a member has accumulated can be taken as a lump sum in cash when that member retires.

- From 1 September 2024 the members pre-1 March 2021 vested benefit and the contributions and/or transfers after 1 March 2021 and up to 31 August will be included in the Vested Component.

- Where the non-vested value, in the Vested Component at retirement and the total value in the Retirement Component, is equal or less than R165 000 (up to 28 February 2026) or is equal or less than R240 000 from 1 March 2026 ,the full value in the Vested Component and the Retirement Component can be taken as a lump sum, if the date of accrual is after 1 September 2024.

- The member can also elect to receive any remaining balance in the Savings Component as a lump sum on retirement. The value must be included in the value of the lump sum to be taken in cash but will not be subject to compulsory annuitisation on retirement.

- Where the member is or was a member of a provident or provident preservation fund on 1 March 2021 and is or was 55 years or older on 1 March 2021, all contributions and growth (that is, both pre- and post-1 March 2021) to a provident fund or transfers to a provident preservation fund (relating to vested benefits in a provident fund) and growth thereon are protected and is not subject to compulsory annuitisation. The member can take the full retirement interest as a lump sum in cash.

- For more information refer to paragraph – ‘Gross amount of lump sum payment’ and paragraph ‘Amount attributed to Pre–1 March 2021 Provident Fund vested rights plus growth’, in this webpage.

- For the completion of the IRP5/IT3(a) tax certificate refer to subparagraph under ‘Gross amount of lump sum payment’ in this webpage.

Retirement due to ill-health

- The rules of a pension fund, provident fund, pension preservation fund or provident preservation fund will indicate when a member can retire due to ill-health.

- The same rules that is applicable for the reason ‘Retirement due to ill health’ is selected. The only difference is that the rules of the fund must provide for ‘Retirement due to ill health’ and SARS’ system will not validate that the member has reached retirement age. For more information refer to paragraph ‘Retirement’ in this webpage above.

- For more information refer to paragraph – ‘Gross amount of lump sum payment’ and paragraph ‘Amount attributed to Pre–1 March 2021 Provident Fund vested rights plus growth’, in this webpage.

- For the completion of the IRP5/IT3(a) tax certificate refer to subparagraph under – ‘Gross amount of lump sum payment’, in this webpage.

Death before retirement

- From January 2008 the total value of the benefit can be commuted for a lump sum where the reason for the tax directive is ‘Death before retirement’.

- From 1 September 2024, the total value in the fund consisting of the value in the Vested Component, Retirement Component and Savings Component can be commuted for a lump sum where the reason for the tax directive is ‘Death before retirement’.

- The date of accrual cannot be after the date of death.

- The error message ‘Date of accrual cannot be greater than the date of estate’ indicates the date of death on the tax directive application form does not correspond with the date of death on SARS’s records.

- The executor of the estate must make an eBooking to visit a SARS branch with the executor’s letter and a certified copy of the death certificate and update the date of death in the branch.

- If the member died after retirement, please refer to the ‘Directive reason’ on Form E – ‘Death Member / Former Member after retirement’.

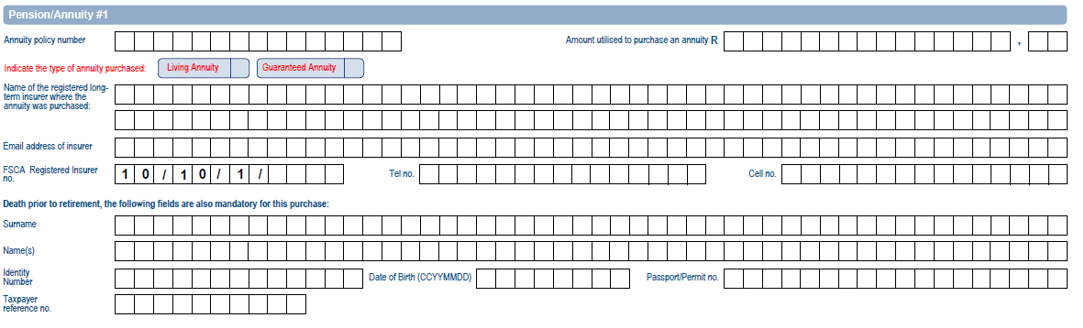

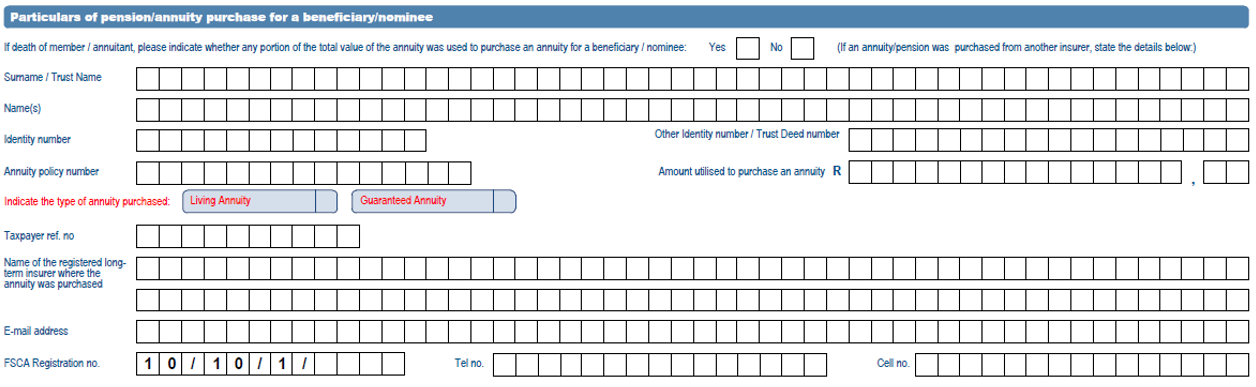

- Where the beneficiaries or nominees elect to purchase an annuity with their portion of the benefit, the beneficiary or nominees’ details must be entered in the ‘Death prior to retirement, the following fields are also mandatory for this purchase’ field.

- The Form A&D makes provision for the purchase of 4 annuities. Where there are more than 4 beneficiaries or nominees electing to purchase an annuity, a second Form A&D must be completed. The ‘Total Value of Gross benefit on Retirement’ must be split accordingly.

- Ensure that the beneficiaries or nominees information is correct as SARS validates that the ID number and the tax reference number of the beneficiary or nominee is valid and belongs to the ID number. If the beneficiary or nominee is not registered the income tax reference number must be obtained before the tax directive application is submitted. The income tax reference number is mandatory to submit the IRP5/IT3(a) tax certificate for the annuity payable to the beneficiary.

- The beneficiaries or nominees cannot transfer their portion of the death benefit to a retirement annuity fund. The beneficiary or nominee can either take their portion in cash or purchase an annuity from a Long-term Insurer.

- From 1 March 2022 the beneficiaries or nominees can elect a combination of whether the retirement benefit must be paid as a lump sum and / or be used to purchase a living / guaranteed annuity from a Long-term Insurer.

- For the completion of the IRP5/IT3(a) tax certificate refer to subparagraph under – Gross amount of lump sum payment’, in this webpage.

Provident fund deemed retirement

- With effect from 1 March 2023, paragraph 4(3) of the Second Schedule to the Act was deleted. This reason cannot be used if the date of accrual is on or after 1 March 2023.

- If the date of accrual is before 1 March 2023, paragraph 4(3) of the Second Schedule to the Act makes provision that the Fund Administrators can request the Commissioner to allow members of a provident fund, to retire before the age of 55 years on grounds other than ill-health. The Commissioner’s office will issue a letter confirming that the member or members of the specific provident fund can retire before reaching the age of 55.

- Where approval was obtained, the reason ‘Provident fund deemed retirement’ must be selected. When the taxpayer has to provide SARS with supporting documents, this approval letter must be part of the supporting documents in order to avoid the lump sum being taxed as a withdrawal benefit.

- The Fund Administrator must send the request to [email protected]. The email must clearly indicate that it is a request for early retirement from a provident fund and must include the reason / motivation why the request should be considered for approval.

- If the date of accrual is before 1 March 2023 the same rules applicable for the reason ‘Retirement‘ applies if the reason ‘Provident Fund Deemed Retirement’ is selected. The only difference is that this reason can only be selected if the approval from SARS was obtained.

- For more information refer to paragraph ‘Gross amount of lump sum payment’ and paragraph ‘Amount attributed to Pre–1 March 2021 Provident Fund vested rights plus growth’, in this webpage.

- For the completion of the IRP5/IT3(a) tax certificate refer to subparagraph under ‘Gross amount of lump sum payment’, in this webpage.

Voluntary transfer before Retirement [Par 2(1)(c)]

- With effect from 1 March 2018 paragraph 2(1)(c) of the Second Schedule to the Act provides that a member’s retirement interest in his or her pension fund or provident fund, can be transferred on or after the member attains normal retirement age, as defined in the rules of the Fund, but before retirement date (before the election to retire) to a retirement annuity fund on a voluntary basis.

- The old reason ‘Transfer before Retirement [Par 2(1)(c)]’ has been amended on the directive application to “Voluntary transfer before Retirement [Par 2(1)(c)]” for this purpose.