Basic Guide to Section 18A approval

SARS has issued a guide to assist organisations in understanding the basic requirements for obtaining and retaining approval under section 18A. The organisations covered in the guide include:

- Public Benefit Organisation (PBO)

- An institution, board or body

- A conduit PBO;

- Government

- Any agency contemplated in the definition of ‘specialised agency’ in section 1 of the Convention on the Privileges and Immunities of the Specialised Agencies, 1947 and

- Specifically named funds, programmes, High Commissioners, offices, entities or organisations.

The guide is comprehensive and deals with prescribed requirements for Section 18A approved organisations, requirement to obtain audit certificates, how noncompliance is dealt with and requirements for using of donations receipts. The guide can be accessed by clicking here: Basic Guide to section 18A Approval

The interpretation note applicable to Public Benefit Organisations (PBO) regarding partial taxation can be accessed by clicking here: Interpretation Note 24 (Issue 5)

Guide to submit a dispute via eFiling updated

If a taxpayer incurred interest and penalty on provisional tax, a taxpayer is allowed to submit a Request for Remission prior to submission of the annual return. In this scenario, the user must click on the ‘Add Dispute Item’ button and select the applicable source code from the list:

- 9995 – Interest (section 89bis) on provisional tax

- 9996 – Penalty (paragraph 27(1)) on provisional tax

The guide can be accessed by clicking here: Guide to submit a dispute via eFiling

Implementing two-factor authentication to login on the SARS MobiApp

To mitigate the risks associated with compromised passwords, an additional security layer has been integrated to access the SARS MobiApp. The two-factor authentication (2FA) security system method consists of two distinct forms of identification requirements. SARS MobiApp users or taxpayers can now enable the 2FA method on their eFiling profile. This implies that once implemented, they will be prompted to provide a one-time-pin (OTP) after they have successfully entered their username and password on the SARS MobiApp. Access to their SARS MobiApp profile will only be granted once they have completed the OTP successfully on their smart device.

The following external guide has been updated with this new development: How to register for the use of the SARS MobiApp.

Enhancements: Tax Compliance Status

The Tax Compliance Status (TCS) process relating to the approval of international transfer (AIT) applications have been adjusted to address feedback from stakeholders. Below is a summary of the key revisions:

- TCS Application Form (TCR01):

- All the fields under the “Foreign Assets and Liabilities Details” container have been made optional based on the date the TCS applicant ceased to be a South African tax resident

- The “Net Worth” field under the “Assets and Liabilities Details” container has been amended to “Net Amount (At cost)”

- The “Trust No.” and “Passport No. of Main Trustee/Representative Taxpayer of the Trust” under the “Local and Foreign Trust Details” container, and the “Local and Foreign Loan to a Trust Details” container have been made optional when “Foreign Trust” is selected

- The “Trust No.” under the “Distribution from Trust Additional Details” container has been made optional when the “Foreign Trust” is selected

- The “Share code” field and “Number of shares sold” field under the “Sale of Shares and Other Securities Details” container have been disabled when the “Listed Shares” is selected.

- TCS Verification Letter (TCR006):

The TCR006 letter has been amended to display the residency status under which the application was approved. - TCS Dashboard:

An “Amount” column has been added to the TCS dashboard to enable the AIT Reviewers and Approvers to view the total value of the international transfer per the TCR01 application (where the application has not yet been approved) or the approved amount per the AIT case.

See the updated guide here: Guide to the Tax Compliance Status functionality on eFiling

Digital fraud reporting now online

If you suspect that your tax profile has been compromised, you can now report it electronically. As part of our ongoing efforts to enhance taxpayer confidence a new feature has been introduced. Simply click here to report the incident and follow the prompts to register your case. This will assist SARS to manage and prioritise your case while making it easier for you to interact with SARS when it comes to digital fraud.

See the updated guide here: SARS Online Query System Guide

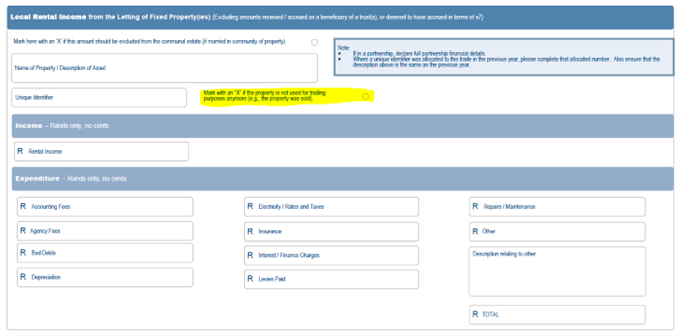

Declaration of proceeds from rental income on the Income Tax Return

SARS received a query about the difficulty in completion of the tax return pertaining to rental income. A taxpayer had two properties from which rental income was declared in the 2022 tax year, however in 2023 tax year, one property was not used for rental income, and the taxpayer was unable to reduce the two properties on the tax return to one in the wizard.

The external guide on the ITR12 provides detailed guidance on this matter. To access the guide, click here: Comprehensive guide to the ITR12 Income Tax Return for Individuals.

The guide from page 49 onwards states that:

- From the 2016 year of assessment, rental income must be declared separately on the return

- Each rental activity must be declared separately (a maximum of 20 is allowed)

- The description of the rented property must be declared and in subsequent years, the same description must be completed

- From the 2023 year of assessment, SARS will prepopulate the description field based on the information available per SARS records. The taxpayer can amend this description,

- SARS will automatically allocate a unique identifier per property. This unique identifier must be used by the taxpayer in subsequent years

- From the 2023 year of assessment, if the property/asset description field and unique identifier fields are prepopulated but the property/asset is no longer used to earn rental income the following information is completed on the tax return:

- Mark with an ‘X’ if the property is not used for trading purposes anymore (e.g., the property was sold)

See the screenshot below for details as to how this will appear in the tax return.