Updated e@syFile Employer Beta Release available for Trade Testing – August 2026

27 July 2026 – The South African Revenue Service will give you an opportunity to test the updated e@syFile™ Employer build before the formal release in mid- September 2026 for the Employer Interim Reconciliation.

The updated e@syFile™ Employer BETA version with enhanced features for download will be released on Monday, 24 August 2026, so that you can start testing immediately.

During the testing period from 24 August 2026 to 11 September 2026, all online functionalities will be disabled to prevent the incorrect submission of test data into the production environment. This means the application will default to offline mode. Certain menu options will also be disabled as a precautionary measure.

The Business Requirements Specification SARS_PAYE_BRS – PAYE Employer Reconciliation V25 3 0 for the Employer Interim Reconciliation submission period 202608 is available.

The BETA version of e@syFile™ encompasses the following:

- New source code for ITREG to mitigate duplicate Income Tax registration for employees.

- Minor amendments to source code validations and descriptions.

A link to give you access to test the software will be provided soon. Please note that this link is confidential and only available to selected employers. In order to maintain its confidential status, please exercise caution and do not share it with others.

SARS will analyse the feedback from the external testers during the test cycle. Please nominate a contact person with his or her contact details to act as a liaison with SARS.

Please send your consolidated feedback to the SARS support team at [email protected] on a daily basis. The team will log it with the relevant SARS development team members to update the software. The feedback will be used to determine the frequency at which updated versions of the test software will be released.

Customs Weekly List of Unentered Goods now available

27 July 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

The latest Government Connect newsletter is now available

24 July 2026 – In the July 2026 edition, we share important updates affecting taxpayers, including reminders on scams and phishing, historical income tax assessment notifications, Auto Assessments, updated Filing Season 2026 guides, required online traveller declarations, and key changes affecting provisional taxpayers.

We encourage taxpayers to familiarise themselves with the latest developments, verify their information, use only official SARS channels, and meet their filing obligations on time.

The latest Tax Practitioner Connect newsletter is now available

24 July 2026 – The July 2026 edition provides updates for tax practitioners and clients, including tax-practitioner registration challenges, historical income tax assessment notifications, Filing Season 2026 developments, Auto Assessment enhancements, provisional taxpayer changes, and new SARS digital services.

We also remind taxpayers and practitioners to stay alert to scams and use only official SARS channels. This issue further covers the online traveller declaration requirements effective from 1 July 2026 and includes links to updated filing-season guides and resources.

Limpopo Mobile Tax Unit Schedules for July & August 2026

24 July 2026 – The Limpopo mobile tax unit schedules for July and August 2026 are now available.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

24 July 2026 – Customs and Excise Act, 1964: Publication details for tariff amendments notices, R7739, R7740, and R7741, as published in Government Gazette 55065 of 24 July 2026, are now available.

Updated Prohibited and Restricted Imports and Exports list

23 July 2026 – The Prohibited and Restricted Imports and Exports list was updated.

- Tariff heading 5301.30 does not require a Plant Inspector Permit.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

23 July 2026 – Customs and Excise Act, 1964: The tariff amendments notices, scheduled for publication in the Government Gazette, relate to the following amendments:

With effect from 24 July 2026

- Part 1 of Schedule No.1, by the substitution of tariff subheading 8467.99.90, in order to increase the general rate of customs duty on rock drilling equipment parts from free of duty to 20% (ITAC Report No. 774)

- Part 1 of Schedule No.1, by the substitution of tariff subheadings 2008.11.11, 2008.11.15 and 2008.11.19, in order to increase the general rate of customs duty on peanut butter from 0,99c/kg to 20% (ITAC Report No. 652)

With retrospective effect from 2 May 2025 up to and including 1 May 2026

- Part 3 of Schedule No. 2, by the substitution of various items under item 260.03, in order to list the rebate items intended to be excluded from the applicable safeguard duty of a rate of 13% on certain hot-rolled steel products, classifiable under Chapter 72 retrospectively from date of implementation (ITAC Revised Minute M02/2025)

Publication details will be made available later

Legal Counsel – Dispute Resolution & Judgments – High Court 2028-2026

23 July 2026 – Customs and Excise Act, 1964

Whether the Commissioner lawfully exercised the powers conferred by sections 61(2), 88(1)(a) and 107(2)(a)(i) of the Customs and Excise Act, 1964, by requiring additional security and detaining the Applicant’s goods to protect the fiscus – whether these actions constituted the lawful exercise of statutory powers under the Act or administrative action that is unlawful and reviewable under the Promotion of Administrative Justice Act, 2000, as alleged by the applicant.

SARS Digital platform upgrades on 24 and 26 July 2026

23 July 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Friday, 24 July 2026 from 18h00 to 23h00,

Sunday, 26 July 2026 from 05h00 to 07h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

23 July 2026 – Customs and Excise Act, 1964: Publication details for the following tariff amendments notices are now available:

With effect from 24 July 2026 up to and including 23 July 2027

- R7734 of Government Gazette 55063

With effect from 24 July 2027 up to and including 23 July 2028

- R7735 of Government Gazette 55062

With effect from 24 July 2028 up to and including 23 July 2029

- R7733 of Government Gazette 55061

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

22 July 2026 – Customs and Excise Act, 1964: The tariff amendments notices, scheduled for publication in the Government Gazette, relate to the following amendments:

With effect from 24 July 2026 up to and including 23 July 2027

- Part 3 of Schedule No. 2, by the substitution of safeguard items 260.03/7318.15.41/01.08; 260.03/7318.15.42/01.08 and 260.03/7318.16.30/01.08, to extend the safeguard duties with a rate of 42,04% on threaded fasteners of iron or steel (excluding those of stainless steel and those identifiable for aircraft) – ITAC Report 780

With effect from 24 July 2027 up to and including 23 July 2028

- Part 3 of Schedule No. 2, by the substitution of safeguard items 260.03/7318.15.41/01.08; 260.03/7318.15.42/01.08 and 260.03/7318.16.30/01.08, to amend the safeguard duties to a rate of 40,04% on threaded fasteners of iron or steel (excluding those of stainless steel and those identifiable for aircraft) – ITAC Report 780

With effect from 24 July 2028 up to and including 23 July 2029

- Part 3 of Schedule No. 2, by the substitution of safeguard items 260.03/7318.15.41/01.08; 260.03/7318.15.42/01.08 and 260.03/7318.16.30/01.08, to amend the safeguard duties to a rate of 38,04% on threaded fasteners of iron or steel (excluding those of stainless steel and those identifiable for aircraft) – ITAC Report 780

Publication details will be made available later

Legal Counsel – Dispute Resolution & Judgments – High Court 2028-2026

22 July 2026 – Superior Court Act, 2013

- Ocean Ark Shipping Ltd and Another v CSARS (Leave to Appeal) (2025/209746) [2026] ZAWCHC 354 (6 July 2026)

- Ocean Ark Shipping Ltd and Another v CSARS (Leave to Appeal) (2025/209746) [2026] ZAWCHC 330 (8 June 2026)

Summaries are available on the High Court Judgments page

Western Cape Mobile Tax Unit Schedules for August 2026

22 July 2026 – The Western Cape mobile tax unit schedules for August 2026 are now available.

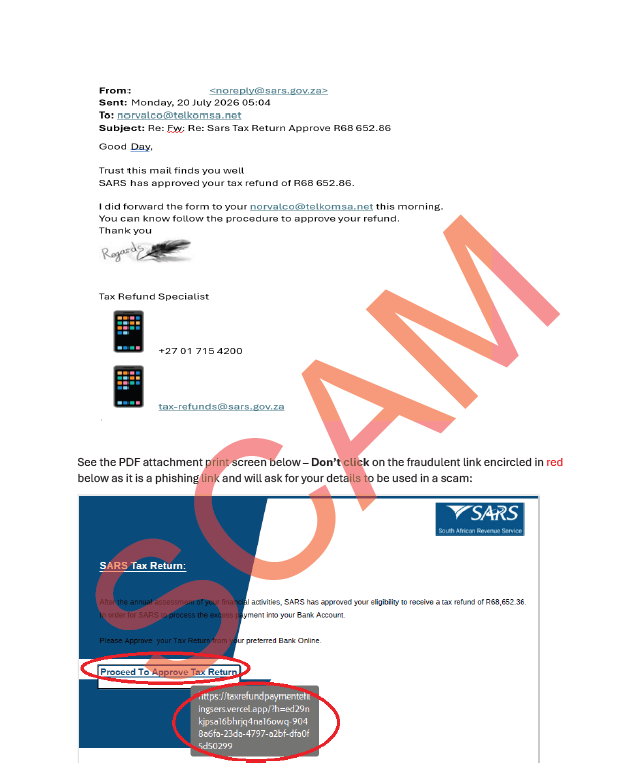

Scam alert – Email appearing to be from a SARS employee

22 July 2026 – Please be aware of emails doing the round appearing to be from a SARS employee, this particular employee’s name is masked on the scam warning example below.

Please don’t open the PDF attached to the email or click on the link in the PDF as it is a fraudulent phishing link designed to extract personal details from you to be used in a scam.

If in doubt, always see the latest scam examples on our Scams & Phishing webpage or email [email protected].

Direct link to this particular scam – SARS-SCAM-396 – Sars Tax Return Approve R68 652.86 – 22 July 2026.

Preview of the scam:

Customs Weekly List of Unentered Goods now available

20 July 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

Legal Counsel Publications – Tables of Interest Rates

20 July 2026 – Income Tax Act, 1962: Updated Tables of Interest Rates

- Table 1 – Interest rates on outstanding taxes and interest rates payable on certain refunds of tax

- Table 2 – Interest rates payable on credit amounts

SARS Digital platform upgrades on 17 July 2026

17 July 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Friday, 17 July 2026 from 21h00 to 23h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Advance Pricing Agreement (APA) programme

17 July 2026 – SARS has published a dedicated webpage, Implementation of Advance Pricing Agreements (APAs) as part of the ongoing implementation of South Africa’s APA programme. The webpage provides an overview of the programme, its objectives, expected benefits, and the planned pilot approach. The APA programme aims to provide upfront tax certainty for qualifying cross-border related-party transactions.

SARS plans to start the pilot phase in 2026. Taxpayers and stakeholders are encouraged to visit the APA webpage for information on the programme and to stay informed about future developments as implementation progresses.

Legal Counsel – Interpretation and Rulings – Interpretation Notes 21-40

17 July 2026 – Value-Added Tax Act, 1991

- Interpretation Note 31 (Issue 5) – Documentary proof required for the zero-rating of goods or services