Legal Counsel Archive – Practice Notes

16 October 2025 – Income Tax Act, 1962

- Practice Note 36 of 1995 – Income Tax: Valuation of trading stock

Government Connect Issue 31 (October 2025) is available now

16 October 2025 – In this edition, we highlight the upcoming Employer Interim Reconciliation submission period, outline requirements for a successful EMP501 submission, and share important enhancements to the e@syFile™ platform. Stay informed so that your organisation remains compliant and takes full advantage of the latest tools and resources available.

The Tax Practitioner Connect Issue 67 (October 2025) in now available

16 October 2025 – In this edition, we highlight the upcoming Employer Interim Reconciliation submission period, outline requirements for a successful EMP501 submission, and share important enhancements to the e@syFile™ platform. Stay informed so that your organisation remains compliant and takes full advantage of the latest tools and resources available.

Media release: SARS urges non-provisional taxpayers to file their Income-Tax returns before 20 October deadline

15 October 2025 — The South African Revenue Service (SARS) reminds non-provisional taxpayers that the deadline to submit annual Income-Tax returns is 20 October 2025.

SARS has made every effort to simplify and support the filing process. Through enhanced digital platforms, Auto Assessment, and accessible helplines, taxpayers have been empowered to meet their obligations with ease and efficiency.

With just five days left before the deadline, SARS Commissioner Edward Kieswetter encourages taxpayers to take advantage of the remaining days to file their returns. He emphasised the legal obligation to file the returns on time and in full

The Commissioner urges all taxpayers not to abdicate their tax obligations: failure to submit a return by the deadline is a serious offence, and non-compliance can lead to administrative penalties and interest charges. As part of our strategic focus to encourage voluntary compliance and enforce the law, SARS will continue to identify and act against those who do not meet their tax obligations.

Commissioner Kieswetter also extends appreciation to the 80% of taxpayers who had filed before the 20 October 2025 deadline. This includes about 6 million taxpayers who have been auto-assessed and received their refunds within 72 hours. This commitment to compliance plays a vital role in building a capable state and funding essential public services. It is making a difference in the lives of so many of our people.

Many taxpayers wait until the last minute to file their returns, hoping to meet the deadline. However, rushing invites errors, misjudgements, unnecessary stress, and long queues at SARS branches. SARS urges taxpayers to submit returns while there is still time to think clearly and avoid mistakes. Filing early protects taxpayers from penalties and ensures a refund, if due, which is payable in 72 hours.

With only five days left before the deadline, 7 900 531 non-provisional taxpayers have already filed their tax returns, with more than 854 408 still outstanding. In the 2024 tax year, over 6.7 million non-provisional taxpayers filed their Income-Tax returns, including those who were auto-assessed.

For further information, please contact [email protected].

Monthly Tax Digest – October 2025

15 October 2025 – The October issue of the Monthly Tax Digest is now available. In this issue we look at SARS Filing Season Deadlines Coming Up.

Selected SARS Branches will open on Saturday 18 October 2025

15 October 2025 – Selected SARS branches will be open to assist taxpayers with filing their income tax returns this Saturday, 18 October 2025, ahead of the Individual Filing Season deadline of 20 October 2025.

See the following open branches per region:

| Region | Branch name | Opening times |

| Free State & Northern Cape | Bethlehem | 08:00 – 13:00 |

| Bloemfontein | ||

| Welkom | ||

| Kimberly | ||

| Western Cape | Cape Town | 08:00 – 13:00 |

| Bellville | ||

| Mitchells Plain | ||

| George | ||

| Paarl | ||

| Eastern Cape | Gqeberha | 08:00 – 13:00 |

| East London | ||

| Mthatha | ||

| KZN | Durban | 08:00 – 13:00 |

| Pinetown | ||

| Pietermaritzburg | ||

| Port Shepstone | ||

| Richards Bay | ||

| Newcastle | ||

| Mpumalanga | Mbombela | 08:00 – 12:00 |

| eMalahleni | ||

| North West | Rustenburg | 08:00 – 13:00 |

| Klerksdorp | ||

| Mmabatho | ||

| Limpopo | Sibasa | 08:00 – 12:00 |

| Giyani | ||

| Lebowakgomo | ||

| Polokwane | ||

| Gauteng | Ashley Gardens | 08:00 – 13:00 |

| Pretoria CBD | ||

| Randburg | ||

| Rissik Street | ||

| Roodepoort | ||

| Alberton | ||

| Edenvale | ||

| Krugersdorp | ||

| Springs | ||

| Doringkloof |

Customs – Registration, Licensing and Accreditation

13 October 2025 – The facility codes used in Box 30 on the Customs Clearance Declaration (CCD) has been updated to include details of the transit shed for SPX Logistix (Pty) Ltd, located at O. R. Tambo International Airport. This addition enables Customs to transmit electronic messages communicating the status of the consignment to these facilities.

Legal Counsel – Dispute Resolution & Judgments – Tax Court: 2025–2023

13 October 2025 – Income Tax Act, 1962

Secondary tax on companies and General anti-avoidance rule: Whether the avoidance arrangement was entered into or carried out by means or in a manner which would not normally be employed for bona fide business purposes, other than obtaining a tax benefit.

Customs Weekly List of Unentered Goods now available

13 October 2025 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Media release: SARS – Narcotics bust operation

12 October 2025 – The SARS Durban Customs office conducted a collaborative intelligence operation led at the Durban Harbour in the early morning of 12 October 2025. The operation resulted in the seizure of 30 bricks of Suspected Narcotics that were in Reefer Refrigeration Unit of the vessel with the estimated street value of R 65 000 000.

The drugs were handed over to SAPS, DPCI for further investigation, prosecution and destruction.

On 12 October 2025 at approximately 02:45 Durban Customs Enforcement Team Launched the Customs Marine Unit Patrol Vessel – Striker to go and intercept the Motor Vessel near the Fairway Bouy at Outer Anchorage about 4 Nautical Miles of the East Coast of the Durban. The Enforcement Team intercepted the vessel as it was entering the port and escorted the vessel to its berth. The Enforcement Team Boarded the Vessel, interviewed the Master of the Vessel, and examined documentation to identify the location of a profiled container.

The Vessel was Rummaged by the Enforcement Team and the container was located on the Vessel where the Refrigeration Unit was examined. This resulted in one positive detection of bricks of suspected narcotics.

SARS Commissioner Mr Edward Kieswetter expressed his gratitude to the SARS Customs and other law enforcement agencies for their salutary work. He said that “Customs demonstrated its gallantry by working so hard and focussed at the death of the night to intercept this vessel. This speaks to an unwavering commitment by SARS to protect our borders and keep at bay all criminals that are bent on shipping harmful substance that cause unmitigated suffering for our inhabitants.”

For more information, please contact [email protected]

Media release: SARS’s response to Mr Lucky Montana’s misleading public statements

11 October 2025 — SARS needs to state upfront that when this matter arose in 2011 Mr Tshepo Lucky Montana was not a political representative, and this matter can therefore never be about his politics or a political witch-hunt.

Mr Tshepo Lucky Montana (“Mr Montana”), a member of Parliament, initiated a public attack on the South African Revenue Service (“SARS”) in recent days via the news agency Independent Online (“IOL”).

Other news outlets subsequently repeated the claims to some extent or another. Mr Montana’s false claims are specific. According to IOL, he claimed the following:

- That SARS “abused it powers”;

- “Maladministration” by SARS;

- That SARS conducted a “politically motivated witch hunt”; and

- That SARS “fraudulently doctored a fake court judgement to justify a hefty tax bill (sic)”

According to IOL, Mr Montana, based on the above claims, “laid charges” against SARS representatives for “fraud” with the South African Police Service (“SAPS”).

On 8 October 2025, SARS responded in a general press statement rejecting the claims as false (annexure 1). SARS proceeded to issue a formal notice to Mr Montana in terms of section 67(5) of the Tax Administration Act 28 of 2011 (“the Tax Administration Act”).

In terms of section 67(5) of the Tax Administration Act, SARS is empowered to publicly disclose taxpayer information where it is necessary to counteract false statements that may undermine the integrity and public confidence in the tax system. The notice afforded Mr Montana the opportunity to retract his statements and false allegations within 24 hours. Mr Montana failed to do so.

To the extent necessary for now, SARS will set out the salient factual sequence of events, with specific reference to the false claims Mr Montana made.

The false claims of “abuse of power”, “maladministration” and “a politically motivated witch hunt”:

Mr Montana made these very same claims before the Gauteng Division of the High Court, Pretoria in the matter of Montana v Commissioner for the South African Revenue Service (2023-047735) [2025] ZAGPPHC 749. Mr Montana had all the opportunity to provide substance to his claims but did not. The judgment in this case speaks for itself (annexure 2).

The court ruled, among other aspects as follows:

“In Par 28.5, Mr Montana accuses SARS of maladministration and abuse of power. In par 29.4 and par 42 he accuses SARS of indulging in a witch hunt against him, motivated by a political agenda… All these allegations are scandalous and vexatious… The allegations are emotive and intemperate, unsupported by facts and constitute gratuitous abuse…While the court is mindful not to stifle robust debate, such allegations fall to be deprecated as irrelevant, unhelpful and calculated to harm. Such conduct warrants a punitive cost order.”

The factual sequence of events:

Mr Montana failed to submit his income tax returns in respect of the 2017, 2018 and 2019 years of assessment. SARS initiated an audit in respect of his 2009 to 2019 years of assessment.

Mr Montana was formally notified of this on 5 November 2020. In the ordinary course and by operation of law, as with any other taxpayer under audit, Mr Montana was requested to provide information for the audit by no later than 4 December 2020.

Mr Montana requested, and SARS granted him, an extension to submit the required relevant material and information by 1 February 2021.

Mr Montana then failed to deliver the requested documentation. This is a contravention of the law.

On 2 February 2021, SARS issued a final demand to Mr Montana to submit the requested relevant material and information.

Again, Mr Montana failed to comply in contravention of the law.

The audit concluded in the ordinary course as in such cases for any taxpayer in audit culminating on 7 July 2021 in a Letter of Findings (“LOF”) to Mr Montana.

Mr Montana was informed that SARS intended to raise additional income tax assessments to the value of approximately R15,5 million in respect of his 2009 to 2019 years of assessment. (Capital only).

SARS found that Mr Montana had unlawfully evaded his tax liability by under-declaring taxable income he received from various sources over the relevant periods of audit. This is a contravention in law.

Again, as in the ordinary course for any taxpayer in such a position, Mr Montana was afforded 21 business days to respond to the audit findings.

On 11 August 2021, Mr Montana requested and was granted an extension until 16 August 2021 to respond to the findings.

On 16 August 2021, Mr Montana responded to a limited extent only, failing to deal with the bulk and essence of the audit findings.

Instead of using the opportunity, Mr Montana elected to attack SARS by making unsubstantiated and unfounded allegations against SARS, accusing it of “vindicative action” and conducting a “witch hunt”.

SARS denied the allegations, advising that it will proceed to finalise the assessments with due consideration of his submissions.

SARS issued Mr Montana with a progress report on 11 October 2021.

Further exchanges between Mr Montana and SARS’s attorneys took place after this.

On 11 April 2022, SARS issued a Finalisation of Audit letter to Mr Montana, advising him that SARS proceeded to raise the assessments.

Mr Montana was informed in absolute detail what the basis of the assessments was.

Mr Montana was at this stage assessed for tax of approximately R28 million (comprising of capital and penalties ) in respect of the 2009 to 2019 years of assessment for underdeclared income.

Mr Montana was advised that if he felt aggrieved by or disagreed with the assessments, he could formally object to the additional assessments by no later than 26 May 2022. This is available to any taxpayer in such a position.

The formal process of objection is contained in section 104 of the Tax Administration Act read with Rule 7.2 of the Tax Court rules. The objection must be filed in a prescribe form ADR1 and lodged on the taxpayer’s eFiling profile

On 27 May 2022, Mr Montana requested and was granted an extension to lodge his objection by no later than 31 May 2022.

On 31 May 2022, SARS received Mr Montana’s “partial objection” which, yet again, made unsubstantiated and unfounded allegations against SARS.

At this point, Mr Montana appointed new auditors/tax representatives and proceeded to request a further extension to lodge an objection to 1 July 2022. SARS granted the request.

On 1 July 2022, Mr Montana and/or his newly appointment representatives did not file the objection as had been undertaken. Instead, they requested a further 30-day extension to respond to the assessments/file an objection.

On 11 July 2022, SARS declined the extension request. Mr Montana did not request a suspension of payment of his assessed tax liability as envisaged in terms of section 164(1) of the Tax Administration Act. The outstanding tax debt was therefore due and payable and SARS issued Mr Montana with a final demand to pay on 11 July 2022. SARS Mr Montana still did not pay, SARS proceeded with the recovery steps detailed later herein

On 22 July 2022, SARS provided copies of Mr Montana’s bank statements to Mr Montana’s representatives, as requested by them.

On 20 September 2022, Mr Montana submitted a further letter to SARS to elaborate on his “objection to the audit raised in his letter dated 31 May 2022”. Significantly, the letter recorded that:”[we] have noted that SARS has subsequently obtained a default judgment against us. We further reserve our right to respond to the default judgment obtained by SARS once we have had time to peruse and evaluate the judgment”. He said that he would address this “under separate cover”. This submission still not complied with the requirements for an objection in terms of the Tax Administration Act, read with the Tax Court rules.

On 23 September 2022, Mr Montana addressed a further letter to SARS to respond to the default judgment SARS obtained against him. In this letter Mr Montana amongst others recorded what transpired when SARS on 15 September 2020 executed the default judgment on him. The letter recorded that:

“Apparently, SARS had obtained a Default Judgment against me at the High Court of South Africa (Gauteng Division, Pretoria) for the total amount of R44,927,320.23. I was not home at the time of the raid nor aware of an impending Court action by SARS. No summons was served on me in this regard.”

The letter continued to state that he was advised that the default judgment was obtained at best by misrepresentation to the High Court and could be rescinded. The fact that Mr Montana has after all this time still not applied to the High Court for the tax judgment to be rescinded is significant. It is by now no longer open for him to do so.

On 30 November 2022, SARS’s attorneys issued a letter informing Mr Montana that his purported objection was invalid and was thus not accepted. Mr Montana was granted until 31 January 2023 to submit a valid objection. Mr Montana’s allegations regarding the default judgment was also addressed in this letter and denied. SARS’s attorneys explained in the letter the due process SARS followed in terms of the Tax Administration Act to obtain the default judgment against him.

On 22 December 2022, Mr Montana informed SARS that he did not intend to file any proper objection and persisted with his previous contentions. According to him, he considered his 20 September 2022 submission sufficient.

On 23 January 2023, SARS responded to Mr Montana and informed him that no further opportunities to file a late objection(s) would be granted.

Mr Montana has still, as at date hereof, not filed a valid objection.

In terms of section 100 of the Tax Administration Act, the additional assessments have therefore become final and are no longer open to dispute.

Mr Montana’s contention that he only recently became aware of the full extent of his tax liability is therefore false and dishonest.

Debt collection process followed:

The Tax Administration Act imposes on SARS the statutory obligation to ensure the efficient and effective collection of tax.

Before the audit referred to above commenced, Mr Montana already had an outstanding assessed tax liability for the 2015 year of assessment. This was in terms of an assessment SARS raised on 1 July 2017. By October 2019, the outstanding tax amounted to R1,800,762.38. Since this amount remained, SARS on 2 October 2019 filed a certified statement in terms of section 172 of the Tax Administration Act, with the Registrar of the High Court of South Africa (Gauteng Division, Pretoria) under case number 72501/19 (“the Registrar”, “the High Court” and “the 2019 certified statement/tax judgment” respectively) as required by the Tax Administration Act.

In terms of section 174 of the Tax Administration Act, provides that such certified statement must be regarded as a civil judgment if lawfully given in the High Court in favour of SARS for the amount specified in the statement.

It is settled law that a certified statement of a tax debt submitted by SARS to the Registrar or Clerk of a competent court is equal to a civil judgment.

On 11 April 2022, SARS raised the assessments against Mr Montana referred to above, with final demands issued on 28 June 2022 and 11 July 2022.

As a result of Mr Montana having not made payment towards the assessed tax liability, an amended certified statement was in terms of section 172 was filed with the Registrar of the High Court on 11 August 2022. This totalled the overdue old and the new tax debts (“the 2022 certified statement/tax judgement”). SARS is permitted to do this in terms of section 175 of the Tax Administration Act. The judgement amount in terms of the 2022 certified statement/tax judgment was R44,927,320. Interest continue to accrue on this amount.

The Registrar issued warrants of execution respectively on 29 October 2019 (based on the 2019 certified statement/tax judgment) and 15 August 2022 (based on the 2022 certified statement/tax judgment”), to be executed in the ordinary course of debt collection as is the position with any taxpayer.

Due to the many physical addresses Mr Montana provided, the Sheriff executed the warrants of execution on 20 November 2019, 22 November 2019, 25 November 2019, 15 January 2020, and 15 September 2022 respectively, at the various addresses.

Mr Montana was only present at the execution address when the warrant was executed on 15 January 2022.

Due to Montana’s non-payment of his tax debts, and the aspect in terms of the Insolvency Act 24 of 1936 (“the Insolvency Act”) being satisfied, SARS launched an application for the sequestration of Mr Montana’s estate on 22 May 2023.

The application was premised on Mr Montana’s outstanding tax debt, which remained unpaid.

Mr Montana’s allegation of SARS “fraudulently doctoring a fake court judgment to justify a hefty tax bill” (sic) is false.

Copies of the certified statements have been provided to Mr Montana on various occasions. They are also attached as annexures to SARS’s sequestration application against Mr Montana.

The SARS application spells this out in no uncertain terms:

“On 2 October 2019, SARS filed a certified statement with the Registrar of the High Court…In terms of section 174 of the Tax Administration Act, the statement has thereupon the effect of a civil judgment granted in SARS’ favour in this Court for the amount in question… On 11 August 2022, SARS filed a certified statement with the Registrar of the High Court…In terms of section 174 of the Tax Administration Act, the statement has thereupon the effect of a civil judgment granted in this Court against the taxpayer…”

The High Court will in due course consider the sequestration application.

Attempts to serve the sequestration application at the different physical addresses that Mr Montana provided, proved to be unsuccessful.

SARS therefore had no other option but to launch an application in the High Court to obtain leave from the Court to serve the application on him via his email address and by publication of the notice of motion in a local newspaper.

Approximately a year later, namely on 5 June 2024, under circumstances where Mr Montana had still not filed his answering affidavit in the sequestration application, Mr Montana launched an application to condone the late filing of his answering affidavit.

SARS opposed the condonation application and Mr Montana delivered a replying affidavit. In the replying affidavit, Mr Montana again made unsubstantiated, unfounded scandalous, vexatious, and irrelevant allegations regarding SARS.

On 14 August 2024, SARS launched an application to strike out the impugned allegations from Mr Montana’s replying affidavit.

On 21 July 2025, the High Court dismissed Mr Montana’s application for condonation with a punitive cost order.

The court also granted SARS’s application to strike out the scandalous, vexatious, and irrelevant allegations from Mr Montana’s replying affidavit.

Mr Montana has applied for leave to appeal against this judgment. This application will be heard in due course.

Recently, on 8 August 2025, Mr Montana submitted a compromise offer to SARS, offering the sum of approximately R 5.4 million to satisfy the total tax debt outstanding which currently stands at R55,133,282.94.

A prerequisite in terms of the Tax Administration Act for SARS to consider a compromise offer, is that the tax debt may not be disputed. In other words, the taxpayer must accept that the tax is due and payable.

On 30 September 2025, SARS responded to Mr Montana’s attorneys, requesting Mr Montana to address the legal and formal requirements for such a compromise.

The requested information is due on 14 October 2025.

It is therefore untenable for Mr Montana to publicly attack SARS and its officials, whilst simultaneously seeking a compromise of a tax debt he accepts.

Dependent on the compromise process Mr Montana initiated and the outcome thereof, SARS intends to set the sequestration application down for hearing in the High Court.

Mr Montana has still not filed his answering affidavit in the sequestration application. SARS’s stated position against him therefore stands uncontested.

Significantly, SARS’s actions against Mr Montana have throughout, and will continue to be, subject to judicial scrutiny.

SARS remains committed to upholding the rule of law and ensuring that all taxpayers are treated equitably.

To this end, the Commissioner for SARS has informed the Commissioner of the SAPS and the National Director of Public Prosecutions that he, and the other SARS officials involved in the enforcement of the tax laws concerning Mr Montana (and any other taxpayer for that matter), will co-operate fully should an investigation follow from Mr Montana’s grievances. In addition, SARS has requested SAPS to address the abuse of resources and complaints procedures by persons who seek to distract, divert and create unnecessary drama.

This public statement is not intended to impinge on any potential investigation(s) that the SAPS or the NPA may consider within this context, and is solely issued with the intent to protect SARS and its officials as provided for in law.

The Commissioner for SARS laments that Mr Montana’s allegations and adverse public commentary against SARS harms the vital institution of the State, which is fundamental to sustaining our country’s democracy and addresses our social and economic challenges.

SARS urges members of the public to be circumspect, to verify information through official SARS channels, and to refrain from disseminating unsubstantiated claims in the public domain.

SARS reserves the right to amplify or add to this public statement if it becomes necessary, which may include making public any records and documents, where deemed appropriate.

Issued by: South African Revenue Service (SARS)

- Annexure 1 – Public Statement: Alleged claims by Mr L Montana MP as reported in Independent Newspapers on 7 October 2025

- https://www.sars.gov.za/issued-notice-of-motion-and-founding-affidavit-lt-montana/

- https://www.sars.gov.za/montana-v-sars-judgment-12/

- https://www.sars.gov.za/issued-sequestration-application-of-lt-montana-annexures/

For further information, please contact [email protected].

Limpopo Mobile Tax Unit Schedules for October & November 2025

10 October 2025 – The Limpopo mobile tax unit schedules for October and November 2025 are now available.

VAT Connect Issue 20 (October 2025) is now available

10 October 2025 – This issue provides an overview of proposed amendments arising from the national budget, a notable Supreme Court of Appeal decision involving Woolworths Holdings and the South African Revenue Service (SARS), the regulations on exporting second-hand goods, taxpayers’ rights regarding SARS-approved apportionment methods, and the determination of liability dates for Value-Added Tax (VAT) collection.

Legal Counsel – Preparation of Legislation – Draft Documents for Public Comment

10 October 2025 – Customs and Excise Act, 1964: Draft amendments to forms for Comment:

- DA 159 – Petroleum Products: Account for Special Storage Warehouse

- DA 160 – Petroleum Products: Account for Manufacturing Warehouse

Due date for comment: 23 October 2025

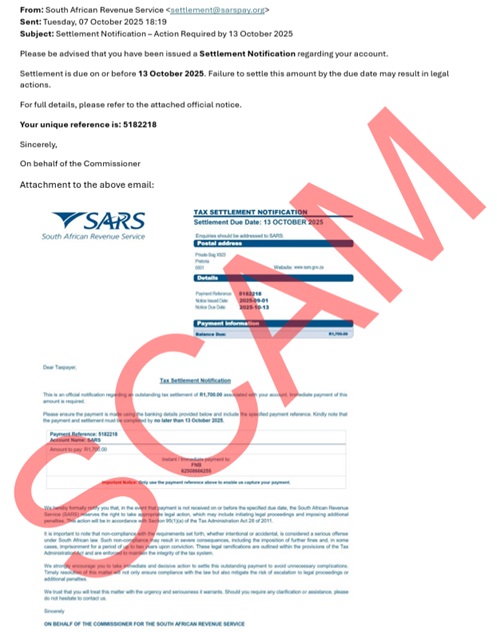

Latest Scam Alert: Email with Settlement Notification

9 October 2025 – The latest scam is an email with the subject line ‘Settlement Notification – Action Required by 13 October 2025’. It continues to say ‘Settlement is due on or before 13 October 2025. Failure to settle this amount by the due date may result in legal actions.’ People are prompted to click on a PDF attachment with fraudulent bank details. Please don’t click on any suspect links, attachments or pay money into bank accounts. See here how payments to SARS are handled.

If in doubt, always see the scam alerts published on the Scams & Phishing webpage or email the SARS Anti-phishing team on [email protected].

Preview of this scam:

Access to Information

8 October 2025 – Promotion of Access to Information Act, 2000, and Protection of Personal Information Act, 2013

The following changes were made to the Promotion of Access to Information Act, 2000 (PAIA) page:

-

Updated to, amongst others, include the Protection of Personal Information Act, 2013

-

Publication of Issue 8 of the Manual on the Promotion of Access to Information Act, 2000, and Protection of Personal Information Act, 2013

Updated e@syFile™ Employer version 8.0.1_325

8 October 2025 – The e@syFile™ Employer version 8.0.1_325 release notes specify the following changes:

- Correction made for users experiencing ‘Packet loss’ popup during submission.

- Correction made for users experiencing ‘An error occurred’ pop-up when requesting pre-pop data.

- Enhancements made to AA88 processing.

- Enhancement made to large import files, resulting in a time-out pop-up.

- Correction made to restrict the option to only generate all PDF certificates for the 02 Reconciliation.

See more detail in the release notes.

Media release: Public statement: Alleged claims by Mr L Montana MP as reported in Independent Newspapers on 7 October 2025

7 October 2025 – The South African Revenue Service (SARS) has noted media reports by Independent Newspapers today wherein it is alleged that Mr Lucky Montana MP has “charged” and “laid criminal charges” against SARS for supposedly “fraudulently doctoring a fake court judgment to justify a hefty tax bill”. Mr Montana further allegedly made public claims against SARS of “maladministration, abuse of power and a politically motivated witch hunt”.

Whereas ordinarily, SARS does not engage publicly with taxpayers that are engaged in dispute processes, the false claims must be addressed immediately. In this respect, it is absolutely essential to provide a background to this matter.

The process of debt collection in general:

The Tax Administration Act imposes on SARS the statutory obligation to ensure the efficient and effective collection of tax. This process may include the filing of a certified statement by SARS, setting out the amount of tax payable to the clerk or registrar of a competent court, where applicable in certain circumstances. In such a case, a warrant of execution is then issued – to be executed in the ordinary course of debt collection. This certified statement, lawfully given in favour of SARS, is then utilised to recover the taxpayer’s tax debt. It is settled law that such a certified statement obtained by SARS from a court with competent jurisdiction over the taxpayer is treated as a civil judgment for purposes of recovery of a tax debt. SARS emphatically denies using “fraudulently doctored court judgments to justify hefty tax bills”.

Case selection in general:

SARS is a state institution and subject to the Constitution and the Bill of Rights. SARS seeks to apply the tax and customs laws it administers with fairness, in a transparent and even-handed manner without any external influence. No single person in SARS can decide who to investigate, who to audit, who to settle tax debts with and who not to. SARS relies on a variety of automated, Artificial Intelligence (AI), risk-based, data-based and research formulated case selection mechanisms. Case selection for investigation or audit is subject to oversight from various mechanisms – committees with governance rules exist to consider and execute certain activities. All these committees exist by statute, policy or governance mechanism and have very clear rules. They comprise of persons with the requisite knowledge and expertise and are themselves subject to oversight mechanisms. SARS is a semi-autonomous public institution with specific statutory obligations. SARS has consistently conducted its work independently and in a non-partisan manner that does not allow for external interference. SARS emphatically denies any “politically motivated witch hunts”.

The modus operandi of false claims to obfuscate, delay, distract, counter, and create uncalled for drama:

It has become commonplace among some who have to face the consequences of their own actions, to try to obfuscate, distract, attack and use delay tactics by abusing formal complaints, oversight and investigative mechanisms and processes, and by lodging false allegations and fake and unsubstantiated “complaints”. Our recent history is littered with examples of how persons have sought to infiltrate and manipulate the media and other public platforms to advance false claims and narratives to achieve all sorts of questionable outcomes. The same goes for abusing and subverting law enforcement agency resources solely to achieve sensationalist headlines. In this regard, SARS has been and will continue to engage with the various Criminal Justice System agencies with a view to examine how best this practice can be curbed, as it is also wasting time and precious resources of law enforcement officials.

SARS urges the media to conduct meaningful fact-checking and to ensure that they’re familiar with legal and standard administrative processes and procedures before reporting on mere claims. SARS, and the media and in fact all citizens of this country owe it to all honest, diligent, and hardworking civil servants to first determine the motive of the claim, be critical of wild claims and at the very least establish facts, before advancing one-sided claims. This does not preclude anyone from seeking any remedy permitted in law from law enforcement agencies, if there is a case to be had. In this case, there is none.

“Charging” and “laying charges”:

The National Prosecuting Authority (NPA) is established by Section 179 of the Constitution and is the sole institution empowered to decide to criminally charge any person, institution, or legal entity and to determine what those charges may be. Nobody other than the NPA can charge SARS or any of its officials.

SARS is allowed to disclose taxpayer information publicly to disprove false allegations:

Considering the claims by Mr Montana, SARS will to the extent necessary, invoke Section 67(5) of the Tax Administration Act, which allows SARS to disclose taxpayer information that would otherwise be treated as confidential, in order to disprove the false allegation made against SARS and its processes.

SARS will make no further public comment in this regard for now, until Mr Montana has been notified in terms of section 67 (5) of the Tax Administration Act to withdraw publicly these false, scandalous and vexatious claims within the necessary time period of 24 hours. Failure to act, SARS will be compelled to disclose the otherwise confidential taxpayer information to correct the misperception.

SARS further encourages taxpayers in dispute with SARS to make use of ongoing and existing dispute platforms to air any grievances they may have.

For further information, please contact [email protected].

Ask Lwazi: SARS AI Assistant – our upgraded Artificial Intelligence Assistant

7 October 2025 – SARS is proud to announce the expansion of the Lwazi Artificial Intelligence (AI) Assistant across the SARS website and SARS MobiApp platforms. The upgraded Lwazi AI Assistant provides instant support with tax reference numbers, statements of account, notices of assessment, and the status of your audit or refund—anytime, anywhere.

Lwazi AI is designed with accessibility at its core, ensuring that tax support is easier for everyone, including users who are visually impaired. Welcome to a new era of smart, secure, and user-friendly tax services with SARS. Try Lwazi AI Assistant today—save time, skip the queues, and get the answers you need instantly!

Tired of long lines at the branch? Discover the SARS Online Query System (SOQS)

7 October 2025 – Watch our new step-by-step video to see what you can do on our online query system – Tired of long lines at the branch? Discover the SARS Online Query System (SOQS).