This edition of SMME Connect reflects on our strategic objectives to provide clarity and certainty for taxpayers to comply with their tax obligations, and to use data to enhance integrity, derive insights, and improve outcomes. We are educating taxpayers and traders through outreach engagements, collaboration with other public stakeholders, and roadshows to gain first-hand understanding of your challenges and needs. Also, read up on the Employer Interim Reconciliation Declaration (EMP501), which is open from 18 September to 31 October 2023.

Contact Centre Calls

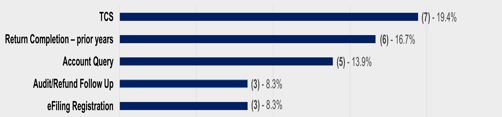

Our SMME division monitors and analyses data to understand clients’ needs and improve our service. We have taken a critical look at the monthly Contact Centre calls and found that our SMMEs still approach the Contact Centre for services that are available on digital channels.

We recommend that SMMEs use eFiling and the SARS Online Query System (SOQS) before calling the Contact Centre.

Top five queries in the Contact Centre

SMME Taxpayer Roadshows

Over the last two months, SARS’s SMME division convened a national roadshow with regional teams to gain insight into SMMEs’ challenges and to find solutions.

On 16 August 2023, the Nelspruit branch hosted an SMME roadshow in Mpumalanga, attended by Nelspruit and Standerton branch management. The session demonstrated the support and guidance that SMME teams can offer, which attendees found valuable.

Education Initiatives

To foster a culture of compliance, newly registered SMME taxpayers receive a welcome pack to inform them of their tax obligations.

Before the employer-reconciliation deadline, we held a webinar to educate employers about their obligations regarding third-party appointments. A third-party appointment (AA88) is when an employer or the bank acts on behalf of SARS to pay the outstanding debt on your behalf. You can learn more about third-party appointments on the SARS YouTube channel.

What’s New?

Enhancements to the eBooking System

To meet SMMEs’ demand for guidance on the eBooking system, we have optimised our system to:

- Enable SMMEs to book a SARS branch walk-in appointment via the eBooking system. Previously, this type of appointment could be booked only through the SARS Contact Centre.

- Display only available timeslots to avoid ‘timeslot not available’ messages.

- Automatically cancel booked slots if supporting documents are not uploaded within 24 hours, thereby freeing up timeslots.

- Accommodate hearing-impaired persons, who can now indicate their needs on the system and be accommodated when they visit a branch for their appointment.

New Dispute Rules

We have introduced new rules governing:

- The procedures when lodging an objection and appeal against an assessment or decision that is subject to objection and appeal under section 104(2) of the Tax Administration Act, 2011 (Act 28 of 2011).

- The dispute-resolution procedures under which SARS and the person aggrieved by an assessment or decision may resolve a dispute in accordance with Part C of the rules.

- The conduct and hearing of an appeal before a tax board or tax court.

Part G of the new rules contains transitional rules, which provide that disputes that have not been finalised by the new commencement date of 10 March 2023 will generally be dealt with and finalised under the new rules.

The most important change is the increase in the number of days in which a taxpayer may lodge an objection from 30 business days to 80 business days.

Compliance Calendar

The Employer Interim Reconciliation Declaration (EMP 501) Submission period is from 1 September to 31 October 2023.

The updated e@syFile™ Employer BETA version with enhanced features for download was released on 14 August 2023. Please see the Business Requirements Specification: PAYE Employer Reconciliation for the Employer Interim Reconciliation submission period 202308.

SMME employers should submit the Employer Declarations (EMP201) monthly because this facilitates the interim reconciliation submission. Importantly, the employer can use any of the following channels:

- eFiling (request and submit)

- eFiling ISV (submit)

- e@syFile Employer (request and submit)

eFiling makes it easy to submit an SMME (EMP501) reconciliation

eFiling is the fast and effortless way to submit EMP501 for small and medium-sized businesses. eFiling must not be used to correct a reconciliation that has already been submitted via e@syFile™ Employer for this filing period.

We urge all employers with 1 to 50 employees to file a reconciliation that contains a maximum of 50 IRP5/IT3(a) certificates (tax certificates) electronically via eFiling. To do this, log into SARS eFiling and click on the EMP501 work page. The employer can complete the tax certificates and the EMP501 reconciliation. The payroll system will generate a tax certificate file which will then be imported into eFiling.

Tax Compliance Status

We are aware that the letter we issued to apply for Tax Compliance Status (TCS) has caused some confusion.

The letter is titled ‘PIN Issued’. This means that SARS has issued a PIN, but this message has been mistaken for an indication that the taxpayer is tax compliant. This is not true.

Instead, the letter indicates:

- TCS details (name and reference number of the taxpayer to whom the PIN applies)

- PIN number

- Expiry date

The letter advised the requestor of the TCS as follows: ‘You may authorise a third party to view your TCS by providing with them the PIN. The PIN only allows the third-party access to your TCS. All other tax information remains secure’.

The third party who receives the PIN will log into their own profile on SARS eFiling and verify your TCS using the PIN provided. The view they will see will indicate:

![]() Green — the taxpayer is tax compliant

Green — the taxpayer is tax compliant

![]() Red — the taxpayer is non-compliant

Red — the taxpayer is non-compliant

For more information on TCS, see:

- Tax Compliance Status Guide

- How to request your Tax Compliance Status on SARS eFiling (video)

- Alternatively, the TCS can be requested via the SARS Online Query System.

Provisional Tax

Provisional tax is not a separate tax, but forms part of your income tax. It is a method of paying tax due to SARS bi-annually. This is to ensure that the taxpayer is not liable to pay a large amount of tax on income that is not subject to PAYE at the end of the tax year.

Provisional tax allows a taxpayer to make payments in advance during the year of assessment. These payments are based on the taxpayer’s estimated taxable income. The final tax liability is calculated upon assessment, and provisional payments made will offset the income-tax liability for that year of assessment.

Provisional tax is payable on all additional income, including business income other than your normal salary income, which is subject to PAYE.

Penalties can be levied for late submission, late payments, and penalties based on the underestimation of your liability. To avoid provisional tax penalties, provisional tax returns (IRP6) should be submitted online via SARS eFiling on or by 31 August 2023 (first provisional return) and February 2024 (second provisional return).

On 24 August 2023, SARS hosted a webinar on provisional tax to help taxpayers and traders fulfil their tax obligations and remain tax compliant. By offering guidance on provisional tax, the webinar was in line with SARS’s strategic objective to make it easy for SMMEs to comply with their tax obligations.

The webinar covered how to:

- Calculate the basic amount

- Calculate taxable income

- Determine the tax credits on the provisional tax

- Access the provisional tax return on eFiling

- Complete provisional tax on eFiling

Top Tips

How do I pay SARS?

You can pay SARS at a bank, via eFiling, or via electronic funds transfer (EFT). For more details on payment options, visit www.sars.gov.za.

Registered Representative

Companies are encouraged to have a representative registered at SARS for the eFiling system to work effectively.

Registered representatives at SARS enjoy benefits on the eFiling system, enabling them to:

- Search and add their SARS registered companies on eFiling

- Approve/reject tax-type activation

- Approve/reject tax-type transfer

- Activate the registered representative on eFiling to have full access

- Update the company’s registered details on the Registration, Amendment and Verification Form (RAV01).

Need help?

- Our online service, Help-You-eFile, allows you to interact with a SARS agent while the agent shares the displayed view of your eFiling profile screen. Through this service, the SARS agent can identify and resolve your tax-filing challenges. You benefit by being able to call on the support and advice of our staff without having to visit a SARS branch. You can even ask a SARS agent to call you back.

- For detailed guidance on how to file, you can watch our tutorial video on the SARS YouTube channel.

- If you must visit a SARS branch, ensure that you have booked your appointment before your visit.

Important Dates

- Individual taxpayers (non-provisional): 7 July 2023 to 23 October 2023

- Individual provisional taxpayers: 7 July 2023 to 24 January 2024

List of Scams

Beware of the latest email scam saying that a letter of demand that requires your attention was issued and telling you to click on a link to open the letter. Please ignore it and do not click on any links. If in doubt, please send an email to [email protected]. See an example of the latest scam.

Useful Links

Tax incentives are effective tools to promote economic growth. We encourage you to learn more about SARS’s incentive tools:

- Turnover Tax for micro businesses that have a turnover of R1 million and less. For more information, click here.

- Small Business Corporation for small businesses with an annual turnover of up to R20 million. These businesses may qualify to pay income tax at a reduced rate. For the qualifying criteria, please see the Tax Guide for Small Businesses.

- Employment Tax Incentive to incentivise employers to hire young job seekers. Click here to see the qualifying criteria.

For more information, go to the SARS website home page and select the Small Business tab.

#YourTaxMatters www.sars.gov.za