Charging of contingency fees

Tax practitioners’ fees for work they undertake on behalf of a client must be proportional to the nature and complexity of the task. In consultation with Recognised Controlling Bodies (RCBs), SARS has updated the criteria for the recognition of controlling bodies and the registration of tax practitioners. These criteria include rules on charging contingency fees. A contingency fee is a fee that a tax practitioner charges a taxpayer based on the percentage of a refund the taxpayer will receive or the percentage of a reduction of the taxpayer’s tax liability. To protect the interests of taxpayers and prevent revenue loss to fiscus, SARS wishes to clarify that:

- The charging of a contingency fee for completing or correcting tax returns is not an acceptable form of remuneration for tax practitioners.

- The charging of a contingency fee is acceptable:

- when there is a dispute between the taxpayer and SARS under Chapter 9 of the TA Act, and

- when the taxpayer brings an application for SARS to review its decisions under section 9 of the TA Act.

Note:

- Charging of contingency fees for submission of tax returns has been forbidden since 2013.

- Charging of contingency fees is not allowed for correcting tax returns from 14 September 2023.

Where contingency fees are allowed, the tax practitioner must enter into a written agreement with his/her client. The agreement should contain sufficient information on:

- The details of the tax practitioner and the taxpayer,

- The outcome upon which the contingency fees are based and its percentage,

- The consequences if the outcome is not achieved, and

- When the contingency fees are charged.

The agreement should also contain a clause that gives:

- The taxpayer client has the right to refer the agreement to the relevant RCB for review, and

- The RCB has the authority to set aside any provision of the agreement or any fees claimable in terms of the agreement if the RCB finds such provision or fees unreasonable or unjust.

Suspension of licences and registration of SMME Traders and Clearing Agents who are not onboarded onto RLA (Registration Licencing and Accreditation) eFiling

In April 2020, SARS rolled out a secure online Customs Trader Portal for online applications for licensing and registrations to Customs through eFiling. SARS enhanced the system and used multiple channels of communication to create awareness around this project. See the letter issued to traders and clearing agents: https://www.sars.gov.za/wp-content/uploads/Docs/Customs/Letter-to-trade-RLA-On-Boarding-26-August-2022.pdf

Following these awareness campaigns, SARS is embarking on a drive to suspend or cancel licences and registrations that are not on RLA eFiling. Traders and Clearing Agents who have not onboarded themselves onto the RLA eFiling system should either apply for licenses or register, whichever is applicable, immediately.

Affected SMME Traders and Clearing Agents who have not onboarded will receive letters of SARS’s intention to suspend or cancel their licenses and registration. They will have a 21-day grace period — from the date of the letter SARS issued to them — to onboard or to provide SARS with reasons why they cannot onboard. Failure to onboard or to respond to the letter will result in suspension or cancellation of the licence and registration and they will be unable to transact with SARS.

For assistance on how to onboard, please view this presentation:

The how-to video can be accessed via:

SARS publishes PAYE monthly submission external BRS

SARS seeks to replace the current employees’ tax, provisional tax, and assessment filing seasons for Employers and non-business individuals with a modern, fully automated tax-assessment, withholding, and tax-payment system.

The first step in achieving this objective requires Employers to submit payroll data monthly from 1 March 2025.

The PAYE Monthly Submission External BRS defines the requirements Employers must adhere to for the monthly submissions.

Additional functionality for the SARS Online Query System (SOQS)

SARS has introduced additional functionality on SOQS. Queries can now be lodged for Large Business Institutions. This information can be found here:

https://www.sars.gov.za/contact-us/

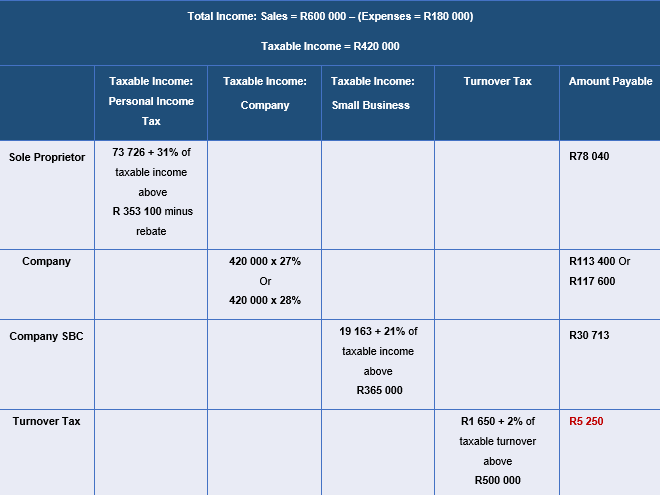

Are you a Tax Practitioner with micro-businesses as clients? Then you must tell them about Turnover Tax

Turnover Tax is an optional simplified tax system for micro-businesses with a qualifying turnover of R1 million or less per year. Turnover Tax taxes turnover and not profit. Turnover Tax simplifies and reduces the number of tax returns that micro-businesses must file and replaces the need to account for Income Tax, VAT (unless you have elected to be in the VAT system), Provisional Tax, Capital Gains Tax, and Dividends Tax.

Who can qualify for Turnover Tax?

- Individuals (sole proprietors)

- Partnerships

- Close corporations

- Companies

- Co-operatives

Take our test at https://www.sars.gov.za/types-of-tax/turnover-tax/quick-test-for-individuals-and-companies/ to see if you qualify for this incentive.

Here’s an example of how Turnover Tax compares with tax rates:

For more information about Turnover Tax, visit the Turnover Tax webpage at https://www.sars.gov.za/types-of-tax/turnover-tax/.

Food manufacturers can now register online for the Excise Diesel Refund for Food Manufacturers Scheme

To learn more about the Excise Diesel Refund for Food Manufacturers Scheme, visit the online registration system at: https://tools.sars.gov.za/sarsonlinequery/DieselRefundsRegistration.

To apply to register as a refund user, fill in the DA185 form and Annexure DA185.4A3. Submit the form and supporting documents on SOQS.

For assistance to complete the DA185, DA185.4A3, or DA66 forms, see the short tutorial videos on the SARS YouTube channel:

For more information on the refund item, see the click Diesel Refund Foodstuff Manufacturers Scheme webpage.

Expansion of IT3 Third Party Data Reporting to include Income from Trusts and Donations Made

Through SARS eFiling, you can securely submit IT3 third party data to SARS.

Two additional third-party data submissions have been added:

- IT3(t): income received from a Trust

- IT3(d): declarations pertaining to Section 18A donations

The third-party data-reporting process requires Representative Taxpayers to report the required ITR12T information via the IT3-01 and IT3-02 forms. Representative Taxpayers can view and correct the data or certificates submitted to SARS on request.

SARS requests that Section 18A approved entities (e.g., Government Institutions, Public Benefit Organisations, or United Nations Agencies) that received donations and issued tax-deductible receipts to Donors, to report those receipts to SARS. If a receipt was issued, then it should be reported to SARS. SARS has updated the documents pertaining to these processes. We have also developed a new guide on how to manage the submission of IT3 third-party data:

- GEN-ENR-01-G01 – Guide for the Submission of Third-Party Data using the Connect Direct channel – External Guide

- GEN-ENR-01-G02 – Guide for the Submission of Third-Party Data using the HTTPS Channel – External Guide

- GEN-ENR-01-G03 – Guide for the Submission and Declaration of IT3 Third-Party Data via eFiling – External Guide

- GEN-ENR-01-G10 – Manage Submission of IT3 Third Party Data – External Guide

Tax Directives system implemented

SARS has enhanced the Tax Directives system in line with the IBIR-006 Tax Directives Interface Specification Version 6.505. SARS thanks those who assisted with the Trade Testing for this solution. For more information, see the I want a Tax Directive webpage.

Customs refunds and drawbacks

Customs and Excise Refunds and Drawbacks have been automated. Apply for these through eFiling. For assistance, read the SC-DT-C-19 – Refunds and Drawbacks–External Guide.

Employer Interim Reconciliation Declarations (EMP501)

The following has been implemented for the PAYE Interim Filing Season:

- No new source codes were added, but there are minor changes to certain field types and validations.

- Enhancements to IRP5 certificates.

- Enhancements to Employment Tax Repository.

- EMP201 returns for suspended (s-coded) Employers: Employers will be prevented from submitting EMP 201 returns once the Employer’s status reflects as suspended. This will be effective for the period from the date of suspension. See the guide here: PAYE-AE-06-G07 – Guide for Validation Rules Applicable to Reconciliation Declarations 2024 – External Guide.

- Enhancements to EMP501 Reconciliation.

- Section 95 estimates.

Updated external guides:

- PAYE-AE-06-G06 – Guide for Codes Applicable to Employees Tax Certificates 2024 – External Guide

- PAYE-AE-06-G07 – Guide for Validation Rules Applicable to Reconciliation Declarations 2024 – External Guide

- PAYE-AE-06-G08 – Guide for Completion and Submission of Employees Tax Certificates 2024 – External Guide

- EMP-GEN-02-G01 – A Guide to the Employer Reconciliation Process – External Guide

Enhancements to Trusts’ beneficial-ownership information

SARS aims to record all beneficial owners of registered Trusts to comply with the Financial Action Task Force requirements. Information in this regard must be submitted via e-Filing. These documents may include:

- An organogram or illustration depicting effective control of the Trust. Where the Beneficial Ownership is in the form of other legal arrangements or legal entities, this should be provided in a separate attachment.

- An Excel spreadsheet containing the above information; or

- Other documents that elaborate on Beneficial Ownership in relation to the Trust.

When capturing the beneficial ownership-information, it is mandatory for the current year’s return to submit at least one document that relates to beneficial-ownership information. If there are more than 20 beneficial owners, the taxpayer must upload a supporting document that reflects the additional beneficial owners.

Submit all minutes, excluding those dealing with internal trustee governance arrangements or administrative matters. A guide on Trusts is available here: IT-AE-36-G02 – Comprehensive Guide to the Income Tax return for Trusts – External Guide

SARS Payment Rules Guide

The SARS Payment Rules Guide has been updated to include African Bank and Bank Zero for electronic fund transfers (EFTs) to SARS’s public beneficiaries listed on the banking platform. With effect from 15 September 2023, Air Passenger Tax payments will be allowed only on eFiling. Access the guide here: GEN-PAYM-01-G01 – SARS Payment Rules – External Guide

VAT Connect Newsletter

The latest VAT Connect Newsletter is available here: VAT Connect Issue 16 (August 2023) | South African Revenue Service (sars.gov.za)

VAT-modernisation discussion paper published

SARS has published a discussion paper on VAT modernisation. This discussion paper sets out SARS’s vision to modernise South Africa’s VAT administrative framework.

The discussion paper invites businesses (vendors), accounting-system software developers or suppliers, technology entities, recognised controlling bodies, public-finance entities, municipal-finance entities, and the public to submit contributions and comments to help modernise the VAT administrative framework.

The discussion paper is available here: Discussion Paper on Value-Added Tax Modernisation. Submit comments by close of business on 31 October 2023 to [email protected].

Information on deceased and insolvent estates

Updated document:

- FAQ on deceased estates and the administration of deceased estates leaflet: https://www.sars.gov.za/lapd-it-g31-faqs-on-deceased-estates/

Resources on estates:

- Estates webpage: https://www.sars.gov.za/businesses-and-employers/estates/

- Estate duty webpage: https://www.sars.gov.za/types-of-tax/estate-duty/

Links to digital channels on SOQS:

- Report new estate case: https://tools.sars.gov.za/SOQS/?queryType=13

- Supporting documents to report a new estate case: https://www.sars.gov.za/faq/faq-what-supporting-documents-must-i-submit-to-report-a-new-estate-case/

- Update the Representative Taxpayer’s details: https://tools.sars.gov.za/SOQS/?queryType=12

- Change of banking details: https://www.sars.gov.za/wp-content/uploads/Ops/Guides/GEN-GEN-41-G01-Change-of-Banking-Details-External-Guide.pdf

- Book an appointment: https://www.sars.gov.za/contact-us/make-an-appointment/

Sequestration of an individual:

- Webpage and FAQ for the insolvent estates of individuals: https://www.sars.gov.za/types-of-tax/personal-income-tax/pit-insolvency/

Liquidations:

- Webpage and FAQ on liquidations: https://www.sars.gov.za/businesses-and-employers/liquidations/