SARS Commissioner, Edward Kieswetter, recently met with the leadership of controlling bodies in the tax practitioner community. The engagement was to create an understanding of the strategic direction of SARS, and to discuss the commitment of external stakeholders towards building a culture of voluntary compliance in the country.

Tax practitioners and their controlling bodies are important stakeholders, as they influence the behaviour of taxpayers. Currently, SARS has almost 24000 registered tax practitioners, representing almost 3.5 million taxpayers, thus making tax practitioners an essential partner for SARS in the journey towards achieving higher compliance levels.

Commissioner Kieswetter is committed to increasing compliance levels and has included the strategic objective “working with and through stakeholders” in his strategic plan for the organisation. This includes RCBs and tax practitioners and emphasizes SARS’ willingness to engage with external bodies on the journey towards improved compliance.

Since taking over the reins at SARS, the Commissioner’s leadership has been characterised by transformation within the organisation. He has a clear vision of building a smart and modern tax authority, with unquestionable integrity, trusted by government, stakeholders, the public and our international peers.

To execute the SARS mandate optimally, a culture of voluntary compliance should prevail that will increase revenue collection, and build a sense of responsible fiscal citizenship. This theme resonated during the recent leadership level meetings with the sector.

The Commissioner noted that the current narrative around State Capture was one of the reasons for lower compliance. He informed the meeting that SARS was on a mission to identify such non-compliance and to address it, whether it existed internally or in the external environment. He also noted that SARS is currently pro-actively working to identify the tax compliance of individuals involved in public spaces like the Zondo Commission and the media.

The Nugent Commission found that SARS had been a victim of State Capture, resulting in a loss of public trust in the institution and its staff. The Commissioner plans to change the current perception by committing SARS to the following nine strategic objectives:

- Make it as easy and simple as possible to comply with tax obligations

- Create awareness of tax obligations, as well as clarity and certainty about expectations

- Make it difficult and costly not to comply

- Modernise SARS’ systems to provide seamless online digital services

- Use data for insights, risks and improved outcomes

- Develop an engaged, agile and diverse workforce

- Use resources efficiently to deliver quality outcomes and excellence

- Work with, and through stakeholders to improve the tax system

- Build credibility, public confidence and trust.

While each of the nine objectives is necessary to achieve voluntary compliance, many of them are inter-related. For example, the importance of credibility, public confidence and trust count among the top strategic objectives.

However, to achieve this, SARS believes in building a strategic partnership with stakeholders to improve the tax system and respond to their needs, which is an essential and interconnected strategic objective.

The new SARS structure is intentionally flatter to entrench more accountability amongst SARS leaders, the Commissioner responded to questions from RCBs attending the meeting, adding that the specific objective was to facilitate deeper focus on different sectors. Whilst the former structure was more centralised, the new segmented approach is meant to increase the authority and responsibilities of the newly appointed 12 regional directors, supported, amongst others, by two senior leaders to take responsibility for stakeholder strategic development and operational matters.

He said a list of Senior SARS Officials (SSOs) would be published on the website as soon as SARS is in a position to finalise the matter, which had been difficult to complete as the external recruitment drive has been held back due to the Covid-19 pandemic.

Regarding SARS’ plans to deal with intentional non-compliance, Commissioner Kieswetter acknowledged that the previous SARS model concentrated more on following up on taxpayers who had submitted and declared income, while deliberate non-compliance was not adequately dealt with. SARS has also identified non-compliance relating to PAYE return submissions as a serious risk, and is currently looking at external sources to develop our capacity in this regard.

Referring to SARS’ strategic objective of working with and through stakeholders to improve the tax system, the Commissioner assured the tax practitioner community that SARS regards tax practitioners as an intrinsic part of the journey to tax morality.

Ms Dipuo Mvelase, as Head of the Government & Tax Practitioner segments, would concentrate on deepening our understanding of these two critical groups of stakeholders. It is expected that from such understanding, SARS will be able to contextualise our service offerings, which the sector will find useful. In addition, this segment will concentrate on incentivising a compliance culture that rewards consistent high compliance. Mr Mark Kingon, as head of Stakeholder Relationships, is responsible for end-to-end relationships with stakeholders, including the RCB’s, and will work together with the Government & Tax Practitioner segment to ensure synergy and consistent messaging when SARS engages the sector. Stakeholder Relations will deal with the critical more systemic escalations and ensure that the relationship with stakeholders is stabilised and improved.

SARS is also considering a mechanism to act as an early warning system for non-compliant tax practitioners, to allow the RCB to intervene before SARS takes action against a tax practitioner, as an initiative to provide a more effective and efficient service to this sector.

In conclusion, the Commissioner said that “SARS is looking forward to building a strategic partnership with the tax practitioner community, which will benefit both your clients and SARS.”

There seems to be some misunderstanding regarding the approvals of tax type transfers by means of Powers of Attorney (PoAs) on eFiling, granted to tax practitioners by taxpayers.

SARS has implemented a new functionality on eFiling, which allows taxpayers or their registered representatives to authorise the transfer or any movement of Personal Income Tax eFiling profiles via the online Power of Attorney (PoA). It forms part of a number of digital enhancements that are meant to make it easy to comply.

This new, streamlined digital process of transferring a taxpayer’s tax affairs per tax type from one practitioner to another, requires the taxpayer to accept and digitally approve an online PoA. This includes approval and provision of a PoA to a new practitioner, thus a taxpayer is obliged to complete the online PoA to enable a tax practitioner to have access to the client’s eFiling profile.

Tax practitioners may not approve a PoA on behalf of a client, pretending to be the taxpayer or their representatives is a misrepresentation of the facts, hence unlawful.

The requirement that a taxpayer must approve a PoA is embedded in the legal principle that a person can only act (including submit a tax return on eFiling) on behalf of another if the latter person has authorised the former to do so. Such authorisation is given in the form of a PoA and misuse of that would be seen as unlawful.

Non-compliance

For example, some practitioners update a taxpayer’s records and approve transfers fraudulently by changing the taxpayer’s cell number to their own, in order to receive an OTP. This is equivalent to imitating a taxpayer’s signature, thereby exceeding the PoA given to the tax practitioner, and constitutes an unlawful practice.

We have started to track IP addresses to identify possible unlawful tax type transfers by means of PoAs approved by tax practitioners, in order to put an end to this practice. In cases where changes or transfers are requested and the approval comes from the same computer (IP address), there is a high probability that it originates from the same person, i.e. the tax practitioner, and SARS will follow the matter up.

SARS has already written a number of Cease and Desist letters to tax practitioners in this regard. Should SARS find that practitioners continue to request transfers and approve their own PoAs, SARS will register cases of fraud and of the statutory offences under section 234 of the Tax Administration Act, as well as lodge a complaint with the relevant controlling body (RCB). This may also result in the suspension of a tax practitioner from eFiling.

For your information, kindly refer to the Guide on How to Register for eFiling and Manage Your Profile, or see the FAQ on the Tax Practitioner’s Page under How do I initiate a tax type transfer on eFiling?

There seems to be some misunderstanding regarding the approvals of tax type transfers by means of Powers of Attorney (PoAs) on eFiling, granted to tax practitioners by taxpayers.

SARS has implemented a new functionality on eFiling, which allows taxpayers or their registered representatives to authorise the transfer or any movement of Personal Income Tax eFiling profiles via the online Power of Attorney (PoA). It forms part of a number of digital enhancements that are meant to make it easy to comply.

This new, streamlined digital process of transferring a taxpayer’s tax affairs per tax type from one practitioner to another, requires the taxpayer to accept and digitally approve an online PoA. This includes approval and provision of a PoA to a new practitioner, thus a taxpayer is obliged to complete the online PoA to enable a tax practitioner to have access to the client’s eFiling profile.

Tax practitioners may not approve a PoA on behalf of a client, pretending to be the taxpayer or their representatives is a misrepresentation of the facts, hence unlawful.

The requirement that a taxpayer must approve a PoA is embedded in the legal principle that a person can only act (including submit a tax return on eFiling) on behalf of another if the latter person has authorised the former to do so. Such authorisation is given in the form of a PoA and misuse of that would be seen as unlawful.

Non-compliance

For example, some practitioners update a taxpayer’s records and approve transfers fraudulently by changing the taxpayer’s cell number to their own, in order to receive an OTP. This is equivalent to imitating a taxpayer’s signature, thereby exceeding the PoA given to the tax practitioner, and constitutes an unlawful practice.

We have started to track IP addresses to identify possible unlawful tax type transfers by means of PoAs approved by tax practitioners, in order to put an end to this practice. In cases where changes or transfers are requested and the approval comes from the same computer (IP address), there is a high probability that it originates from the same person, i.e. the tax practitioner, and SARS will follow the matter up.

SARS has already written a number of Cease and Desist letters to tax practitioners in this regard. Should SARS find that practitioners continue to request transfers and approve their own PoAs, SARS will register cases of fraud and of the statutory offences under section 234 of the Tax Administration Act, as well as lodge a complaint with the relevant controlling body (RCB). This may also result in the suspension of a tax practitioner from eFiling.

For your information, kindly refer to the How to register for eFiling and manage your user profile, or see the FAQ on the Tax Practitioner’s Page under How do I initiate a tax type transfer on eFiling?

SARS welcomes a recent Gauteng High Court’s decision, which clarified an important principle. The principle in this case was whether a decision to audit a taxpayer is an administrative action. If a decision to audit is deemed an administrative act, then that decision is reviewable in terms of the Promotion of Administrative Justice Act or under the principle of legality.

If that were the case, SARS would need to demonstrate that the decision to audit is rational and justifiable. This would have to take place before the actual audit engagement.

In the judgement, handed down on 31 August 2020, the court however, found that to select a taxpayer for an audit does not adversely affect a taxpayer’s rights, and that a SARS audit is the start of an investigation and the initiation thereof is not subject to review, as the decision is incomplete.

According the SARS Litigation Unit, there has been an increase in the number of administrative challenges to SARS’ actions and decisions over the years. Such a legal challenge on an administrative matter delays the progress of an audit, sometimes for years, which is often the purpose of such an administrative or collateral challenge.

In this particular case, the taxpayers suspected non-compliance with the Customs and Excise Act, which led SARS to include a risk assessment on the taxpayer’s compliance with Value Added Tax (VAT) and Income Tax. This process established that there were discrepancies in the turnovers declared by the taxpayers and their customs declarations, leading to the decision to audit the taxpayers. The taxpayers elected not to participate in the audit nor provide any of the requested information as they contended their tax affairs were in order, and that the decision to audit them was unlawful. SARS continued with an audit and the taxpayers launched a review application in the High Court in April 2015.

The taxpayers requested the court to review and set aside the Commissioner’s decision to audit the taxpayers, arguing that the decision was unlawful for being arbitrary and irrational, and done for ulterior motives and in bad faith. SARS opposed the application on the basis that a decision to audit the taxpayers is not a reviewable administration action and that the taxpayers would have an opportunity to dispute the findings using the dispute procedure.

The Gauteng High Court concurred with SARS in its judgment on 31 August 2020.

It was pointed out that it was equally important to recognise that decisions like these provide clarity and certainty, and that SARS will continue to make it hard and costly to raise collateral challenges unnecessarily.

To read the judgement, click here.

Service offerings available on eFiling

There is no need to go to a branch office for the following service offerings:

- Enquire on debt outstanding and make a payment

- Enquire on returns outstanding

- Tax Compliance Status

- Notice of Registration (IT150)

- Filing your Income Tax Return

- Update personal details (including Bank Details)

- Request Statement of Account

- Register for Income Tax (Completed by your employer on eFiling)

- Submission of Supporting Documents for an audit case

- Progress of an audit case

SARS online query system

SARS has introduced an online query system. Click on the link for more information and instructions to follow when making use of this online facility SARS Online Query System.

This means it is not necessary to go to a branch to do any of the following:

- Submit supporting documents,

- Submit a payment allocation,

- Request your Tax Reference Number if you have forgotten it.

If your case number and tax number does not match our records or if we did not receive the documents due to technical error, we will send you an email with instructions to resubmit the documents.

Note: It is recommended that you use Google Chrome, Microsoft Edge, Firefox or Safari to access the form. Please do not use Internet Explorer.

How to make an eBooking

There are two options to book an appointment with SARS:

- Book an appointment via our eBooking online system for video or telephonic engagement.

- Book an appointment by calling us on 0800 11 7277 (toll-free) for video telephonic engagements.

- You may also request a physical walk-in appointment through the

0800 11 7277 number.

Click here to find all the information relating to making an appointment with a SARS consultant. The web page also indicates what you need to know before you make an appointment.

Note that you will be able to submit relevant supporting documents electronically through the SARS Online Query System.

SARS has also rationalised the email addresses to be used by taxpayers and tax practitioners. The email addresses to be used are as follows:

- Tax practitioners: [email protected]

- Taxpayers: [email protected]

For the uploading of supporting documents tax practitioners and taxpayers can make use of [email protected].

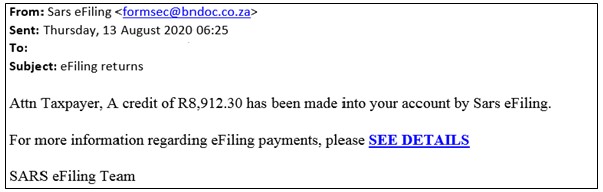

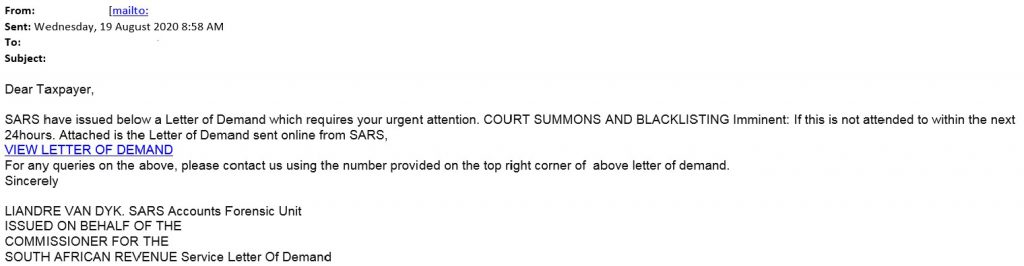

There has been an increase in email scams and phishing attacks in which our SARS brand is being abused. Members of the public are randomly emailed using false email addresses that seem as if they were sent from SARS, but are in fact fraudulent emails aimed at enticing unsuspecting taxpayers to part with personal information such as bank account details.

Mr Fred Salimane, Executive: Internal Investigations in the Anti-Corruption Unit, says these scams come in various forms such as letters, emails, website links and even individuals either posing as SARS officials, debt collectors or tax preparers.

Some of these scams are presented as notifications of tax refunds that are due to the taxpayers. Examples include emails that appear to be from SARS, with addresses such as [email protected] or [email protected]. In some instances, they provide a link to a website identical to the SARS e filings website. When the taxpayer accesses the e-filing replica via the link, they are asked to select a link to their bank to enable a refund to be paid into their bank account, which directs them to their bank’s fake website.

Recently, SARS employees were also the target of a phishing attack where some employees received an email requesting them to revalidate ’web directory and login details’ sent from ’ICT Service’.

Tips to protect yourself against identity theft and identity fraud

1. SARS will never request a taxpayer’s banking details in any communication that they receive via post, email, or SMS. However, for the purpose of telephonic engagement and authentication purposes, SARS will verify your personal details.

Importantly, SARS will not send any hyperlinks to other websites – even those of banks.

2. SARS will never ask for a taxpayer’s credit card details.

3. SARS does not send *.htm or *.html attachments

4. Taxpayers should never give anyone their ID number or other personal information unless the taxpayer initiated the contact, or if she/he is sure they know who they are dealing with.

5. Protect financial information. Taxpayers must ensure that their tax information, bank statements and other financial documents are kept in a secure place.

6. Don’t respond to emails that provide a website link, which requires you to log in and provide your password details, or update your personal information.

Top Tip: Be sure you can identify a secure website:

- Check the website URL. The website address usually starts with HTTP, but with a secure connection, the address should begin with HTTPS. The S stands for ‘Secure’.

The lock icon is not just a picture. Click or double-click on it to see the details of the site’s security. This is important to know as some fraudulent websites are built with a bar at the bottom of the webpage to copy the lock icon of the browser. Therefore, it is necessary to test the icon to make sure you can view the security information. SARS therefore urges tax practitioners to be vigilant of these phishing attacks and to report them at [email protected]. Additionally, we also recommend that you please make your clients aware of these phishing scams, see list of all known scams.

Recent examples:

We would like to remind you of a number of key dates in this year’s filing season.

Taxpayers who require assistance may call our contact centre to complete their tax returns, with the assistance of an agent until 16 November.

Taxpayers may make an appointment over the phone or use our appointment facility on our website, and will be assigned a slot to visit a SARS branch. We are concerned for your safety and that of our employees and as such we would urge you to use the many electronic avenues available to you.

SARS has introduced a toll-free number for taxpayers to call and make branch appointments, and the number is 0800 11 7277. All the information on making an appointment with SARS is available here.

16 NOVEMBER 2020

This is the closing date for taxpayers who file online using the eFiling website or MobiApp.

29 JANUARY 2021

This is the final date for provisional taxpayers to fulfil all their outstanding filing obligations.