Monthly Tax Digest newsletter is now available

17 February 2026 – In the February 2026 issue we take a closer look at important SARS deadlines that are around the corner and the Voluntary Disclosure Programme (VDP).

Crypto Asset reporting framework (CARF) external BRS

16 February 2026 – Final External BRS V 1.5 for Crypto Asset Reporting Framework (CARF) for implementation effective 1 March 2026.

- Under the CARF Reporting Crypto-Asset Service Providers (RCASPs) are required perform due diligence for the purpose of reporting crypto data to SARS.

- The schema documentation covers:

- CARF_SARS – specifies the SARS requirements

- CARF_OECD – specifies the OECD standard requirements

Automatic Exchange of Information BRS AEOI: CRS & FATCA

16 February 2026 – The Final External BRS Version 3.0.0-17 for AEOI: CRS & FATCA applicable from 01 March 2026.

Changes are aligned to the:

- CRS XML Schema V.3

- Revised Common Reporting Standard (CRS) Regulations.

Amendments are as follows:

- Account Holder Demographic Data: Added new fields for Equity Interest Type and Self Certification.

- Account Holder Financial Data: Added Account Number Type, Account Type, Due Diligence Procedure, and Joint Account.

- Controlling Person Demographic Data: Added Controlling Person Type and Self Certification.

- The Reporting Financial Institution (RFI) may now submit one or more records in a single submission to SARS, provided all are NULL declaration submissions.

Customs Weekly List of Unentered Goods now available

16 February 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Adjustment to Diesel Refund for Onland Users in Farming, Forestry, and Mining Sectors

13 February 2026 – Effective from 1 April 2026, primary sector claimants operating onland will be entitled to claim a refund on 100% of eligible diesel used in qualifying farming, forestry, and mining activities. This amendment streamlines the administration of the Diesel Refund Scheme. To ease the transition, the new rate, which is effectively applied from the April 2026 return, will reflect only from the calendar month when this VAT return must be submitted, i.e. May 2026.

For more information, see the letter to stakeholders.

Global Minimum Tax

13 February 2026 – The Business Requirements Specification (BRS) for the Global Anti-Base Erosion (GLOBE) programme has now been published on the GLOBE webpage.

Excise Fuel Registrations

13 February 2026 – From 3 February 2026, you need to complete and submit the DA185 form to apply for or renew your permission to participate in these activities:

- To possess, control, or use goods consisting of a mixture which includes marked goods as provided for in section 37A(9) and rule 37A.12.

- Supply of aviation kerosene or aviation spirit (rebate items 460.05 / 496.00 or 623.11 / 671.01) as provided for in section 37A(9) and rule 37A.13.

- Producing goods not capable for use in any engine as provided for in section 37A(4) and rule 37A.11.

Submit the completed DA185 form, together with the applicable annexures, at the nearest SARS branch office, to which the applicant’s business premises will be registered.

For enquiries, please send email to [email protected].

Legal Counsel – Preparation of Legislation – Draft Documents for Public Comment

13 February 2026 – Customs and Excise Act, 1964

- Draft amendments to rules under sections 47B and 120 – Air passenger tax

Due date for comment: 6 March 2026

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

13 February 2026 – Customs and Excise Act, 1964: Publication details for tariff amendments notices R7114, and R7115, as published in Government Gazette 54108 of 13 February 2026, are now available.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

12 February 2026 – Customs and Excise Act, 1964: The tariff amendments notices, scheduled for publication in the Government Gazette, relate to the amendments to –

- Part 1 of Schedule No. 1, by the substitution of tariff subheadings 1701.12, 1701.13, 1701.14, 1701.91, and 1701.99, to increase the rate of customs duty on sugar from 436.38c/kg to 483.72c/kg in terms of the existing variable tariff formula (ITAC Minute 10/2025); and

- Part 1 of Schedule No. 1, by the substitution of tariff subheadings 1001.91 and 1001.99 as well as 1101.00.10, 1101.00.20, 1101.00.30 and 1101.00.90, to reduce the rate of customs duty on wheat and wheaten flour from 85.15c/kg and 127.72c/kg, respectively to 61.90c/kg and 92.85c/kg, in terms of the existing variable tariff formula (ITAC Minute M09/2025).

Publication details will be made available later

Legal Counsel – Secondary Legislation – Rules Amendments 2026

12 February 2026 – Customs and Excise Act, 1964: Publication of rules amendments notice R7132, as published in Government Gazette 54129 of 12 February 2026:

- Amendment to the rules under sections 17 and 120 – State warehouse rent (DAR268)

BRS – PAYE Employer Reconciliation for 2026 / 2027

12 February 2026 – The BRS – PAYE Employer Reconciliation for 2026 / 2027 is now available.

What has changed:

- New fields were added to prevent duplicate registrations using the ITREG process

- Validation and/or description changes to some existing source codes.

SARS Digital platform upgrades on 13 February 2026

12 February 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Friday, 13 February 2026 from 18h00 to 23h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Responses (CUSRES messages) to Customs declarations submitted during this time may be delayed, however, arrival and exit management functions will be available at land border posts for all released declarations and manifests.

Stakeholders are therefore urged to submit all Goods Declarations (bills of entry) and Road Manifest, especially those deemed priority, by Friday, 13 February 2026 @ 17h00.

The latest SMME Connect Newsletter is now available

11 February 2026 – This issue reminds Small, Medium, and Micro Enterprises (SMMEs) to submit outstanding returns, pay any tax due, and use available incentives. Qualifying businesses are also encouraged to register for Turnover tax and we look at the updated guide to supply of electronic services by foreign suppliers.

Tax Directives: Revised ISV trade testing dates

11 February 2026 – Originally, we communicated that trade testing would commence on 9 February 2026 and conclude on 12 March 2026. However, due to unforeseen technical difficulties, we regret to inform you that the ISV trade testing will now commence from the 2 March 2026 and conclude on the 15 April 2026.

We understand the inconvenience this delay might cause and appreciate your patience and understanding as we work through these technical challenges. The final software implementation is planned for April 2026.

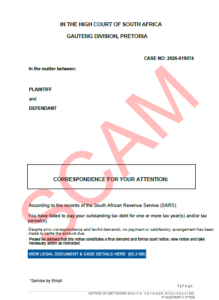

Latest Scam Alert: Email with Summons Notification

10 February 2026 – Beware of a PDF letter being emailed to people with the email subject line ‘ATTACHED SARS SUMMON AGAINST YOU’. Scams are changed on a regular basis so the subject line may differ. The letter contains a link to a fraudulent phishing website. Please do not click on any links. You should always type in the SARS eFiling address in your browser or click on the eFiling login from the SARS website homepage (sars.gov.za). If in doubt, go to our Scams and Phishing webpage where we will publish some examples or forward the suspicious email to [email protected].

Preview of this scam:

Legal Counsel – Dispute Resolution & Judgments – High Court 2028-2026

9 February 2026 – Tax Administration Act, 2011, and Promotion of Administrative Justice Act 3 of 2000

Section 164(3) of the Tax Administration Act 28 of 2011 (TAA) – Pay Now Argue Later – Section 9 reconsideration request – Section 6(2)(f) of Promotion of Administrative Justice Act 3 of 2000 (PAJA) – whether SARS, acting under section 9 and section 164 of the TAA, and subject to review under section 6 of PAJA, acted lawfully and fairly when it refused to suspend the taxpayer’s obligation to pay the disputed tax debt despite the taxpayer offering substantial security through his TMM shareholding.

Legal Counsel – Dispute Resolution & Judgments – High Court 2025–2023

9 February 2026 – Tax Administration Act, 2011

Tax Administration Act, 2011 – section 177 – whether the respondent is factual insolvent with inability to pay his tax debt – whether the respondent has committed acts of insolvency by dissipating his immovable property to the family trust.

Customs Weekly List of Unentered Goods now available

9 February 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Final demand issued for annual income tax returns for Trusts

9 February 2026 – In an effort to increase the compliance levels of trusts, SARS has issued final demands to trusts who did not submit an annual tax return for the 2024 and 2025 years of assessment. In terms of section 210(2) of the Tax Administration Act, SARS will shortly issue the related public notice for the imposition of administrative non-compliance penalties for trusts. It is important that those in receipt of such final demands as referred to above, take steps to correct the non-filing of the annual income tax returns within the period before the administrative penalties will be raised. SARS notes that, subsequent to the issuance of the final demand, several trusts have already taken steps towards improving their tax compliance. SARS supports and appreciates these efforts.

It is reiterated that all trusts, whether economically active or passive, are required to submit annual income tax returns in accordance with the requirements set out in the public notice. This obligation is an operation of law and is applicable to every registered resident trust (without exception) and certain qualifying non-resident trusts.

SARS emphasises that the responsibility for obtaining, maintaining, and updating accurate trust information rests exclusively with the trustees. This includes the initiation of de-registration processes for trusts that meet the applicable criteria. The trustees must undertake these actions for compliance with statutory requirements and adherence to proper governance practices. This will assist SARS to ensure that the trust tax register is up to date.

Trustees bear sole responsibility for ensuring that all trust information reflected on the SARS Registration, Amendments and Verification (RAV) system is up to date and properly maintained.