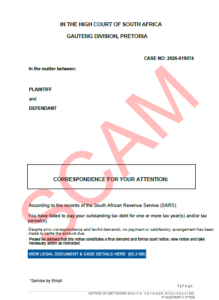

Latest Scam Alert: Email with Summons Notification

10 February 2026 – Beware of a PDF letter being emailed to people with the email subject line ‘ATTACHED SARS SUMMON AGAINST YOU’. Scams are changed on a regular basis so the subject line may differ. The letter contains a link to a fraudulent phishing website. Please do not click on any links. You should always type in the SARS eFiling address in your browser or click on the eFiling login from the SARS website homepage (sars.gov.za). If in doubt, go to our Scams and Phishing webpage where we will publish some examples or forward the suspicious email to [email protected].

Preview of this scam:

Legal Counsel – Dispute Resolution & Judgments – High Court 2028-2026

9 February 2026 – Tax Administration Act, 2011, and Promotion of Administrative Justice Act 3 of 2000

Section 164(3) of the Tax Administration Act 28 of 2011 (TAA) – Pay Now Argue Later – Section 9 reconsideration request – Section 6(2)(f) of Promotion of Administrative Justice Act 3 of 2000 (PAJA) – whether SARS, acting under section 9 and section 164 of the TAA, and subject to review under section 6 of PAJA, acted lawfully and fairly when it refused to suspend the taxpayer’s obligation to pay the disputed tax debt despite the taxpayer offering substantial security through his TMM shareholding.

Legal Counsel – Dispute Resolution & Judgments – High Court 2025–2023

9 February 2026 – Tax Administration Act, 2011

Tax Administration Act, 2011 – section 177 – whether the respondent is factual insolvent with inability to pay his tax debt – whether the respondent has committed acts of insolvency by dissipating his immovable property to the family trust.

Customs Weekly List of Unentered Goods now available

9 February 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Final demand issued for annual income tax returns for Trusts

9 February 2026 – In an effort to increase the compliance levels of trusts, SARS has issued final demands to trusts who did not submit an annual tax return for the 2024 and 2025 years of assessment. In terms of section 210(2) of the Tax Administration Act, SARS will shortly issue the related public notice for the imposition of administrative non-compliance penalties for trusts. It is important that those in receipt of such final demands as referred to above, take steps to correct the non-filing of the annual income tax returns within the period before the administrative penalties will be raised. SARS notes that, subsequent to the issuance of the final demand, several trusts have already taken steps towards improving their tax compliance. SARS supports and appreciates these efforts.

It is reiterated that all trusts, whether economically active or passive, are required to submit annual income tax returns in accordance with the requirements set out in the public notice. This obligation is an operation of law and is applicable to every registered resident trust (without exception) and certain qualifying non-resident trusts.

SARS emphasises that the responsibility for obtaining, maintaining, and updating accurate trust information rests exclusively with the trustees. This includes the initiation of de-registration processes for trusts that meet the applicable criteria. The trustees must undertake these actions for compliance with statutory requirements and adherence to proper governance practices. This will assist SARS to ensure that the trust tax register is up to date.

Trustees bear sole responsibility for ensuring that all trust information reflected on the SARS Registration, Amendments and Verification (RAV) system is up to date and properly maintained.

Legal Counsel – Interpretation and Rulings – Binding Private Rulings 421–440

6 February 2026 – Income Tax Act, 1962

- Binding Private Ruling 424 – Interest incurred on loan funding used to redeem preference shares and settle dividends

Updated: SARS Digital platform upgrades on 7 February 2026

5 February 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Saturday, 7 February 2026 from 05h00 to 07h00.

Saturday, 7 February 2026, from 18h00 to 21h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Arrival and exit management functions will be available at land border posts for declarations and manifests.

Media advisory: President Ramaphosa undertakes a visit to the SARS National Command Centre

04 February 2026 – President Cyril Ramaphosa will on Thursday, 05 February 2026, undertake a visit to the South African Revenue Service (SARS) National Command Centre in Brooklyn, Pretoria.

The visit forms part of a broader engagement with key government institutions, including the Ministry of Finance and National Treasury, aimed at demonstrating SARS’ progress and showcasing its modernisation initiatives.

SARS was established in terms of the South African Revenue Service Act, 1997 (Act No. 34 of 1997) to function as an autonomous agency responsible for administering South Africa’s tax system and customs service.

During the visit, the President will participate in a walkabout of exhibitions showcasing the work of various SARS business units, including Customs, Taxpayer Engagement, and the Modernisation and Innovation Hub.

The President will be briefed on the operations and ongoing modernisation of the National Command Centre, which is designed to monitor tax compliance, revenue collection, and key operational metrics in real time.

The President will also deliver a keynote address and interact with SARS staff members.

The Visit will take place as follows:

Date: Thursday, 05 February 2026

Time: 10h30

Live stream: https://youtu.be/kKM36T8A8uM

Note to media: Due to space limitations, a media pool is in place for the visit. The keynote address will be live streamed on all Presidency and SARS social media platforms.

For further information, contact [email protected].

Tax directives: interface specification version 6.902

4 February 2026 – The South African Revenue Service (SARS) has issued an updated version 6.902 of the interface specification IBIR-006, due to certain errors that were identified.

These included:

- The maximum record length (increase from 5000 to 6000 characters)

- The number of occurrences of the values of the amounts pertaining to Two Pot transfers, when transferring before retirement on Form A&D (decrease from 4 to 1).

Trade testing dates remain as communicated. This commences on 09 February 2026 and will run until 12 March 2026.

The final software implementation is planned for April 2026.

Legal Counsel – Secondary Legislation – Rule Amendments 2026

3 February 2026 – Customs and Excise Act, 1964: Publication of rules amendments notice R7066, as published in Government Gazette 54060 of 2 February 2026:

- Correction Notice: Government Notice No. R. 7033 of Government Gazette No. 54025 dated 28 January 2026 is hereby corrected by the deletion of the reference to form “DA 199.04C Calculation of the volume assembly localisation allowance in respect of electric vehicles produced and ready for sale for the SACU market this quarter”

Customs Weekly List of Unentered Goods now available

2 February 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Legal Counsel – Secondary Legislation – Proclamations

30 January 2026 – South African Revenue Service Act, 1997

Media Release: Trade Statistics for December 2025

30 January 2026 – South Africa recorded a preliminary trade balance surplus of R23.2 billion in December 2025. This surplus was attributable to exports of R164.3 billion and imports of R141.1 billion, inclusive of trade with Botswana, Eswatini, Lesotho and Namibia (BELN).

See the full Media Release here.

Or visit the Trade Statistics webpage.

Reminder: Voluntary Disclosure Programme (VDP) Awareness Campaign Webinar on 2 February 2026

29 January 2026 – SARS invites you to participate in an informative webinar on the Voluntary Disclosure Programme (VDP). This session is part of SARS’s ongoing commitment to providing clarity on tax obligations and supporting voluntary compliance.

What You Will Gain:

- Legislative Insights: Understand the legislation governing the VDP, including qualifying criteria and the application process.

- Benefits of Disclosure: Learn about the advantages of voluntary disclosure, such as increased certainty and potential relief from penalties.

- Application Guidance: Receive step-by-step instructions on submitting a high-quality VDP application using eFiling, completing the VDP01 form and discovering where to access official resources.

- Interactive Q&A: Post questions to address common challenges, including “non-voluntary” triggers, similar defaults, and full and complete requirements based on our observations and feedback from previous professional body engagements.

Webinar Details:

- Theme: Let’s work together to regularise your tax matters – SARS is here to guide you every step of the way.

- Date: Monday, 2 February 2026

- Time: 10:00 – 12:00

- Platforms: Zoom and YouTube

How to Register:

- Register in advance via Zoom: https://sars-gov-za.zoom.us/webinar/register/WN_FkgcsDeATpOCcwbXquuLIg

- Meeting ID: 969 1545 2907

- Passcode: 533752

- Or join us live on YouTube: https://youtube.com/live/AxabPNTW1Yk?feature=share

Upon registration, you will receive a confirmation email with instructions on how to access the webinar.

We look forward to your participation as we work together to promote voluntary tax compliance.

Legal Counsel – Secondary Legislation – Rule Amendments 2026

28 January 2026 – Customs and Excise Act, 1964: Publication of rules amendments notice R7033, as published in Government Gazette 54025 of 28 January 2026:

- Amendment to the rules under section 120 – by the substitution of the Automotive Production and Development Programme (APDP) quarterly account (DAR266)

-

- DA199 – Customs account for registrants for the purpose of rebate item 317.04

- DA199.00 – The amount on the production rebate certificates utilised this quarter

- DA199.01 – Calculation of “the value in terms of note 8.1” to rebate item 317.04

- DA199.02 – Calculation of the volume assembly localisation allowance originally allocated to motor vehicles at the time of production and ready for sale exported this quarter

- DA199.03 – Calculation of the volume assembly localisation allowance to be utilised for this quarter and the excess volume assembly localisation allowance to be carried forward as an opening balance to the next quarter

- DA199.04A – Calculation of the volume assembly localisation allowance in respect of specified motor vehicles produced and ready for sale for the SACU market this quarter

- DA199.04B – Calculation of the volume assembly localisation allowance in respect of specified motor vehicles produced and exported outside the SACU this quarter

- DA199.10 – Determining the value for the calculation of customs duty and additional VAT on original equipment components imported by the registrant

- DA199.11 – The value for customs duty purposes of imported original equipment components and EV batteries cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 this quarter

- DA199.12 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 in unopened containers or unit load devices at the end of this quarter

- DA199.13 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 used in the manufacture of original equipment components and supplied to other registrants this quarter

- DA199.14 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 used in the manufacture of original equipment components exported this quarter

- DA199.15 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 returned to the overseas suppliers this quarter

- DA199.16 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 transferred to parts and accessories this quarter

- DA199.17 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 used in the manufacture of specified motor vehicles exported this quarter

- DA199.18 – The value for customs duty purposes of imported original equipment components cleared under procedure code ‘processing for home use’ under Chapter 98 of Schedule No. 1 destroyed under customs supervision this quarter

- DA199.19 – The value for customs duty purposes of EV batteries cleared under procedure code ‘processing for home use under Chapter 98 of Schedule No. 1 used in the manufacture of specified motor vehicles for the SACU domestic market this quarter

- DA199.20 – Determining the value for the calculation of the customs duty and additional VAT on original equipment components received by the registrant

- DA199.21 – The imported component value of original equipment components and EV batteries received from any person in SACU during previous quarter

- DA199.22 – The imported component value of original equipment components received from any person in SACU used in the manufacture of original equipment components and exported during the current quarter

- DA199.23 – The imported component value of original equipment components received from any person in SACU used in the manufacture of specified motor vehicles and exported during the current quarter

- DA199.24 – The imported component value of original equipment received from any person in SACU transferred to parts and accessories during the current quarter

- DA199.25 – The imported component value of original equipment components received from any person in SACU destroyed under customs supervision during the current quarter

- DA199.26 – The imported component value of EV batteries received from any person in SACU and used in the manufacture of specified motor vehicles for the SACU domestic market during the current quarter

- DA199.A – Amended customs account for registrants for the purpose of rebate item 317.04

Mpumalanga Mobile Tax Unit Schedules for February and March 2026

28 January 2026 – The Mpumalanga mobile tax unit schedules for February and March 2026 are now available.

SARS Digital platform upgrades on 30 to 31 January 2026

28 January 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Friday, 30 January 2026 from 18h00 to 22h00

Saturday, 31 January 2026 from 20h00 to 23h59

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Arrival and exit management functions will be available at land border posts for declarations and manifests.

Customs Weekly List of Unentered Goods now available

26 January 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

See the latest Customs Weekly List of Unentered Goods here.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

23 January 2026 – Customs and Excise Act, 1964: Publication details for tariff amendments notices R7018, and R7019, as published in Government Gazette 53984 of 23 January 2026, are now available.

Legal Counsel – Secondary Legislation – Tariff Amendments 2026

22 January 2026 – Customs and Excise Act, 1964: The tariff amendments notices, scheduled for publication in the Government Gazette, relate to the following amendments:

With effect from 23 January 2026 up to and including 22 July 2026

- Imposition of provisional payments in relation to anti-dumping duties against the alleged dumping of 3 mm, 4 mm, 5 mm and 6mm clear float glass classifiable under tariff subheadings 7005.29.17, 7005.29.23, 7005.29.25, and 7005.29.35, originating in or imported from Tanzania (ITAC Report No. 762)

With effect from 23 January 2026

- Amendment to Part 1 of Schedule No. 1, by the deletion of tariff subheadings 0307.39.20, 0307.39.30, and 0307.39.40 and the insertion of tariff subheadings 0307.32.20, 0307.32.30, and 0307.32.40, in order to provide for frozen mussels

Publication details will be made available later