Legal Counsel – Secondary Legislation – Tariff Amendments 2026

9 July 2026 – Customs and Excise Act, 1964: The tariff amendments notice, scheduled for publication in the Government Gazette, relates to the following:

Up to and including 9 January 2027

- Imposition of provisional payment in the form of anti-dumping duty against the alleged dumping of ceramic and porcelain wall and floor tiles, excluding finishing ceramics, mosaic cubes and the like classifiable in tariff subheadings 6904.90, 6907.21, 6907.22 and 6907.40 originating in or imported from the Republic of India (India), the Republic of Mozambique (Mozambique), the Republic of Zambia (Zambia) and the Republic of Zimbabwe (Zimbabwe) (ITAC Report 782)

Publication details will be made available later

SARS Digital platform upgrades on 9 July 2026

9 July 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Thursday, 09 July 2026 from 21h30 to 23h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Updated e@syFile™ Employer version 8.0.1_338

7 July 2026 – The e@syFile™ Employer version 8.0.1_338 release notes specify the following changes:

- Enhancement made to Bulk Payment function to include bulk payments for ITA88’s.

See more detail in the release notes.

Legal Counsel – Dispute Resolution & Judgments – Tax Court 2028-2026

7 July 2026 – Income Tax Act, 1962; Tax Administration Act, 2011

Whether the GAAR applies to the composite transaction. Two further questions arise: 1) The first is the appellants’ preliminary objection to the Commissioner’s pleading of the avoidance arrangement. 2) The second is the fate of the penalties and interest.

Legal Counsel – Secondary Legislation – Rules Amendments 2026

7 July 2026 – Customs and Excise Act, 1964: Publication details for rules amendments notice R.7656, as published in Government Gazette 54939 of 3 July 2026, relating to invoice data and customs worksheet data (with effect from 3 July 2026), are now available.

Customs Weekly List of Unentered Goods now available

7 July 2026 – The state provides state warehouses for the safekeeping of goods. These are managed by Customs. The purpose of this list of unentered goods is to notify the importer, exporter and any other person that has interest in the goods that the goods have been taken up into the State warehouse and if they remain unentered they will be disposed in accordance with the provisions of the Customs & Excise Act.

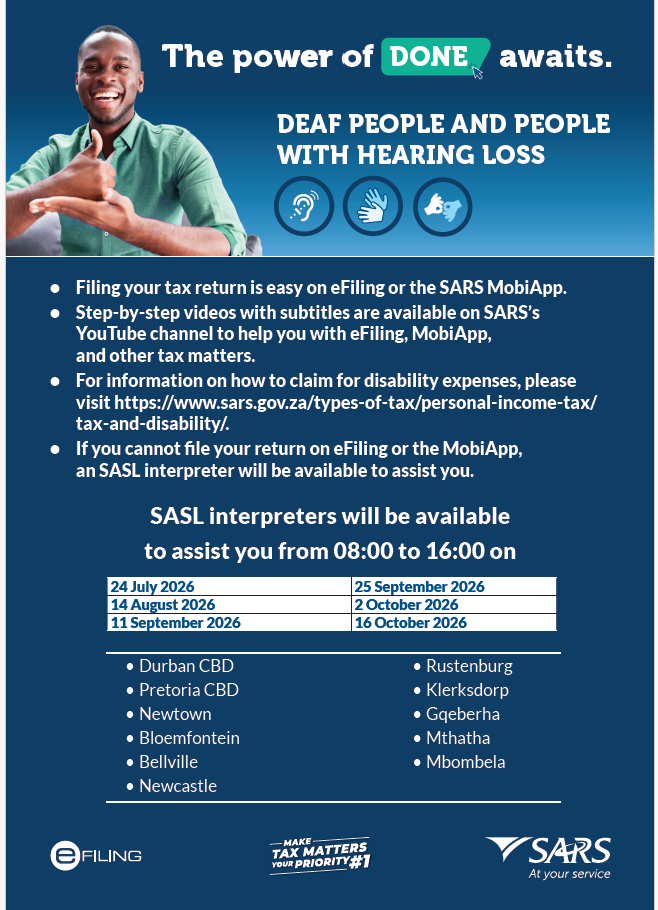

South African Sign Language Interpreters available at SARS Service Centres

7 July 2026 – South African Sign Language (SASL) Interpreters will be available to assist you from 08:00 to 16:00 on the following dates:

- 24 July 2026

- 25 September 2026

- 14 August 2026

- 2 October 2026

- 11 September 2026

- 16 October 2026

At the following Service Centres:

- Durban CBD

- Pretoria CBD

- Newtown

- Bloemfontein

- Bellville

- Newcastle

- Rustenburg

- Klerksdorp

- Gqeberha

- Mthatha

- Mbombela

For more information, see our Tax & Disability webpage.

To see our Service Centres’ locations, click here.

Legal Counsel – Dispute Resolution & Judgments – Supreme Court of Appeal 2028-2026

6 July 2026 – Customs and Excise Act, 1964, and Promotion of Administrative Justice Act, 2000

Customs and Excise Act 91 of 1964 – Statutory obligations of clearing agents appointed under section 64B – proof required to acquit goods entered for removal in bond or in transit – Commissioner’s assessment of proof of export – liability for duties and levies – separate discretion under section 88(2) to demand an amount in lieu of forfeiture – distinction between procedural rationality and procedural fairness – review under the principle of legality and section 6(2)(f)(ii) of the Promotion of Administrative Justice Act 3 of 2000 – remittal to the Commissioner.

Legal Counsel – Secondary Legislation – Public Notices

3 July 2026 – Tax Administration Act, 2011: Public Notices in Government Gazette 54941 of 3 July 2026:

- Notice 7664 specifying the addresses at which any notice under section 11(4) of the Act, or any processes by which legal proceedings are instituted against the Commissioner must be served

- Notice 7663, prescribing the addresses at which a document or notice must be delivered, or a request must be made for purposes of rule 2(1)(c)(ii) and rule 3(1) read together with rule 2(1)(c)(iii) of the rules

Beware of scams

2 July 2026 – SARS will never request passwords, one-time pins (OTPs), banking PINs, or eFiling login credentials through email, SMS, social media, or telephone. Taxpayers must use only official SARS channels and verify the credentials of any tax practitioner before sharing personal information.

See examples here of the latest SARS scams. If in doubt, please email [email protected].

SARS Digital platform upgrades on 3 July 2026

2 July 2026 – Achieving our Vision of a smart, modern SARS with unquestionable integrity that is trusted and admired is of paramount importance. Pivotal to the delivery of our vision are our digital platforms and technology infrastructure. To provide clarity and certainty, make it easy for taxpayers and traders to comply with their obligations and building public trust and confidence, our technology assets must demonstrate the highest levels of availability, robustness and security.

In accordance with our Vision and Strategic Objectives, which include modernising our systems to provide Digital and Streamlined online services, we are hard at work ensuring that our digital platforms and technology infrastructure are available, robust and secure, by performing regular upgrades, enhancements and maintenance.

Considering the above, SARS Digital platform maintenance is scheduled for:

Friday, 03 July 2026 from 18h00 to 22h00.

During this time, you may experience intermittent service interruption on our eFiling, Tax and Customs Digital Platforms.

Media release: SARS unveils smarter, simpler, more secure Filing Season experience for Taxpayers

2 July 2026 – South Africa’s 2026 Filing Season officially opened with the South African Revenue Service (SARS) rolling out a range of digital enhancements to the taxpayer experience, making tax compliance simpler, faster, and more secure for millions of taxpayers. As at the end of 1 July 2026, more than 1.9 million taxpayers were auto-assessed with about R8 billion in refunds paid out within 72 hours.

The improvements form part of SARS’s commitment to excellent service and its vision to build a smart, modern SARS with unquestionable integrity. SARS aims to give clarity and certainty, and to make it easy for taxpayers to comply with their obligations.

Filing Season 2026 builds on the success of Auto Assessment and SARS’s significant investment in technology, artificial intelligence, data integration, and digital service delivery. Taxpayers will benefit from a more streamlined filing process, expanded self-service capabilities, enhanced security features, and improved digital channels, designed to reduce effort, improve accuracy, and minimise the need to visit SARS branches.

“Our goal is to make compliance effortless for honest taxpayers”, said Dr Johnstone Makhubu, SARS Commissioner. “Every enhancement introduced this Filing Season is designed to improve service, reduce complexity, and give taxpayers greater confidence when engaging with SARS. We want taxpayers to spend less time dealing with administration and more time benefiting from our modern digital services.”

Key enhancements introduced for Filing Season 2026:

- More accurate Auto Assessments driven by expanded third-party data sources.

- Expanded digital self-service capabilities through eFiling, SARS MobiApp, and SARS Online Query System.

- Enhanced profile security through biometric authentication, two-factor authentication, and device-level security controls.

- Expanded support through the Lwazi AI virtual assistant.

- The ability to upload supporting documents through WhatsApp.

- Delivery of Notices of Assessment and Statements of Account through WhatsApp and other digital channels.

- Improved integration of taxpayer information and enhanced pre-population of returns.

- SARS has created necessary capacity to cater for increased volumes of taxpayers interacting with it through the various channels.

These enhancements form part of SARS’s strategy to create a seamless end-to-end filing experience that covers every stage of the taxpayer journey, from registration and Auto Assessment, to eFiling, verification, assessment outcomes, and refunds. The improvements are expected to reduce administrative burdens, shorten turnaround times, and improve taxpayer satisfaction.

SARS expects more than six million taxpayers to receive Auto Assessments this year. By using information from employers, banks, medical schemes, retirement funds, and other third-party providers, SARS can pre-populate returns and significantly reduce the information taxpayers need to capture themselves.

Taxpayers selected for Auto Assessment between 1 and 12 July 2026 should not rush to SARS Service Centres. Instead, they should wait for official SARS communication and review their assessments through eFiling, the SARS MobiApp, or other authorised digital channels.

“Through innovation, data-driven processes, and digital transformation, SARS is creating a filing experience that is simpler, faster, and more convenient”, the Commissioner said. “The objective is clear: to make it easy for taxpayers to comply while improving service, creating certainty, and fostering trust in the tax system.”

Although SARS has strengthened its digital services and security controls, the Commissioner cautioned taxpayers to remain vigilant against scams, phishing attacks, fake refund schemes, and unregistered tax practitioners who frequently target taxpayers during Filing Season.

SARS will never request passwords, one-time pins (OTPs), banking PINs, or eFiling login credentials through email, SMS, social media, or telephone. Taxpayers must use only official SARS channels and verify the credentials of any tax practitioner before sharing personal information.

“Taxpayers should be cautious of anyone who guarantees a refund or requests sensitive information without proper verification. Protecting personal information remains a shared responsibility between SARS and taxpayers”, Commissioner Makhubu warned.

He added: “Filing Season 2026 demonstrates the progress SARS continues to make in modernising tax administration and improving the taxpayer experience. Through enhanced Auto Assessments, stronger digital platforms, improved security, expanded self-service channels, and innovative solutions such as WhatsApp functionality, we are making compliance easier than ever before.”

“Our message to taxpayers is simple: make use of these digital services, trust the official SARS channels, and let the technology work for you. The easier we make compliance, the stronger our tax ecosystem becomes for everyone.”

Please direct media enquiries to [email protected].

Customs & Excise – Revision of sample documentation for commercial goods

1 July 2026 – The sample documentation for commercial goods has been revised. The updates focused on aligning policy provisions with the Customs and Excise Act, 1964, and improving clarity where existing wording was unclear. The revision has clarified the circumstances where the owner is liable for analysis costs and has refined the provisions for deferred payment of duty.

Mpumalanga Mobile Tax Unit Schedules for July and August 2026

1 July 2026 – The Mpumalanga mobile tax unit schedules for July and August 2026 are now available.

Legal Counsel – Preparation of Legislation – Draft Documents for Public Comment

1 July 2026 – Income Tax Act, 1962

Due date for comment: 31 August 2026

Legal Counsel – Dispute Resolution & Judgments – High Court 2028-2026

1 July 2026 – Income Tax Act, 1962, and Tax Administration Act, 2011

Insurance Law: Traditional insurance contract – spreading of risk – economic theory of insurance – simulated insurance contract – self structured insurance contract not insurance at all – premium deductions not allowed in terms of section 11(a) of the Income Tax Act 58 of 1962 – Period of limitation for assessment for issuance of assessment and the non-barring of assessment in terms of section 99(1)(a) and 99(2)(a) respectively of the Tax Administration Act 28 of 2011 – understatement penalties imposition confirmed – appeal upheld.

Legal Counsel – Secondary Legislation – Public Notices

1 July 2026 – Tax Administration Act, 2011: Notice 7645 published in terms of section 187(2), published in Government Gazette 54921 of 30 June 2026, prescribing the date from which the method of calculation interest in terms of this section will apply to interest imposed under section 7 of the Global Minimum Tax Act, 2024, read with Chapter 12 of the Tax Administration Act.

Required Online Traveller Declarations from 1 July 2026

1 July 2026 – From 1 July 2026, all travellers entering or leaving South Africa through air, land, sea and rail ports of entry are required to submit an online traveller declaration before travelling. The implementation adopts a whole-of-government approach to strengthen data integration and facilitate Inter-agency risk management, thereby enhancing the monitoring, analysis, and reporting of cross-border activities. The South African Traveller Management System (SATMS) enables travellers to meet their legal obligation to declare goods in their possession, including currency through convenient digital channels such as the SARS Customs Online Traveller Declaration Portal, the SATMS mobile application, and Scan-to-Declare QR codes. Through convenience and digital accessibility, SATMS promotes voluntary compliance to simplify the declaration process and enhance the overall traveller border experience.

Travellers will not be denied entry into or departure from South Africa solely because they have not completed a declaration before arriving at a port of entry. SARS Customs officials, supported by self-service declaration terminals, will be available to assist travellers who were unable to submit their declarations before travelling. SARS encourages all travellers to familiarise themselves with the new requirements and complete their declarations in advance to ensure a seamless and efficient travel experience. For more information and clarity, travellers can access our FAQs for the Required Online Traveller Declarations from 1 July 2026 webpage.

Visit the Customs Online Declaration webpage.

Go directly to the online Traveller Management System tool.

Watch our easy step-by-step video on how to declare.

Legal Counsel – Interpretation and Rulings – Binding General Rulings 61-80

30 June 2026 – Value-Added Tax Act, 1991

- Binding General Ruling 75 – Value-Added Tax Treatment of Ambulance Services

Legal Counsel – Interpretation and Rulings – Practice Notes

30 June 2026 – Value-Added Tax Act, 1991: Notice is hereby given that VAT Practice Note 7 of 1992 – Passenger transport will be withdrawn effective 1 January 2027